I recently attended the conference “Piecing together a paradigm” at the European Central University in Budapest. The conference was organized by the Young Scholars Initiative (YSI) of the Institute for New Economic Thinking (INET), a research network that was founded by George Soros in the wake of the financial crisis. Soros, of course, is famously known for breaking the Bank of England during the European Exchange Rate Mechanism crisis in 1992. He founded the research network INET in the aftermath of the recent global financial crisis, which revealed some serious flaws in the current macroeconomic paradigm. The aim of INET and the Young Scholars Initiative is to bring together numerous economic researchers who operate to a certain extent outside the current mainstream of economic theory.

The event took off with a debate on helicopter money between Lord Adair Turner and Richard Koo, both of them being known for their somewhat unconventional views on the resolution of the current global economic stagnation. Koo is obviously famous for the invention of the term “balance sheet recession”. In his book “The holy grail of macreconomics” he describes in detail the economic disaster that struck the Japanese economy in the early 1990s after the burst of the real estate and stock market bubble. Koo argues that both the Great Depression of the 1930s in the U.S. as well as the Japanese experience in the 1990s are simply not normal recessions but balance sheet recessions instead. Koo shows how financial leverage in the private sector increased by an enormous amount in Japan in the buildup of the crisis. Both corporations as well as households increased their debt levels in tandem with the significant appreciation of their assets (real estate and stocks). With the bursting of the bubble, however, private sector liabilities suddenly exceeded private sector assets by a large amount. Private agents were suddenly highly indebted (in net terms) and tried to minimize their debt levels by all means possible. This is, according to Koo, the typical balance sheet recession. Firms stop maximizing profits, but instead start to minimize debt. The private sector goes into financial surplus. Current income streams are not used for investments anymore. Firms and households are trying to repair their balance sheets by paying back debt and building up financial assets as a buffer for the next economic downturn. Nominal GDP shrinks as a result of this behavior as private expenditures fall rapidly.

According to conventional macroeconomics, monetary policy is a powerful tool to fight recessions. Adjusting the level of interest rates and/or printing more money should be sufficient to prevent the economy from falling into a downward spiral. Demand-side recessions are a nominal problem that result from a sudden increase in the demand for money balances and other safe assets. Any shortfall in nominal expenditures can thus be easily repaired, according to the conventional view, by increasing the money stock in the economy by any means necessary. Classical macoreconomics thus literally suggests that dumping enough money at the problem will eventually lead to a fix.

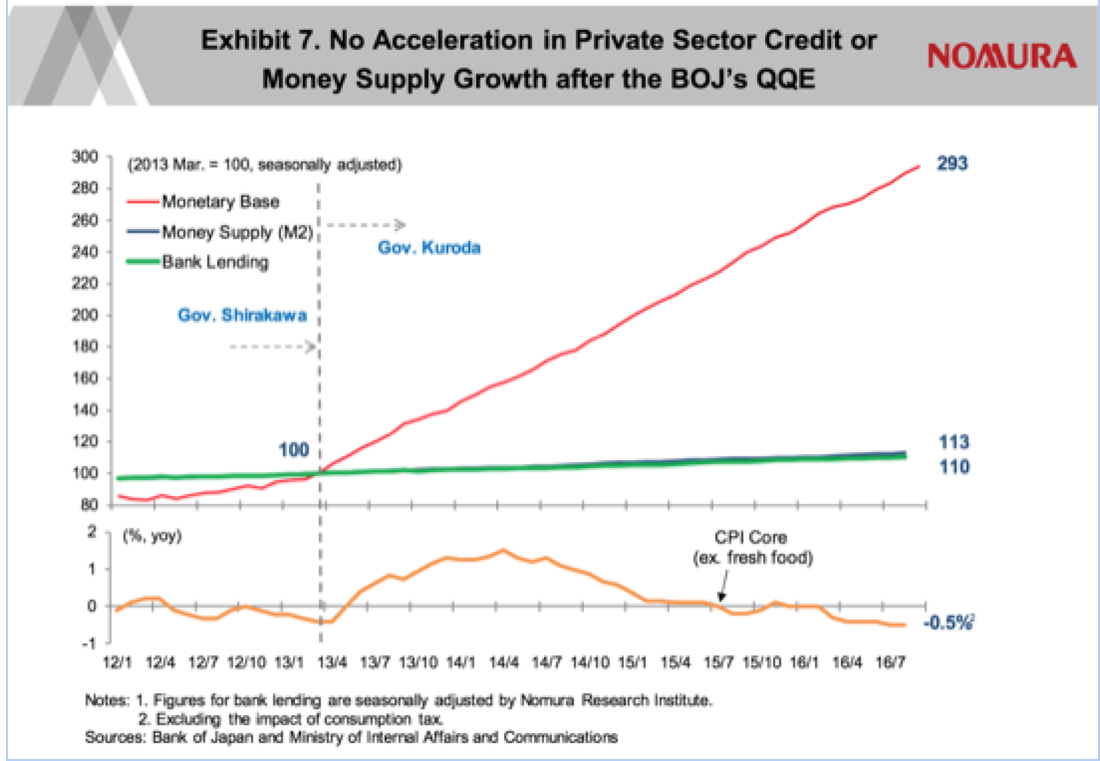

Koo, however, does not buy this argument. A decrease in the nominal interest would in normal times increase borrowing in the economy. In a balance sheet recession, however, there are simply not enough willing borrowers in the private sector as everybody attempts to minimize debt instead. Conventional monetary policy has lost all traction. The money multiplier is zero or even negative at margin as the amount of credit shrinks in the economy despite the Central Bank’s attempt to increase the money stock (see graph). Additional reserves are simply sitting in the banking system without being lent out. Koo argues that under such circumstance there is only one actor that can prevent the economy from going into free fall, that is the government. As the private sector goes into surplus, the public sector has to go into deficit by an equal amount in order to prevent a shortfall in nominal GDP. Furthermore, any attempt at austerity will be self-defeating. Interest rates on government bonds are extremely low in a balance sheet recession since private actors accumulate government debt as a safe asset. Under such circumstances, increased public expenditures are the only sensible thing to do. Austerity would only amplify the economic downturn and the debt to GDP ratio might ironically increase as nominal GDP falls faster than debt outstanding (see Delong and Summers[1] for more detail). The eurozone countries in Southern Europe provide the best example of such unfavorable debt dynamics.

While Koo is an adherent proponent of fiscal stimulus, he does not favor helicopter money for reasons that are not entirely clear to me. Helicopter money is fiscal stimulus that is financed by printing money instead of issuing debt. According to Koo, such a policy might lead to a dangerous path because it could involve substantially higher inflation rates down the road once the economy recovers from the balance sheet recession. However, this argument is somewhat inconsistent. His own analysis shows that the Japanese economy has been experiencing extremely slow nominal GDP growth for now almost 3 decades. Lawrence Summers once pointed out in response to a question of mine[2] that helicopter money is nothing else than a combination of Quantitative Easing (increases in the amount of base money) and fiscal stimulus, which is exactly what has already been happening in Japan. The program of “Abenomics”, which was launched in late 2012, after all involves massive amounts of monetary stimulus combined with modest fiscal expansion. While the policy ended two decades of Japanese deflation and achieved an increase in nominal GDP, the effects of the massive stimulus were not as large as some proponents expected them to be.

Lord Adair Turner points out that monetary finance, the financing of public expenditures by printing money, is already a reality in Japan. While the country’s debt to GDP ratio is the highest in the world at about 230%, the Bank of Japan now owns Japanese debt equivalent to 80% of GDP and this ratio will only increase at the current pace of bond purchases. So helicopter money is in a way already pursued by Japanese policy makers. Its impact on nominal demand, however, has been relatively modest. This in contrast to the claims of Lord Turner who argues that a drop of helicopter money into the economy, provided it is sufficiently large, should always be effective in stimulating nominal GDP. This is the classical Friedmanite [3] argument that somebody simply must pick up the additional money and will put it into circulation by buying stuff, which will increase the total amount of expenditures in the economy. Some modern Keynesians, however, have disputed the notion that helicopter money will always be effective. Paul Krugman[4] famously argued that monetary policy in a liquidity trap with interest rates stuck at the zero-lower bound is only works if the increases in the money stock are perceived as permanent. If somebody gave me a hundred bucks today but told me he will take it away from me again in two weeks from now, I probably would not change my behavior as a result since my net worth is also unchanged. Similarly, temporary increases in the money supply should have no substantial effect on output and prices since everybody expects that the Central Bank’s operations are reversed in the foreseeable future. Instead, the Central Bank must credibly promise to be irresponsible and explicitly aim for higher inflation down the road[5].

Richard Koo’s distaste for helicopter money is thus somewhat puzzling. It seems to rely on the notion of strong non-linearities. He seems to suggest that a helicopter drop could suddenly lead to high and rapid inflation rates once the economy recovers from the balance sheet recession. Banks would suddenly lent out all their excess reserves that have accumulated in the banking system as soon as borrowers have repaired their balance sheets and are willing to take on new debt again. Excess reserves in Japan, for example, are currently about 30 times required reserves, suggesting that private sector credit could theoretically grow by a similar amount. In practice, however, we simply have not observed a situation in advanced economies in recent times where there is an almost instantaneous regime switch from a low-pressure economy to a high-pressure economy in which inflation cannot be kept in check. Koo simply does not present any convincing evidence or theoretical framework that would explain why a Central Bank would be unable to prevent an economy from overheating. The Volcker disinflation of the 1980s surely shows that a Central Bank can always hike interest rates rapidly enough and pursue a policy of sufficiently tight money that could put an end to any inflationary boom.

In that sense, the ideas of Lord Adair Turner seems to be more convincing to me. Given the recent shortfalls in nominal demand, technocrats in Central Banks should be able to design helicopter drops in incremental steps that would just hit the sweet spot if you will, sufficiently large to raise aggregate demand but not large enough to create an inflationary boom. There is little doubt in my mind that Central Banks, by carefully assessing asset markets and labor market indicators, always have the capability of preventing an economy from overheating before such an outcome would occur. Non-linearities where the inflation rate suddenly jumps by a large amount are relatively unlikely.

However, the debate between Richard Koo and Lord Turner was missing one key ingredient. Helicopter money is simply a monetary policy tool to raise aggregate demand. Much more important, however, is the debate on monetary regimes. Delong and Summers[6] already explained in 1992 that a 2% inflation target might give Central Banks not enough levy room to lower interest rates in the case of an significant adverse macroeconomic shock. The recent years with most Central Banks being constrained by the zero-lower bound have forcefully vindicated this view. Furthermore, the 2% inflation target represents a significant constraint on monetary policy. Central Banks have made it abundantly clear in recent years that they are unwilling to overshoot their inflation target. As explained above, this unwillingness might render helicopter money virtually ineffective if the monetary expansion is only perceived as temporary.

Many monetary theorists have now accepted the view that alternative monetary regimes might not only provide more accommodation right now but also might be better at smoothing the business cycle in general. Targeting the level of nominal GDP or even the level of nominal wages would in all likelihood stabilize employment fluctuations and GDP fluctuations to a much greater extent, thus taming if not completely eliminating the business cycle[7]. The only reason why we have a 2% inflation target in the first place is because the Bank of New Zealand adopted it in 1990 and many other Central Banks simply followed suit in the years thereafter. However, there was never any convincing theoretical or empirical justification for a 2% inflation target to begin with. The debate on helicopter money, as important as it is in the current low-growth and low-inflation rate environment, is in my mind only secondary. The real debate we should be having, an issue that the two discussants completely failed to address, is whether Central Banks should adopt an alternative monetary regime. Unfortunately it seems like the 2% inflation target is set in stone. Policy makers and Central Bankers have not accepted the reality yet that their current monetary framework has failed them in recent years. We have now experienced almost a decade of subpar economic performance and historically low global real interest rates. Financial markets predict that we will not escape this environment of secular stagnation for many years[8]. Central Bankers are setting themselves up for failure for years to come by not accepting how dire the situation really is. A change in the current operating framework of Central Banks is desperately needed, but unlikely to happen. In the meantime we all will have to live with the adverse consequences of policy failure, such as abysmal economic performance, elevated unemployment, populist movements, and the backlash against globalization. 1930s, anyone?

[1] DeLong, J. Bradford, and Lawrence H. Summers. "Fiscal policy in a depressed economy." Brookings Papers on Economic Activity 2012.1 (2012): 233-297.

[2] See the video on secular stagnation. My question to Larry Summers on helicopter money and different monetary targets starts at minute 57: http://www.diw.de/sixcms/detail.php?m=Video&y=2015&r=Veranstaltung&action=anwenden&gsid=diw_01.c.439035.de&id=439035&skip=18

[3] https://www.brookings.edu/blog/ben-bernanke/2016/04/11/what-tools-does-the-fed-have-left-part-3-helicopter-money/

[4] See Krugman, Paul R., Kathryn M. Dominquez, and Kenneth Rogoff. "It's baaack: Japan's slump and the return of the liquidity trap." Brookings Papers on Economic Activity 1998.2 (1998): 137-205.

[5] http://web.mit.edu/krugman/www/japtrap.html

[6] De Long, J. Bradford, and Lawrence H. Summers. "Macroeconomic policy and long-run growth." Economic Review-Federal Reserve Bank of Kansas City 77.4 (1992): 5.

[7] See this discussion on different monetary policy targets: http://www.cbpp.org/research/full-employment/monetary-rules-and-targets-finding-the-best-path-to-full-employment

[8] Summers, Laurence H. "Reflections on the ‘New Secular Stagnation Hypothesis’." Secular stagnation: Facts, causes and cures (2014): 27-40.

The event took off with a debate on helicopter money between Lord Adair Turner and Richard Koo, both of them being known for their somewhat unconventional views on the resolution of the current global economic stagnation. Koo is obviously famous for the invention of the term “balance sheet recession”. In his book “The holy grail of macreconomics” he describes in detail the economic disaster that struck the Japanese economy in the early 1990s after the burst of the real estate and stock market bubble. Koo argues that both the Great Depression of the 1930s in the U.S. as well as the Japanese experience in the 1990s are simply not normal recessions but balance sheet recessions instead. Koo shows how financial leverage in the private sector increased by an enormous amount in Japan in the buildup of the crisis. Both corporations as well as households increased their debt levels in tandem with the significant appreciation of their assets (real estate and stocks). With the bursting of the bubble, however, private sector liabilities suddenly exceeded private sector assets by a large amount. Private agents were suddenly highly indebted (in net terms) and tried to minimize their debt levels by all means possible. This is, according to Koo, the typical balance sheet recession. Firms stop maximizing profits, but instead start to minimize debt. The private sector goes into financial surplus. Current income streams are not used for investments anymore. Firms and households are trying to repair their balance sheets by paying back debt and building up financial assets as a buffer for the next economic downturn. Nominal GDP shrinks as a result of this behavior as private expenditures fall rapidly.

According to conventional macroeconomics, monetary policy is a powerful tool to fight recessions. Adjusting the level of interest rates and/or printing more money should be sufficient to prevent the economy from falling into a downward spiral. Demand-side recessions are a nominal problem that result from a sudden increase in the demand for money balances and other safe assets. Any shortfall in nominal expenditures can thus be easily repaired, according to the conventional view, by increasing the money stock in the economy by any means necessary. Classical macoreconomics thus literally suggests that dumping enough money at the problem will eventually lead to a fix.

Koo, however, does not buy this argument. A decrease in the nominal interest would in normal times increase borrowing in the economy. In a balance sheet recession, however, there are simply not enough willing borrowers in the private sector as everybody attempts to minimize debt instead. Conventional monetary policy has lost all traction. The money multiplier is zero or even negative at margin as the amount of credit shrinks in the economy despite the Central Bank’s attempt to increase the money stock (see graph). Additional reserves are simply sitting in the banking system without being lent out. Koo argues that under such circumstance there is only one actor that can prevent the economy from going into free fall, that is the government. As the private sector goes into surplus, the public sector has to go into deficit by an equal amount in order to prevent a shortfall in nominal GDP. Furthermore, any attempt at austerity will be self-defeating. Interest rates on government bonds are extremely low in a balance sheet recession since private actors accumulate government debt as a safe asset. Under such circumstances, increased public expenditures are the only sensible thing to do. Austerity would only amplify the economic downturn and the debt to GDP ratio might ironically increase as nominal GDP falls faster than debt outstanding (see Delong and Summers[1] for more detail). The eurozone countries in Southern Europe provide the best example of such unfavorable debt dynamics.

While Koo is an adherent proponent of fiscal stimulus, he does not favor helicopter money for reasons that are not entirely clear to me. Helicopter money is fiscal stimulus that is financed by printing money instead of issuing debt. According to Koo, such a policy might lead to a dangerous path because it could involve substantially higher inflation rates down the road once the economy recovers from the balance sheet recession. However, this argument is somewhat inconsistent. His own analysis shows that the Japanese economy has been experiencing extremely slow nominal GDP growth for now almost 3 decades. Lawrence Summers once pointed out in response to a question of mine[2] that helicopter money is nothing else than a combination of Quantitative Easing (increases in the amount of base money) and fiscal stimulus, which is exactly what has already been happening in Japan. The program of “Abenomics”, which was launched in late 2012, after all involves massive amounts of monetary stimulus combined with modest fiscal expansion. While the policy ended two decades of Japanese deflation and achieved an increase in nominal GDP, the effects of the massive stimulus were not as large as some proponents expected them to be.

Lord Adair Turner points out that monetary finance, the financing of public expenditures by printing money, is already a reality in Japan. While the country’s debt to GDP ratio is the highest in the world at about 230%, the Bank of Japan now owns Japanese debt equivalent to 80% of GDP and this ratio will only increase at the current pace of bond purchases. So helicopter money is in a way already pursued by Japanese policy makers. Its impact on nominal demand, however, has been relatively modest. This in contrast to the claims of Lord Turner who argues that a drop of helicopter money into the economy, provided it is sufficiently large, should always be effective in stimulating nominal GDP. This is the classical Friedmanite [3] argument that somebody simply must pick up the additional money and will put it into circulation by buying stuff, which will increase the total amount of expenditures in the economy. Some modern Keynesians, however, have disputed the notion that helicopter money will always be effective. Paul Krugman[4] famously argued that monetary policy in a liquidity trap with interest rates stuck at the zero-lower bound is only works if the increases in the money stock are perceived as permanent. If somebody gave me a hundred bucks today but told me he will take it away from me again in two weeks from now, I probably would not change my behavior as a result since my net worth is also unchanged. Similarly, temporary increases in the money supply should have no substantial effect on output and prices since everybody expects that the Central Bank’s operations are reversed in the foreseeable future. Instead, the Central Bank must credibly promise to be irresponsible and explicitly aim for higher inflation down the road[5].

Richard Koo’s distaste for helicopter money is thus somewhat puzzling. It seems to rely on the notion of strong non-linearities. He seems to suggest that a helicopter drop could suddenly lead to high and rapid inflation rates once the economy recovers from the balance sheet recession. Banks would suddenly lent out all their excess reserves that have accumulated in the banking system as soon as borrowers have repaired their balance sheets and are willing to take on new debt again. Excess reserves in Japan, for example, are currently about 30 times required reserves, suggesting that private sector credit could theoretically grow by a similar amount. In practice, however, we simply have not observed a situation in advanced economies in recent times where there is an almost instantaneous regime switch from a low-pressure economy to a high-pressure economy in which inflation cannot be kept in check. Koo simply does not present any convincing evidence or theoretical framework that would explain why a Central Bank would be unable to prevent an economy from overheating. The Volcker disinflation of the 1980s surely shows that a Central Bank can always hike interest rates rapidly enough and pursue a policy of sufficiently tight money that could put an end to any inflationary boom.

In that sense, the ideas of Lord Adair Turner seems to be more convincing to me. Given the recent shortfalls in nominal demand, technocrats in Central Banks should be able to design helicopter drops in incremental steps that would just hit the sweet spot if you will, sufficiently large to raise aggregate demand but not large enough to create an inflationary boom. There is little doubt in my mind that Central Banks, by carefully assessing asset markets and labor market indicators, always have the capability of preventing an economy from overheating before such an outcome would occur. Non-linearities where the inflation rate suddenly jumps by a large amount are relatively unlikely.

However, the debate between Richard Koo and Lord Turner was missing one key ingredient. Helicopter money is simply a monetary policy tool to raise aggregate demand. Much more important, however, is the debate on monetary regimes. Delong and Summers[6] already explained in 1992 that a 2% inflation target might give Central Banks not enough levy room to lower interest rates in the case of an significant adverse macroeconomic shock. The recent years with most Central Banks being constrained by the zero-lower bound have forcefully vindicated this view. Furthermore, the 2% inflation target represents a significant constraint on monetary policy. Central Banks have made it abundantly clear in recent years that they are unwilling to overshoot their inflation target. As explained above, this unwillingness might render helicopter money virtually ineffective if the monetary expansion is only perceived as temporary.

Many monetary theorists have now accepted the view that alternative monetary regimes might not only provide more accommodation right now but also might be better at smoothing the business cycle in general. Targeting the level of nominal GDP or even the level of nominal wages would in all likelihood stabilize employment fluctuations and GDP fluctuations to a much greater extent, thus taming if not completely eliminating the business cycle[7]. The only reason why we have a 2% inflation target in the first place is because the Bank of New Zealand adopted it in 1990 and many other Central Banks simply followed suit in the years thereafter. However, there was never any convincing theoretical or empirical justification for a 2% inflation target to begin with. The debate on helicopter money, as important as it is in the current low-growth and low-inflation rate environment, is in my mind only secondary. The real debate we should be having, an issue that the two discussants completely failed to address, is whether Central Banks should adopt an alternative monetary regime. Unfortunately it seems like the 2% inflation target is set in stone. Policy makers and Central Bankers have not accepted the reality yet that their current monetary framework has failed them in recent years. We have now experienced almost a decade of subpar economic performance and historically low global real interest rates. Financial markets predict that we will not escape this environment of secular stagnation for many years[8]. Central Bankers are setting themselves up for failure for years to come by not accepting how dire the situation really is. A change in the current operating framework of Central Banks is desperately needed, but unlikely to happen. In the meantime we all will have to live with the adverse consequences of policy failure, such as abysmal economic performance, elevated unemployment, populist movements, and the backlash against globalization. 1930s, anyone?

[1] DeLong, J. Bradford, and Lawrence H. Summers. "Fiscal policy in a depressed economy." Brookings Papers on Economic Activity 2012.1 (2012): 233-297.

[2] See the video on secular stagnation. My question to Larry Summers on helicopter money and different monetary targets starts at minute 57: http://www.diw.de/sixcms/detail.php?m=Video&y=2015&r=Veranstaltung&action=anwenden&gsid=diw_01.c.439035.de&id=439035&skip=18

[3] https://www.brookings.edu/blog/ben-bernanke/2016/04/11/what-tools-does-the-fed-have-left-part-3-helicopter-money/

[4] See Krugman, Paul R., Kathryn M. Dominquez, and Kenneth Rogoff. "It's baaack: Japan's slump and the return of the liquidity trap." Brookings Papers on Economic Activity 1998.2 (1998): 137-205.

[5] http://web.mit.edu/krugman/www/japtrap.html

[6] De Long, J. Bradford, and Lawrence H. Summers. "Macroeconomic policy and long-run growth." Economic Review-Federal Reserve Bank of Kansas City 77.4 (1992): 5.

[7] See this discussion on different monetary policy targets: http://www.cbpp.org/research/full-employment/monetary-rules-and-targets-finding-the-best-path-to-full-employment

[8] Summers, Laurence H. "Reflections on the ‘New Secular Stagnation Hypothesis’." Secular stagnation: Facts, causes and cures (2014): 27-40.

Source: Richard Koo’s presentation at the INET conference in Budapest.

RSS Feed

RSS Feed