Fed chairman Jerome Powell recently gave his remarks at the annual monetary policy conference at Jackson Hole. The speech was extremely interesting and it was also seen as slightly dovish as the dollar slightly dropped on the day whereas stock markets were slightly up. While the speech was certainly written by a Fed economist, Powell is originally a lawyer, he has been a Fed insider and monetary policy maker for many years to understand the issues at hand clearly and to communicate them to the public. And sometimes an outsider’s view can be actually helpful.

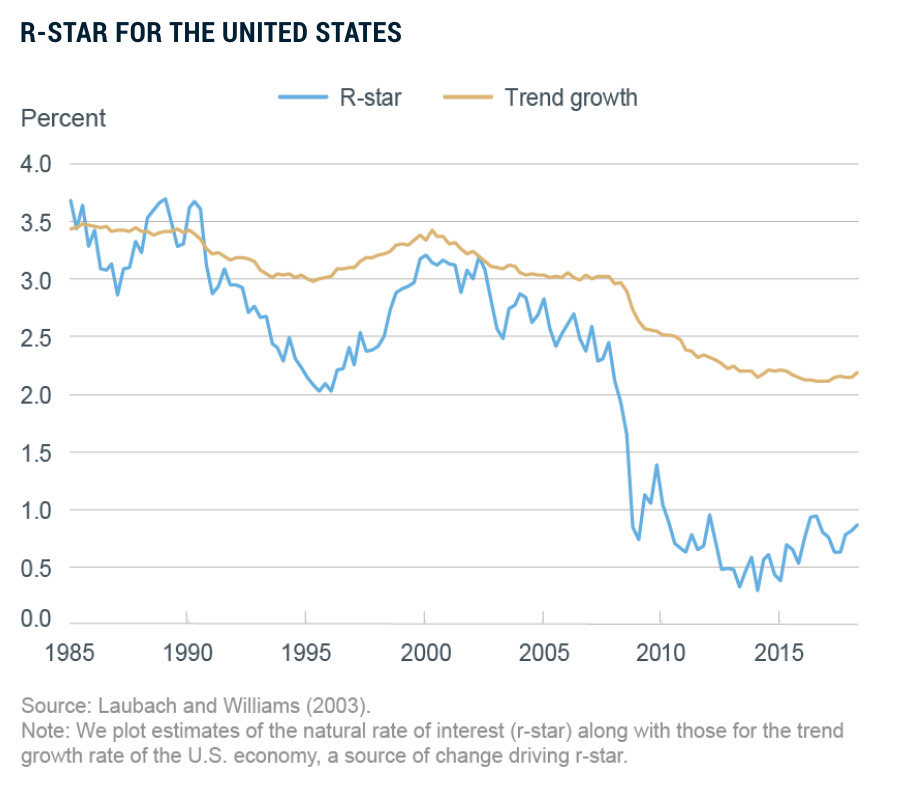

The main topic of the speech was the uncertainty monetary policy makers face when assessing the macroeconomy. There are two variables in particular, the natural rate of interest r* (r-star) and the natural rate of unemployment u*, which Central Bankers rely on. r* is the interest rate that is consistent with price stability, usually defined as an inflation rate of 2%, and u* is the unemployment rate consistent with full employment. The problem with these two variables is that they are unobservable, and even more problematic, there is a high degree of uncertainty about these variables. While macroeconomists use a variety of models to estimate r* and u*, the confidence intervals around those estimates are usually extremely large, meaning that they cannot be estimated with any precision. As an example, the New York Fed recently released an estimate for the natural rate of interest for the US economy. While the current estimate for the natural rate is relatively close to 1% (see chart below), the confidence interval for this estimate can easily exceed more than one hundred basis points, depending on the model at hand. Also note that current real interest rate is still negative, with the Fed funds rate being close to 2% while the inflation rate is running at about 2.2% at the moment, thus implying a negative real interest rate of just about minus 20 basis points. According to the New York Fed’s model, real interest rates have been persistently below the natural rate ever since the financial crisis in 2008, so basically for an entire decade now. According to the new-Keynesian model, monetary policy was thus super accommodative for almost 10 years. This begs the question why we haven’t experienced runaway inflation and high levels of nominal GDP growth given the amount of monetary accommodation. The answer, is of course, that monetary policy was actually tight until quite recently, given that unemployment rates were still relatively high, nominal GDP growth was low, and the economy still experienced extremely large negative output gaps in the aftermath of the crisis.

All of this suggests that the actual natural rate must have been considerably lower for a prolonged period in the aftermath of the crisis than what their model suggests.

The second “star variable”, the natural rate of unemployment, also cannot be known with any degree of certainty. Just a few years ago, the Fed suggested that it could not push the unemployment considerably lower than 6.5% without accepting a rising inflation rate above their 2% target. This turned out to be a super hawkish projection. Well, unemployment declined to less than 4% this year and both inflation as well as wage growth are still quite moderate, suggesting that the economy might still have some extra spare capacity left (even though considerably less than a few years ago). However, all of this also implies that monetary policy was actually much tighter in retrospect than what we thought and that a higher degree of monetary policy accommodation could have restored full employment much earlier. The US economy basically spent an entire decade having excessive unemployment and the same can be said for most of Europe.

This is by far the biggest policy blunder since the Great Depression as millions of people suffered from unemployment and/or underemployment for many years. Trillions of economic output have been lost during those years, and according to some estimates the Great Recession even depressed the economy’s long-run potential, thus scarring the economy for many years: We are most likely on a much lower growth path going forward than we would have been if the Great Recession was avoided.

The policy mistakes that are associated with a failure to correctly identify the natural rate of interest and the natural rate of unemployment can thus be quite severe. It is, in my opinion, a severe mistake to pursue monetary policy based on these immeasurable variables alone, which economists cannot even correctly identify ex-post. And there are much better alternatives. Ultimately, the rate of inflation and the rate of nominal GDP growth are the only correct way to identify the stance of monetary policy. The Fed should target the level of nominal GDP instead and largely ignore the estimates of the “star variables”, which more often than not are just a silly distraction instead of being a useful guide for future monetary policy.

The main topic of the speech was the uncertainty monetary policy makers face when assessing the macroeconomy. There are two variables in particular, the natural rate of interest r* (r-star) and the natural rate of unemployment u*, which Central Bankers rely on. r* is the interest rate that is consistent with price stability, usually defined as an inflation rate of 2%, and u* is the unemployment rate consistent with full employment. The problem with these two variables is that they are unobservable, and even more problematic, there is a high degree of uncertainty about these variables. While macroeconomists use a variety of models to estimate r* and u*, the confidence intervals around those estimates are usually extremely large, meaning that they cannot be estimated with any precision. As an example, the New York Fed recently released an estimate for the natural rate of interest for the US economy. While the current estimate for the natural rate is relatively close to 1% (see chart below), the confidence interval for this estimate can easily exceed more than one hundred basis points, depending on the model at hand. Also note that current real interest rate is still negative, with the Fed funds rate being close to 2% while the inflation rate is running at about 2.2% at the moment, thus implying a negative real interest rate of just about minus 20 basis points. According to the New York Fed’s model, real interest rates have been persistently below the natural rate ever since the financial crisis in 2008, so basically for an entire decade now. According to the new-Keynesian model, monetary policy was thus super accommodative for almost 10 years. This begs the question why we haven’t experienced runaway inflation and high levels of nominal GDP growth given the amount of monetary accommodation. The answer, is of course, that monetary policy was actually tight until quite recently, given that unemployment rates were still relatively high, nominal GDP growth was low, and the economy still experienced extremely large negative output gaps in the aftermath of the crisis.

All of this suggests that the actual natural rate must have been considerably lower for a prolonged period in the aftermath of the crisis than what their model suggests.

The second “star variable”, the natural rate of unemployment, also cannot be known with any degree of certainty. Just a few years ago, the Fed suggested that it could not push the unemployment considerably lower than 6.5% without accepting a rising inflation rate above their 2% target. This turned out to be a super hawkish projection. Well, unemployment declined to less than 4% this year and both inflation as well as wage growth are still quite moderate, suggesting that the economy might still have some extra spare capacity left (even though considerably less than a few years ago). However, all of this also implies that monetary policy was actually much tighter in retrospect than what we thought and that a higher degree of monetary policy accommodation could have restored full employment much earlier. The US economy basically spent an entire decade having excessive unemployment and the same can be said for most of Europe.

This is by far the biggest policy blunder since the Great Depression as millions of people suffered from unemployment and/or underemployment for many years. Trillions of economic output have been lost during those years, and according to some estimates the Great Recession even depressed the economy’s long-run potential, thus scarring the economy for many years: We are most likely on a much lower growth path going forward than we would have been if the Great Recession was avoided.

The policy mistakes that are associated with a failure to correctly identify the natural rate of interest and the natural rate of unemployment can thus be quite severe. It is, in my opinion, a severe mistake to pursue monetary policy based on these immeasurable variables alone, which economists cannot even correctly identify ex-post. And there are much better alternatives. Ultimately, the rate of inflation and the rate of nominal GDP growth are the only correct way to identify the stance of monetary policy. The Fed should target the level of nominal GDP instead and largely ignore the estimates of the “star variables”, which more often than not are just a silly distraction instead of being a useful guide for future monetary policy.

PS: Note how according to the model trend growth for the US economy is still estimated to be above 2%. This seems to me another dubious assumption. Trend growth since the crisis has been lower, and will most likely remain relatively low in the foreseeable future according to the "secular stagnation" theory put forward by Larry Summers (or the supply-side pessimism story put forward by Robert Gordon).

RSS Feed

RSS Feed