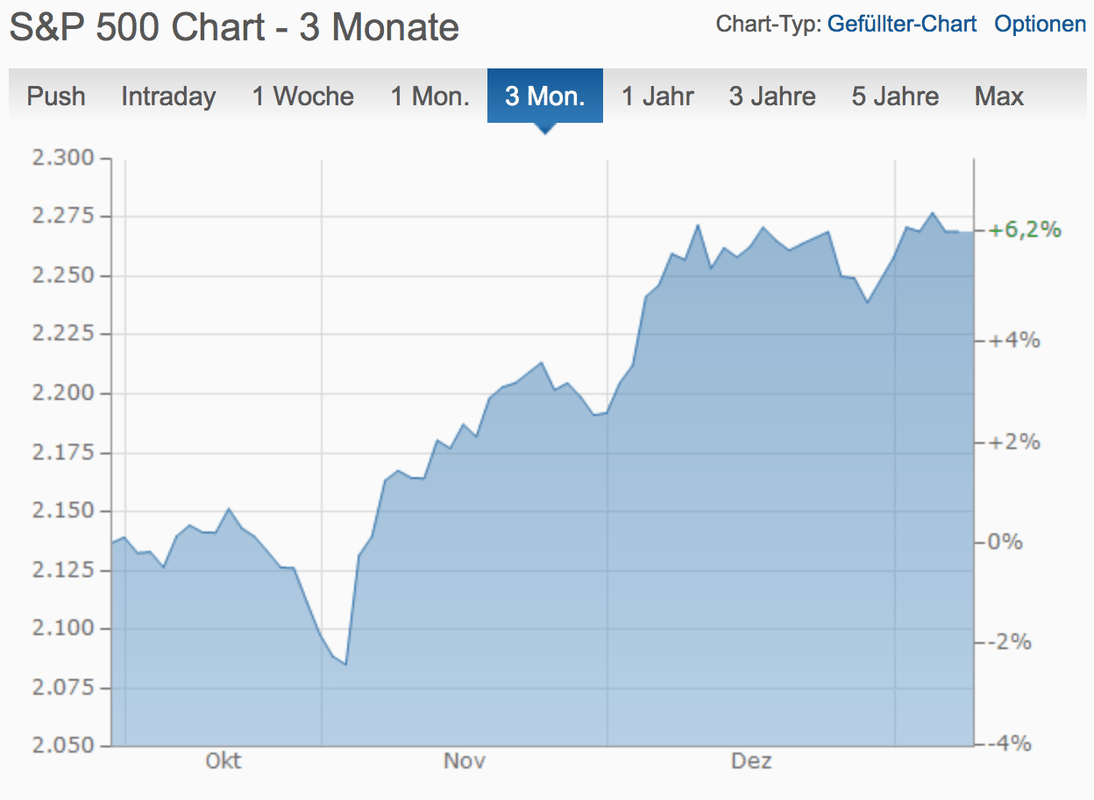

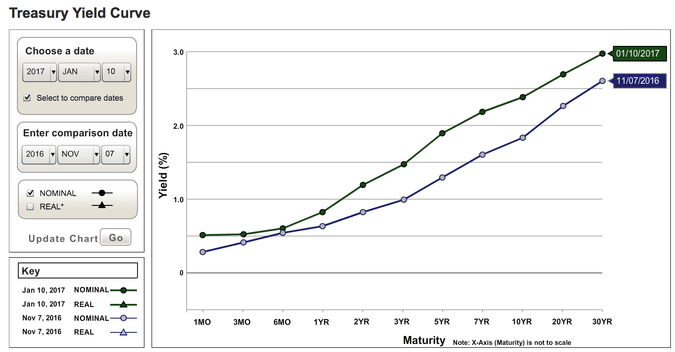

As far as I can tell, the new Trump administration will pursue a number of policies that will, on average, do more harm than good to the U.S. economy. Yet something remarkable has happened since last November. Economic growth has accelerated and asset prices have surged. There has been a great reshuffling of financial portfolios as investors have dumped safe assets (Treasuries) and increased their exposure towards riskier assets like stocks. Consequently, yields have risen across the board, especially in the light of another Fed interest rate hike as economy approaches full employment. The stock market gained more than 6% over the last 3 months. These events are very surprising insofar as economic fundamentals should not have changed that much in the aftermath of the recent election outcome. This begs the question to what extent the rally in asset prices is rational or whether it is purely driven by Keynesian animal spirits. Here are some proposed policies of the Trump administration one should be concerned about in the years to come:

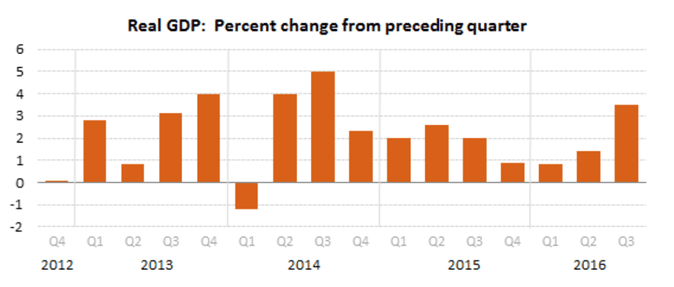

It thus seems that investors are currently ignoring economic fundamentals to a certain degree and that they are discounting most of the negative risks and potential Black swan events that might be associated with the Trump administration. After years of disappointing GDP growth, depressed business investment and depressed sentiment, it looks like both consumers and firms now finally leave caution behind and adopt a “risk-on” mode.

In my opinion, the current trends in financial markets cannot entirely be explained by economic fundamentals, but are rather based on Keynesian animal spirits, an exogenous shift in expectations and sentiment. Of course, one should bear in mind that economic fundamentals are themselves a function of expectations. In that sense, the current improvement in the U.S. economy and U.S. financial markets are based on a self-fulfilling prophecy, which is, of course, welcome news. However, caution is in order because one can easily imagine a scenario in which investors rapidly dump stocks again and flock into a safe haven (Treasuries) if one or several of the adverse Trump shocks occur. There thus seems to be a lot of downside risk that financial markets are for whatever reason downplaying at the moment.

- Deregulation of financial markets: This will boost the profits of financial firms, but it comes at the expense of greater risk of financial instability. Banks like Goldman Sachs have been the biggest winners of the recent stock market rally as deregulation leads to prospects of greater profit opportunities. A more laissez-faire approach when it comes to financial markets might of course sow the seeds for a future financial crisis.

- Harassment of individual corporations and threat of a trade war: Trump has persistently pursued and harassed individual companies, such as Toyota, which produce for the U.S. market in Mexico. He has also labeled China a currency manipulator, even thought this is clearly nonsensical. While a few years back China was indeed pushing down the valua of its currency, the government is currently in the exact opposite position. With the weakening of the domestic economy China is currently propping up the value of the yuan. A trade war with China, while not being a financial catastrophe, is a negative sum game in nature and would reduce economic growth.

- Tax cuts for the rich: Tax cuts for the rich will not lead to higher spending in the economy because the rich have a very low marginal propensity to consume. Furthermore, at full employment any fiscal stimulus will be offset by the Fed, which determines the amount of nominal expenditures in the economy. There also seems to be little evidence for positive supply side effects from lower top marginal income taxes. Instead, such a policy would lead to a higher budget deficit and higher taxes down the road to finance the debt, thus actually reducing growth.

- Infrastructure investments: The U.S. just like many other advanced economies is in desperate need of better infrastructure. Investments into infrastructure are unlikely to lead to much more nominal spending in the economy for standard monetary offset reasons when monetary policy is not constrained by the zero-lower bound. More government spending could still be desirable because it would allow the Fed to raise interest rates at a quicker pace and would thus give monetary policy more leeway for the next recession. However, a combination of more stimulative fiscal policy and more restrictive monetary policy would strengthen the dollar even further, thus threatening the manfacturing jobs Trump has sworn to protect. Finally, better infrastructure could also raise the economy’s potential output. However, there is a good chance that the infrastructure investments will lead to a lot of waste. Crony capitalism is a real concern with the new Trump administration.

- Appreciation of the dollar: The dollar has strongly appreciated since the election outcome in early November. This partly reflects concerns over emerging markets who would suffer from more protectionist policies as well as a different macroeconomic policy mix in the U.S. with looser fiscal policy and tighter monetary policy. Ironically, the appreciation of the dollar is causing trouble for U.S. manufacturing, the sector Trump has sworn to protect. Furthermore, a strengthening of the dollar might also cause be a small negative for the world economy. That is because many emerging markets are on the so-called “dollar standard”: their currencies are pegged to the greenback. This means that they will import the monetary tightening from the U.S. Furthermore, many emerging markets have large liabilities in U.S. dollars. A strengthening U.S. currency thus means a deterioration of their balance sheets.

- Corporate tax reform: The U.S. corporate tax rate is one of the highest in the world Consequently, American companies have haorded trillions of dollars overseas in order to avoid taxation. The American economy would greatly benefit from a repatriation of profits that U.S. companies have parked abroad. However, there is some doubt over the efficacy of the tax reforms that the Trump team has suggested. Furthermore, reducing corporate taxation would only exacerbate the already high levels of inequality.

- Health care reform: The Republicans seems very eager to repeal the ACA as soon as possible without suggesting any feasible replacement. Such an act might leave as much as 20 million people without health insurance. States will loose billions of dollars in subsidies from the federal government. The health care industry will be in disarray and many will be lost in the insurance sector as well as in the provision of healthcare if the ACA is repelled.

It thus seems that investors are currently ignoring economic fundamentals to a certain degree and that they are discounting most of the negative risks and potential Black swan events that might be associated with the Trump administration. After years of disappointing GDP growth, depressed business investment and depressed sentiment, it looks like both consumers and firms now finally leave caution behind and adopt a “risk-on” mode.

In my opinion, the current trends in financial markets cannot entirely be explained by economic fundamentals, but are rather based on Keynesian animal spirits, an exogenous shift in expectations and sentiment. Of course, one should bear in mind that economic fundamentals are themselves a function of expectations. In that sense, the current improvement in the U.S. economy and U.S. financial markets are based on a self-fulfilling prophecy, which is, of course, welcome news. However, caution is in order because one can easily imagine a scenario in which investors rapidly dump stocks again and flock into a safe haven (Treasuries) if one or several of the adverse Trump shocks occur. There thus seems to be a lot of downside risk that financial markets are for whatever reason downplaying at the moment.

RSS Feed

RSS Feed