The Eurozone's economic performance has been abysmal over the last decade while the U.S. has performed much better. The biggest difference has been monetary policy. The Fed, under the leadership of Ben Bernanke, started Quantitative Easing in 2010 while it took the ECB another 4 years to introduce a similar program. Furthermore, the ECB also started very prematurely a tightening cycle in 2011, hiking interest rates twice, which plunged the Eurozone back into recession and sparked the Eurozone debt crisis.

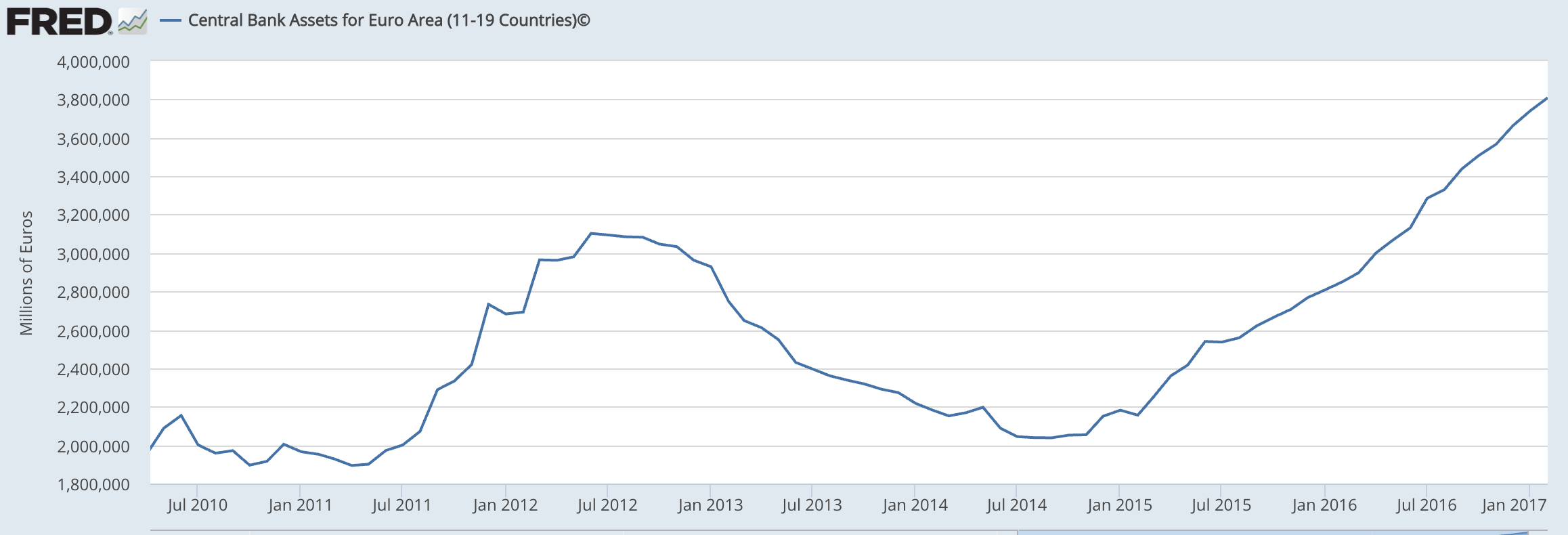

The ECB finally started to pull it together when Mario Draghi was appointed in 2011. Under his leadership, the ECB finally implemented a large-scale credit lending programs as well as an asset purchase programs aka Quantitative Easing. Finally, the ECB also introduced a negative interest rate on bank reserves.

The following chart shows the trajectory of real GDP since the financial crisis. Only in 2015 did the Eurozone reach its pre-crisis peak of 2007, 8 years of zero growth!

The ECB finally started to pull it together when Mario Draghi was appointed in 2011. Under his leadership, the ECB finally implemented a large-scale credit lending programs as well as an asset purchase programs aka Quantitative Easing. Finally, the ECB also introduced a negative interest rate on bank reserves.

The following chart shows the trajectory of real GDP since the financial crisis. Only in 2015 did the Eurozone reach its pre-crisis peak of 2007, 8 years of zero growth!

Economic growth finally resumed in 2014, or around the same time when the ECB started to ease monetary policy by a significant amount by dramatically expanding its balance sheet and cutting interest rates to the zero lower bound.

So now with a recovery finally on its way after almost a decade of stagnation, we also see that the inflation rate in the Eurozone is starting to approach the ECB's inflation target of 2%.

EUROZONE INFLATION RATE

And, surely enough, the German media, the German government, and the German populace is freaking out about it and demanding an end of the ECB's policy of "easy money", never mind that inflation rates have been at a historic low, and that both money growth (M3) and credit growth have been far lower than before the crisis.

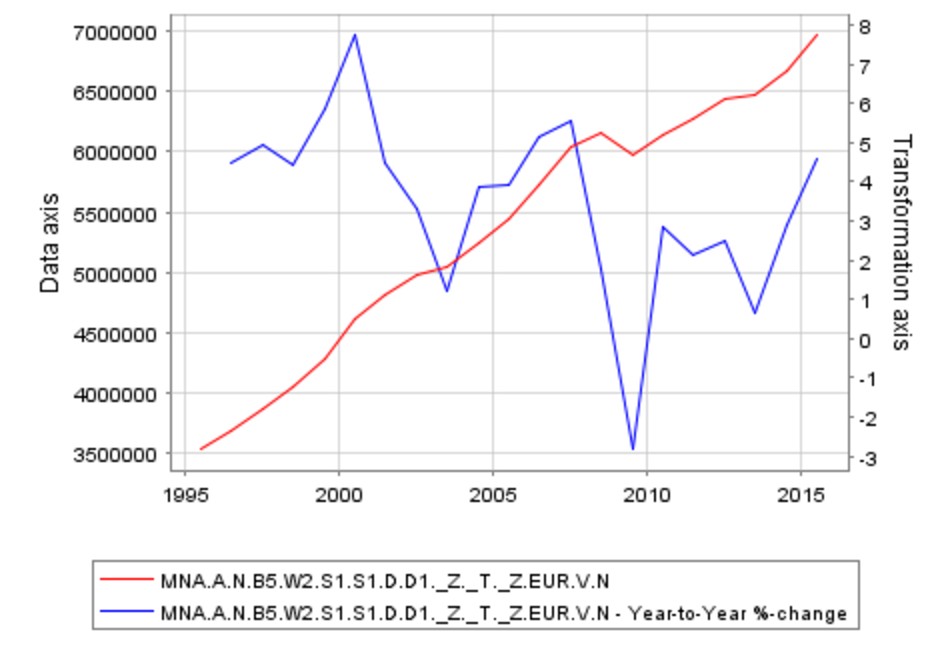

What people in Germany fail to understand is that a higher inflation rate is desperately actually desirable and should be welcomed. It shows that aggregate demand in the Eurozone is finally rising again. The increase in the inflation rate is not a result of higher commodity prices, which indeed would be bad, a but a result of higher demand. As the economy is approaching potential, prices and wages are starting to go up. The graph below shows that wage growth (blue line) is finally approaching a pre-crisis level. Rising wages is good news, obviously!

EUROZONE WAGE GROWTH

Total wages in billions of euros (red, left axis)

Yearly change (blue, right axis)

What people in Germany fail to understand is that a higher inflation rate is desperately actually desirable and should be welcomed. It shows that aggregate demand in the Eurozone is finally rising again. The increase in the inflation rate is not a result of higher commodity prices, which indeed would be bad, a but a result of higher demand. As the economy is approaching potential, prices and wages are starting to go up. The graph below shows that wage growth (blue line) is finally approaching a pre-crisis level. Rising wages is good news, obviously!

EUROZONE WAGE GROWTH

Total wages in billions of euros (red, left axis)

Yearly change (blue, right axis)

Germany is the one country where things are seen quite differently. In fact, Germany's previous and current governments have embraced an economic doctrine that can be characterized as mercantilism. Even though the concept of competitiveness is relatively meaningless when applied to entire countries, Germans have eagerly accepted the notion that Germany's current economic success is the result of its competitiveness.

It is true that the so-called Hartz reforms started during the Schröder government in the mid-2000s led to a period of wage stagnation, especially for workers at the bottom at the distribution. It is not entirely clear though why this is a good thing. In fact, this can be considered as a beggar-thy-neighbor policy within the Eurozone because unilateral wage restraints on the national level are not offset via changes in the exchange rate. It truly would be stupid to embrace a race to the bottom where every Eurozone country restricts wage growth in order to gain an edge vis-a-vis the rest of the currency area.

An additional negative sideeffect of Germany's policies has been a continuous increase in its current account. In 2016, Germany exported about 300 billion of goods and services more than it imported, which amounts to more than 8% of GDP. This is a disaster in the current period of secular stagnation. Higher domestic wage growth would most likely increase imports and hopefully also increase domestic investments, thus leading to a reduction in the current account and increasing global aggregate demand.

Finally, the current account surplus means that Germany is exporting capital in the amount of 300 billion to the rest of the world, effectively depressing global real interest rates. Draghi is not to blame for low real interest rates, but German savers are. Only higher domestic investment and restoring full employment in the Eurozone can bring about higher interest rates, the U.S. economy being the prime example thereof.

It is true that the so-called Hartz reforms started during the Schröder government in the mid-2000s led to a period of wage stagnation, especially for workers at the bottom at the distribution. It is not entirely clear though why this is a good thing. In fact, this can be considered as a beggar-thy-neighbor policy within the Eurozone because unilateral wage restraints on the national level are not offset via changes in the exchange rate. It truly would be stupid to embrace a race to the bottom where every Eurozone country restricts wage growth in order to gain an edge vis-a-vis the rest of the currency area.

An additional negative sideeffect of Germany's policies has been a continuous increase in its current account. In 2016, Germany exported about 300 billion of goods and services more than it imported, which amounts to more than 8% of GDP. This is a disaster in the current period of secular stagnation. Higher domestic wage growth would most likely increase imports and hopefully also increase domestic investments, thus leading to a reduction in the current account and increasing global aggregate demand.

Finally, the current account surplus means that Germany is exporting capital in the amount of 300 billion to the rest of the world, effectively depressing global real interest rates. Draghi is not to blame for low real interest rates, but German savers are. Only higher domestic investment and restoring full employment in the Eurozone can bring about higher interest rates, the U.S. economy being the prime example thereof.

RSS Feed

RSS Feed