Some thoughts on the Chinese economy, inspired by a lecture that former chief economist of the World Bank Justin Yifu Lin gave today at Lund University. The topic of the talk was the Chinese economy.

We know that economists cannot forecast recessions, which in itself is not very astonishing. Similarly, engineers cannot predict the collapse of a bridge and doctors cannot predict sickness. Economists are much better at conditional forecasts. During the financial crisis of 2008/2009, many economists warned that much greater fiscal stimulus and monetary policy accommodation was needed to prevent a severe downturn from happening. Unfortunately, those warnings were shrugged off and policy makers repeated to a some extent the mistakes that were made during the Great Depression, thus leading to a prolonged period of economic stagnation and a rise of populism across advanced economies, a repeat of the 1930s if you will (It probably didn’t help either that within the economics profession a small but quite influential group proclaimed that fiscal stimulus cannot increase aggregate demand or that prolonged monetary stimulus would lead to hyperinflation, two fallacies that should have died a long time ago with Keynes’ General Theory).

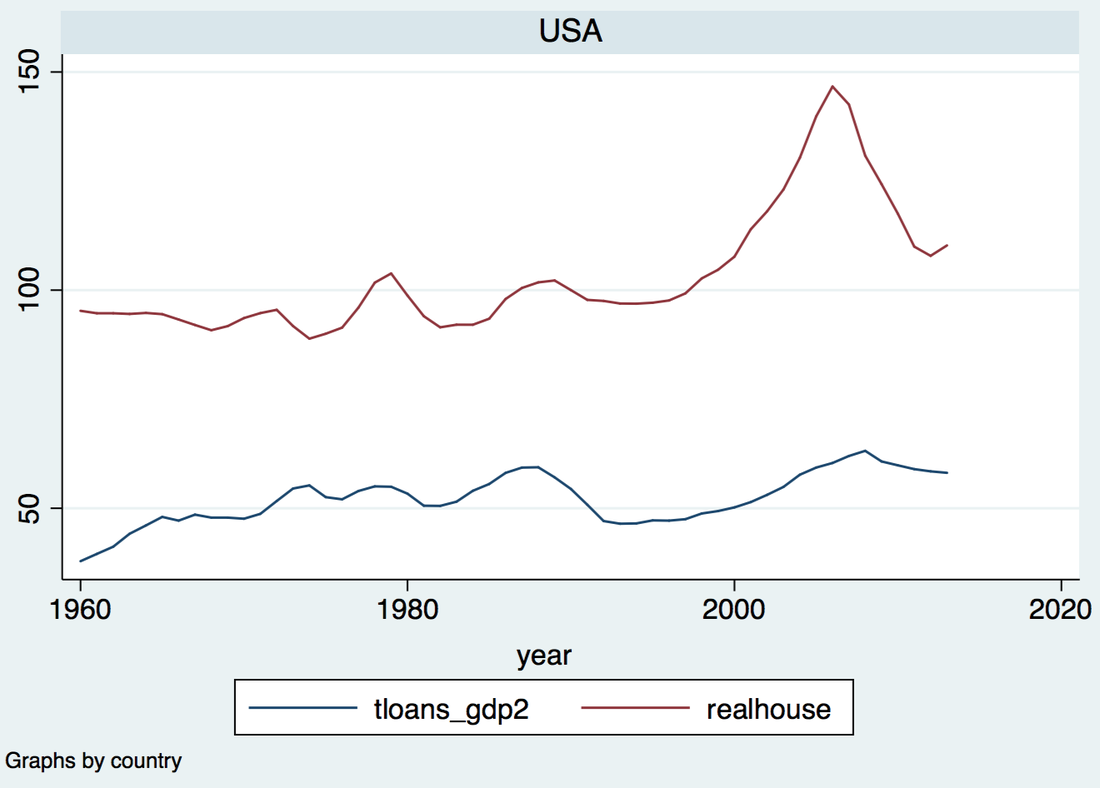

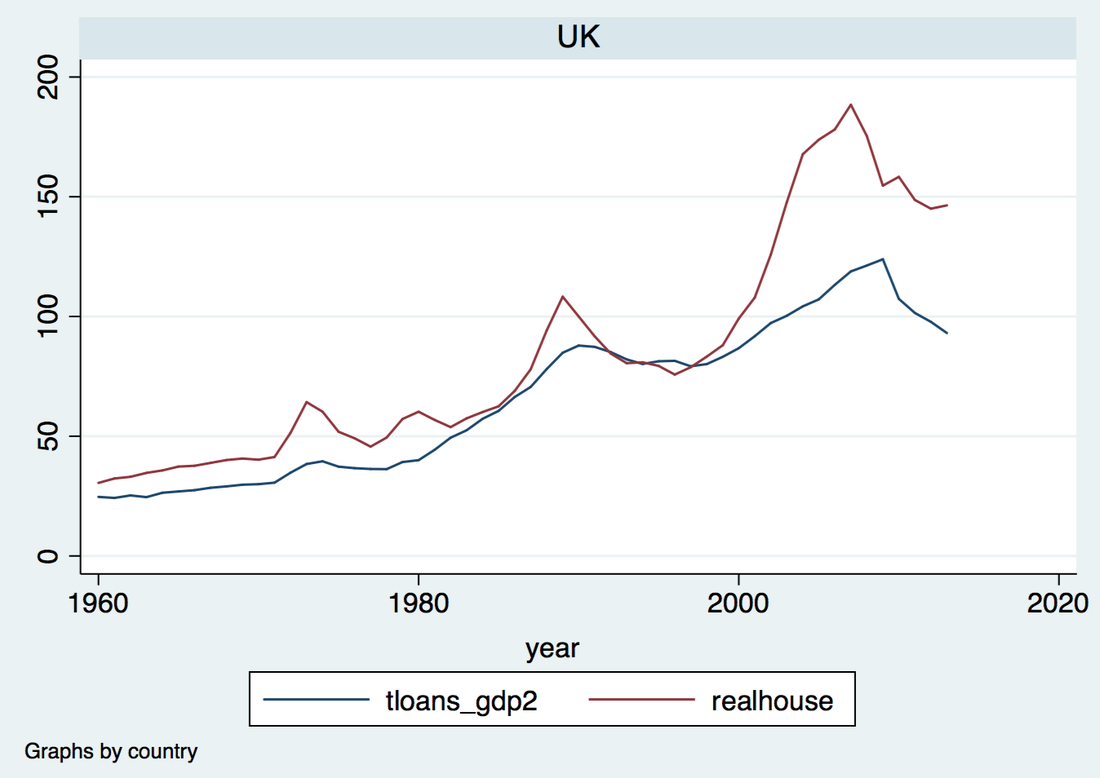

More recently, economic historians have found that the best predictor of a coming financial crisis and economic recession is a large run-up in debt combined with elevated asset prices, either stocks or real estate. More specifically, private sector debt seems to matter more than public debt. The financial crisis in the U.S. and in the Eurozone, for example, was preceded by large increases in mortgage to GDP ratios and rapidly rising house prices, see below (the run-up in private debt was actually much more impressive in the UK than in the U.S.).

More recently, economic historians have found that the best predictor of a coming financial crisis and economic recession is a large run-up in debt combined with elevated asset prices, either stocks or real estate. More specifically, private sector debt seems to matter more than public debt. The financial crisis in the U.S. and in the Eurozone, for example, was preceded by large increases in mortgage to GDP ratios and rapidly rising house prices, see below (the run-up in private debt was actually much more impressive in the UK than in the U.S.).

Real house prices and private sector loans to GDP ratio in the U.S. and the UK

Source: Òscar Jordà, Moritz Schularick, and Alan M. Taylor. 2017. “Macrofinancial History and the New Business Cycle Facts.

http://www.macrohistory.net/data/

http://www.macrohistory.net/data/

In the case of China, the country has experienced a large sunup in private sector debt over the last year with the debt to GDP ratio exceeding 250% (see graph below). Moreover, house prices have rapidly inflated at the same time.

While growth rates in the early 2000s have averaged above 10%, the country has slowed down in recent years with growth now averaging 6-7% after the Global Financial Crisis. However, this slowdown was to be expected as China’s GDP per capita rises. The country’s capacity for catch-up growth reduces as the country becomes more wealthy, thus leading to an eventual slowdown. Moreover, China’s demographics are quite unfavourable, partly a result of the one-child policy. With population growth slowing down and eventually reaching a negative, potential GDP growth is also reduced. Finally, the country has had extremely high investment rates in recent years, up to a point that many economists have started to worry about malinvestment. While high investment rates can lead to transitory growth, eventually diminishing returns will kick in. This is true both for private investment as well as for public investment (infrastructure, housing, etc.).

The big question is whether China will be able to manage a smooth transition from an unsustainable growth model with too high investment rates to a growth model that focuses to a bigger extent on domestic consumption. More recently, many economists as well as a number of financial market participants have turned extremely bearish on China, by which I mean that they were betting on an eventual economic crisis and financial collapse. During the years 2015-2017, those bets looked increasingly appealing as GDP growth slowed. Moreover, private debt increased at a higher rate. Meanwhile, the country lost about a fourth of its 4 trillion reserves over a time period of little more than a year as the Chinese were trying to defend their currency peg against the dollar, thus preventing the currency from rapidly depreciating amidst the economic slowdown. However, over the last year pressures against the currency have eased, the level of foreign reserves and private debt levels have stabilized. Moreover, many hedge funds have lost a considerable amount of money by betting against China’s macroeconomy. Being a China bear has not paid off in recent years!

While the transition from 10% growth in the early 2000s to about 6-7% growth nowadays has occurred more smoothly than anticipated, there is a question on how well the country will manage the transition to a slower growth regime. Modernisation theory, a theory that relates economic development with democratisation, has not panned out so far in the case of China. Justin Yifu Lin thinks that the country has still a lot of room for catch-up growth, given that its income per capita is barely a fifth of that of the U.S. However, the country will soon enough experience negative population growth, which should translate into a lower GDP growth rates. I’m a little bit sceptical on China’s ability to grow at above 6% over the next two decades and think that a growth rate in between 4-5% might be more realistic (given that the country does not experience a financial collapse). However, regardless on how strong the ultimate decline in potential growth will be, what matters much more is whether the country will be able to manage the transition in a smooth way. This is indeed the trillion dollar question (given the size of the Chinese economy). Furthermore, it will be of enormous importance whether the country will eventually move towards a democratic system. With the exception of the resource rich gulf states and Singapore, every rich country in the world is a Western- style democracy. This begs the question whether the China can continue to make progress being an authoritarian regime.

For now though, being bearish on China is a losing bet. Furthermore, with about 3 trillion in foreign reserves as well as a relatively low public debt to GDP ratio, the country has definitely the resources and the firepower to prevent any financial crisis from becoming a full-blown economic meltdown. In that sense, being an authoritarian regime might actually be of help, at least in the short-run, because any emergency measures can be quickly directed from above without going through lengthy parliamentary procedures.

While growth rates in the early 2000s have averaged above 10%, the country has slowed down in recent years with growth now averaging 6-7% after the Global Financial Crisis. However, this slowdown was to be expected as China’s GDP per capita rises. The country’s capacity for catch-up growth reduces as the country becomes more wealthy, thus leading to an eventual slowdown. Moreover, China’s demographics are quite unfavourable, partly a result of the one-child policy. With population growth slowing down and eventually reaching a negative, potential GDP growth is also reduced. Finally, the country has had extremely high investment rates in recent years, up to a point that many economists have started to worry about malinvestment. While high investment rates can lead to transitory growth, eventually diminishing returns will kick in. This is true both for private investment as well as for public investment (infrastructure, housing, etc.).

The big question is whether China will be able to manage a smooth transition from an unsustainable growth model with too high investment rates to a growth model that focuses to a bigger extent on domestic consumption. More recently, many economists as well as a number of financial market participants have turned extremely bearish on China, by which I mean that they were betting on an eventual economic crisis and financial collapse. During the years 2015-2017, those bets looked increasingly appealing as GDP growth slowed. Moreover, private debt increased at a higher rate. Meanwhile, the country lost about a fourth of its 4 trillion reserves over a time period of little more than a year as the Chinese were trying to defend their currency peg against the dollar, thus preventing the currency from rapidly depreciating amidst the economic slowdown. However, over the last year pressures against the currency have eased, the level of foreign reserves and private debt levels have stabilized. Moreover, many hedge funds have lost a considerable amount of money by betting against China’s macroeconomy. Being a China bear has not paid off in recent years!

While the transition from 10% growth in the early 2000s to about 6-7% growth nowadays has occurred more smoothly than anticipated, there is a question on how well the country will manage the transition to a slower growth regime. Modernisation theory, a theory that relates economic development with democratisation, has not panned out so far in the case of China. Justin Yifu Lin thinks that the country has still a lot of room for catch-up growth, given that its income per capita is barely a fifth of that of the U.S. However, the country will soon enough experience negative population growth, which should translate into a lower GDP growth rates. I’m a little bit sceptical on China’s ability to grow at above 6% over the next two decades and think that a growth rate in between 4-5% might be more realistic (given that the country does not experience a financial collapse). However, regardless on how strong the ultimate decline in potential growth will be, what matters much more is whether the country will be able to manage the transition in a smooth way. This is indeed the trillion dollar question (given the size of the Chinese economy). Furthermore, it will be of enormous importance whether the country will eventually move towards a democratic system. With the exception of the resource rich gulf states and Singapore, every rich country in the world is a Western- style democracy. This begs the question whether the China can continue to make progress being an authoritarian regime.

For now though, being bearish on China is a losing bet. Furthermore, with about 3 trillion in foreign reserves as well as a relatively low public debt to GDP ratio, the country has definitely the resources and the firepower to prevent any financial crisis from becoming a full-blown economic meltdown. In that sense, being an authoritarian regime might actually be of help, at least in the short-run, because any emergency measures can be quickly directed from above without going through lengthy parliamentary procedures.

RSS Feed

RSS Feed