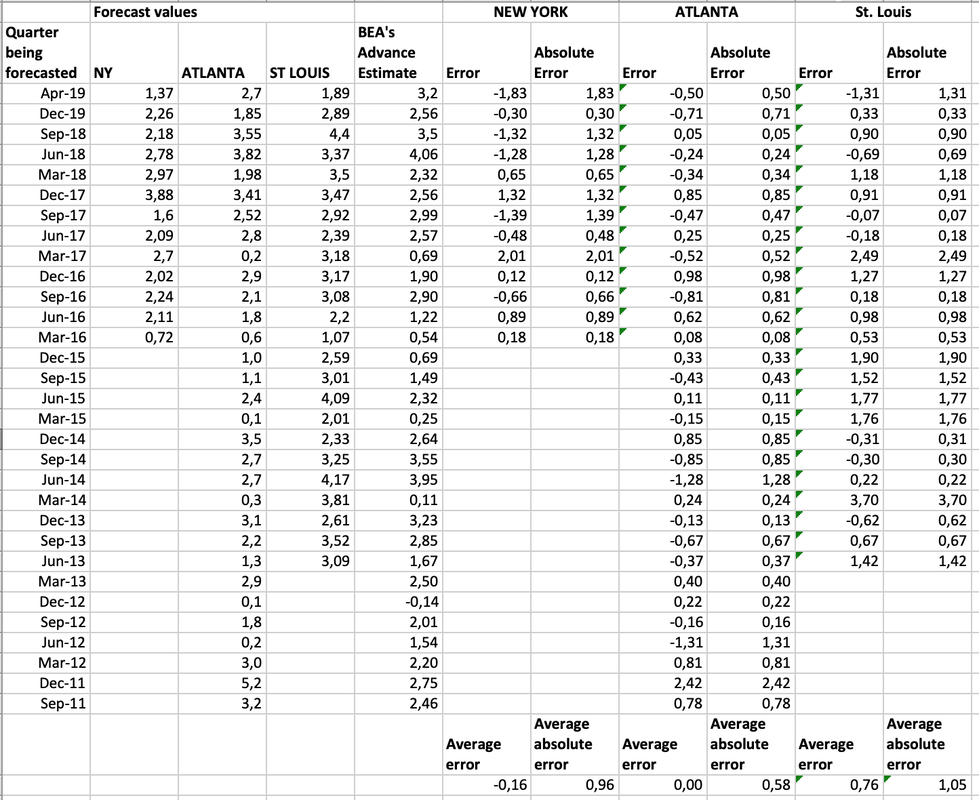

US quarterly GDP for the first quarter with a growth rate of 3.2% came in surprisingly strong yesterday. However, a substantial part of this can be attributed to inventories and net exports, meaning that another big upside surprise for next quarter is rather unlikely. I have kept track of the different Nowcast models on this blog before (see here, for example). So far, the Atlanta GDP Nowcast has turned out to be the most accurate (see table below). Not only does it have the smallest absolute forecast error, but it’s missed also seem to be unbiased, i.e. they average out over time.

More importantly, the Atlanta Fed model revised its Nowcast upwards on several occasions over the last few months whereas the New York Nowcast and all the private forecasters revised their GDP estimate downwards. Clearly, the Atlanta's model forecast got better overt time as this quarter progressed whereas most other GDP estimates got worse. It therefore seem that the GDP Nowcast model has a significant edge, not only compared to the other Nowcast models, but also compared to private sector estimates. This quarter's GDP Nowcast estimate is another big win for the Atlanta model!

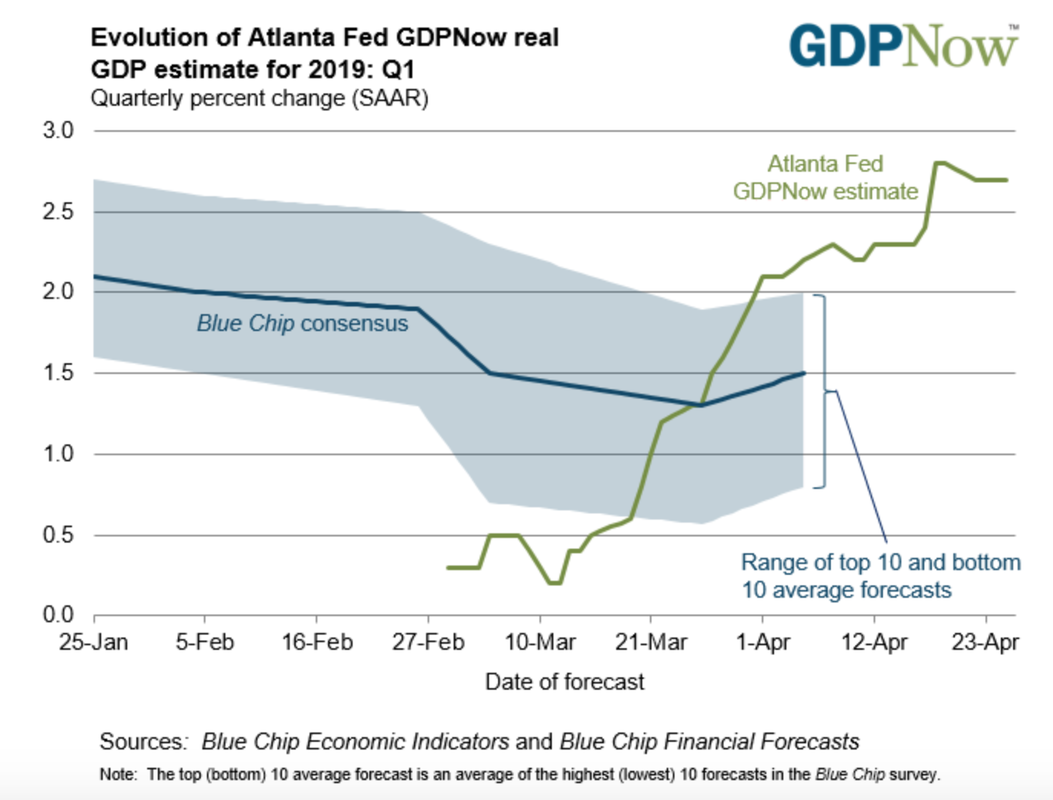

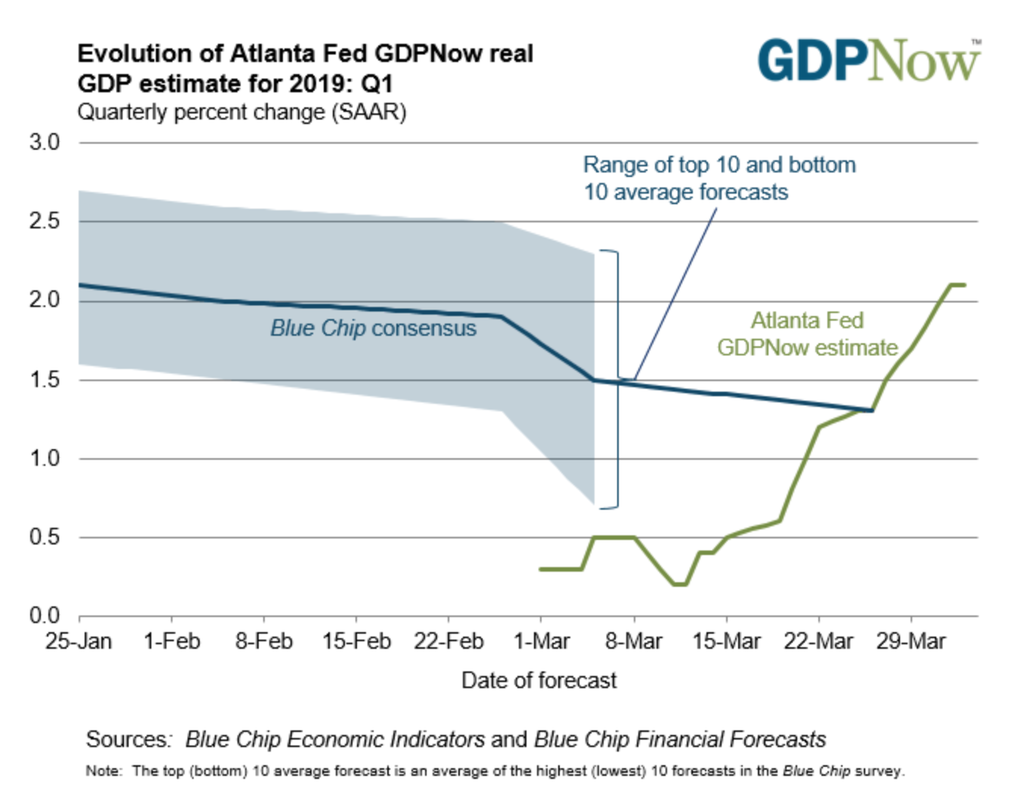

The Atlanta Nowcast estimate for Q1

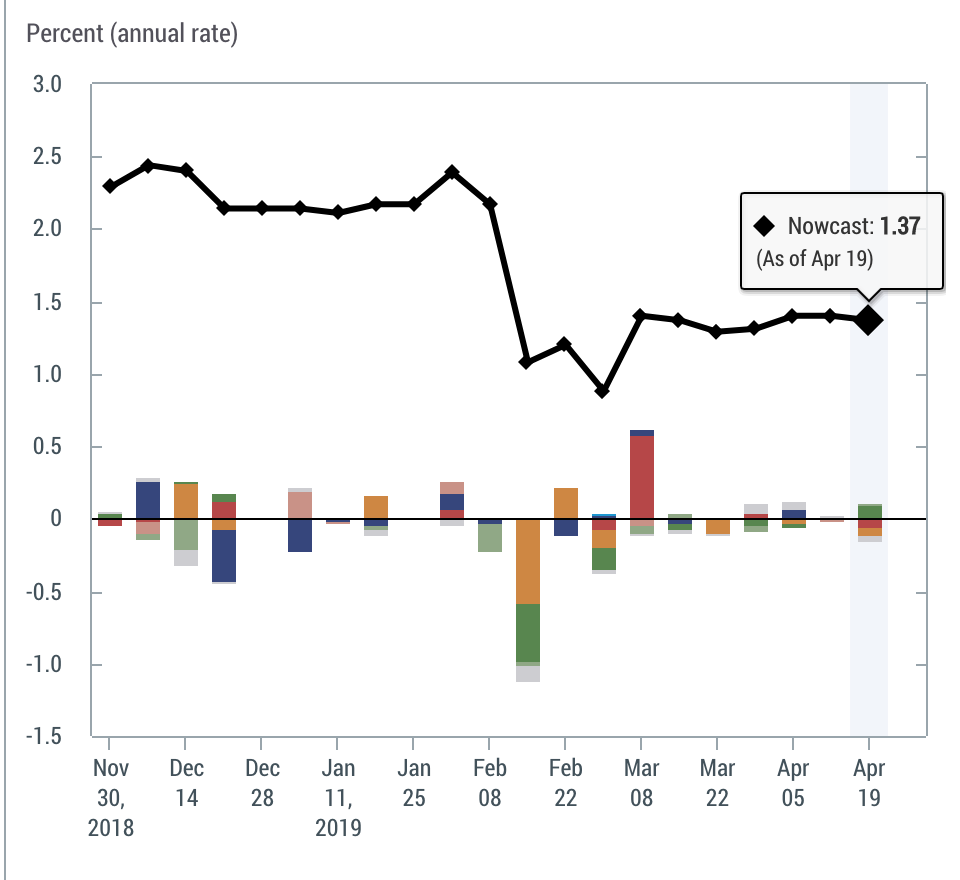

The New York Nowcast estimate for Q1

RSS Feed

RSS Feed