I have written about the various GDP Nowcast models the Fed uses on this blog before. Both the Atlanta Fed Nowcast and the New York Fed Nowcast model are based on the dynamic factor methodology. The idea is to extract on common factor variables from a large number of macroeconomic time series data that is available at a higher frequency than GDP. The latent factor then helps us to recover an estimate for GDP in real-time. The St. Louis Nowcast, on the other hand, is based on a different methodology that extracts information from economic surprises.

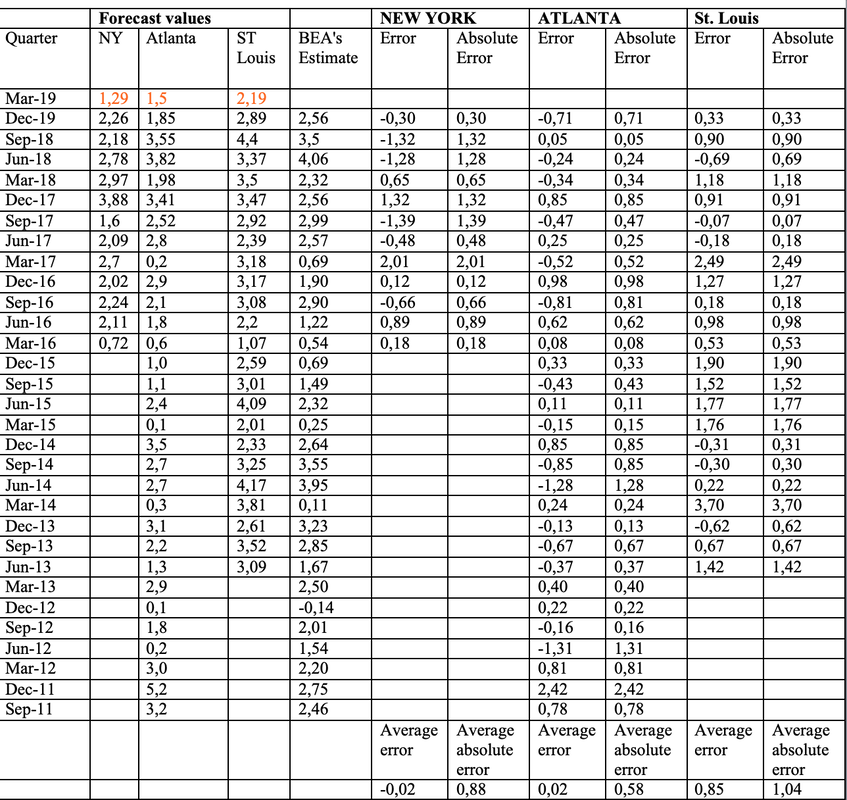

Based on my previous analysis, I found that the Atlanta GDP Nowcast model has so far the best track record with an average absolute forecast error for quarterly GDP figures of about 0.6% whereas the New York Nowcast and the St. Louis Nowcast produce absolute forecast errors of 0.9% and 1.1%, respectively. By the way, the St. Louis Nowcast doesn't seem to produce much better results than a simple random walk (simply predicting that next quarter's GDP growth will be the same as the previous quarter), and thus seems to be relatively inaccurate as a forecasting device.

Last year's GDP figure came in very strong with an annual growth rate of about 3% for 2018 despite the fact that the Fed hiked interest rates 4 times. It is now a relatively safe bet to assume that the massive Trump tax cut provided a short-term stimulus to the economy. However, it does not seem to have done much to the economy's long-run potential. Business investment is not substantially higher and most estimates of the economy's long-run growth rates have remained unchanged.

As for 2019, we can already see a substantial slowdown in economic activity across the globe. While the economic data for the Eurozone seems to be worse, GDP Nowcast models suggest that the first quarter of 2019 might come in at just about 1.5% while the NY Nowcast for the 2nd quarter is at 1.7%. Both values are therefore slightly below the economy's long-run potential which Fed economists have pegged at just a little below 2%.

For those who want to keep track of the GDP Nowcast forecasts and its accuracy, have a look at the table below. Both the Atlanta as well as the NY model seem to be unbiased, meaning that errors cancel out over time, whereas the St. Louis model consistently overestimates GDP growth. As mentioned above, the Atlanta model produces the lowest absolute forecast errors. Taken all the predictions into account, it wouldn't surprise me if Q1 GDP growth comes in somewhere in between 1% and 1.5%, which would represent a significant slowdown from last year's expansion.

Based on my previous analysis, I found that the Atlanta GDP Nowcast model has so far the best track record with an average absolute forecast error for quarterly GDP figures of about 0.6% whereas the New York Nowcast and the St. Louis Nowcast produce absolute forecast errors of 0.9% and 1.1%, respectively. By the way, the St. Louis Nowcast doesn't seem to produce much better results than a simple random walk (simply predicting that next quarter's GDP growth will be the same as the previous quarter), and thus seems to be relatively inaccurate as a forecasting device.

Last year's GDP figure came in very strong with an annual growth rate of about 3% for 2018 despite the fact that the Fed hiked interest rates 4 times. It is now a relatively safe bet to assume that the massive Trump tax cut provided a short-term stimulus to the economy. However, it does not seem to have done much to the economy's long-run potential. Business investment is not substantially higher and most estimates of the economy's long-run growth rates have remained unchanged.

As for 2019, we can already see a substantial slowdown in economic activity across the globe. While the economic data for the Eurozone seems to be worse, GDP Nowcast models suggest that the first quarter of 2019 might come in at just about 1.5% while the NY Nowcast for the 2nd quarter is at 1.7%. Both values are therefore slightly below the economy's long-run potential which Fed economists have pegged at just a little below 2%.

For those who want to keep track of the GDP Nowcast forecasts and its accuracy, have a look at the table below. Both the Atlanta as well as the NY model seem to be unbiased, meaning that errors cancel out over time, whereas the St. Louis model consistently overestimates GDP growth. As mentioned above, the Atlanta model produces the lowest absolute forecast errors. Taken all the predictions into account, it wouldn't surprise me if Q1 GDP growth comes in somewhere in between 1% and 1.5%, which would represent a significant slowdown from last year's expansion.

GDP Nowcast models

On the right hand side of the table, you can find the forecasted values compared to the BEA's advanced GDP estimate for the quarter in question. On the left hand side, I have calculated the error and absolute value of the error for each model.

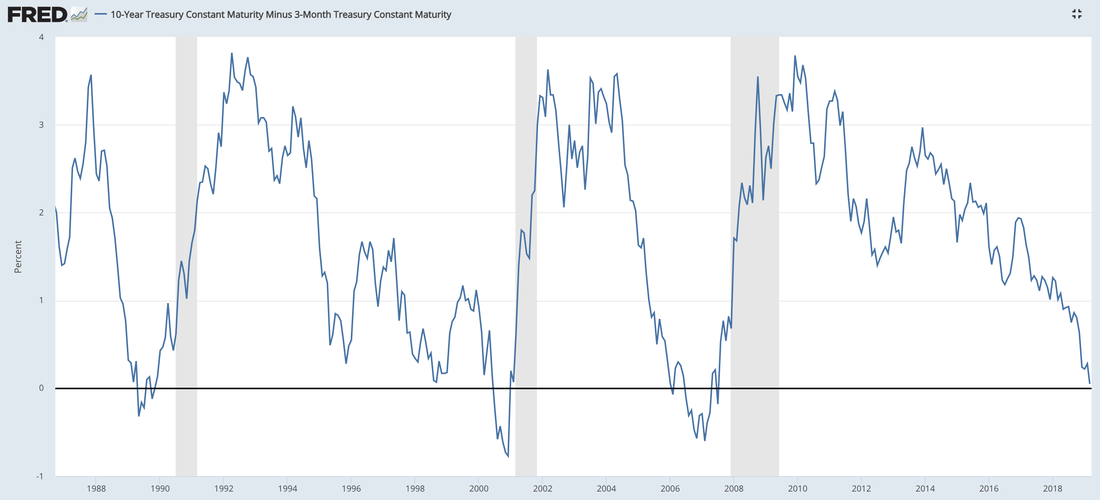

It therefore seems that last year's Fed rate hike cycle was somewhat premature and that it has now turned into a drag for the overall economy. Financial markets are already pricing in that the Fed will lower rates again this year. This also implies, by the way, that monetary policy is actively becoming tighter as we speak if the Fed persists on not lowering rates, given that the natural rate of interest seems to be decreasing again. The recent yield curve inversion, historically one of the only reliable predictors of a future recession, seems to indicate to me that the Fed has already increased the short-run rate above the natural rate, and that is why the risk of a recession has increased sharply.

Furthermore, as Paul Krugman recently pointed out on Twitter, it might make a fundamental difference that the yield curve inversion happened when rates are just at 2.5% instead of at more than 5%, as during the previous expansion. In the past, the Fed has lowered interest rates by about 500 basis points each time when an economic downturn occurred. Given that long-term rates indicate the expected future path of short-term interest rates, any yield curve inversion in the past must have reflected at least some probability that the Fed would lower rates by at least 500 basis points to combat an upcoming recession. However, as of right now, the Fed can lower rates by only about 240 basis bounds until it hits the zero-lower bound again. Bond markets therefore already price in the possibility that the Fed cannot ease monetary policy to the same extent as it did in the past. It would therefore only be prudent for the Fed to take out some recession insurance right now, meaning that it should aggressively ease monetary policy before it's too late. A strong commitment to keep nominal GDP on a stable path of 4 to 5% annual growth combined with a rate cut of maybe 50 basis points might actually do the trick. Unfortunately, I believe that the Fed board will be reluctant to decrease interest rates again just half a year after they announced that the rate hike cycle would continue in 2019. While in the Fed meeting of last week Powell and Co. have now sworn off any further rate hikes for the rest of the year, I do not think that this will be enough to keep the economy from decelerating. Current policy is still characterized by too much interest rate inertia, and more likely than not, the Fed will find itself behind the curve again in a few months' time. Last week’s Fed meeting was therefore much less dovish than the financial press has acknowledged so far.

The recent decline in long-term interest rates indicates that the global economy must brace for another economic slowdown, thus confirming Larry Summer's theory on secular stagnation. Some 10 trillion of debt are having a negative yield again, which is totally crazy when you think about it, with 10-year German government bonds having a yield of zero and their Japanese equivalent having a yield that is a few basis points below zero.

While a coordinated strong fiscal expansion across the Eurozone could be the cure, it is extremely unlikely that Europe will get any positive fiscal impulse any time soon, as the German government still insists on balanced budgets. Given that the ECB just ended its asset purchase program in December of last year and interest rates are still negative, the ECB has even much less room to maneuver than the Fed. More likely than not, the next recession will start in the Eurozone whereas policy makers in the US potentially have the capacity to engineer a soft ending for the end of this now 10-year long expansion. Unfortunately, history is not on their side.

Furthermore, as Paul Krugman recently pointed out on Twitter, it might make a fundamental difference that the yield curve inversion happened when rates are just at 2.5% instead of at more than 5%, as during the previous expansion. In the past, the Fed has lowered interest rates by about 500 basis points each time when an economic downturn occurred. Given that long-term rates indicate the expected future path of short-term interest rates, any yield curve inversion in the past must have reflected at least some probability that the Fed would lower rates by at least 500 basis points to combat an upcoming recession. However, as of right now, the Fed can lower rates by only about 240 basis bounds until it hits the zero-lower bound again. Bond markets therefore already price in the possibility that the Fed cannot ease monetary policy to the same extent as it did in the past. It would therefore only be prudent for the Fed to take out some recession insurance right now, meaning that it should aggressively ease monetary policy before it's too late. A strong commitment to keep nominal GDP on a stable path of 4 to 5% annual growth combined with a rate cut of maybe 50 basis points might actually do the trick. Unfortunately, I believe that the Fed board will be reluctant to decrease interest rates again just half a year after they announced that the rate hike cycle would continue in 2019. While in the Fed meeting of last week Powell and Co. have now sworn off any further rate hikes for the rest of the year, I do not think that this will be enough to keep the economy from decelerating. Current policy is still characterized by too much interest rate inertia, and more likely than not, the Fed will find itself behind the curve again in a few months' time. Last week’s Fed meeting was therefore much less dovish than the financial press has acknowledged so far.

The recent decline in long-term interest rates indicates that the global economy must brace for another economic slowdown, thus confirming Larry Summer's theory on secular stagnation. Some 10 trillion of debt are having a negative yield again, which is totally crazy when you think about it, with 10-year German government bonds having a yield of zero and their Japanese equivalent having a yield that is a few basis points below zero.

While a coordinated strong fiscal expansion across the Eurozone could be the cure, it is extremely unlikely that Europe will get any positive fiscal impulse any time soon, as the German government still insists on balanced budgets. Given that the ECB just ended its asset purchase program in December of last year and interest rates are still negative, the ECB has even much less room to maneuver than the Fed. More likely than not, the next recession will start in the Eurozone whereas policy makers in the US potentially have the capacity to engineer a soft ending for the end of this now 10-year long expansion. Unfortunately, history is not on their side.

RSS Feed

RSS Feed