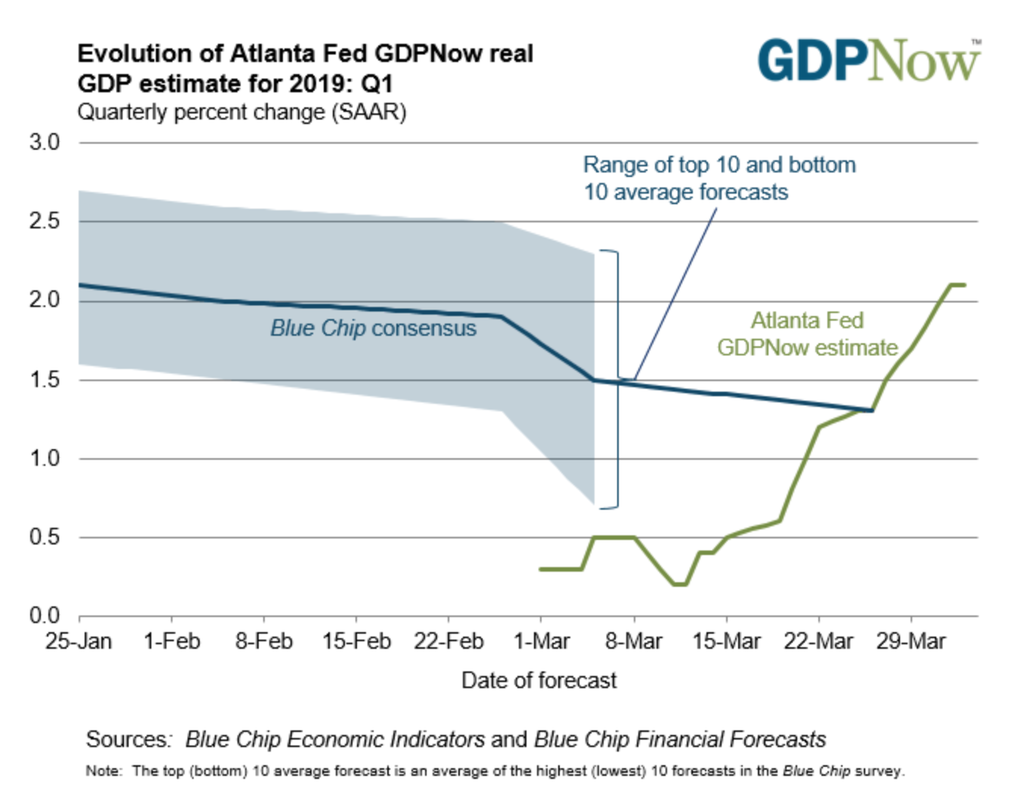

In my previous two blogposts (here and here), I have written about the fact the fact that the global economy is currently slowing down quite rapidly, especially in the Eurozone. However, GDP predictions for Q1 for the US were looking quite miserable as well. However, this might have been maybe a too hasty judgement since the most recent data has shown some improvement. I have written before on the different GDP Nowcast models. Historically, the GDP Nowcast model used by the Atlanta Fed has been the most accurate with an average absolute forecast error of under 0.6%. Just in the beginning of March the model forecasted a Q1 GDP figure of less than 0.5%. Now one month later, this estimate has increased to 2.1% and is therefore much more bullish than both the NY Fed Nowcast (at 1.3%) or the Blue Chip consensus (see figure below).

There is still a good chance that the first quarter growth rays might come in at only 1%, which would be well-below the Fed’s estimate of the economy’s long-run potential (~2%), but the probability of this happening seems to be lower now than just a few weeks ago.

According to the Atlanta model, the increase in its GDP estimate comes mostly from a higher contribution of net exports as well as inventories. While both items were supposedly subtracting from GDP growth more than a month ago, their contributions have now turned positive in recent weeks, therefore leading to the revised GDP estimate. As previously stated, the Atlanta model has so far outperformed its NY counterpart in terms of forecast accuracy. The upward revision in its GDP estimate has been quite dramatic and as far as I recall there are very few quarters where the forecast has changed to such an amount in one direction within just a few weeks. Furthermore, the Blue Chip consensus estimate as well as the NY Fed Nowcast have remained fairly stable/slightly trended downwards over that time period. We will find out in a couple of weeks from now whether the dramatic improvement in the Atlanta Fed’s model was warranted or whether it will turn out to be an outlier. Stay tuned!

There is still a good chance that the first quarter growth rays might come in at only 1%, which would be well-below the Fed’s estimate of the economy’s long-run potential (~2%), but the probability of this happening seems to be lower now than just a few weeks ago.

According to the Atlanta model, the increase in its GDP estimate comes mostly from a higher contribution of net exports as well as inventories. While both items were supposedly subtracting from GDP growth more than a month ago, their contributions have now turned positive in recent weeks, therefore leading to the revised GDP estimate. As previously stated, the Atlanta model has so far outperformed its NY counterpart in terms of forecast accuracy. The upward revision in its GDP estimate has been quite dramatic and as far as I recall there are very few quarters where the forecast has changed to such an amount in one direction within just a few weeks. Furthermore, the Blue Chip consensus estimate as well as the NY Fed Nowcast have remained fairly stable/slightly trended downwards over that time period. We will find out in a couple of weeks from now whether the dramatic improvement in the Atlanta Fed’s model was warranted or whether it will turn out to be an outlier. Stay tuned!

RSS Feed

RSS Feed