After being criticized by the US for its policies, the German government demonstrated once more that 6 years into the crisis it still has no clue whatsoever what is going on

(http://www.spiegel.de/international/germany/germany-defends-trade-surplus-after-critical-us-treasury-report-a-931126.html).

So I'll try to explain it. I think that many people will at first not agree with what I am writing here but I hope that by the end of this post I will have made the case for my statement.

I will start with some basic accounting identities. Let’s start with the simple GDP equation for an open economy:

(http://www.spiegel.de/international/germany/germany-defends-trade-surplus-after-critical-us-treasury-report-a-931126.html).

So I'll try to explain it. I think that many people will at first not agree with what I am writing here but I hope that by the end of this post I will have made the case for my statement.

I will start with some basic accounting identities. Let’s start with the simple GDP equation for an open economy:

GDP (Y) is equal to the sum of domestic consumption (C) plus investment (I) plus government expenditures (G) plus exports (X) minus imports (IM).

Obviously, we define the current account CA as exports minus imports.

Obviously, we define the current account CA as exports minus imports.

Similarly, we can define national savings as the remainder of domestic income once domestic consumption and government expenditures are subtracted.

Fooling around with these equations, we get that the current account is actually equal to savings minus investments.

Obviously, in a closed economy there is no trade and savings must be equal to investment.

Looking at an open economy, however, one must realize that a country with a current account (henceforth CA) surplus by definition has higher domestic saving than investment. A deficit country on the other hand has higher domestic investment than savings. This is obviously true because the CA is the mirror image of the capital account. So surplus countries will have capital outflows as residents channel capital (excess savings) abroad, whereas deficit countries experience capital inflows (surplus countries are net creditors while deficit countries are net lenders).

Alternatively, one can say that surplus countries temporarily produce more than they consume whereas deficit countries produce less than they consume.

Now, it should be obvious that the world as whole cannot run a CA surplus or deficit (unless we start interplanetary trade :D). This also means that if there is at least one country running a CA surplus then there must be at least one other country running the corresponding CA deficit.

Alternatively, one can say that surplus countries temporarily produce more than they consume whereas deficit countries produce less than they consume.

Now, it should be obvious that the world as whole cannot run a CA surplus or deficit (unless we start interplanetary trade :D). This also means that if there is at least one country running a CA surplus then there must be at least one other country running the corresponding CA deficit.

Since the outbreak of the global economic crisis some economists (see Obstfeld & Rogoff, 2009) have argued that global imbalances, excessive CA surpluses by some countries and the corresponding CA deficits by other countries, have been playing a key role in creating the global economic crisis (actually some people were already worried about these global imbalances well before 2007).

In fact, China was artificially depressing the value of its currency for years in order to make its exports more competitive. Continuous sterilization policies by the Chinese Central Bank meant that it could keep the value of the Yuan low without and keeping domestic inflation in check (a rising domestic price level would have otherwise eroded the artificial boost in competitiveness).

The huge CA surplus artificially created by China implied that other countries, such as the U.S., had to run the corresponding deficit. Goods were thus flowing from China to the U.S., while $ were flowing in the other direction. However, since the American dollars were of no use to the Chinese, they acquired American assets with these $. These American assets were mainly U.S. government bonds but to some extent also private assets such as the famous mortgage-backed securities (MBS)!

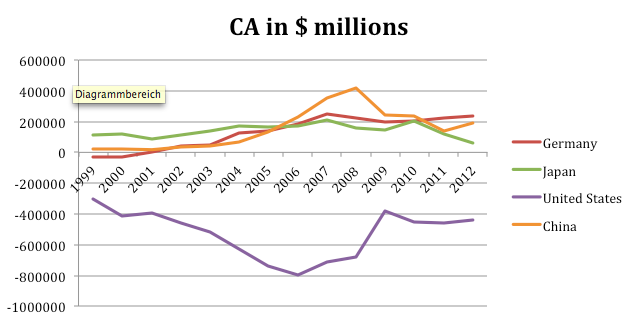

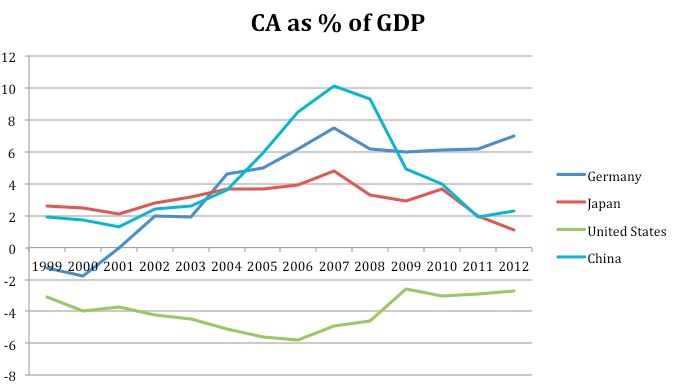

Other countries in South-East Asia as well as Japan and Germany, for example, were also running quite huge and persistent CA surpluses. All these excess savings, that is higher domestic savings than investment, meant that huge capital flows were channeled towards the deficit countries, mainly the U.S. (and Southern Europe). It is uncontroversial to say that these huge capital flows are at least partially responsible for the American housing bubble: The U.S. experienced capital inflows in the order of almost 800$ billion in 2006 (almost 6% U.S. GDP): see the two charts below.

The cumulative inflow of capital in between 2000 and 2008 was about 4.6 TRILLION $ (in comparison, American GDP in 2008 was slightly above 14 Trillion $). It seems reasonable that these immense inflows of capital at least partially contributed to the enormous housing bubble (Notice how the U.S. CA deficits was greatest in the years just before the crisis, which were also the years when the American houses gained most of their value. Nonetheless, as always in economics an apparent correlation does not necessarily imply causation! However, it is safe to assume here that these large inflows DID have an impact on American asset prices).

In fact, China was artificially depressing the value of its currency for years in order to make its exports more competitive. Continuous sterilization policies by the Chinese Central Bank meant that it could keep the value of the Yuan low without and keeping domestic inflation in check (a rising domestic price level would have otherwise eroded the artificial boost in competitiveness).

The huge CA surplus artificially created by China implied that other countries, such as the U.S., had to run the corresponding deficit. Goods were thus flowing from China to the U.S., while $ were flowing in the other direction. However, since the American dollars were of no use to the Chinese, they acquired American assets with these $. These American assets were mainly U.S. government bonds but to some extent also private assets such as the famous mortgage-backed securities (MBS)!

Other countries in South-East Asia as well as Japan and Germany, for example, were also running quite huge and persistent CA surpluses. All these excess savings, that is higher domestic savings than investment, meant that huge capital flows were channeled towards the deficit countries, mainly the U.S. (and Southern Europe). It is uncontroversial to say that these huge capital flows are at least partially responsible for the American housing bubble: The U.S. experienced capital inflows in the order of almost 800$ billion in 2006 (almost 6% U.S. GDP): see the two charts below.

The cumulative inflow of capital in between 2000 and 2008 was about 4.6 TRILLION $ (in comparison, American GDP in 2008 was slightly above 14 Trillion $). It seems reasonable that these immense inflows of capital at least partially contributed to the enormous housing bubble (Notice how the U.S. CA deficits was greatest in the years just before the crisis, which were also the years when the American houses gained most of their value. Nonetheless, as always in economics an apparent correlation does not necessarily imply causation! However, it is safe to assume here that these large inflows DID have an impact on American asset prices).

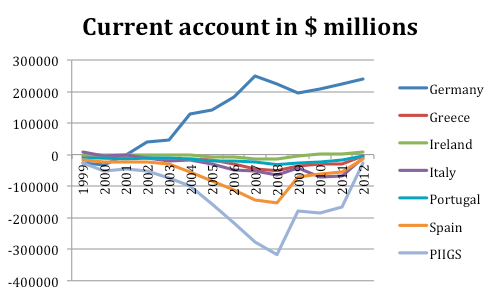

Similarly, the same kind of imbalances observed between China and the U.S. were also apparent (and still are!) in the Eurozone. The creation of a common currency implied that exchange rate risk was completely eliminated. Capital in the Eurozone was thus chasing for yield (higher returns), which was to be found in Southern Europe. The enormous flows of capital from Northern Europe and foremost Germany led to the creation of the asset bubbles (especially housing) in the now so-called PIIGS countries (Portugal, Italy, Ireland, Greece, and Spain).

Furthermore, the capital flows were also largely responsible for relatively high wage increases and price increases in these countries (compared to Germany), which largely eroded their competitiveness over time.

Last but not least, there is significant evidence that monetary policy in the years before the crisis was too easy for the PIIGS countries but somewhat too tight for Germany (This can easily be seen by using a simple Taylor-rule approach to evaluate the stance of monetary policy in the different Eurozone countries. See Nechio (2011), for example.). As a consequence, this fueled the bubble and the increases in prices and wages in the Southern European countries while wages and prices rose significantly less in Germany, thus boosting its competitiveness.

Germany's businessmen and politicians, patting themselves on their backs for being so competitive, really deserve much less credit! And so do the widely cited “Hartz reforms” (structural reforms undertaken by the German government in the beginning of the 2000s to combat the high level of unemployment that the country experienced in the beginning of the decade). It is true that these reforms did increase labor market flexibility and that Germany benefited and became more competitive as a result. However, the impact of these reforms is probably widely overrated. Most of the increase in German competitiveness relative to Southern Europe, however, can directly be attributed to the capital flows just mentioned above as well as easy money in the European periphery before the crisis (obviously these two phenomena are related).

Following Bernanke’s reasoning that the U.S. current account deficit has mainly been driven by international capital flows in the years before the crisis (Bernanke, 2005), I think that a similar argument can be made for Germany and the Eurozone periphery. I guess this is the point that most people don’t understand, but the German CA surplus is the result of domestic savings/investment decisions. As described earlier, excess savings by German residents have been channeled mainly to Southern Europe and this dynamic largely fed on itself for several years until the bubbles popped.

Now ever since the beginning of the Eurozone crisis, the deficit countries had to make painful adjustments. As capital flows to Southern Europe suddenly stopped after the outbreak of the crisis, these countries were forced to bring down their respective CA deficits. Since it is impossible to significantly increase exports within a short period of time, the adjustment process only could come about a significant reduction in imports, which in turn required lower national spending on foreign goods. The reversal of capital flows thus required the deficit countries to go through an adjustment process that involved falling levels of domestic spending (GDP).

The graph below shows how the deficit countries reduced their respective CA deficits over the last couple of years. Germany, on the other hand, has done the opposite. Instead of rebalancing its economy, the German CA has increased over the last years to excessive levels: 7% of GDP in 2012 (or about 240 billion $)! Germany has made no attempt to decrease the global imbalances that fuelled the crisis in the first place.

Furthermore, the capital flows were also largely responsible for relatively high wage increases and price increases in these countries (compared to Germany), which largely eroded their competitiveness over time.

Last but not least, there is significant evidence that monetary policy in the years before the crisis was too easy for the PIIGS countries but somewhat too tight for Germany (This can easily be seen by using a simple Taylor-rule approach to evaluate the stance of monetary policy in the different Eurozone countries. See Nechio (2011), for example.). As a consequence, this fueled the bubble and the increases in prices and wages in the Southern European countries while wages and prices rose significantly less in Germany, thus boosting its competitiveness.

Germany's businessmen and politicians, patting themselves on their backs for being so competitive, really deserve much less credit! And so do the widely cited “Hartz reforms” (structural reforms undertaken by the German government in the beginning of the 2000s to combat the high level of unemployment that the country experienced in the beginning of the decade). It is true that these reforms did increase labor market flexibility and that Germany benefited and became more competitive as a result. However, the impact of these reforms is probably widely overrated. Most of the increase in German competitiveness relative to Southern Europe, however, can directly be attributed to the capital flows just mentioned above as well as easy money in the European periphery before the crisis (obviously these two phenomena are related).

Following Bernanke’s reasoning that the U.S. current account deficit has mainly been driven by international capital flows in the years before the crisis (Bernanke, 2005), I think that a similar argument can be made for Germany and the Eurozone periphery. I guess this is the point that most people don’t understand, but the German CA surplus is the result of domestic savings/investment decisions. As described earlier, excess savings by German residents have been channeled mainly to Southern Europe and this dynamic largely fed on itself for several years until the bubbles popped.

Now ever since the beginning of the Eurozone crisis, the deficit countries had to make painful adjustments. As capital flows to Southern Europe suddenly stopped after the outbreak of the crisis, these countries were forced to bring down their respective CA deficits. Since it is impossible to significantly increase exports within a short period of time, the adjustment process only could come about a significant reduction in imports, which in turn required lower national spending on foreign goods. The reversal of capital flows thus required the deficit countries to go through an adjustment process that involved falling levels of domestic spending (GDP).

The graph below shows how the deficit countries reduced their respective CA deficits over the last couple of years. Germany, on the other hand, has done the opposite. Instead of rebalancing its economy, the German CA has increased over the last years to excessive levels: 7% of GDP in 2012 (or about 240 billion $)! Germany has made no attempt to decrease the global imbalances that fuelled the crisis in the first place.

Furthermore, neither German officials nor German business papers seem to have any clue about the underlying problems at hand. Any serious discussion about the German CA surplus should involve the following questions and issues:

- Why is in Germany’s interest to have such a big CA surplus in the first place?

The surplus just shows that German domestic investment is very low compared to domestic savings. How can it be in Germany’s interest to constantly channel excess savings abroad instead of making domestic investments? How do policy makers not see that low domestic investments are potentially a bad thing?

- How can it be in Germany’s interest to have such high domestic savings in a time where the entire Eurozone experiences a lack of aggregate demand?

Higher German domestic spending would be a big relief for the Eurozone as a whole because of multiplier and spillover effects. Higher domestic German consumption would be better for the German economy as well. German nominal GDP growth has been somewhat higher that of most other Eurozone countries over the last years but it still has been below what many would consider healthy growth.

- How can it be in Germany’s interest to demand from every Eurozone country to cut wages to ridiculous low levels to remain competitive?

Germany successfully demonstrates that a country in a currency area can become more competitive than the other member countries by depressing its wage level. A race to the bottom, where all countries try to steal services and industries from each other by depressing their wage levels cannot be in anyone’s interest in a currency union. Higher wages in Germany would make the adjustment mechanism for the other member countries much easier. It would also be in Germany’s interest, as higher wages would stimulate domestic consumption. It is crazy how one of the biggest economies in the world is so focused on export-led growth at the expense of its domestic economy.

- Finally, and this is really mind-boggling: How the hell does the German government expect the Eurozone with roughly 14% of world output to undertake an export-led growth strategy? This is arithmetically impossible. A small country like Belgium would be able to do it but not the Eurozone as a whole. Not everyone can become “German”. Nonetheless, that is what they apparently have been counting on. Going back to:

- Why is in Germany’s interest to have such a big CA surplus in the first place?

The surplus just shows that German domestic investment is very low compared to domestic savings. How can it be in Germany’s interest to constantly channel excess savings abroad instead of making domestic investments? How do policy makers not see that low domestic investments are potentially a bad thing?

- How can it be in Germany’s interest to have such high domestic savings in a time where the entire Eurozone experiences a lack of aggregate demand?

Higher German domestic spending would be a big relief for the Eurozone as a whole because of multiplier and spillover effects. Higher domestic German consumption would be better for the German economy as well. German nominal GDP growth has been somewhat higher that of most other Eurozone countries over the last years but it still has been below what many would consider healthy growth.

- How can it be in Germany’s interest to demand from every Eurozone country to cut wages to ridiculous low levels to remain competitive?

Germany successfully demonstrates that a country in a currency area can become more competitive than the other member countries by depressing its wage level. A race to the bottom, where all countries try to steal services and industries from each other by depressing their wage levels cannot be in anyone’s interest in a currency union. Higher wages in Germany would make the adjustment mechanism for the other member countries much easier. It would also be in Germany’s interest, as higher wages would stimulate domestic consumption. It is crazy how one of the biggest economies in the world is so focused on export-led growth at the expense of its domestic economy.

- Finally, and this is really mind-boggling: How the hell does the German government expect the Eurozone with roughly 14% of world output to undertake an export-led growth strategy? This is arithmetically impossible. A small country like Belgium would be able to do it but not the Eurozone as a whole. Not everyone can become “German”. Nonetheless, that is what they apparently have been counting on. Going back to:

The Eurozone crisis meant that there was a sharp reduction of C and I by the private sector. Austerity measures further reduced GDP by depressing government expenditures G, implying that only X - IM is left for lifting domestic income! How is that supposed to work?

(I know. I am neglecting here how structural reforms are somehow magically supposed to lift C and I and that this is how the Eurozone would quickly recover and come out of the depression even stronger. Well, that hasn’t worked out very well so far.)

So any serious discussion about the German CA should have raised all the points I just mentioned above. Nobody in the German government, however, has acknowledged any of these issues and their words and policy actions have made it sufficiently clear that they are really unaware. They just do not understand to what extent the German policies have represented beggar-thy-neighbor policies over the last couple of years. The extent of how clueless they really are about the nature of the crisis was again demonstrated this week when the U.S. rightfully attacked Germany for pursuing these kind of policies but nobody in the German government and/or press would acknowledge the problems associated with Germany’s policy actions, thus the genesis of this post.

Meanwhile popular newspapers and some policy makers have been constantly accusing another country, Japan, for pursuing beggar-thy-neighbor policies even though that is exactly NOT what Japan is doing, just illustrating once more how clueless really everybody is!

Supposedly, the aggressive Japanese monetary expansion is depressing the value of the Yen and thus artificially making Japanese goods more competitive. While it is true that the SIDE EFFECT of the monetary expansion has been a depreciation of the Japanese currency, the GOAL of the policy was never really export-promotion but stimulating aggregate demand. The Bank of Japan succeeded in doing so and the Japanese CA actually went down (to some extent visible in my graph even though 2013 is not included) instead of going up. That is for two reasons, a lower Yen meant that imports become more expansive but higher aggregate demand also means that Japanese are buying MORE foreign goods (meanwhile exports do not increase in the very short-run). This implies that the Japanese monetary expansion is the opposite of a beggar-thy-neighbor policy as it is actually beneficial to the rest of the world.

PS: I just saw that Krugman wrote two very short blogposts about the same topic. As far as I can tell I basically wrote a very similar story as he did, just much more lengthy.

http://krugman.blogs.nytimes.com/2013/11/01/the-harm-germany-does/

http://krugman.blogs.nytimes.com/2013/11/01/more-notes-on-germany/

Sources:

- Bernanke, B. (2005). The global saving glut and the u.s. current account deficit. http://www.federalreserve.gov/boarddocs/speeches/2005/200503102/

- Nechio, F. (2011, June 13). Monetary policy when one size does not fit all. Retrieved

from http://www.frbsf.org/economic-research/files/el2011-18.pdf

on the 2nd of November, 2013.

- Obstfeld, M. & Rogoff, K. (2009). Global imbalances and the financial crisis: products of common causes.

(I know. I am neglecting here how structural reforms are somehow magically supposed to lift C and I and that this is how the Eurozone would quickly recover and come out of the depression even stronger. Well, that hasn’t worked out very well so far.)

So any serious discussion about the German CA should have raised all the points I just mentioned above. Nobody in the German government, however, has acknowledged any of these issues and their words and policy actions have made it sufficiently clear that they are really unaware. They just do not understand to what extent the German policies have represented beggar-thy-neighbor policies over the last couple of years. The extent of how clueless they really are about the nature of the crisis was again demonstrated this week when the U.S. rightfully attacked Germany for pursuing these kind of policies but nobody in the German government and/or press would acknowledge the problems associated with Germany’s policy actions, thus the genesis of this post.

Meanwhile popular newspapers and some policy makers have been constantly accusing another country, Japan, for pursuing beggar-thy-neighbor policies even though that is exactly NOT what Japan is doing, just illustrating once more how clueless really everybody is!

Supposedly, the aggressive Japanese monetary expansion is depressing the value of the Yen and thus artificially making Japanese goods more competitive. While it is true that the SIDE EFFECT of the monetary expansion has been a depreciation of the Japanese currency, the GOAL of the policy was never really export-promotion but stimulating aggregate demand. The Bank of Japan succeeded in doing so and the Japanese CA actually went down (to some extent visible in my graph even though 2013 is not included) instead of going up. That is for two reasons, a lower Yen meant that imports become more expansive but higher aggregate demand also means that Japanese are buying MORE foreign goods (meanwhile exports do not increase in the very short-run). This implies that the Japanese monetary expansion is the opposite of a beggar-thy-neighbor policy as it is actually beneficial to the rest of the world.

PS: I just saw that Krugman wrote two very short blogposts about the same topic. As far as I can tell I basically wrote a very similar story as he did, just much more lengthy.

http://krugman.blogs.nytimes.com/2013/11/01/the-harm-germany-does/

http://krugman.blogs.nytimes.com/2013/11/01/more-notes-on-germany/

Sources:

- Bernanke, B. (2005). The global saving glut and the u.s. current account deficit. http://www.federalreserve.gov/boarddocs/speeches/2005/200503102/

- Nechio, F. (2011, June 13). Monetary policy when one size does not fit all. Retrieved

from http://www.frbsf.org/economic-research/files/el2011-18.pdf

on the 2nd of November, 2013.

- Obstfeld, M. & Rogoff, K. (2009). Global imbalances and the financial crisis: products of common causes.

RSS Feed

RSS Feed