So the Fed raised their interest rates yesterday for the third time since the financial crisis. One can argue about whether the U.S. economy has already approached full employment or not. I myself believe that monetary tightening is somewhat premature and that there remains some slack in the labor market. However, the U.S. economy has performed reasonably well over the last year. The rate hike was mostly anticipated by financial markets and was thus priced in. What was somewhat surprising was the financial markets' reaction to the rate hike and the Fed statement.

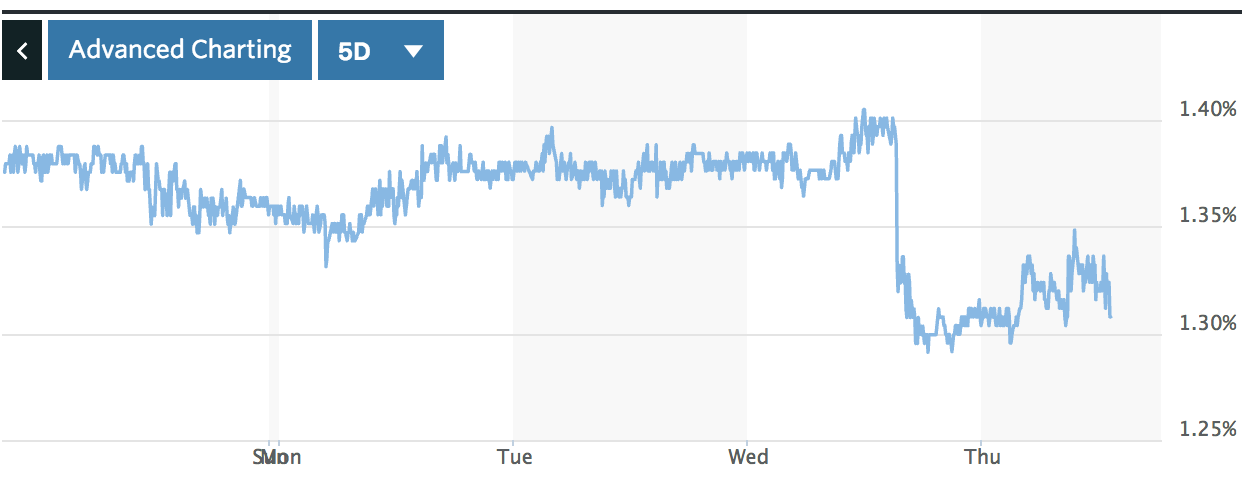

The euro appreciated versus the dollar by almost one percent in the immediate aftermath. U.S. stock markets were up as well. The S&P 500 rose by about half a percent. Finally, 2-year U.S. Treasuries declined by almost 10 basis points. In fact, the entire yield curve shifted down by a bit with long-term bonds (10 years) declining by about 10 basis bonds.

All these indicators thus suggest that monetary policy was eased despite the fact that the Fed hiked interest rates.

The euro appreciated versus the dollar by almost one percent in the immediate aftermath. U.S. stock markets were up as well. The S&P 500 rose by about half a percent. Finally, 2-year U.S. Treasuries declined by almost 10 basis points. In fact, the entire yield curve shifted down by a bit with long-term bonds (10 years) declining by about 10 basis bonds.

All these indicators thus suggest that monetary policy was eased despite the fact that the Fed hiked interest rates.

2 year US Treasury yield, 5-day chart

The answer, of course, lies in the fact that the short-term interest rates in itself is a pretty lousy indicator of monetary policy. Most of the monetary policy action is about expectations and expectations management. Yesterday's Fed statement made it abundantly clear that the 2% inflation target is symmetrical. Since the 2% number is not a ceiling but an average, meaning that inflation is just as likely to be above target as below target. This shows that there is some commitment to not tighten the moment the inflation rate temporarily overshoots the 2% mark. Furthermore, the famous dot-plot indicates that the Fed expects another two rate hikes this year. Again, in so far as as some market participants expected three rate hikes, this still seems to be on the dovish side.

The stance of monetary policy cannot be measured by interest rates. Whether monetary policy is easy or tight depends on where the natural rate of interest rate. Now with the U.S. economy approaching full employment, the natural rate of interest is finally moving up after almost a decade where it supposedly below zero. Monetary policy thus actually becomes easier if the Fed does not increase the overnight rate in tandem with increases in the natural intrest rate.

To sum up, the Fed's rate hike was widely anticipated by financial market participants and was thus priced in. Furthermore, various financial market prices suggest that monetary policy actually became somewhat easier. This is most likely due to a to the fact that the Fed made it abundantly clear that the tightening cycle will be very gradual with about two more rate hikes this year, a pace that financial markets feel very comfortable with.

The stance of monetary policy cannot be measured by interest rates. Whether monetary policy is easy or tight depends on where the natural rate of interest rate. Now with the U.S. economy approaching full employment, the natural rate of interest is finally moving up after almost a decade where it supposedly below zero. Monetary policy thus actually becomes easier if the Fed does not increase the overnight rate in tandem with increases in the natural intrest rate.

To sum up, the Fed's rate hike was widely anticipated by financial market participants and was thus priced in. Furthermore, various financial market prices suggest that monetary policy actually became somewhat easier. This is most likely due to a to the fact that the Fed made it abundantly clear that the tightening cycle will be very gradual with about two more rate hikes this year, a pace that financial markets feel very comfortable with.

RSS Feed

RSS Feed