Gold. One of the many topics that make me despair nowadays. Public opinion on gold differs a lot from that of economists. And guess who is wrong. It’s not the experts. Word on the street has it that gold is a very valuable investment. It appreciates over time, leading to large capital gains. Furthermore, it is seen as a valuable hedge in times of crisis. Last but not least, in some kind of doomsday scenario it is believed that gold would be a valuable asset to hold on to if the economic system collapses and fiat money becomes worthless. Unfortunately, none of these claims are true.

A paper by Robert Barro and Sanyaj Misra (2013) shows that gold returns in between 1836 to 2011 have averaged only about 1.1% in real terms. This is comparable to the annual real return of 1% of 3 months Treasury bills. So historically, gold only has a comparable performance to short-term government bonds, a safe asset that has an extremely low yield. Compare that to the average stock market return in real terms since 1870, which is close to 7% per year.

One should also note that gold has an extremely high volatility, much larger than that of bonds, making it a very risky investment. The standard deviation of annual gold returns was close to 14%, almost as high as the 17% standard deviation of the U.S. stock market. Gold is thus a low-return but high-volatility asset. Its extreme riskiness combined with its low relative payoffs thus make it a very poor investment indeed.

There would be one rationale to include substantial amounts of gold in one’s investment portfolio despite its poor performance. That is if gold serves as a hedge. Its low returns would be justified if it has a negative correlation to other assets in times of economic hardship. This is indeed what many people believe. In times of crisis when stocks go down gold prices will go up. However, the evidence is not supportive of this hypothesis. Barro and Misra identify 56 macroeconomic disasters for 19 countries in between 1880 and 2011. A macroeconomic disaster is defined as a decline of GDP by more than 10%. During this period the real price of gold increased by about 1.5% per year. During times of crisis, the performance of gold was only marginally better, namely 2.1% per year. Its annual standard deviation of 22% during that time period makes it an extremely risky investment. Furthermore, in more than half of the macroeconomic distasters identified the real price of gold actually fell. So gold is a low-return and high-volatiltiy investment that does not even provide a good hedge in times of crisis when other assets such as stocks or housing perform badly.

So why is gold still seen by many as such a good investment. My best guess is that there is something mysterious about gold. It is something real and considered to be valuable in all scenarios. Furthermore, some people still have a deep distrust of fiat money and favor a return to the gold standard, never mind that the gold standard actually would not lead to price stability. To the contrary, under a system where money is fixed to the price of gold, inflation would actually behave erratically. Domestic prices would depend on the international price of gold, which is determined by global demand and supply and can fluctuate wildly. Indeed, fiat money has led to high price stability in advanced economies over the last 3 decades. In fact, Central Banks nowadays arguably care far too much about low inflation and do not care enough about achieving adequate stability in nominal GDP growth and full employment.

There are only two equilibria in which fiat money like the dollar could become worthless, neither of them being very pleasant, and gold wouldn’t provide any meaningful relief in either case. The first one would be a full-blown hyperinflation. The second one would be even worse, a total collapse of the financial and economic system. But in both cases, gold would surely not replace fiat money simply because it is not a very convenient medium of exchange. During periods of hyperinflation or in the unlikely case that the entire economic system collapses, people would resort to barter trade. But you simply do not require gold in such a scenario. What you really need then is a lot of canned food, some guns and ammo as well a nice, hidden concrete bunker in your garden. Not that such an outcome will ever occur in our lifetime, hopefully. Financial markets basically attach a zero probability to the hyperinflation scenario. In fact, financial markets believe that Central Banks in many advanced economies will continue to undershoot their inflation target for many years to come, maybe even decades.

The basic point is that even in such an adverse state of nature gold would not be such a valuable asset to hold on to as is commonly believed. Money exchanges would be replaced by barter trade and some commodity, most likely food, might assume the role of money. In Ancient Egypt, for example, grain had a monetary function.

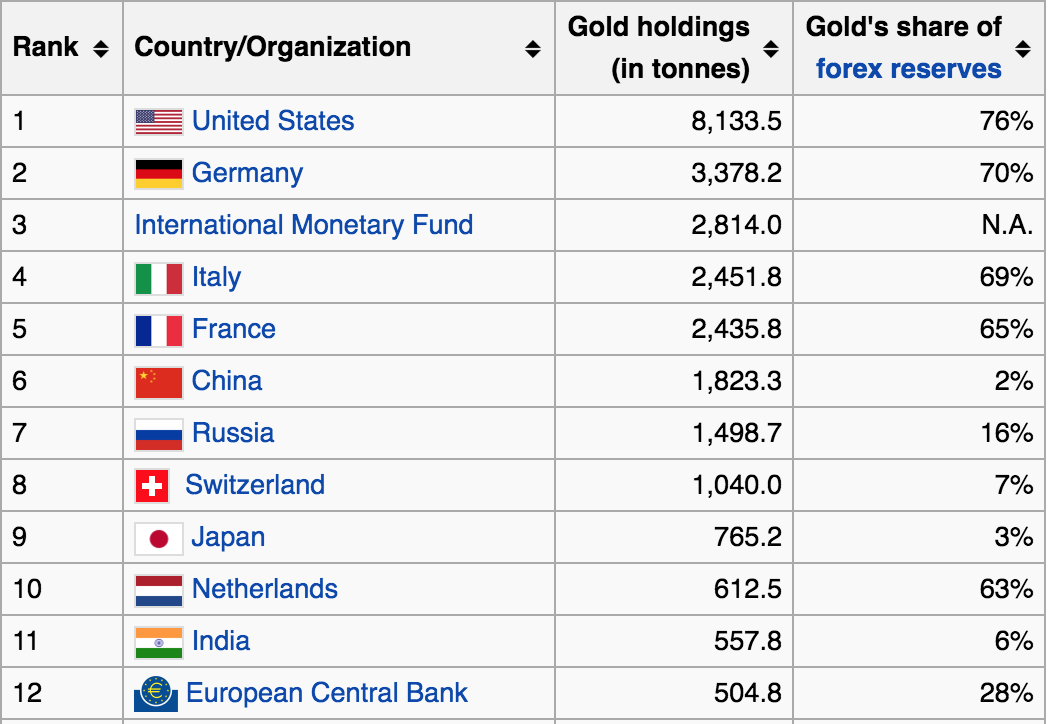

Given that gold is not a productive asset and that it is also an underperforming investment, it might seem somehwat surprising that many governments still hold on to large gold reserves, despite the fact that today’s monetary system does not need to be backed up by any commodity at all. Germany’s gold reserves are with about 3380 tons the second highest in the world (see graph below). In some sense it is actually not surprising that Germany trumps other countries again in this regard. After all, Germany is a country where macroeconomic illiteracy seems to be a key qualification to become a top public official. As a case in point, Germans have some weird sensation of pride about the fact that, instead of investing at home in infrastructure and education, the country is currently exporting capital in the amount of more than 300 billion USD net on an annual basis. The German public also does not regard with dismay that our current government is extremely dogmatic about fiscal expenditures. Instead of taking advantage of the fact that the German state can issue safe assets and borrow money at negative interest rates for up to 10 years, Germany’s finance minister Schäuble insists on runnung budget surpluses. Investments into infrastructure and education have a high social return and would basically pay for themselves in the current economic environment. Even a larger fiscal investment program, let’s say an additional 0.5% of GDP each year over the next 5 years, would only marginally increase the long-term debt-to-GDP ratio, if it does so at all. But these arguments are marginalized in the German public debate.

When it comes to the country’s gold reserves, Germany seems to be equally dogmatic. For historic reasons, a large part of the reserves are stored in London and the U.S, a relic from the Cold War. If the Soviets ever invaded Germany, its population would be screwed, but at least the gold would be safe across the sea.

At current market prices, a ton being valued at about 35 million USD, Germany’s gold reserves of 3380 tons is worth roughly 118 billion USD. Note that the value of the gold reserves went down by an astounding 50 billion dollars since 2012 when gold was valued at about 1800 USD per ounce (the current price is roughly 1230 USD per ounce).

So here is my question. Why not sell all this shitty gold which is of no goddamn use to anyone? It did not benefit the last generation, it doesn’t benefit the current generation, and it will not benefit the next generation if it is simply sititng in some vaults in London and New York. It is an entirely unproductive asset with low rates of return. Under a system of fiat money, gold is not needed. The entire point of fiat money is that its supply is elastic and that it does not need to be backed up by an unproductive commodity. Elasticity is key in times of crisis when Central Banks need to inject additional money into the economy in order to stabilize nominal spending, at least that’s the idea. In practice, Central Banks have spectacularly failed to do so over the last few years.

So here are two suggestions how the proceeds from the gold sale could be used. First, Germany could sell gold reserves of about 100 billion USD over the course of let’s say 5 years and invest the money into education and infrastructure, which have a high social return. According to institutions like the IMF and the World Bank, there is a substantial deficit in infrastructure spending worldwide. Part of Germany’s infrastructure is crumbling and would desperately need a much required upgrade. Spending on education is relatively low compared to other OECD countries. Increased investment in education and infrastructure would lead to higher economic growth and thus also higher tax receipts for the German state. The proceeds from the gold sales could thus be used for these two purposes. This proposal would also have the benefit of not increasing the debt to GDP ratio, even though this consideration is mute in the current environment of negative interest rates.

An alternative proposal could involve setting up a Souvereign Wealth Fund à la Norway. The German state could sell gold reserves worth 100 billion USD and invest the proceeds in global equities. As stated before, returns on such an investment fund would be in the ballpark of 5-7% on an annual basis. More than 3% of the return is due to dividend yields, meaning an annual payout of about 3 billion USD. The Souvereign Wealth Fund would grow over time and the payouts could be used as an additional funding for education and infrastructure, for example. This obviously only makes sense if the state does not cut its normal funding by an equivalent amount.

Do I think that any two of those proposals even have a minimal chance of being adopted at some point in time? No, I don’t. As I said earlier, politicians and citizens have a rather dogmatic view when it comes to gold. No statistic reveals this better than the fact that private gold holdings of German households actually far exceeds government holdings. German households now hoard abot 8700 tons of gold, having increasing their holdings by 500 tons since 2014, meaning that German households have lost a tremendous amount of money over the last couple of years due the enormous decline in the gold price. Pragmatic economic policies consistently seem to be rejected by the German governement and the German public at large, the eurozone crisis being probably the best example. As a matter of logic, long-lasting economic stagnation in Southern Europe simply cannot be in Germany’s interest. Regardless, German policy makers have consistently called for more contractionary policies being imposed on the rest of Europe, which exactly produce said outcome of economic stagnation. It is thus reasonable to assume that the German government will continue to hold on to its enormous gold reserves basically forever with no economic benefit to anybody, but regardless such a policy is backed up by the German public at large.

Let me thus end this post with a quote from John Maynard Keynes:

“A preference for a tangible gold currency is no longer more than a relic of a time when Governments were less trustworthy in these matters than they are now…”.

UPDATE:

I wrote this post in the summer, but didn’t quite finish it. Recent events, of course, have only corroborated the fact that gold is mainly driven by irrational excuberrance, or “Keynesian animal spirits”, if you will. Before the election outcome, gold was perceived as a hedge against a Trump victory and the correlation between the price of gold and the probability of him winning was positive despite the fact that gold would not provide a good hedge, as argued above. As soon as a Trump victory was certain the day after, gold prices actually plummeted. This seems to be driven by the fact that markets think Trump’s infrastructure spending will be mildly inflationary, and gold is simply a terrible hedge against inflation.

References:

Barro, Robert J., and Sanjay P. Misra. Gold returns. No. w18759. National Bureau of Economic Research, 2013.

Keynes, John Maynard. Indian currency and finance. Macmillan and Company, 1913.

A paper by Robert Barro and Sanyaj Misra (2013) shows that gold returns in between 1836 to 2011 have averaged only about 1.1% in real terms. This is comparable to the annual real return of 1% of 3 months Treasury bills. So historically, gold only has a comparable performance to short-term government bonds, a safe asset that has an extremely low yield. Compare that to the average stock market return in real terms since 1870, which is close to 7% per year.

One should also note that gold has an extremely high volatility, much larger than that of bonds, making it a very risky investment. The standard deviation of annual gold returns was close to 14%, almost as high as the 17% standard deviation of the U.S. stock market. Gold is thus a low-return but high-volatility asset. Its extreme riskiness combined with its low relative payoffs thus make it a very poor investment indeed.

There would be one rationale to include substantial amounts of gold in one’s investment portfolio despite its poor performance. That is if gold serves as a hedge. Its low returns would be justified if it has a negative correlation to other assets in times of economic hardship. This is indeed what many people believe. In times of crisis when stocks go down gold prices will go up. However, the evidence is not supportive of this hypothesis. Barro and Misra identify 56 macroeconomic disasters for 19 countries in between 1880 and 2011. A macroeconomic disaster is defined as a decline of GDP by more than 10%. During this period the real price of gold increased by about 1.5% per year. During times of crisis, the performance of gold was only marginally better, namely 2.1% per year. Its annual standard deviation of 22% during that time period makes it an extremely risky investment. Furthermore, in more than half of the macroeconomic distasters identified the real price of gold actually fell. So gold is a low-return and high-volatiltiy investment that does not even provide a good hedge in times of crisis when other assets such as stocks or housing perform badly.

So why is gold still seen by many as such a good investment. My best guess is that there is something mysterious about gold. It is something real and considered to be valuable in all scenarios. Furthermore, some people still have a deep distrust of fiat money and favor a return to the gold standard, never mind that the gold standard actually would not lead to price stability. To the contrary, under a system where money is fixed to the price of gold, inflation would actually behave erratically. Domestic prices would depend on the international price of gold, which is determined by global demand and supply and can fluctuate wildly. Indeed, fiat money has led to high price stability in advanced economies over the last 3 decades. In fact, Central Banks nowadays arguably care far too much about low inflation and do not care enough about achieving adequate stability in nominal GDP growth and full employment.

There are only two equilibria in which fiat money like the dollar could become worthless, neither of them being very pleasant, and gold wouldn’t provide any meaningful relief in either case. The first one would be a full-blown hyperinflation. The second one would be even worse, a total collapse of the financial and economic system. But in both cases, gold would surely not replace fiat money simply because it is not a very convenient medium of exchange. During periods of hyperinflation or in the unlikely case that the entire economic system collapses, people would resort to barter trade. But you simply do not require gold in such a scenario. What you really need then is a lot of canned food, some guns and ammo as well a nice, hidden concrete bunker in your garden. Not that such an outcome will ever occur in our lifetime, hopefully. Financial markets basically attach a zero probability to the hyperinflation scenario. In fact, financial markets believe that Central Banks in many advanced economies will continue to undershoot their inflation target for many years to come, maybe even decades.

The basic point is that even in such an adverse state of nature gold would not be such a valuable asset to hold on to as is commonly believed. Money exchanges would be replaced by barter trade and some commodity, most likely food, might assume the role of money. In Ancient Egypt, for example, grain had a monetary function.

Given that gold is not a productive asset and that it is also an underperforming investment, it might seem somehwat surprising that many governments still hold on to large gold reserves, despite the fact that today’s monetary system does not need to be backed up by any commodity at all. Germany’s gold reserves are with about 3380 tons the second highest in the world (see graph below). In some sense it is actually not surprising that Germany trumps other countries again in this regard. After all, Germany is a country where macroeconomic illiteracy seems to be a key qualification to become a top public official. As a case in point, Germans have some weird sensation of pride about the fact that, instead of investing at home in infrastructure and education, the country is currently exporting capital in the amount of more than 300 billion USD net on an annual basis. The German public also does not regard with dismay that our current government is extremely dogmatic about fiscal expenditures. Instead of taking advantage of the fact that the German state can issue safe assets and borrow money at negative interest rates for up to 10 years, Germany’s finance minister Schäuble insists on runnung budget surpluses. Investments into infrastructure and education have a high social return and would basically pay for themselves in the current economic environment. Even a larger fiscal investment program, let’s say an additional 0.5% of GDP each year over the next 5 years, would only marginally increase the long-term debt-to-GDP ratio, if it does so at all. But these arguments are marginalized in the German public debate.

When it comes to the country’s gold reserves, Germany seems to be equally dogmatic. For historic reasons, a large part of the reserves are stored in London and the U.S, a relic from the Cold War. If the Soviets ever invaded Germany, its population would be screwed, but at least the gold would be safe across the sea.

At current market prices, a ton being valued at about 35 million USD, Germany’s gold reserves of 3380 tons is worth roughly 118 billion USD. Note that the value of the gold reserves went down by an astounding 50 billion dollars since 2012 when gold was valued at about 1800 USD per ounce (the current price is roughly 1230 USD per ounce).

So here is my question. Why not sell all this shitty gold which is of no goddamn use to anyone? It did not benefit the last generation, it doesn’t benefit the current generation, and it will not benefit the next generation if it is simply sititng in some vaults in London and New York. It is an entirely unproductive asset with low rates of return. Under a system of fiat money, gold is not needed. The entire point of fiat money is that its supply is elastic and that it does not need to be backed up by an unproductive commodity. Elasticity is key in times of crisis when Central Banks need to inject additional money into the economy in order to stabilize nominal spending, at least that’s the idea. In practice, Central Banks have spectacularly failed to do so over the last few years.

So here are two suggestions how the proceeds from the gold sale could be used. First, Germany could sell gold reserves of about 100 billion USD over the course of let’s say 5 years and invest the money into education and infrastructure, which have a high social return. According to institutions like the IMF and the World Bank, there is a substantial deficit in infrastructure spending worldwide. Part of Germany’s infrastructure is crumbling and would desperately need a much required upgrade. Spending on education is relatively low compared to other OECD countries. Increased investment in education and infrastructure would lead to higher economic growth and thus also higher tax receipts for the German state. The proceeds from the gold sales could thus be used for these two purposes. This proposal would also have the benefit of not increasing the debt to GDP ratio, even though this consideration is mute in the current environment of negative interest rates.

An alternative proposal could involve setting up a Souvereign Wealth Fund à la Norway. The German state could sell gold reserves worth 100 billion USD and invest the proceeds in global equities. As stated before, returns on such an investment fund would be in the ballpark of 5-7% on an annual basis. More than 3% of the return is due to dividend yields, meaning an annual payout of about 3 billion USD. The Souvereign Wealth Fund would grow over time and the payouts could be used as an additional funding for education and infrastructure, for example. This obviously only makes sense if the state does not cut its normal funding by an equivalent amount.

Do I think that any two of those proposals even have a minimal chance of being adopted at some point in time? No, I don’t. As I said earlier, politicians and citizens have a rather dogmatic view when it comes to gold. No statistic reveals this better than the fact that private gold holdings of German households actually far exceeds government holdings. German households now hoard abot 8700 tons of gold, having increasing their holdings by 500 tons since 2014, meaning that German households have lost a tremendous amount of money over the last couple of years due the enormous decline in the gold price. Pragmatic economic policies consistently seem to be rejected by the German governement and the German public at large, the eurozone crisis being probably the best example. As a matter of logic, long-lasting economic stagnation in Southern Europe simply cannot be in Germany’s interest. Regardless, German policy makers have consistently called for more contractionary policies being imposed on the rest of Europe, which exactly produce said outcome of economic stagnation. It is thus reasonable to assume that the German government will continue to hold on to its enormous gold reserves basically forever with no economic benefit to anybody, but regardless such a policy is backed up by the German public at large.

Let me thus end this post with a quote from John Maynard Keynes:

“A preference for a tangible gold currency is no longer more than a relic of a time when Governments were less trustworthy in these matters than they are now…”.

UPDATE:

I wrote this post in the summer, but didn’t quite finish it. Recent events, of course, have only corroborated the fact that gold is mainly driven by irrational excuberrance, or “Keynesian animal spirits”, if you will. Before the election outcome, gold was perceived as a hedge against a Trump victory and the correlation between the price of gold and the probability of him winning was positive despite the fact that gold would not provide a good hedge, as argued above. As soon as a Trump victory was certain the day after, gold prices actually plummeted. This seems to be driven by the fact that markets think Trump’s infrastructure spending will be mildly inflationary, and gold is simply a terrible hedge against inflation.

References:

Barro, Robert J., and Sanjay P. Misra. Gold returns. No. w18759. National Bureau of Economic Research, 2013.

Keynes, John Maynard. Indian currency and finance. Macmillan and Company, 1913.

World's major gold holders:

RSS Feed

RSS Feed