One of the most hotly debated topics in macroeconomics is about the role of fiscal policy as a tool for macroeconomic stabilization and the size of the government multiplier. The discussion is not only very controversial but also very context specific. In particular, the fiscal multiplier depends crucially on the state of the economy, but even more so on the monetary policy regime.

The Great Moderation, the period from the mid 1980s until 2007, has been a period of macroeconomic stability for most of the developed countries as both inflation and output volatility have been much lower than in the preceding decades. This favorable outcome has been achieved by successful monetary policy. It is uncontroversial that monetary policy has been at least since the 1980s the main driver of macroeconomic stability.

During the Great Moderation fiscal policy was only responsible for macroeconomic outcomes insofar as it would determine the supply side of the economy. Fiscal policy was thus limited to issues such as taxation policies, health care policies, pension schemes, etc. All these issues affect the growth path of an economy mostly via the supply side. Fiscal policy, however, did not have any useful role to play in macroeconomic stabilization since that was solely determined by the Central Bank.

The following statement thus should be relatively uncontroversial:

The fiscal multiplier crucially depends on the monetary regime and the reaction function of the Central Bank. Furthermore, monetary policy regimes such as inflation targeting and nominal GDP targeting will usually result in a fiscal multiplier that is (and should be) 0.

In normal times, the fiscal multiplier will be 0 under a regime of inflation targeting (or NGDP targeting) because the Central Bank will engage in full monetary offset. That is, any government expenditures raising aggregate demand will result in monetary tightening whereas any fiscal contraction depressing aggregate demand will result in monetary expansion.

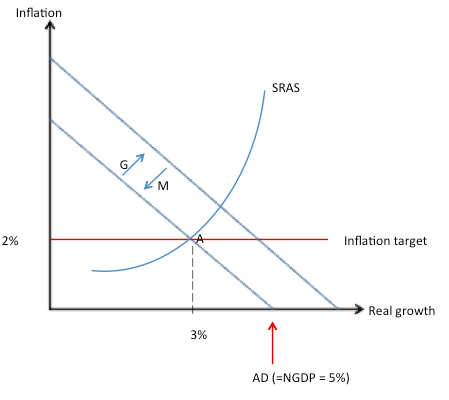

The concept of the 0 fiscal multiplier is easy to see in the Cowen/Tabarrok AS-AD framework. We assume that the economy starts at a point where NGDP is growing at 5%. NGDP is split up such that 3% is real growth and 2% is inflation (in accordance with the Central Banks inflation target). The economy is thus at point A depicted in the graph below.

The Great Moderation, the period from the mid 1980s until 2007, has been a period of macroeconomic stability for most of the developed countries as both inflation and output volatility have been much lower than in the preceding decades. This favorable outcome has been achieved by successful monetary policy. It is uncontroversial that monetary policy has been at least since the 1980s the main driver of macroeconomic stability.

During the Great Moderation fiscal policy was only responsible for macroeconomic outcomes insofar as it would determine the supply side of the economy. Fiscal policy was thus limited to issues such as taxation policies, health care policies, pension schemes, etc. All these issues affect the growth path of an economy mostly via the supply side. Fiscal policy, however, did not have any useful role to play in macroeconomic stabilization since that was solely determined by the Central Bank.

The following statement thus should be relatively uncontroversial:

The fiscal multiplier crucially depends on the monetary regime and the reaction function of the Central Bank. Furthermore, monetary policy regimes such as inflation targeting and nominal GDP targeting will usually result in a fiscal multiplier that is (and should be) 0.

In normal times, the fiscal multiplier will be 0 under a regime of inflation targeting (or NGDP targeting) because the Central Bank will engage in full monetary offset. That is, any government expenditures raising aggregate demand will result in monetary tightening whereas any fiscal contraction depressing aggregate demand will result in monetary expansion.

The concept of the 0 fiscal multiplier is easy to see in the Cowen/Tabarrok AS-AD framework. We assume that the economy starts at a point where NGDP is growing at 5%. NGDP is split up such that 3% is real growth and 2% is inflation (in accordance with the Central Banks inflation target). The economy is thus at point A depicted in the graph below.

Any fiscal expansion would thus lead to a rightward shift in aggregate demand (AD) pushing the economy on a higher nominal GDP growth rate. Due to the upward-sloping short-run aggregate supply (SRAS) curve the increase in aggregate demand would also lead to a higher inflation rate. This, however, contradicts the inflation target of the Central Bank, which will in turn raise interest rates in order to get aggregate demand back on track. This raise in interest rates will effectively crowd out some private consumption and investment. The Central Bank’s strict adherence to the 2% inflation rule thus effectively leads to a 0 fiscal multiplier.

Obviously, this argument also works in the other direction. Spending cuts by the government lead to a reduction in AD. In response, the Central Bank lowers the interest rate. The cut in rates will lead to higher borrowing and increased consumption levels and investment in the private sector. Again, the fiscal multiplier is 0 as the Central Bank offsets the spending cuts that take place in the public sector in order to keep inflation at its target.

This mechanism, however, breaks down at the Zero-lower bound (ZLB), a situation where the Central Bank cannot reduce its interest rate anymore in order to stimulate the economy because the rate is already at 0.

This is effectively the situation we have experienced over the last couple of years where the Central Banks’ rate is set at 0 and the economy is deeply depressed.

DeLong and Summers, and many others argue that the fiscal multiplier is in such a situation potentially very large because the Central Bank does not engage in monetary offset anymore. There is another hotly debated discussion about the potency of monetary policy at the ZLB. Market monetarists, such as Sumner, argue that the FED should never run out of ammunition and that the right monetary regime (NGDP targeting) could eliminate the ZLB constraint altogether. This is a discussion for another time. A lot of evidence, however, supports the hypothesis that the ZLB has represented a significant constraint for the FED over the last couple of years. That is because monetary policy makers are apparently worried about several issues other than price stability and maximum employment when at the ZLB. These worries are amongst others:

- The fear of inflation as a result of Quantitative Easing (QE) and other unconventional policies even though theory (see Krugman’s paper about Japan) predicts that inflation will remain low in a liquidity trap environment. Furthermore, markets predicted low inflation all along (see TIPS spreads) and have provided better forecasts than the FED’s inflation estimates that have constantly been too high in recent years.

- The fear of asset bubbles in a low interest rate environment even though there does not seem to be a lot of evidence to support this hypothesis (one could look at P/E ratios of stocks and related measures to see whether asset prices are excessively high). Also it is not clear how asset bubbles can form in a high unemployment economy since such bubbles normally are created in a full-employment economy where overconfidence and optimism dominate investor behavior – hardly the environment we have right now.

- The fear of overblown balanced sheets and related losses. The acquisition of billions of assets as a result of QE has led to a very large balance sheet of the FED. Central Bankers seem to worry about potential future losses. Such losses (at least one paper) could occur as interest rates pick up again when the economy recovers (that is because bond prices move inversely to the interest rate). These fears, however, seem to be blown out of proportion. It is noteworthy that the FED actually paid substantial amounts to the Treasury (in the magnitude of dozens of billions of $) over the last couple of years as a result of the accrued interest on their enormous bond holdings. This will make it easier for the FED to justify any future losses. Also the FED is not a for-profit organization. It should stabilize inflation and employment and ensure financial stability, and that’s it.

- The fear of distorted financial markets. Some arguments have been made that the continuous purchase of assets by the FED could lead to distortions in financial markets. I have not yet read any supportive evidence in favor of this view. But even if that view were correct, the question arises to what extent these distortions matter in the face of a low-inflation/high unemployment economic environment.

Effectively, all these fears made the FED to engage in too little monetary stimulus in order to achieve a full and substantiated recovery: Inflation levels have been low and unemployment has been devastatingly high since 2008 as a result of too little aggregate demand.

Furthermore, the fiscal multiplier is certainly above 0 in such an environment. Any reduction in aggregate demand by the government would in this case not be offset to 100% by the Central Bank with additional unconventional monetary policies because Central Banks feel uncomfortable employing these tools.

This is definitely the environment that has dominated the periphery of the Eurozone over the last couple of years. The ECB has been unwilling to keep aggregate demand (nominal spending) on track. The drop in nominal GDP in many Southern European countries led to highly elevated levels of unemployment and deeply depressed levels of real output. The situation was aggravated by fiscal consolidation. Government multipliers were high because the ECB has been unwilling to offset any reduction in nominal spending caused by fiscal austerity. Consequently, these reductions in government expenditures led to even higher unemployment levels and output losses, and ironically also higher debt levels. That is because with a high fiscal multiplier the reduction in GDP is greater than the reduction in debt, thus increasing the debt/GDP ratio instead of reducing it. If the whole point of fiscal austerity was thus to reduce debt levels, then the policy failed completely as it actually increased debt ratios in the Eurozone periphery.

DeLong and Summers actually even go further than this. They explain in their paper that fiscal multipliers have been reasonably large. Indeed, they cite the IMF and other authors who found out that the fiscal multiplier at the ZLB could be well above 1. There is, however, large uncertainty about its actual value and it could range from 1 to values like 2.5. Again, it is crucial to note that the fiscal multiplier is very context specific as it depends on the reaction function of the Central Bank, which will determine to what extent it will offset any increase in aggregate demand from government spending.

DeLong and Summers provide a model that explains how under certain conditions and reasonable assumptions about hysteresis effects (that is to what extent a current recession has negative effects on future output) government spending could even be self-financing. They explain that with sufficiently large values for both the multiplier and the hysteresis effects any increased government spending would not raise the debt level. That is because increased aggregate demand raises current production and thus today’s tax revenues and it also leads to a future-period boosts to potential output since a smaller recession now decreases hysteresis effects, thus increasing future tax revenues as well.

The assumption of self-financing stimulus seems to be too good to be true. It would be a free lunch and certainly only exists under the special circumstances mentioned above. Nonetheless, even if expansionary spending raises current debt levels to a certain extent, expansionary fiscal policies could easily pass a sensible Benefit-Cost test. The costs of a recession and high unemployment levels potentially cast a big shadow on future output. That is because workers might get discouraged, which makes them permanently quit the labor force and loose their human capital. Young workers might have trouble beginning their career due to elevated levels of youth unemployment, affecting their career paths and lifetime incomes. These and other mechanism suggest that fiscal policy can and should play a stabilization role in case monetary policy is unable or unwilling to do so.

Recent events in Southern Europe certainly prove that fiscal multipliers can be large at times. Based on these facts, the premise that the FED will and always can offset any fiscal consolidation seems to be flawed. Specifically, Bernanke testified before Congress that the spending cuts imposed by the sequester might hurt the economy, leading to lower growth and higher unemployment (compared to a situation without these cuts). Bernanke thus specifically told Congress that the FED has indeed not fully offset government spending cuts recently and that the multiplier is above 0 right now.

References:

Bernanke on the Great Moderation:

http://www.federalreserve.gov/boarddocs/speeches/2004/20040220/

DeLong and Summers on Fiscal policy at the ZLB (pdf):

http://www.brookings.edu/~/media/Projects/BPEA/Spring%202012/2012a_DeLong.pdf

Krugman on the liquidity trap in Japan (pdf):

http://www.brookings.edu/~/media/projects/bpea/1998%202/1998b_bpea_krugman_dominquez_rogoff.pdf

Summers on nominal GDP targeting (pdf):

http://mercatus.org/sites/default/files/NGDP_Sumner_v-10-copy.pdf

Obviously, this argument also works in the other direction. Spending cuts by the government lead to a reduction in AD. In response, the Central Bank lowers the interest rate. The cut in rates will lead to higher borrowing and increased consumption levels and investment in the private sector. Again, the fiscal multiplier is 0 as the Central Bank offsets the spending cuts that take place in the public sector in order to keep inflation at its target.

This mechanism, however, breaks down at the Zero-lower bound (ZLB), a situation where the Central Bank cannot reduce its interest rate anymore in order to stimulate the economy because the rate is already at 0.

This is effectively the situation we have experienced over the last couple of years where the Central Banks’ rate is set at 0 and the economy is deeply depressed.

DeLong and Summers, and many others argue that the fiscal multiplier is in such a situation potentially very large because the Central Bank does not engage in monetary offset anymore. There is another hotly debated discussion about the potency of monetary policy at the ZLB. Market monetarists, such as Sumner, argue that the FED should never run out of ammunition and that the right monetary regime (NGDP targeting) could eliminate the ZLB constraint altogether. This is a discussion for another time. A lot of evidence, however, supports the hypothesis that the ZLB has represented a significant constraint for the FED over the last couple of years. That is because monetary policy makers are apparently worried about several issues other than price stability and maximum employment when at the ZLB. These worries are amongst others:

- The fear of inflation as a result of Quantitative Easing (QE) and other unconventional policies even though theory (see Krugman’s paper about Japan) predicts that inflation will remain low in a liquidity trap environment. Furthermore, markets predicted low inflation all along (see TIPS spreads) and have provided better forecasts than the FED’s inflation estimates that have constantly been too high in recent years.

- The fear of asset bubbles in a low interest rate environment even though there does not seem to be a lot of evidence to support this hypothesis (one could look at P/E ratios of stocks and related measures to see whether asset prices are excessively high). Also it is not clear how asset bubbles can form in a high unemployment economy since such bubbles normally are created in a full-employment economy where overconfidence and optimism dominate investor behavior – hardly the environment we have right now.

- The fear of overblown balanced sheets and related losses. The acquisition of billions of assets as a result of QE has led to a very large balance sheet of the FED. Central Bankers seem to worry about potential future losses. Such losses (at least one paper) could occur as interest rates pick up again when the economy recovers (that is because bond prices move inversely to the interest rate). These fears, however, seem to be blown out of proportion. It is noteworthy that the FED actually paid substantial amounts to the Treasury (in the magnitude of dozens of billions of $) over the last couple of years as a result of the accrued interest on their enormous bond holdings. This will make it easier for the FED to justify any future losses. Also the FED is not a for-profit organization. It should stabilize inflation and employment and ensure financial stability, and that’s it.

- The fear of distorted financial markets. Some arguments have been made that the continuous purchase of assets by the FED could lead to distortions in financial markets. I have not yet read any supportive evidence in favor of this view. But even if that view were correct, the question arises to what extent these distortions matter in the face of a low-inflation/high unemployment economic environment.

Effectively, all these fears made the FED to engage in too little monetary stimulus in order to achieve a full and substantiated recovery: Inflation levels have been low and unemployment has been devastatingly high since 2008 as a result of too little aggregate demand.

Furthermore, the fiscal multiplier is certainly above 0 in such an environment. Any reduction in aggregate demand by the government would in this case not be offset to 100% by the Central Bank with additional unconventional monetary policies because Central Banks feel uncomfortable employing these tools.

This is definitely the environment that has dominated the periphery of the Eurozone over the last couple of years. The ECB has been unwilling to keep aggregate demand (nominal spending) on track. The drop in nominal GDP in many Southern European countries led to highly elevated levels of unemployment and deeply depressed levels of real output. The situation was aggravated by fiscal consolidation. Government multipliers were high because the ECB has been unwilling to offset any reduction in nominal spending caused by fiscal austerity. Consequently, these reductions in government expenditures led to even higher unemployment levels and output losses, and ironically also higher debt levels. That is because with a high fiscal multiplier the reduction in GDP is greater than the reduction in debt, thus increasing the debt/GDP ratio instead of reducing it. If the whole point of fiscal austerity was thus to reduce debt levels, then the policy failed completely as it actually increased debt ratios in the Eurozone periphery.

DeLong and Summers actually even go further than this. They explain in their paper that fiscal multipliers have been reasonably large. Indeed, they cite the IMF and other authors who found out that the fiscal multiplier at the ZLB could be well above 1. There is, however, large uncertainty about its actual value and it could range from 1 to values like 2.5. Again, it is crucial to note that the fiscal multiplier is very context specific as it depends on the reaction function of the Central Bank, which will determine to what extent it will offset any increase in aggregate demand from government spending.

DeLong and Summers provide a model that explains how under certain conditions and reasonable assumptions about hysteresis effects (that is to what extent a current recession has negative effects on future output) government spending could even be self-financing. They explain that with sufficiently large values for both the multiplier and the hysteresis effects any increased government spending would not raise the debt level. That is because increased aggregate demand raises current production and thus today’s tax revenues and it also leads to a future-period boosts to potential output since a smaller recession now decreases hysteresis effects, thus increasing future tax revenues as well.

The assumption of self-financing stimulus seems to be too good to be true. It would be a free lunch and certainly only exists under the special circumstances mentioned above. Nonetheless, even if expansionary spending raises current debt levels to a certain extent, expansionary fiscal policies could easily pass a sensible Benefit-Cost test. The costs of a recession and high unemployment levels potentially cast a big shadow on future output. That is because workers might get discouraged, which makes them permanently quit the labor force and loose their human capital. Young workers might have trouble beginning their career due to elevated levels of youth unemployment, affecting their career paths and lifetime incomes. These and other mechanism suggest that fiscal policy can and should play a stabilization role in case monetary policy is unable or unwilling to do so.

Recent events in Southern Europe certainly prove that fiscal multipliers can be large at times. Based on these facts, the premise that the FED will and always can offset any fiscal consolidation seems to be flawed. Specifically, Bernanke testified before Congress that the spending cuts imposed by the sequester might hurt the economy, leading to lower growth and higher unemployment (compared to a situation without these cuts). Bernanke thus specifically told Congress that the FED has indeed not fully offset government spending cuts recently and that the multiplier is above 0 right now.

References:

Bernanke on the Great Moderation:

http://www.federalreserve.gov/boarddocs/speeches/2004/20040220/

DeLong and Summers on Fiscal policy at the ZLB (pdf):

http://www.brookings.edu/~/media/Projects/BPEA/Spring%202012/2012a_DeLong.pdf

Krugman on the liquidity trap in Japan (pdf):

http://www.brookings.edu/~/media/projects/bpea/1998%202/1998b_bpea_krugman_dominquez_rogoff.pdf

Summers on nominal GDP targeting (pdf):

http://mercatus.org/sites/default/files/NGDP_Sumner_v-10-copy.pdf

RSS Feed

RSS Feed