I wrote this a couple of weeks ago and tried to get it published in an online newspaper. Since it didn't happen, I will publish it here now. Scott Sumner at Econlog wrote a very similar blogpost. His version is shorter and better. Read mine anyway since I have the charts. :D

Most Central Banks in advanced economies have implemented in recent decades what is known as an inflation target to ensure overall price stability in the economy. Following the bad experience of the 1970s where most countries suffered from a combination of high inflation rates and low productivity growth, economists and politicians agreed that independent Central Banks should become the ultimate goalkeeper of price stability, which would also ensure superior macroeconomic performance. However, the history of the 2% inflation target is more random than what most Central Bankers would like to admit.

Why are many Central Banks targeting 2% inflation?

Even though the high inflationary episode of the 1970s were quite scarring for many advanced countries, economists largely agree that prolonged deflationary episodes are actually much more harmful to the economy. During the Great Depression prices in the U.S. and other countries fell as much as 20% over the span of several years. This pushed up unemployment to more than 25% amidst a prolonged episode of plunging stock prices, falling house prices, and massive bank failures. Since episodes of falling prices are usually more costly to the economy, it was generally agreed upon that Central Banks should target a positive rate of inflation with the target being high enough to avoid deflationary outcomes. In 1990, the Central Bank of New Zealand was the first to implement a 2% inflation target. While the 2% number was more or less chosen at random, it seemed high enough to avoid episodes of falling prices and zero interest rates but also low enough as to be characterized as price stability: with 2% inflation prices roughly double every 36 years.

Soon enough other Central Banks followed suit and one by one adopted the same target, simply because the 2% number seemed about right and because New Zealand also had it. This is what economists call path dependency: A historical accident or initial random event leads to a sequence of events that will have a disproportionate impact on future outcomes.

Why is the 2% inflation target not appropriate?

Many macroeconomists now agree that the 2% number was badly chosen and that a higher inflation target would be more appropriate (or that Central Banks should avoid targeting prices altogether and instead target nominal GDP). In the 1990s, 2% inflation generally seemed high enough but this is no longer the case. Note that the rate of inflation is directly proportionate to the nominal interest rate, which Central Banks nowadays use to steer the economy. The Federal Reserve usually lowers its interest rate by more than 5% in response to a recession. However, during the Great Recession the Fed did not have much more room to maneuver once its interest rate hit zero as Central Banks in general cannot push interest rates far below zero. Consequently, the Fed and many other Central Banks had to resort to other tools to stimulate the economy. Most of them resorted to Quantitative Easing (QE), which is just a fancy word that describes how Central Banks purchase financial assets (government bonds, corporate bonds, and even stocks) as to inject more money into the economy in order to increase economy-wide demand.

While many studies now agree that QE was stimulative to the economy, it is a tool that seems to be somewhat more crude and maybe also less effective than directly changing the interest rate.

However, Larry Summers recently noted that interest rates have been on a steady downward trend since the late 1980s, meaning that episodes where interest rates hit the so-called zero lower bound are becoming much more likely. Central Banks would then have to resort to QE again in the case of a future recession. In order to prevent such an outcome, Central Banks could increase their inflation target instead. With higher rates of inflation, the nominal interest rate would be higher as well, which would give Central Banks more leeway to cut interest rates in the case of a future economic downturn.

Norway goes in the opposite direction?!

Norway's prior inflation target was actually at 2.5%, reflecting the fact that Norway's continuous income stream from its oil revenues would allow the government to inject some of that money into the economy with higher government spending. It is to be expected that Norway's oil revenues are going to decline in the near future as its reserves are being depleted and the government is already taking this into account by reducing the amount of money it can withdraw on annual basis from its sovereign wealth fund.

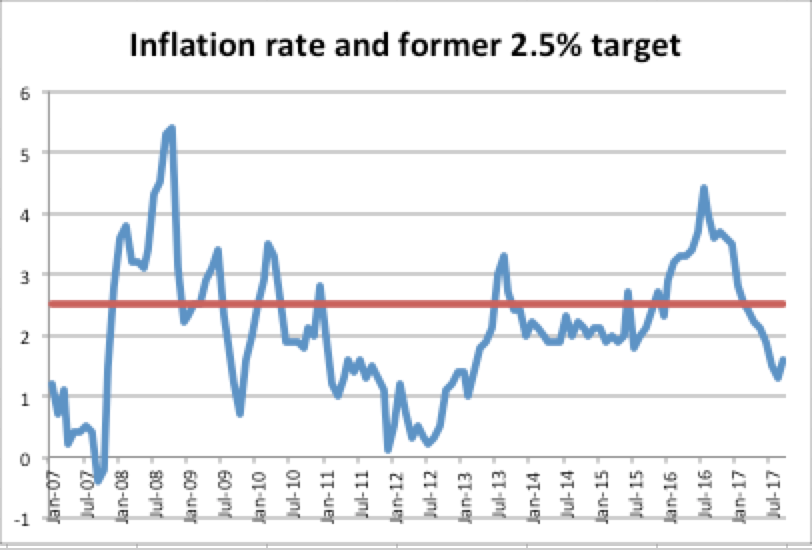

The chart below shows that Norway's inflation rate has been persistently below target in recent years. The average inflation rate from 2010 to today is almost exactly 2% instead of the actual target rate of 2.5%, meaning that the Norges Bank effectively has already behaved as if it had a 2% inflation target.

Why are many Central Banks targeting 2% inflation?

Even though the high inflationary episode of the 1970s were quite scarring for many advanced countries, economists largely agree that prolonged deflationary episodes are actually much more harmful to the economy. During the Great Depression prices in the U.S. and other countries fell as much as 20% over the span of several years. This pushed up unemployment to more than 25% amidst a prolonged episode of plunging stock prices, falling house prices, and massive bank failures. Since episodes of falling prices are usually more costly to the economy, it was generally agreed upon that Central Banks should target a positive rate of inflation with the target being high enough to avoid deflationary outcomes. In 1990, the Central Bank of New Zealand was the first to implement a 2% inflation target. While the 2% number was more or less chosen at random, it seemed high enough to avoid episodes of falling prices and zero interest rates but also low enough as to be characterized as price stability: with 2% inflation prices roughly double every 36 years.

Soon enough other Central Banks followed suit and one by one adopted the same target, simply because the 2% number seemed about right and because New Zealand also had it. This is what economists call path dependency: A historical accident or initial random event leads to a sequence of events that will have a disproportionate impact on future outcomes.

Why is the 2% inflation target not appropriate?

Many macroeconomists now agree that the 2% number was badly chosen and that a higher inflation target would be more appropriate (or that Central Banks should avoid targeting prices altogether and instead target nominal GDP). In the 1990s, 2% inflation generally seemed high enough but this is no longer the case. Note that the rate of inflation is directly proportionate to the nominal interest rate, which Central Banks nowadays use to steer the economy. The Federal Reserve usually lowers its interest rate by more than 5% in response to a recession. However, during the Great Recession the Fed did not have much more room to maneuver once its interest rate hit zero as Central Banks in general cannot push interest rates far below zero. Consequently, the Fed and many other Central Banks had to resort to other tools to stimulate the economy. Most of them resorted to Quantitative Easing (QE), which is just a fancy word that describes how Central Banks purchase financial assets (government bonds, corporate bonds, and even stocks) as to inject more money into the economy in order to increase economy-wide demand.

While many studies now agree that QE was stimulative to the economy, it is a tool that seems to be somewhat more crude and maybe also less effective than directly changing the interest rate.

However, Larry Summers recently noted that interest rates have been on a steady downward trend since the late 1980s, meaning that episodes where interest rates hit the so-called zero lower bound are becoming much more likely. Central Banks would then have to resort to QE again in the case of a future recession. In order to prevent such an outcome, Central Banks could increase their inflation target instead. With higher rates of inflation, the nominal interest rate would be higher as well, which would give Central Banks more leeway to cut interest rates in the case of a future economic downturn.

Norway goes in the opposite direction?!

Norway's prior inflation target was actually at 2.5%, reflecting the fact that Norway's continuous income stream from its oil revenues would allow the government to inject some of that money into the economy with higher government spending. It is to be expected that Norway's oil revenues are going to decline in the near future as its reserves are being depleted and the government is already taking this into account by reducing the amount of money it can withdraw on annual basis from its sovereign wealth fund.

The chart below shows that Norway's inflation rate has been persistently below target in recent years. The average inflation rate from 2010 to today is almost exactly 2% instead of the actual target rate of 2.5%, meaning that the Norges Bank effectively has already behaved as if it had a 2% inflation target.

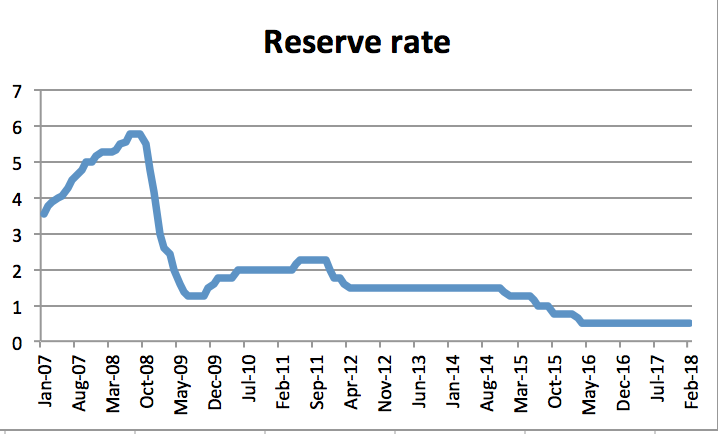

The second chart below shows that the nominal interest rate in Norway never hit the zero, being in stark contrast with most other advanced economies where the zero lower bound was a reality for many Central Bankers for many years.

This demonstrates that the Norges Bank could have pursued a more stimulative policy in recent years to push up the actual inflation rate back to its official target. However, Central Bankers in Norway effectively behaved as if they had a 2% inflation target and now simply chose to lower the target rate instead of pursuing a different policy. This seems to me completely misguided for two distinct reasons. First, it does some harm to credibility if Central Bankers simply decide to move their goalpost when they fail instead of implementing the adequate amount of stimulus.

Second, as mentioned previously, many macroeconomists and even some former Central Bankers now agree that the 2% inflation target was probably set too low. In the 1990s, it was vastly underestimated how big the danger of hitting the zero lower bound really was and how costly such episodes could be in terms of employment losses and GDP growth, as Central Banks would fail to provide the adequate amount of stimulus during recessions. In the aftermath of 2008, some Central Bankers had to grapple with the zero lower bound for several years. In that sense, the decision of Norges Bank to lower its inflation target is a step in the wrong direction and definitely seems to go against the consensus view in the economics profession. This decision could turn out to be costly in the future in the case of a severe economic downturn when Norges Bank would have to cut its interest rate by several percentage points but does not have the room to do so.

Second, as mentioned previously, many macroeconomists and even some former Central Bankers now agree that the 2% inflation target was probably set too low. In the 1990s, it was vastly underestimated how big the danger of hitting the zero lower bound really was and how costly such episodes could be in terms of employment losses and GDP growth, as Central Banks would fail to provide the adequate amount of stimulus during recessions. In the aftermath of 2008, some Central Bankers had to grapple with the zero lower bound for several years. In that sense, the decision of Norges Bank to lower its inflation target is a step in the wrong direction and definitely seems to go against the consensus view in the economics profession. This decision could turn out to be costly in the future in the case of a severe economic downturn when Norges Bank would have to cut its interest rate by several percentage points but does not have the room to do so.

RSS Feed

RSS Feed