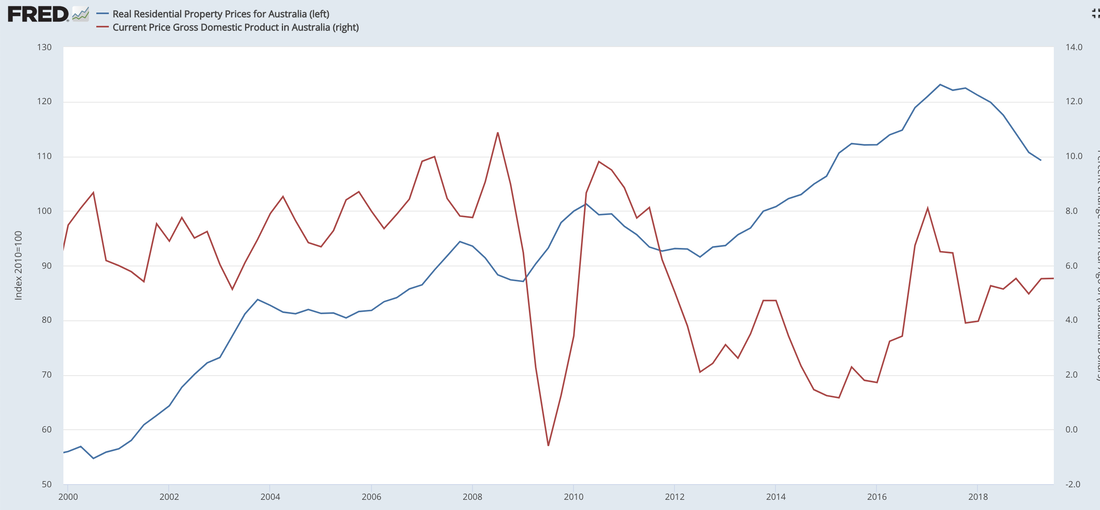

I haven't followed Australian economic data for a while. So I was extremely surprised to find the following chart that shows that real house prices have declined by more than 10% over the last two years. In fact, the Australian housing market seems to have peaked in early 2017.

While over the last 10 years, a large number of people have proclaimed that the Australian housing market is in a bubble, these bubble calls were always pretty much nonsense. Making many wrong predictions in a row and then finally having one good call doesn't make you right. Therefore most bubble predictions turn out to be utter nonsense. Moreover, timing is everything. Even if you correctly called the Dot-Com bubble, for example, but started to short the market too early, you still would have lost a lot of money. It is basically impossible to correctly identify market turning points ahead of time, and anybody who claims otherwise is just misleading.

While over the last 10 years, a large number of people have proclaimed that the Australian housing market is in a bubble, these bubble calls were always pretty much nonsense. Making many wrong predictions in a row and then finally having one good call doesn't make you right. Therefore most bubble predictions turn out to be utter nonsense. Moreover, timing is everything. Even if you correctly called the Dot-Com bubble, for example, but started to short the market too early, you still would have lost a lot of money. It is basically impossible to correctly identify market turning points ahead of time, and anybody who claims otherwise is just misleading.

So the graph above does not show in any meaningful way that the Australian housing bubble is finally bursting. However, given the extraordinary house price boom that the country has experienced since the 2000s, this definitely seems to be a turning point. Going ahead, it is not clear though whether the decline will continue. Moreover, as of right now, the price decline does not seem to have significantly affected economy-side spending, which seems to hold up rather nicely as NGDP growth has only slowed down very moderately. However, this could obviously change quickly if the housing bust worsens, but this remains to be seen.

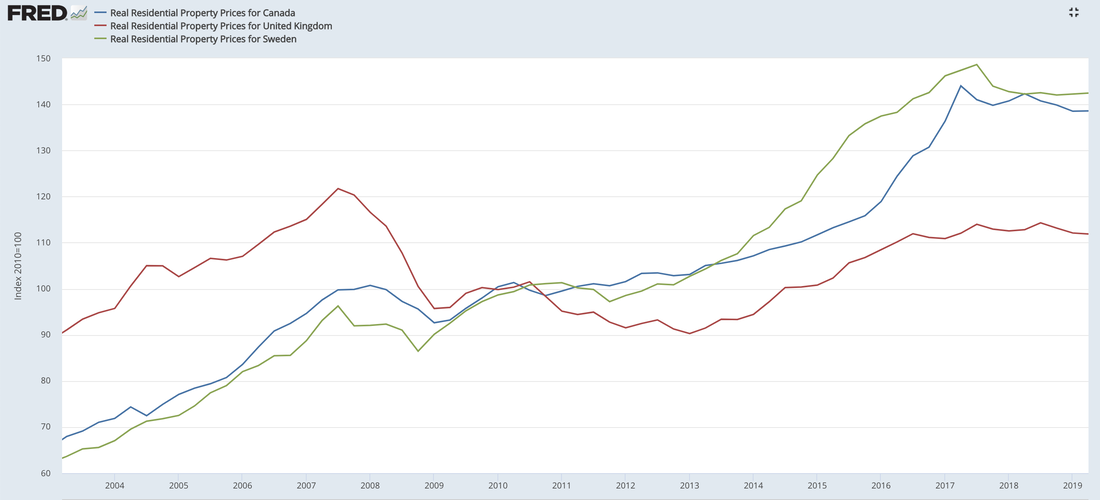

What is interesting is that Australia is currently not the only country where house prices have stalled after a significant booming period that has lasted for more than two decades. This obviously raises the question whether the current global boom in real estate has finally approached an inflection point. Canada, the UK, and Sweden have also experienced in recent years a peak in the real price of housing, followed by a moderate decline. While at least in Sweden this trend might have reversed (based on Swedish data), this does not seem to be the case for Canada and the UK.

What is interesting is that Australia is currently not the only country where house prices have stalled after a significant booming period that has lasted for more than two decades. This obviously raises the question whether the current global boom in real estate has finally approached an inflection point. Canada, the UK, and Sweden have also experienced in recent years a peak in the real price of housing, followed by a moderate decline. While at least in Sweden this trend might have reversed (based on Swedish data), this does not seem to be the case for Canada and the UK.

Obviously, this begs the question whether the long-awaited burst of the housing bubbles has finally arrived. While it is theoretically possible that the moderate declines indicating some kind of local or even global inflection point, this seems rather unlikely. While it is true that mortgage to GDP ratios have also steadily increased in recent years, especially in the aforementioned economies, global housing prices are not solely determined by what some have dubbed increasing fianancialization. Certainly, the effect of greater leverage might have contributed to the recent increase in price. However, there are also several real factors that have contributed to the price appreciations many advanced economies have experienced.

First, the forces of economic geography have pushed up house prices around the world. Over the last couple of decades, many advanced economies have experienced rising concentration where some superstar cities have pulled ahead of many rural areas and even small to medium-sized cities. Consequently, real house prices have increased in large metropolitan areas to an even larger extent, thus putting added pressure on aggregate national indices.

Second, a lot of advanced economies suffer from NIMBYism in one form or the other. Especially in large metropolitan areas where additional supply is needed the most, construction has lagged way behind. Some cities like Berlin are now even resorting to non-sensical policies like rent control, which is supposed to alleviate the pressure from rising rents but will also negatively affect residential investment and therefore simply aggravate the housing crisis in the long-run. Therefore, many large European cities have seen their housing prices appreciate considerably in recent decades.

Third, low interest rates combined with a high mortgage to GDP ratios will continue to support high house price valuations in the foreseeable future.

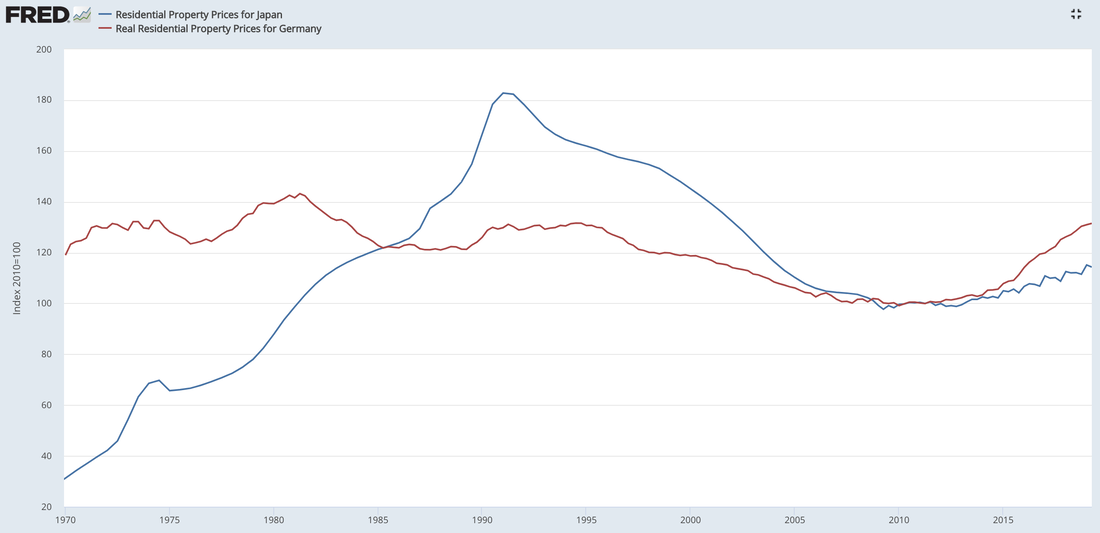

By the way, recent reports by the Bundesbank and others suggest that policy makers in Germany are increasingly worried about appreciating house prices and the emergence of a real estate bubble, which they also seem to blame on ECB policy. This is actually quite ridiculous. As I have written before, the ECB has actually little to do with low real interest rates, which can be observed globally and are determined by global macroeconomic conditions. Moreover, as you can see from the chart above to which I have added German real estate prices, Germany's experience is somewhat unique. Besides Japan, it is one of the very few countries in which real house prices stagnated for several decades (see below). Only over the last few years has the German economy seen significant real house price appreciations, and mostly in the large cities like Munich, Hamburg, and Berlin, etc. However, the recent appreciation in Germany nowhere comes close to what other advanced economies have experienced in recent decades. It therefore seems quite a stretch to me to call the German situation a housing bubble. While not denying that the housing market in cities like Frankfurt is very tight, these problems must be addressed by local policy makers.

First, the forces of economic geography have pushed up house prices around the world. Over the last couple of decades, many advanced economies have experienced rising concentration where some superstar cities have pulled ahead of many rural areas and even small to medium-sized cities. Consequently, real house prices have increased in large metropolitan areas to an even larger extent, thus putting added pressure on aggregate national indices.

Second, a lot of advanced economies suffer from NIMBYism in one form or the other. Especially in large metropolitan areas where additional supply is needed the most, construction has lagged way behind. Some cities like Berlin are now even resorting to non-sensical policies like rent control, which is supposed to alleviate the pressure from rising rents but will also negatively affect residential investment and therefore simply aggravate the housing crisis in the long-run. Therefore, many large European cities have seen their housing prices appreciate considerably in recent decades.

Third, low interest rates combined with a high mortgage to GDP ratios will continue to support high house price valuations in the foreseeable future.

By the way, recent reports by the Bundesbank and others suggest that policy makers in Germany are increasingly worried about appreciating house prices and the emergence of a real estate bubble, which they also seem to blame on ECB policy. This is actually quite ridiculous. As I have written before, the ECB has actually little to do with low real interest rates, which can be observed globally and are determined by global macroeconomic conditions. Moreover, as you can see from the chart above to which I have added German real estate prices, Germany's experience is somewhat unique. Besides Japan, it is one of the very few countries in which real house prices stagnated for several decades (see below). Only over the last few years has the German economy seen significant real house price appreciations, and mostly in the large cities like Munich, Hamburg, and Berlin, etc. However, the recent appreciation in Germany nowhere comes close to what other advanced economies have experienced in recent decades. It therefore seems quite a stretch to me to call the German situation a housing bubble. While not denying that the housing market in cities like Frankfurt is very tight, these problems must be addressed by local policy makers.

RSS Feed

RSS Feed