Last year, the Federal Reserve undertook a major tightening cycle and hiked rates 4 times. Just half a year ago, members of the Fed board thought that in 2019 they would be able to accomplish the same feat and hike interest rates another 4 times to reach a level of about 3% by the end of the year. This was always utopian thinking. It is unfortunate that I didn't mark my beliefs to market lat the time because in my mind it was never plausible that they would reach a level of 3% by the end of this year, or any time soon. So unfortunately I cannot link to any previous writing of mine in which I called out that such a substantial rate hike cycle for 2019 would be quite unlikely.

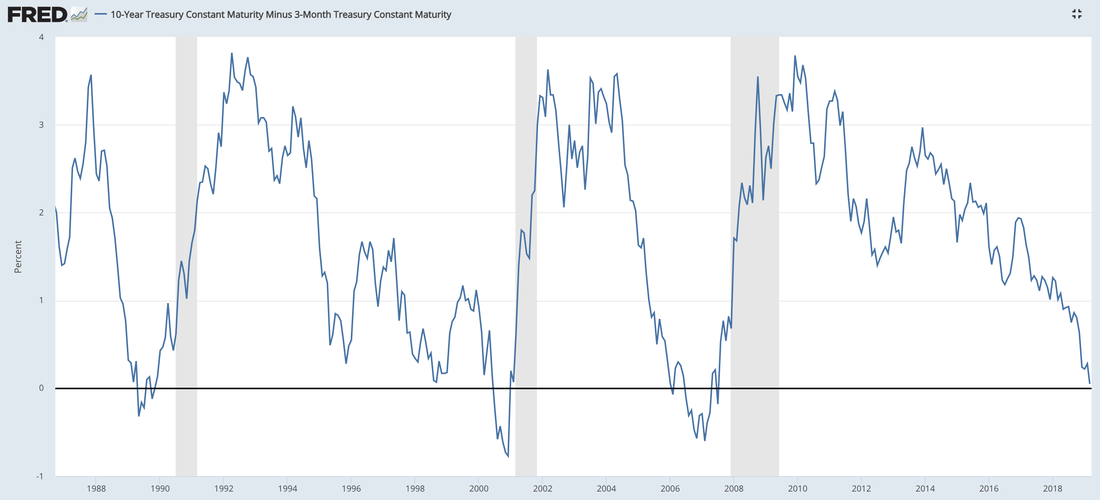

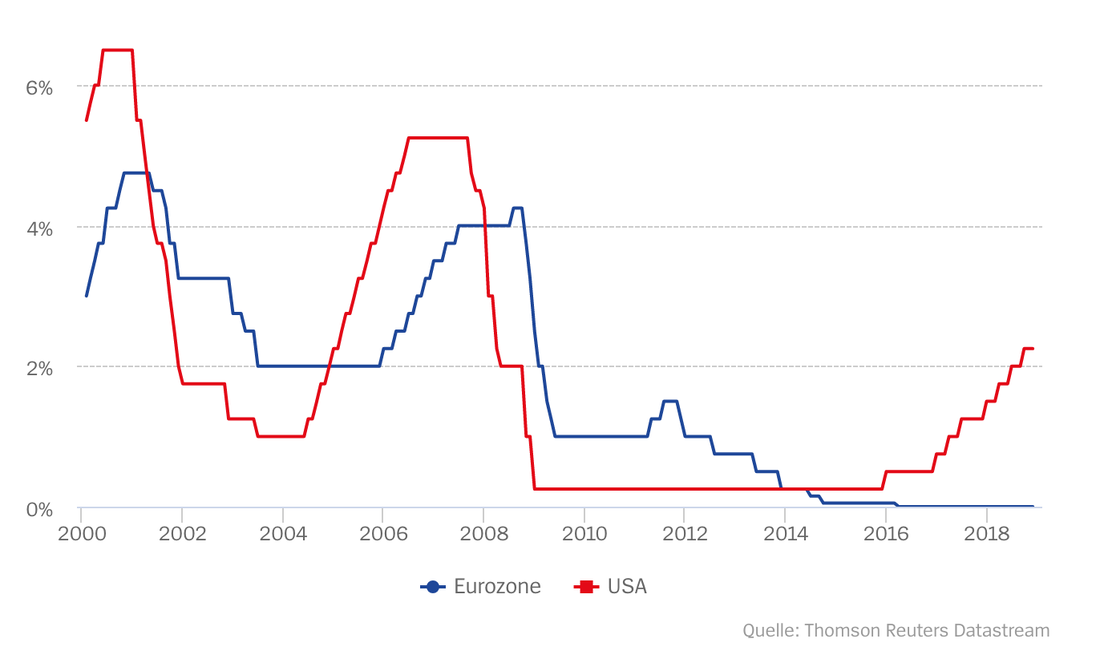

However, now it turns out that this view is vindicated. In fact, the yield curve has just inverted on Friday, meaning that interest rates on 3-months Treasuries are now higher than rates on 10-year bonds. The yield curve inversion has been in the past the only and most reliable signal of a future recession. Furthermore, it now looks more likely than not that the next interest rate moves will be a decrease rather than an increase. It therefore increasingly looks like the tightening cycle of last year was somewhat premature. With the global economy slowing down quite substantially and the stimulatory effect of the Trump tax cut wearing off right now, it might be necessary now to cut rates again even though they are only at a little over 2%. And financial markets seem to agree, given that they are pricing in at least one rate decrease over the next year.

Secular stagnation is therefore a reality now. Nominal interest rates are still negative in Japan, the Eurozone, Sweden and Switzerland. In fact, interest rates are low across the globe because several structural factors have pushed them down for decades now: Ageing societies, low productivity growth, rising inequality, and maybe rising monopolization.

Even though the Fed is to some extent the global Central Banker, providing dollar liquidity to the entire world, they also are not immune from these long-run macroeconomic forces that have affected the global economy substantially. Interest rates in the US have already decoupled from other advanced economies quite substantially. However, a further divergence always seemed unlikely, given that the gap between US rates and Euro rates already exceeds 2 percentage points. Further interest rate hikes would push up the value of the dollar substantially, making US industries uncompetitive and slowing down domestic demand. In fact, my own research shows that interest rates are to a very large extent determined by global factors in today's world of global capital flows. This is also true for the US economy.

While I do not predict a US recession over the next 12 months, GDP Nowcast models already show a substantial economic slowdown compared to the 3% growth the US economy achieved last year. However, the odds of a recession have increased with the inversion of the yield curve, which seems to indicate to me that the Fed tightened too much over the last year.

Everything will now depend on the reaction function of the Fed. Just this week, Powell indicated that they will not increase rates anymore this year. While the US economy never really accomplished a soft landing, a recession does not necessarily have to be baked in by now. It will mostly depend on the degree of interest rate inertia, meaning how quickly the Fed will respond to a slowdown of the economy by starting to ease monetary policy again.

While the past does not give us too much hope, maybe this time is different?

PS: We should be much more worried about the Eurozone where the latest economic data has been extremely disappointing just as the ECB stopped its program of Quantitative Easing. Coincidence? Given that rates are still negative, the ECB can only ease policy by purchasing new assets. However, this seems to be a relatively unlikely step, given how much political backlash such a policy would produce. So we should all be very worried if the slowdown in the Eurozone turns out to be much more severe and persistent.

However, now it turns out that this view is vindicated. In fact, the yield curve has just inverted on Friday, meaning that interest rates on 3-months Treasuries are now higher than rates on 10-year bonds. The yield curve inversion has been in the past the only and most reliable signal of a future recession. Furthermore, it now looks more likely than not that the next interest rate moves will be a decrease rather than an increase. It therefore increasingly looks like the tightening cycle of last year was somewhat premature. With the global economy slowing down quite substantially and the stimulatory effect of the Trump tax cut wearing off right now, it might be necessary now to cut rates again even though they are only at a little over 2%. And financial markets seem to agree, given that they are pricing in at least one rate decrease over the next year.

Secular stagnation is therefore a reality now. Nominal interest rates are still negative in Japan, the Eurozone, Sweden and Switzerland. In fact, interest rates are low across the globe because several structural factors have pushed them down for decades now: Ageing societies, low productivity growth, rising inequality, and maybe rising monopolization.

Even though the Fed is to some extent the global Central Banker, providing dollar liquidity to the entire world, they also are not immune from these long-run macroeconomic forces that have affected the global economy substantially. Interest rates in the US have already decoupled from other advanced economies quite substantially. However, a further divergence always seemed unlikely, given that the gap between US rates and Euro rates already exceeds 2 percentage points. Further interest rate hikes would push up the value of the dollar substantially, making US industries uncompetitive and slowing down domestic demand. In fact, my own research shows that interest rates are to a very large extent determined by global factors in today's world of global capital flows. This is also true for the US economy.

While I do not predict a US recession over the next 12 months, GDP Nowcast models already show a substantial economic slowdown compared to the 3% growth the US economy achieved last year. However, the odds of a recession have increased with the inversion of the yield curve, which seems to indicate to me that the Fed tightened too much over the last year.

Everything will now depend on the reaction function of the Fed. Just this week, Powell indicated that they will not increase rates anymore this year. While the US economy never really accomplished a soft landing, a recession does not necessarily have to be baked in by now. It will mostly depend on the degree of interest rate inertia, meaning how quickly the Fed will respond to a slowdown of the economy by starting to ease monetary policy again.

While the past does not give us too much hope, maybe this time is different?

PS: We should be much more worried about the Eurozone where the latest economic data has been extremely disappointing just as the ECB stopped its program of Quantitative Easing. Coincidence? Given that rates are still negative, the ECB can only ease policy by purchasing new assets. However, this seems to be a relatively unlikely step, given how much political backlash such a policy would produce. So we should all be very worried if the slowdown in the Eurozone turns out to be much more severe and persistent.

Another US yield curve inversion: Harbinger of bad news?

RSS Feed

RSS Feed