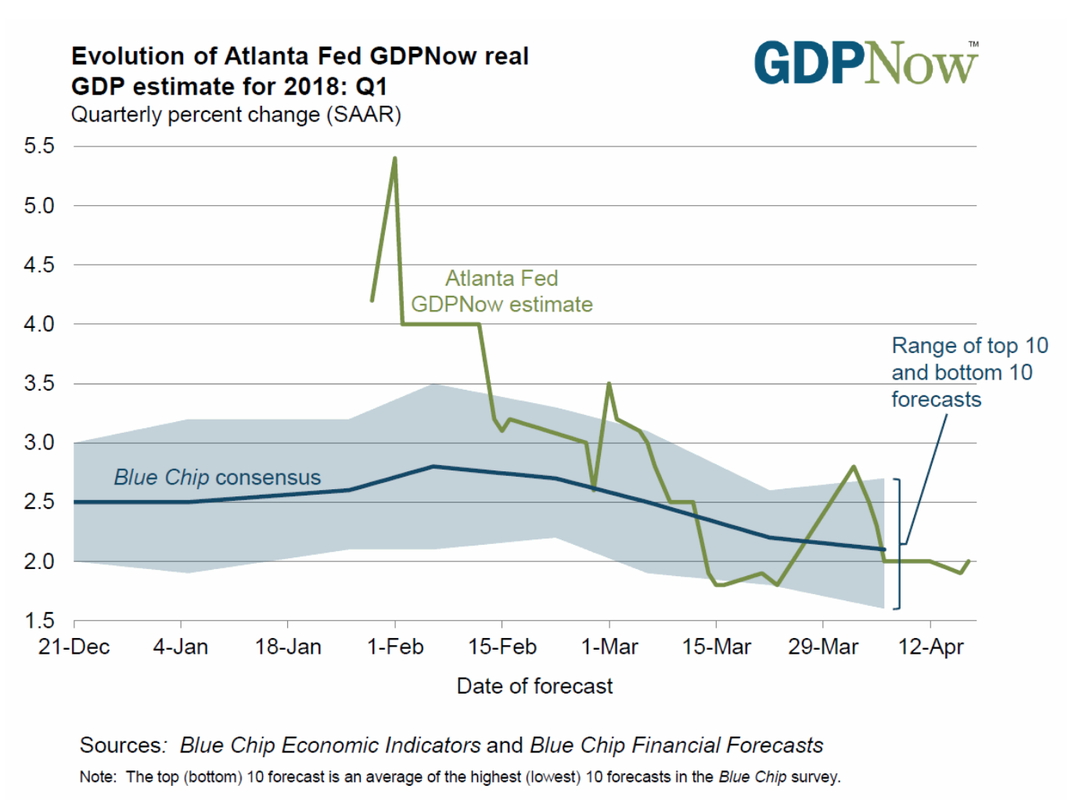

Ok. So that didn't last long. Over the last couple of years we have seen a global uptick in economic activity as both advanced and developing economies finally experienced an increase in their annual growth rates after years of mediocre macroeconomic performance at best. Unfortunately, this synchronized upswing did not seem to last very long. The Atlanta GDP Nowcast model now predicts a quarterly growth rate of only 2% for the US now for quarter 1 (just a few months ago this estimate was above 4%). While a 2% real growth rate is not abysmal, it's really not that great either.

One caveat, of course, is that over the last decade or so, growth in quarter 1 in the US has been actually much lower than growth in the other 3 quarters, implying that there might be some seasonal effect at work (weather and such). Theoretically, seasonal adjustment is supposed to take care of such effects, but this does not seem to be the case anymore.

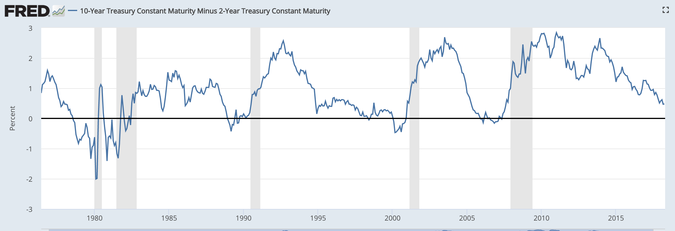

A more worrying trend is the flattening of the yield curve as can be seen by the difference between interest rates on 10-year government bonds and 2-year government bonds. An inversion of the yield curve has historically been one of the very few reliable indicators that a recession is looming.

While global factors are currently putting downward pressure on at the long-end of the yield curve, the Fed has been hiking interest rates at the short end. If they continue with their projected two to three rate hikes this year, an inversion of the yield curve seems relatively likely. Rüdiger Dornbusch once said that expansions don't die of old age, but every single one of them was murdered by the Fed. The big worry here is that Fed officials are simply too eager to hike interest rates and tighten monetary conditions even if economic conditions do not warrant the rate hikes. There is good reason to believe that the neutral equilibrium real interest rate is much lower than before the crisis, meaning that monetary policy is actually much less accommodative than what is commonly assumed.

Furthermore, one important factor that the Fed does not seem to take sufficiently into account is the dollar's continuous role as global currency. Monetary tightening in the US tends to produce ripple effects in many emerging markets where firms and consumers continue to borrow in dollars. The Fed's interest rate hikes thus imply that global monetary conditions are tightening as well.

Meanwhile in the Eurozone a lot of economic data points to a slowdown as well. This is quite worrying because policy makers at the ECB were planning to phase out QE by the end of this year despite the fact that inflation is still very much below the ECB's own target rate of close to 2%. Given that there still is quite a bit of economic slack in Southern Europe combined with the fact that inflation is too low, this should rather point towards an extension of QE.

One big worry, of course, is that the ECB is slowly but surely running out of government bonds to buy as the balance sheet increases in size. However, just as the Bank of Japan, the ECB could simply buy stocks instead, or alternatively foreign bonds (US Treasuries). Unfortunately, such proposals do not seem to be politically feasible.

One caveat, of course, is that over the last decade or so, growth in quarter 1 in the US has been actually much lower than growth in the other 3 quarters, implying that there might be some seasonal effect at work (weather and such). Theoretically, seasonal adjustment is supposed to take care of such effects, but this does not seem to be the case anymore.

A more worrying trend is the flattening of the yield curve as can be seen by the difference between interest rates on 10-year government bonds and 2-year government bonds. An inversion of the yield curve has historically been one of the very few reliable indicators that a recession is looming.

While global factors are currently putting downward pressure on at the long-end of the yield curve, the Fed has been hiking interest rates at the short end. If they continue with their projected two to three rate hikes this year, an inversion of the yield curve seems relatively likely. Rüdiger Dornbusch once said that expansions don't die of old age, but every single one of them was murdered by the Fed. The big worry here is that Fed officials are simply too eager to hike interest rates and tighten monetary conditions even if economic conditions do not warrant the rate hikes. There is good reason to believe that the neutral equilibrium real interest rate is much lower than before the crisis, meaning that monetary policy is actually much less accommodative than what is commonly assumed.

Furthermore, one important factor that the Fed does not seem to take sufficiently into account is the dollar's continuous role as global currency. Monetary tightening in the US tends to produce ripple effects in many emerging markets where firms and consumers continue to borrow in dollars. The Fed's interest rate hikes thus imply that global monetary conditions are tightening as well.

Meanwhile in the Eurozone a lot of economic data points to a slowdown as well. This is quite worrying because policy makers at the ECB were planning to phase out QE by the end of this year despite the fact that inflation is still very much below the ECB's own target rate of close to 2%. Given that there still is quite a bit of economic slack in Southern Europe combined with the fact that inflation is too low, this should rather point towards an extension of QE.

One big worry, of course, is that the ECB is slowly but surely running out of government bonds to buy as the balance sheet increases in size. However, just as the Bank of Japan, the ECB could simply buy stocks instead, or alternatively foreign bonds (US Treasuries). Unfortunately, such proposals do not seem to be politically feasible.

Atlanta GDP Nowcast US

10-year minus 2-year Treasury yield

Note that every recession (shaded grey) was preceded by an inversion of the yield curve with interest rates on 10-year bonds falling below interest rates on 2-year bonds.

PS: According to my last regression based on the results from two GDP Nowcast models (the Atlanta and the NY Fed model), the best approximation for quarterly GDP growth is the following weighted average:

0.18 * New York Fed Nowcast + 0.7 * Atlanta Nowcast

Consequently, we should expect US Q1 GDP to come in at about 0.18*2.9 + 0.7*2 = 1.92

Historically, the Atlanta model has performed better than the New York Fed model, which is why the second one has only a very small weight in the regression. Moreover, as the coefficients do not add up to one, the quarterly GDP forecast based on this regression actually comes in lower than what the Atlanta model predicts. The actual numbers will be released by the BEA today.

PS: According to my last regression based on the results from two GDP Nowcast models (the Atlanta and the NY Fed model), the best approximation for quarterly GDP growth is the following weighted average:

0.18 * New York Fed Nowcast + 0.7 * Atlanta Nowcast

Consequently, we should expect US Q1 GDP to come in at about 0.18*2.9 + 0.7*2 = 1.92

Historically, the Atlanta model has performed better than the New York Fed model, which is why the second one has only a very small weight in the regression. Moreover, as the coefficients do not add up to one, the quarterly GDP forecast based on this regression actually comes in lower than what the Atlanta model predicts. The actual numbers will be released by the BEA today.

RSS Feed

RSS Feed