One of the most amazing things about the financial crisis is how well standard macroeconomics has performed over the last few years, despite many claims to the contrary. But those are usually just plainly unintelligent and wrong. So here are some events that turned out exactly as predicted in advance by the likes of Paul Krugman, Brad DeLong and others:

All these events thus turned out pretty much in accordance with standard macroeconomics. The failure of the Eurozone, for example, was anticipated by many American economists even before the introduction of the euro. Again, the theory of optimal currency areas was developed decades ago and it was well understood by economists that an external shock of sufficient size would be sufficient to cause extreme and painful divergences in economic performance between the countries that shared the euro. Of course, nobody did predict exactly when the shock would occur, but it was just a matter of time until it would happen eventually. The appalling incompetence of European policy makers, both at the ECB as well as in the national fiscal authorities, also could not have been foreseen in advance.

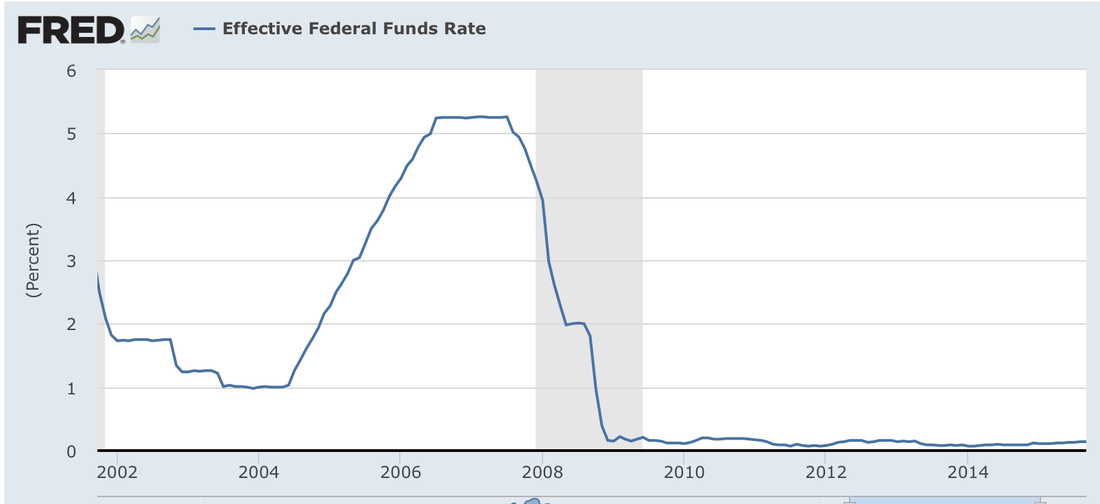

This point is related to the quite ignorant claim that macroeconomists should have seen the crisis in the US coming. This, of course, totally neglects the fact that the Fed normally steers the nominal economy. If they do their job, then we should never have observed such a huge shortfall in aggregate demand as it occurred in 2008/2009. The Fed minutes from 2008 make this point abundantly clear. They show that the Central Bankers were more concerned about inflation at that time than an economy in free fall. Already existent stress in the financial system was exacerbated by a slowing economy, thus leading to the financial crisis, which in turn caused the Great Recession. Unfortunately, at that time the Fed still had lots of ammunition left, but refused to employ it. The choice to let Lehmann Brothers fail and to not cut interest rates immediately thereafter, still at 2% back then, was in the end the critical moment in which a nasty recession turned into the largest and most prolonged economic downturn since the 1930s. Since the gross incompetence of a select group of individuals, in this case the board of the Fed, is inherently unpredictable, a crisis of such a large scale could not have been foreseen.

In all fairness, one must say that the Bernanke Fed made up for its mistakes in 2008 and largely outperformed other Central Banks (the ECB, the Swedish Riksbank) in subsequent years. QE and forward guidance have turned out to be the most essential policies helping the American economy back to its feet.

Unfortunately, the Yellen Fed seems to be quite determined to hit the brakes now even though there still seems to be significant amount of slack in the labor market and financial markets expect the Fed to undershoot its inflation target for years to come.

Ironically, Larry Summers appears to be much more dovish nowadays than Janet Yellen, even though at the time when both of them were still in the race for the Fed chair it was widely believed that the reverse is true. Today, Larry Summers repeatedly warns about the consequences of “secular stagnation" while the Fed under Yellen seems to be alarmingly unconcerned. Moreover, just as in all the previous years since 2008, the Fed staff seems to be overly optimistic when it comes to the future path of interest rates, inflation rates and economic growth.

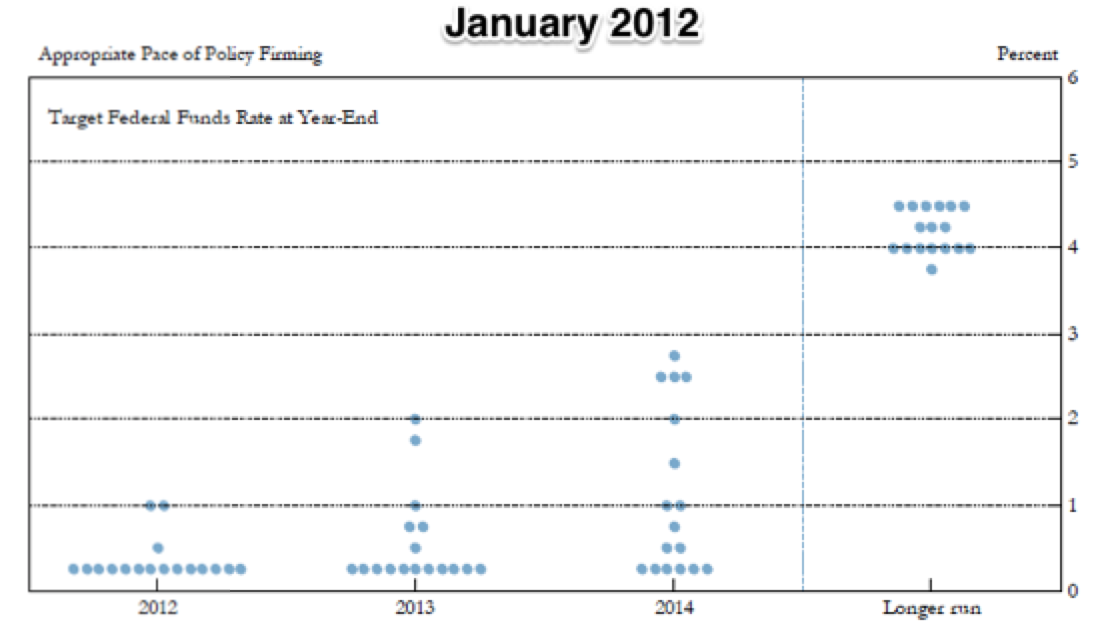

The following dot plot shows that in January 2012 the Fed median interest rate projection by the board of governors for 2014 was 1%. Meanwhile, the interest rate is still stuck at the zero-lower bound as of October 2015 and markets expect this to remain true until early 2016, at least.

- Austerity in the Eurozone would be self-defeating because fiscal multipliers are potentially large when Central Banks are constrained by the zero lower bound on interest rates. Indeed, the IMF has estimated retrospectively that fiscal multipliers might have been as large as 2, meaning that every euro saved by the government would depress total economic output by 2 euros. Under these circumstances reducing government spending would increase the debt to GDP ratio both in the short and in the long run, thus exactly leading to the scenario that austerity was supposed to cure.

- Large increases in the monetary base would not be inflationary. Indeed, the liquidity trap has panned out exactly as the “Japanese warriors” have predicted (Krugman’s term for the macroeconomists who studied the Japanese lost decade in detail: himself, Ben Bernanke, Lars Svensson and Michael Woodford). At zero interest rates, base money and government bonds become perfect substitutes. Any purchases of government bonds will thus have very limited effects on the broader economy since the additional base money is just sitting as excess reserves in the banking system. Large increases in the monetary base would thus would not turn the U.S into Zimbabwe and any claims of inherent hyperinflation have turned out spectacularly wrong. Indeed, financial markets correctly forecasted that inflation after 2008 would remain subdued, and even more worryingly, markets now expect that the Fed will continue to undershoot its own inflation target for another decade. Larry Summer’s secular stagnation hypothesis is looking better by the minute.

- Doomsday sayers also predicted that interest rates on government debt would soar in the wake of large and rising government deficits as the economic recession began. This analysis was obviously serious flawed, at least for countries that can print their own currencies and are not locked up in a suboptimal currency union (such as the Eurozone). Once the crisis hit of course the exact opposite happened, again quite in accordance with standard macroeconomic theory. The temporary collapse of the financial market, the enormous fall in asset prices and the looming depression led to an enormous flight to safety. Both domestic as well as international investors thus searched the ultimate safe haven, that is, debt issued by the American Federal government. Even though the crisis originated in the US, the American dollar soared as investors worldwide bought American government bonds in their flight to safety, driving down short-term interest rates to zero. Under such a scenario even large increases in the government deficit do not lead to rising interest rates. The large excess demand for safe assets imply close to zero interest rate, at least at the short end of the yield curve, as the private sector simply swallows all additional debt issuance by the government. As a side note, even all the dumping of American government debt by the Chinese state over the last few months did not have any visible effect on US interest rates. Again, many people feared exactly this scenario , but Paul Krugman already called it out a few years back that this would be a stupid thing to worry about under current circumstances.

All these events thus turned out pretty much in accordance with standard macroeconomics. The failure of the Eurozone, for example, was anticipated by many American economists even before the introduction of the euro. Again, the theory of optimal currency areas was developed decades ago and it was well understood by economists that an external shock of sufficient size would be sufficient to cause extreme and painful divergences in economic performance between the countries that shared the euro. Of course, nobody did predict exactly when the shock would occur, but it was just a matter of time until it would happen eventually. The appalling incompetence of European policy makers, both at the ECB as well as in the national fiscal authorities, also could not have been foreseen in advance.

This point is related to the quite ignorant claim that macroeconomists should have seen the crisis in the US coming. This, of course, totally neglects the fact that the Fed normally steers the nominal economy. If they do their job, then we should never have observed such a huge shortfall in aggregate demand as it occurred in 2008/2009. The Fed minutes from 2008 make this point abundantly clear. They show that the Central Bankers were more concerned about inflation at that time than an economy in free fall. Already existent stress in the financial system was exacerbated by a slowing economy, thus leading to the financial crisis, which in turn caused the Great Recession. Unfortunately, at that time the Fed still had lots of ammunition left, but refused to employ it. The choice to let Lehmann Brothers fail and to not cut interest rates immediately thereafter, still at 2% back then, was in the end the critical moment in which a nasty recession turned into the largest and most prolonged economic downturn since the 1930s. Since the gross incompetence of a select group of individuals, in this case the board of the Fed, is inherently unpredictable, a crisis of such a large scale could not have been foreseen.

In all fairness, one must say that the Bernanke Fed made up for its mistakes in 2008 and largely outperformed other Central Banks (the ECB, the Swedish Riksbank) in subsequent years. QE and forward guidance have turned out to be the most essential policies helping the American economy back to its feet.

Unfortunately, the Yellen Fed seems to be quite determined to hit the brakes now even though there still seems to be significant amount of slack in the labor market and financial markets expect the Fed to undershoot its inflation target for years to come.

Ironically, Larry Summers appears to be much more dovish nowadays than Janet Yellen, even though at the time when both of them were still in the race for the Fed chair it was widely believed that the reverse is true. Today, Larry Summers repeatedly warns about the consequences of “secular stagnation" while the Fed under Yellen seems to be alarmingly unconcerned. Moreover, just as in all the previous years since 2008, the Fed staff seems to be overly optimistic when it comes to the future path of interest rates, inflation rates and economic growth.

The following dot plot shows that in January 2012 the Fed median interest rate projection by the board of governors for 2014 was 1%. Meanwhile, the interest rate is still stuck at the zero-lower bound as of October 2015 and markets expect this to remain true until early 2016, at least.

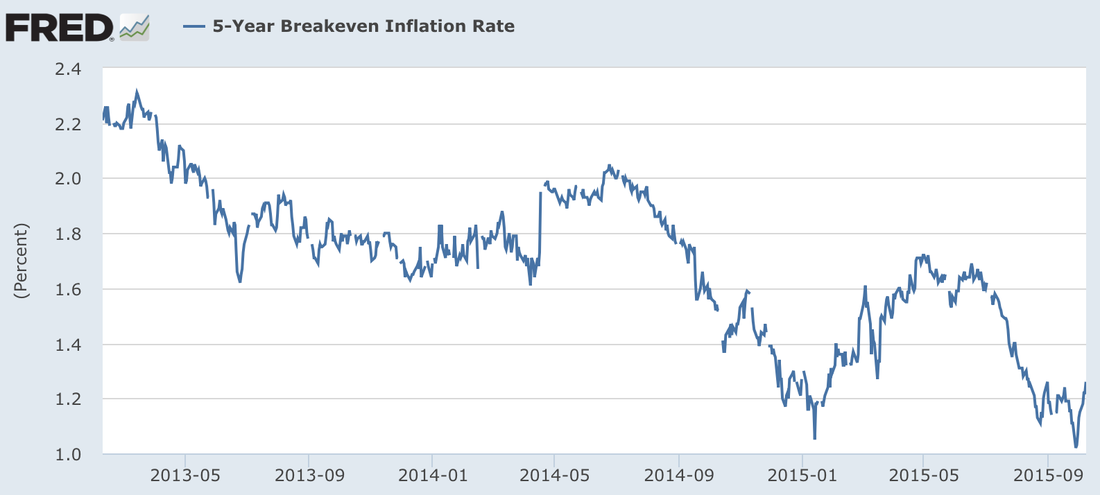

There is a quite striking disconnect between what the Fed thinks and what financial markets think the economy will perform like over the next few years. It is very revealing that market participants seem to have accepted the “secular stagnation” hypothesis put forward by Larry Summers. Indeed, the TIPS spread, i.e. the spread between normal Treasury bonds and inflation-protected Treasury bonds, tells us that financial markets expect the average inflation rate as measured by the CPI to be about 1.3% over the next 5 years. This would lead to an increase of the price level by about 6.7% whereas the Fed’s own mandate requires an increase of about 11.5%: The Fed targets a 2% increase in the core personal consumption expenditure (PCE), which is roughly consistent with an annual CPI increase of 2.2% (2.2%^5 = 11.5%). Financial markets thus expect the price level to be 5% lower than the Fed’s official target in 5 years time.

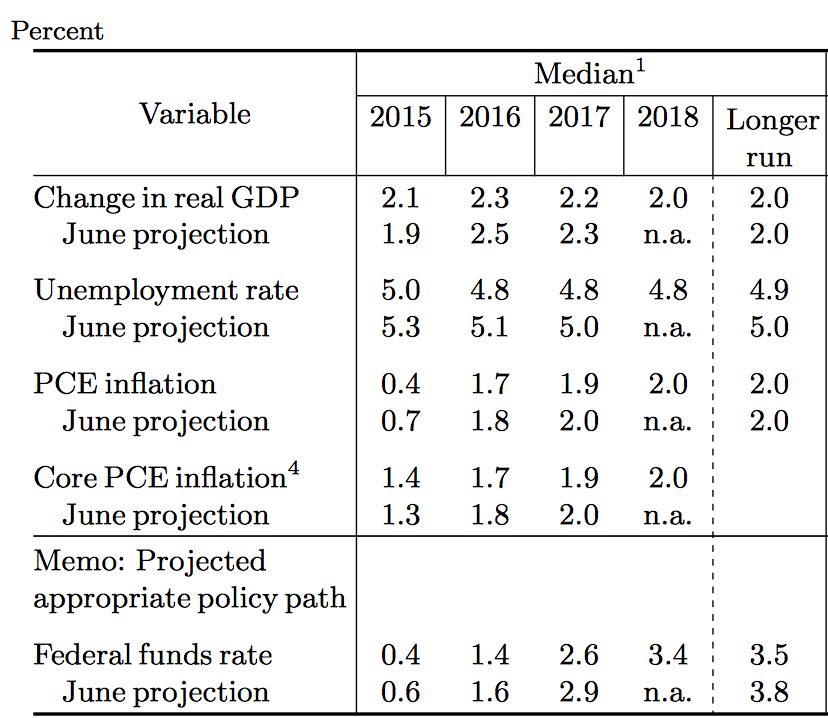

Interestingly enough, the Fed’s own projections suggest that they do not think that such a massive undershooting will occur. One can see below that their forecast is that they will basically hit the target again by 2017. However, their own forecasts still suggest that monetary policy is still more restrictive than what should be the case: 1.7%*1.9%*2.0%*2.0%*2.0% = 10% (and I am actually being overly generous here by overlooking the 0.4% forecast for the year 2015).

According to Lars Svensson’s, monetary policy should be conducted in a way what he calls “target the forecast”. Since internal and financial market projections suggest that monetary policy is still quite restrictive, the Fed should move towards easier money until forecasts are in line with the official inflation target.

What is also striking is that the Fed still expects interest rate normalization over the coming years despite having been wrong over and over again in recent years. Financial markets, on the other hand, remain highly sceptical. The Fed funds future market predicts a nominal interest rate of about 1% by the end of 2017 while the Fed’s median forecast is an astonishing 2.6%. Only one member, Kocherlakota, seems to have accepted the secular stagnation hypothesis (he is the lonely dot far below the other ones for the years 2016 and 2017). Note that he recommends a negative interest rate for this year and the year to come!

I have made some predictions in the past that turned out correct, such as the rapid depreciation of the euro vs. the dollar as a consequence of the QE program launched by the ECB, for example. I have even made some money on this deal. And no, it was not a one-sided bet. But since I cannot prove this, I will start to mark my beliefs to market occasionally so that I and other people can evaluate in retrospect the forecasts I have made. As I have explained above, I will primarily rely on market forecasts, which have been on balance more accurate than the FED’s internal projections. Consequently, my views on the US economy are in line with Summer’s secular stagnation hypothesis and thus significantly more bearish than the more optimistic FED projections.

- The 5-year breakeven inflation rate is alarmingly low at the moment. I forecast the inflation rate, as measured by the CPI, to be around 1.3 - 1.5 % in the 5 years to come. I thus expect significant undershooting with respect to the Fed’s official target.

- The US economy is likely to experience real GDP growth rates of only about 2% in the foreseeable future, which would be still significantly higher than what one will observe in Europe or Japan. Consequently, I expect nominal GDP growth to average 3.5 to 4% over the next 5 years (that is a real GDP growth rate of about 2% and roughly 1.5 % inflation). A nominal GDP growth rate of close to 4% is thus the “new normal” compared to almost 6% before the financial crisis of 2008.

- Just as Larry Summers, I expect that nominal interest rates (and also real interest rates) will remain at extremely low levels or a significant amount of time. Global real interest rates have plunged for the last two decades and there is no reason to believe that this trend will reverse any time soon. I expect the Fed funds rate to be 0.75% by the end of next year and 1% by the end of 2017, following Kocherlakota and the Fed funds future market. Thereafter, “normalization" will occur to some extent and the interest rate will probably increase and remain in a range of about 2.5 to 3% for the years 2018-2020. Note that I am going out on a limb here with these projections since they are quite significantly lower than what any of the FED forecasts suggest. But I strongly believe that the FED is wrong again and that, on balance, financial markets get it right.

References:

Krugman on the negligible impact of a Chinese dumping of US treasuries:

- Krugman, P. (2014). Currency regimes, capital flows, and crises. IMF Economic Review, 62(4), 470-493.

Krugman on the liquidity trap:

- Krugman, P. R., Dominquez, K. M., & Rogoff, K. (1998). It's baaack: Japan's slump and the return of the liquidity trap. Brookings Papers on Economic Activity, 137-205.

Larry Summers on secular stagnation:

- Summers, L. H. (2014). US economic prospects: Secular stagnation, hysteresis, and the zero lower bound. Business Economics, 49(2), 65-73.

Lars Svensson on forescast targeting:

- Svensson, Lars EO, and Michael Woodford. "Implementing optimal policy through inflation-forecast targeting." The inflation-targeting debate. University of Chicago Press, 2004. 19-92.

RSS Feed

RSS Feed