So I am seeing a lot of analysis on Bloomberg and other media outlets how last quarter's GDP figures in the US defied expectations (true) and how this now calls into question the Fed's desire to ease monetary policy (false).

This is nonsense for several reasons. It is true that Q2 GDP growth of 2.1% in the US was above expectations. The Atlanta GDP Nowcast, for example, had a forecast of only 1.3%. So while this Nowcast estimate has historically produced relatively good estimates, they were off the mark for this quarter. However, it should be noted that quarterly GDP figures are actually quite volatile. It is therefore extremely misleading to make inferences about the state of the economy based on one quarter's GDP figure.

Second, quarterly GDP figures are often subject to substantial revisions. Until a couple of days ago, we actually thought that the US economy was growing at the rate of 3% last year. Well, it turns out that actual growth was more like 2.5%, meaning that Trump's policies, including the enormous tax cut, did actually deliver even less than what the administration actually suggested. The impact of the tax cut on business investment is barely noticeable. The downward revision for last year came about a revision for Q2 from 4.2 to 3.5% and an even greater revision for Q4 from 2.2 to 1.1%. All of this is obviously bad news. And it also means that the current estimate of 2.1% for last quarter is relatively meaningless and it definitely does not imply that the Fed should not go forward with interest rate cuts.

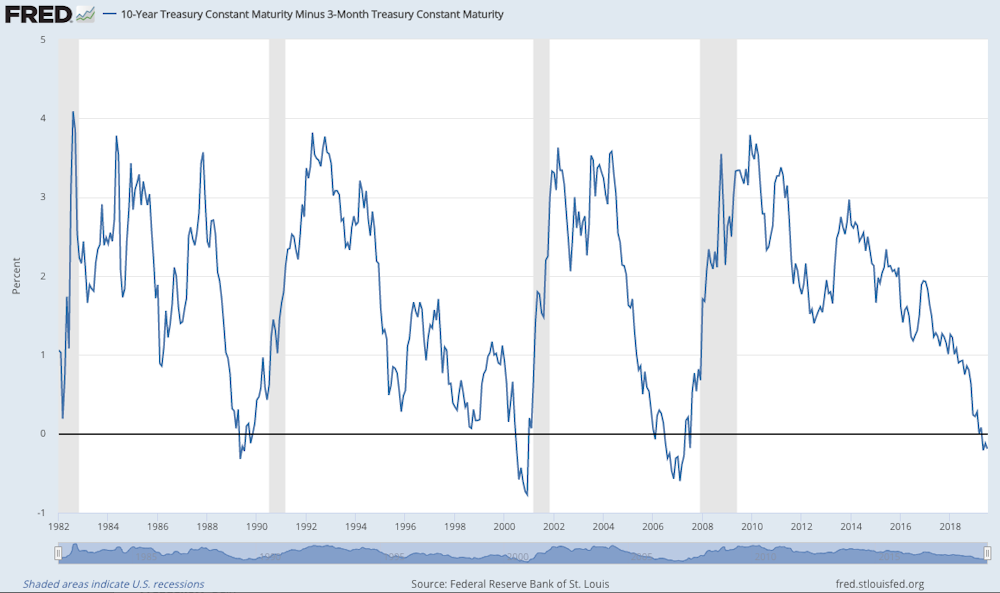

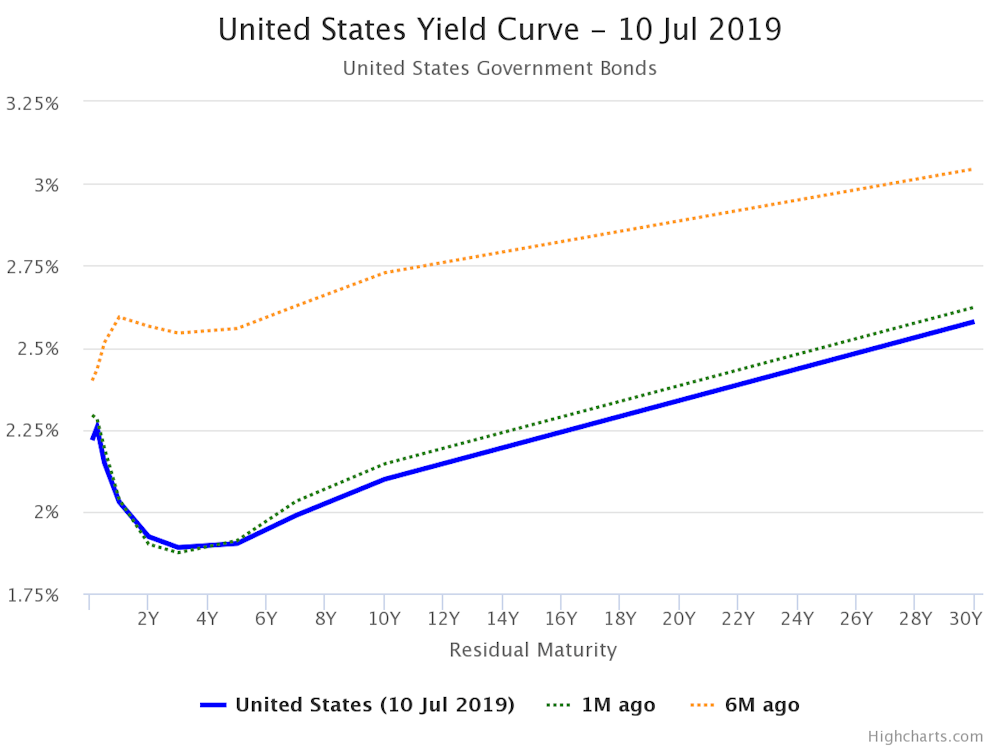

In fact, I believe that a 50 basis points rate cut would be actually more appropriate than a simple 25 bps rate cut for several reasons. First, it looks like the natural rate of interest is trending downward sharply, both in the Eurozone but also in the US. This means that the Fed needs to cut rates just to keep monetary policy neutral and NGDP growing at a stable rate.

Second, financial markets expect about 2 to 2.5 rate cuts by the Fed by the end of this year. So why not simply cut 50 bps right now, deliver a dovish message and get it over with instead of being more prudent. It does not make sense to delay the inevitable. The US economy's interest rates are actually quite high from a global perspective and this divergence was unlikely to continue. Given that the economic slowdown in the Eurozone is even more pronounced and that the ECB is expected to go even more negative and resume QE in a few months, it makes sense for the Fed to cut rates and prevent the dollar from appreciating, which would put further pressure on the domestic economy.

This is nonsense for several reasons. It is true that Q2 GDP growth of 2.1% in the US was above expectations. The Atlanta GDP Nowcast, for example, had a forecast of only 1.3%. So while this Nowcast estimate has historically produced relatively good estimates, they were off the mark for this quarter. However, it should be noted that quarterly GDP figures are actually quite volatile. It is therefore extremely misleading to make inferences about the state of the economy based on one quarter's GDP figure.

Second, quarterly GDP figures are often subject to substantial revisions. Until a couple of days ago, we actually thought that the US economy was growing at the rate of 3% last year. Well, it turns out that actual growth was more like 2.5%, meaning that Trump's policies, including the enormous tax cut, did actually deliver even less than what the administration actually suggested. The impact of the tax cut on business investment is barely noticeable. The downward revision for last year came about a revision for Q2 from 4.2 to 3.5% and an even greater revision for Q4 from 2.2 to 1.1%. All of this is obviously bad news. And it also means that the current estimate of 2.1% for last quarter is relatively meaningless and it definitely does not imply that the Fed should not go forward with interest rate cuts.

In fact, I believe that a 50 basis points rate cut would be actually more appropriate than a simple 25 bps rate cut for several reasons. First, it looks like the natural rate of interest is trending downward sharply, both in the Eurozone but also in the US. This means that the Fed needs to cut rates just to keep monetary policy neutral and NGDP growing at a stable rate.

Second, financial markets expect about 2 to 2.5 rate cuts by the Fed by the end of this year. So why not simply cut 50 bps right now, deliver a dovish message and get it over with instead of being more prudent. It does not make sense to delay the inevitable. The US economy's interest rates are actually quite high from a global perspective and this divergence was unlikely to continue. Given that the economic slowdown in the Eurozone is even more pronounced and that the ECB is expected to go even more negative and resume QE in a few months, it makes sense for the Fed to cut rates and prevent the dollar from appreciating, which would put further pressure on the domestic economy.

RSS Feed

RSS Feed