So this is quite amazing. It's the middle of April now, meaning that the first quarter of 2017 is over. I just looked at current forecast of GDP growth for Q1 2017. The Atlanta Fed has a forecast of 0.6% for the first quarter of 2017 (down from 1.2% a few weeks ago). This would be pretty much stall speed, given that trend GDP growth is estimated to be about 2%. The New York Fed, on the other hand, predicts a growth rate of 2.8% for Q1 2017 (down from 3.2% a few weeks ago). An estimate that is significantly higher than trend growth. It would mean an acceleration from a relatively decent performance in the end of 2016 with an annual growth rate of 3.5% and 1.9% in the last two quarters.

So here we have it. We are more than three months into 2017 and first quarter GDP growth could more or less be anything in between 0% and 3%. This is a really wide margin of error.

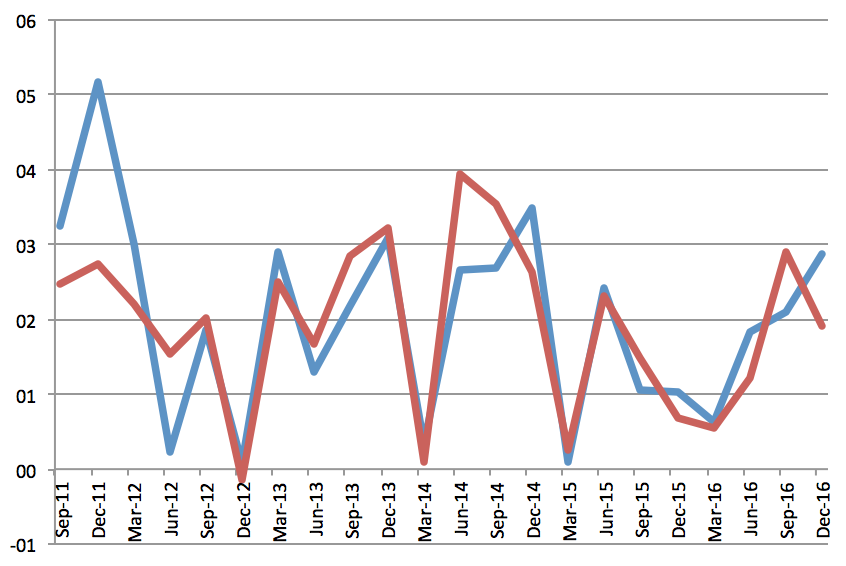

The following graph shows the GDP forecast of the Atlanta Fed with actual GDP growth. As you can see, the so-called "GDPNow" forecast does a pretty decent job at predicting quarterly growth and follows quite closely changes in the growth rate, but there are a couple of large misses along the way.

So here we have it. We are more than three months into 2017 and first quarter GDP growth could more or less be anything in between 0% and 3%. This is a really wide margin of error.

The following graph shows the GDP forecast of the Atlanta Fed with actual GDP growth. As you can see, the so-called "GDPNow" forecast does a pretty decent job at predicting quarterly growth and follows quite closely changes in the growth rate, but there are a couple of large misses along the way.

In Q3 of 2011, for example, GDPNow predicted a growth rate of about 3.2% while the actual figure for GDP growth came in at 2.5%, a difference of 0.8%. In Q2 of 2014, GDPNow predicted a growth rate of about 2.7% while the actual growth rate was later determined as 4%, a miss of 1.3%.

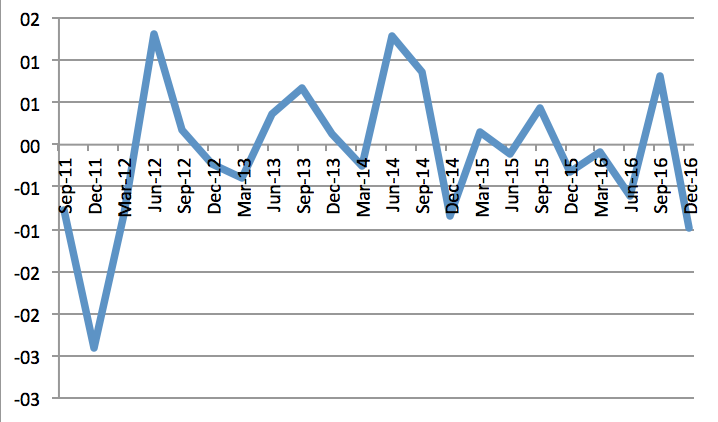

In the following graph I have plotted the difference between the GDPNow forecast and the actual growth rate.

In the following graph I have plotted the difference between the GDPNow forecast and the actual growth rate.

While a few predictions are clearly way off the mark, on average, the performance of the GDPNow tracker seems to be within a reasonable margin of error. The total sum of deviations since its introduction in Q3 2011 is 1.7%. It would be zero if the Atlanta Fed's forecast misses on the upside are as big as its misses on the downside. This number thus means that GDPNow has somewhat overestimated actual GDP growth since its introduction, but the magnitude of the effect is quite small. The average quarterly deviation in absolute values is about 0.6%.

While GDPNow performs better in the first quarter, the difference is actually not statistically significant (there are only 6 available forecasts available for each quarter since GDPNow was only introduced in 2011).

Some large inaccuracies notwithstanding, predictions about economic growth rates are not completely useless. It just means that predicting current GDP is relatively hard, but regardless these estimates still contain a lot of useful information. According to the BEA, for example, current quarterly estimates of GDP growth correctly forecast the direction of change of GDP 96% of the time. Furthermore, they correctly indicate whether GDP is accelerating or decelerating about 75% of the time, and whether current GDP growth is above or below trend 83% of the time.

Consequently, policy makers can use different GDP growth forecasts as a guideline on whether the economy is underperforming, overperforming, or growing roughly in line with the estimated long-run trend.

So what about growth in Q1 2017 ?

GDP growth in the last quarter of 2016 was 1.9%, which is roughly in line with trend growth. Monetary policy became somehwat easier this month despite the fact that the Fed hiked interest rates a week ago.

Frankly, the very low forecast of 0.9% for Q1 2017 by the Atlanta Fed seems a little suspicious to me. So I contacted Pat Higgins, the person who constructed the Nowcast model for the Atlanta Fed. According to him, most of the reducution can be attributed to lower government spending, mostly on the state and local level, as well as an increase in imports.

Similarly, the 2.8% forecast by the New York Fed would imply a dramatic acceleration in GDP growth that is quite far above trend, which also seems somewhat unlikely. There is as of now no no incoming data that would suggest that the economy is suddenly taking off at rocket speed. The concensus seems to be that the U.S. will grow at a pace of about 1.5% to 2.5%. This sounds about right as 2% is roughly the estimated trend growth. There is thus a pretty good chance that both the New York Fed as well as the Atlanta Fed are way off the mark for this quarter, but only time will tell.

What about predicting recessions ?

Economists have gotten a lot of bad press recently because they missed the Global Financial Crisis of 2008, and many also got the short-run impact of Brexit wrong, predicting a recession while the economy did not even slow down.

According to the Economist, there were 220 instances when a year of positive growth was followed by a year of negative growth across all major countries over the past several decades. In its April forecast during the year of positive growth, the IMF was unable to predict a coming recession on a single occasion!

This, however, is actually not very suprising, given our inability to accurately predict current growth rates. Furthermore, recessions are usually the result of either unexpected negative shocks that hit the economy or unpredictable policy failure. The famous German macroeconomist Rudi Dornbusch once said that economic expansions don't die of old aga, but that the Fed murdered every single one of them.

Indeed, most economic recessions in advanced economies are demand-side recessions and thus a result of macroeconomic mismanagment. Indeed, it would be very weird if we could predict recessions because that would imply that Central Bankers just idly stand by as economic conditions change. While this can happen, the example of Brexit shows that this is not the norm. There is a good chance that the Brexit vote would have caused a recession had the Bank of England not changed its policy. However, they decreased their policy rate and started a program of asset purchases (QE) in the immediate aftermath of the vote. This led to a substantial depreciation of the pound. This actually led to a slight increase in economic growth as consumers pull purchases forward in anticipation of higher inflation in the future. Instead of causing an immediate recession, the costs of Brexit will be an erosion of purchasing power as well as lower income gains that will be spread out over a period of many years. While Brexit didn't cause too much damage in the very short-run, the economic costs might become increasingly apparent over the course of a decade.

The prediction that the Brexit vote would cause a recession was wrong because the BoE quickly took the pessimistic forecasts into account and reacted to them preemptively. The BoE thus prevented the recession that would otherwise surely have taken palce was it not for the aggressive monetary easing.

In my opinion, point forecasts of economic variables are pretty much useless, especially the further out you reach into the future. Just intuitively, the economics profession would be much better off if we also provided confidence intervals around the estimate. Saying that annual GDP growth will be in between 1.5% and 2.5% with a 90% confidence interval might be much more useful than providing a point estimate of 2% that will most likely be off the mark one way or another.

Alternatively, conditional estimates can also be of use. Here an example:

Conditional on the the BoE not changing its policy stance, the Brexit vote will cause a recession.

Or:

Conditional on the BoE adapting a more accommodative stance of monetary policy by lowering its benchmark interest rates by 50 basis points, the Brexit vote will not cause a recession.

Obviously, while both scenraios cannot be true at the same time, either the BoE will change its policy or not, those are not useless forecasts to make. In order to mek such conditional forecasts even more relevant, one could attach a probability to each of the scenarios so that policy makers can rank them in order of likelihood.

So here the punchline: John Kenneth Galbraith once said "The only function of forecasting is to make astrology respectable." However, reality is not that dire. While most economic forecasts are not highly accurate, they are far from useless. Macroeconomists can, in my opinion, improve upon their reputation though by providing more conditional forecasts as well as forecast ranges instead of simply giving point estimates.

Update: I wrote this post a while ago. There are a few indicators that seem to corroborate that the Q1 2017 might not have been that good after all. March job growth was with a 100.000 new jobs in line with what Fed economists think is trend growth, but it was quite a bit lower than January and February (both about 200.000). Furthermore, car sales seem to have taken a hit recently. This seems to have been a somewhat reliable indicator of economic slowdown in the past. So maybe the Atlanta GDPNow estimate is not that far off after all. We'll know more by the end of this month when the BEA releases its first estimate of Q1 GDP growth.

Some large inaccuracies notwithstanding, predictions about economic growth rates are not completely useless. It just means that predicting current GDP is relatively hard, but regardless these estimates still contain a lot of useful information. According to the BEA, for example, current quarterly estimates of GDP growth correctly forecast the direction of change of GDP 96% of the time. Furthermore, they correctly indicate whether GDP is accelerating or decelerating about 75% of the time, and whether current GDP growth is above or below trend 83% of the time.

Consequently, policy makers can use different GDP growth forecasts as a guideline on whether the economy is underperforming, overperforming, or growing roughly in line with the estimated long-run trend.

So what about growth in Q1 2017 ?

GDP growth in the last quarter of 2016 was 1.9%, which is roughly in line with trend growth. Monetary policy became somehwat easier this month despite the fact that the Fed hiked interest rates a week ago.

Frankly, the very low forecast of 0.9% for Q1 2017 by the Atlanta Fed seems a little suspicious to me. So I contacted Pat Higgins, the person who constructed the Nowcast model for the Atlanta Fed. According to him, most of the reducution can be attributed to lower government spending, mostly on the state and local level, as well as an increase in imports.

Similarly, the 2.8% forecast by the New York Fed would imply a dramatic acceleration in GDP growth that is quite far above trend, which also seems somewhat unlikely. There is as of now no no incoming data that would suggest that the economy is suddenly taking off at rocket speed. The concensus seems to be that the U.S. will grow at a pace of about 1.5% to 2.5%. This sounds about right as 2% is roughly the estimated trend growth. There is thus a pretty good chance that both the New York Fed as well as the Atlanta Fed are way off the mark for this quarter, but only time will tell.

What about predicting recessions ?

Economists have gotten a lot of bad press recently because they missed the Global Financial Crisis of 2008, and many also got the short-run impact of Brexit wrong, predicting a recession while the economy did not even slow down.

According to the Economist, there were 220 instances when a year of positive growth was followed by a year of negative growth across all major countries over the past several decades. In its April forecast during the year of positive growth, the IMF was unable to predict a coming recession on a single occasion!

This, however, is actually not very suprising, given our inability to accurately predict current growth rates. Furthermore, recessions are usually the result of either unexpected negative shocks that hit the economy or unpredictable policy failure. The famous German macroeconomist Rudi Dornbusch once said that economic expansions don't die of old aga, but that the Fed murdered every single one of them.

Indeed, most economic recessions in advanced economies are demand-side recessions and thus a result of macroeconomic mismanagment. Indeed, it would be very weird if we could predict recessions because that would imply that Central Bankers just idly stand by as economic conditions change. While this can happen, the example of Brexit shows that this is not the norm. There is a good chance that the Brexit vote would have caused a recession had the Bank of England not changed its policy. However, they decreased their policy rate and started a program of asset purchases (QE) in the immediate aftermath of the vote. This led to a substantial depreciation of the pound. This actually led to a slight increase in economic growth as consumers pull purchases forward in anticipation of higher inflation in the future. Instead of causing an immediate recession, the costs of Brexit will be an erosion of purchasing power as well as lower income gains that will be spread out over a period of many years. While Brexit didn't cause too much damage in the very short-run, the economic costs might become increasingly apparent over the course of a decade.

The prediction that the Brexit vote would cause a recession was wrong because the BoE quickly took the pessimistic forecasts into account and reacted to them preemptively. The BoE thus prevented the recession that would otherwise surely have taken palce was it not for the aggressive monetary easing.

In my opinion, point forecasts of economic variables are pretty much useless, especially the further out you reach into the future. Just intuitively, the economics profession would be much better off if we also provided confidence intervals around the estimate. Saying that annual GDP growth will be in between 1.5% and 2.5% with a 90% confidence interval might be much more useful than providing a point estimate of 2% that will most likely be off the mark one way or another.

Alternatively, conditional estimates can also be of use. Here an example:

Conditional on the the BoE not changing its policy stance, the Brexit vote will cause a recession.

Or:

Conditional on the BoE adapting a more accommodative stance of monetary policy by lowering its benchmark interest rates by 50 basis points, the Brexit vote will not cause a recession.

Obviously, while both scenraios cannot be true at the same time, either the BoE will change its policy or not, those are not useless forecasts to make. In order to mek such conditional forecasts even more relevant, one could attach a probability to each of the scenarios so that policy makers can rank them in order of likelihood.

So here the punchline: John Kenneth Galbraith once said "The only function of forecasting is to make astrology respectable." However, reality is not that dire. While most economic forecasts are not highly accurate, they are far from useless. Macroeconomists can, in my opinion, improve upon their reputation though by providing more conditional forecasts as well as forecast ranges instead of simply giving point estimates.

Update: I wrote this post a while ago. There are a few indicators that seem to corroborate that the Q1 2017 might not have been that good after all. March job growth was with a 100.000 new jobs in line with what Fed economists think is trend growth, but it was quite a bit lower than January and February (both about 200.000). Furthermore, car sales seem to have taken a hit recently. This seems to have been a somewhat reliable indicator of economic slowdown in the past. So maybe the Atlanta GDPNow estimate is not that far off after all. We'll know more by the end of this month when the BEA releases its first estimate of Q1 GDP growth.

RSS Feed

RSS Feed