Today’s issue of the ‘Financial Times’ had an article by Wolfgang Schäuble, the current German finance minister, with the title: “Ignore the doom-mongers – Europe is being fixed”. What he writes is so insanely wrong that I was really mad after reading it, and consequently decided to write this post.

The German government, and Schäuble in particular, still believe that austerity is a success story. Why? Because the Eurozone finally had one quarter of positive real GDP growth in the Eurozone (roughly +0.3%) for the first time since the beginning of 2011! Impressive!

Here is Schäuble:

The German government, and Schäuble in particular, still believe that austerity is a success story. Why? Because the Eurozone finally had one quarter of positive real GDP growth in the Eurozone (roughly +0.3%) for the first time since the beginning of 2011! Impressive!

Here is Schäuble:

“What is happening turns out to be pretty much what the proponents of Europe’s cool-headed crisis management predicted. The fiscal and structural repair work is paying off, laying the foundations for sustainable growth.”

I don’t know in what universe he is living in, but the definition of ‘success’ seems to be very different. The following graphs do not point to a success story in any sense of the word.

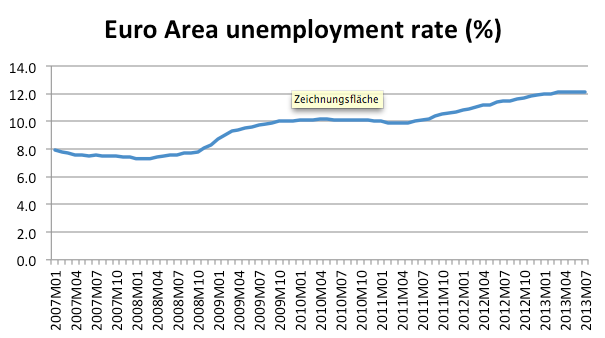

Here is the Euro Area unemployment rate, rising from 8% in 2007 to 12% in 2013. This figure even understates the extent of the problem since the unemployment rate does not take into account all the discouraged workers who have left the labor force because they would not be able to find a job anyways.

Here is the Euro Area unemployment rate, rising from 8% in 2007 to 12% in 2013. This figure even understates the extent of the problem since the unemployment rate does not take into account all the discouraged workers who have left the labor force because they would not be able to find a job anyways.

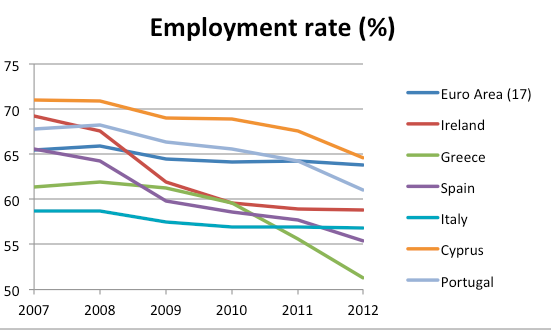

The following graph shows the decline in employment rate for the Eurozone and a selected number of ‘austerity countries’. The downward trend is evident for every country as well as for the Eurozone as a whole.

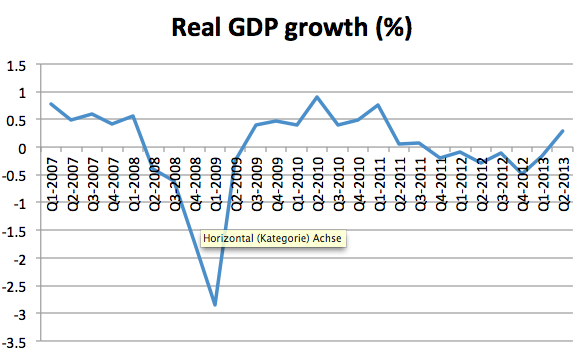

Next comes real GDP. One can see that Eurozone GDP did not grow in real terms right after the outbreak of the financial crisis in 2008/2009. Furthermore, real GDP growth was hardly positive afterwards and turned negative again from 2011 until 2013 as austerity measures started to kick in. Not really a success story either.

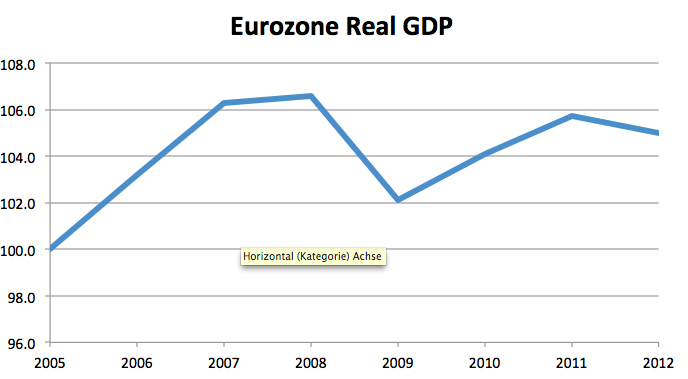

And below real GDP again as an index (2005 = base year). Note the astonishing performance since 2007.

Last but not least, the final graph shows the dramatic increase in government debt. For some countries, Spain and Ireland, the increase is partially the result of large bank bailouts. However, government debt has also increased as a result of austerity. This is ironic as the whole point of austerity was to reduce debt levels. If government multipliers are high and everything points towards the fact that they are really high in these times (see my 1st post), then spending cuts will lead to even higher reductions in GDP. As a result, the debt to GDP ratio actually increases. Austerity is then self-defeating: debt levels rise, unemployment soars, output levels remain depressed.

Then Schäuble goes on:

“This (the fact that, according to him, austerity works) has taken critical observers aback. It should not have, because, in truth, we have seen it all before, many times and in many places.” (Parenthesis added by me)

This is so wrong! Where and when did we see that austerity pays off? I am not aware of any sucessful austerity case in history. All countries in the Great Depression that pursued austerity policies performed so much worse than countries that engaged in expansionary monetary (and also fiscal) policies.

Sweden and the other Scandinavian countries, for example, left the gold standard early and could pursue expansionary monetary policies and thus performed much better than countries like France, which stayed on gold for much longer and experienced depressed output levels for several years.

The United States were basically pulled out of the Recession by the 2nd world war because government spending soared (as a share of GDP) as a result of increasing military expenditures.

He continues:

Sweden and the other Scandinavian countries, for example, left the gold standard early and could pursue expansionary monetary policies and thus performed much better than countries like France, which stayed on gold for much longer and experienced depressed output levels for several years.

The United States were basically pulled out of the Recession by the 2nd world war because government spending soared (as a share of GDP) as a result of increasing military expenditures.

He continues:

“…we live in the real world, not in a parallel universe where well-established economic principles no longer apply.”

I really have no clue what he is talking about here. The concept of the government multiplier is a well established fact in standard macroeconomics, even though some people desperately try to dismiss it (think 'Chicago school'). The evidence for high multipliers in recent times is overwhelming. The economic principle behind austerity on the other hand is totally dubious. There is no theory and even less evidence why and how it should work? Through which channels are austerity policies supposed to lead to higher growth?

Then Schäuble decides to bring up the most stupid examples one could possibly think of. He explains how Germany was the sick man of Europe with more than 5 million unemployed in the mid-200s. Through tough and painful structural reforms (the so-called Hartz reforms), however, the government was able to bring Germany back on the right track: labor market flexibility increased as well as ‘competitiveness’, unemployment benefits were cut, etc.

While it is true that these reforms in Germany were relatively successful, the context was completely different from today. Germany was able to implement these structural reforms in an environment of high economic growth: The mid-2000s were characterized by world output growth of roughly 4% as well as high growth rates in the Eurozone as a whole. The external conditions were thus very favorable and that is why Germany was able to implement these reforms in the first place.

The situation over the last couple of years, however, has been obviously very different. How are countries in Southern Europe supposed to implement structural reforms in the face of lower growth all around the world, and especially negative growth and mass unemployment in the Eurozone?

His second and third example about successful structural reforms is that of Sweden in the early 1990s (after its financial crisis) and Southeast Asia after the Asian crisis in 1997/1998. He completely ignores the fact that in both cases these cases the repsective countries had their own currencies. Consequently, expansionary monetary policy and massive currency devaluations were possible to stimualte aggregate demand. Obviously, the ‘PIIGS’ countries (Portugal, Ireland, Italy, Greece, and Spain) do not have this option since they do not possess their own currency anymore.

Schäuble also raises the issue of global competivenes. This German obsession with competiveness and exports is even sillier. It should be clear that not every country in the world can be a net exporter. Some countries must be net importers instead, thus consuming more than their income. This kind of imbalance, with some countries spending more than their income and others consuming less than their income, was one of the reasons why the crisis erupted and that got us into this mess in the first place. So I don’t exactly understand why Schäuble raises this issue. If he wants the PIIGS countries to significantly increase their exports, then some other countries have to buy their products. But who is it going to be? Aggregate demand is depressed in the entire Eurozone.

Then, in the end of his astonishing article Schäuble finally defines what he actually meant by success:

Then Schäuble decides to bring up the most stupid examples one could possibly think of. He explains how Germany was the sick man of Europe with more than 5 million unemployed in the mid-200s. Through tough and painful structural reforms (the so-called Hartz reforms), however, the government was able to bring Germany back on the right track: labor market flexibility increased as well as ‘competitiveness’, unemployment benefits were cut, etc.

While it is true that these reforms in Germany were relatively successful, the context was completely different from today. Germany was able to implement these structural reforms in an environment of high economic growth: The mid-2000s were characterized by world output growth of roughly 4% as well as high growth rates in the Eurozone as a whole. The external conditions were thus very favorable and that is why Germany was able to implement these reforms in the first place.

The situation over the last couple of years, however, has been obviously very different. How are countries in Southern Europe supposed to implement structural reforms in the face of lower growth all around the world, and especially negative growth and mass unemployment in the Eurozone?

His second and third example about successful structural reforms is that of Sweden in the early 1990s (after its financial crisis) and Southeast Asia after the Asian crisis in 1997/1998. He completely ignores the fact that in both cases these cases the repsective countries had their own currencies. Consequently, expansionary monetary policy and massive currency devaluations were possible to stimualte aggregate demand. Obviously, the ‘PIIGS’ countries (Portugal, Ireland, Italy, Greece, and Spain) do not have this option since they do not possess their own currency anymore.

Schäuble also raises the issue of global competivenes. This German obsession with competiveness and exports is even sillier. It should be clear that not every country in the world can be a net exporter. Some countries must be net importers instead, thus consuming more than their income. This kind of imbalance, with some countries spending more than their income and others consuming less than their income, was one of the reasons why the crisis erupted and that got us into this mess in the first place. So I don’t exactly understand why Schäuble raises this issue. If he wants the PIIGS countries to significantly increase their exports, then some other countries have to buy their products. But who is it going to be? Aggregate demand is depressed in the entire Eurozone.

Then, in the end of his astonishing article Schäuble finally defines what he actually meant by success:

“…In just three years, public deficits in Europe have halved, unit labour costs and competitiveness are rapidly adjusting, bank balance sheets are on the mend and current account deficits are disappearing...”

- It is no wonder that the cost of labor is now low in the PIIGS countries in the face of mass unemployment. This is just a matter of supply and demand.

- Current account deficits have indeed been rapidly falling in Southern Europe. This, however, is just the result of deeply depressed output levels. As people’s incomes have been falling rapidly, their consumption on foreign goods massively decreased as well, consequently leading to lower imports, and thus explaining lower current account deficits across the board in the Eurozone periphery.

It is thus fair to say that I am more than unhappy with Schäuble’s description of the situation! Austerity has done a great deal of harm allover Europe and it is incredible that some people still try to claim that these policies were successful. Given the upcoming German election it is, however, no wonder that the German government cannot admit that they have been wrong about almost everything since the outbreak of the Euro Crisis, whereas other people (think Krugman, DeLong) have been right about almost everything from the start.

I also want to emphasize that I do not argue against structural reforms. Especially the ‘PIIGS’ countries have to implement a lot of structural reforms. The point is that this would be much easier to accomplish in a favorable economic enviornment.

The Eurozone has been trapped in an aggregate demand crisis for more than 5 years now. It can only be solved by aggregate demand management.

One should also note that not only the governments are to blame for the current situation. The ECB has proven in recent years that it is one of the most conservative Central Bank in the World. It has done close to nothing to improve the economic situation in the Eurozone. The same could be said for the Bank of Japan (BOJ), where money has been extremely tight for almost 2 decades (since the bursting of the housing bubble in the early 90s). Last year, however, Japan started aggressively to ease monetary conditions, combined with a fiscal stimulus (the monetary stimulus is by far more important). Consequently, Japan experienced the highest real GDP growth rate of all G7 countries over the last year or so.

It turns out that expansionary policies really are expansionary! Who could have known? :D

It took the BOJ, however, 20 years to realize that 0% nominal interest rates do not imply easy money. This mistake led to two decades of anemic growth. My fear is that the ECB will continue to do what it has done over the last 5 years – basically nothing – and that it will behave in a very similar way to the BOJ. The current 1 quarter of barely positive GDP growth is meaningless. We are now 6 years into the crisis and Europe’s performance has been abyssal. One should not be surprised if we end up doing worse than Japan has ever done and in some respect we already do: the Japanes economy is structurally very different from ours and despite its 2 decades of poor growth Japan has never experienced substantial levels of unemployment (compared to what we have in the Eurozone right now).

- Current account deficits have indeed been rapidly falling in Southern Europe. This, however, is just the result of deeply depressed output levels. As people’s incomes have been falling rapidly, their consumption on foreign goods massively decreased as well, consequently leading to lower imports, and thus explaining lower current account deficits across the board in the Eurozone periphery.

It is thus fair to say that I am more than unhappy with Schäuble’s description of the situation! Austerity has done a great deal of harm allover Europe and it is incredible that some people still try to claim that these policies were successful. Given the upcoming German election it is, however, no wonder that the German government cannot admit that they have been wrong about almost everything since the outbreak of the Euro Crisis, whereas other people (think Krugman, DeLong) have been right about almost everything from the start.

I also want to emphasize that I do not argue against structural reforms. Especially the ‘PIIGS’ countries have to implement a lot of structural reforms. The point is that this would be much easier to accomplish in a favorable economic enviornment.

The Eurozone has been trapped in an aggregate demand crisis for more than 5 years now. It can only be solved by aggregate demand management.

One should also note that not only the governments are to blame for the current situation. The ECB has proven in recent years that it is one of the most conservative Central Bank in the World. It has done close to nothing to improve the economic situation in the Eurozone. The same could be said for the Bank of Japan (BOJ), where money has been extremely tight for almost 2 decades (since the bursting of the housing bubble in the early 90s). Last year, however, Japan started aggressively to ease monetary conditions, combined with a fiscal stimulus (the monetary stimulus is by far more important). Consequently, Japan experienced the highest real GDP growth rate of all G7 countries over the last year or so.

It turns out that expansionary policies really are expansionary! Who could have known? :D

It took the BOJ, however, 20 years to realize that 0% nominal interest rates do not imply easy money. This mistake led to two decades of anemic growth. My fear is that the ECB will continue to do what it has done over the last 5 years – basically nothing – and that it will behave in a very similar way to the BOJ. The current 1 quarter of barely positive GDP growth is meaningless. We are now 6 years into the crisis and Europe’s performance has been abyssal. One should not be surprised if we end up doing worse than Japan has ever done and in some respect we already do: the Japanes economy is structurally very different from ours and despite its 2 decades of poor growth Japan has never experienced substantial levels of unemployment (compared to what we have in the Eurozone right now).

RSS Feed

RSS Feed