This blogpost is inspired by Scott Sumner who is blogging at The money illusion. Scott recently wrote a couple of blogposts about Japan. Japan's monetary policy is usually described as very accommodative despite the fact that the country has experienced stagnating consumer prices for decades now. Saying that monetary policy in Japan is easy is actually quite crazy given its long-run history of mild deflation since the 1990s.

As Friedman has noted a long time ago, interest rates are an extremely poor indicator of monetary policy. The same goes for the amount of base money that Central Banks inject into the economy (such as Q.E.). Krugman and others have shown that monetary injections at the zero-lower bound will only affect the price level and thus nominal GDP if they are perceived as being permanent. Temporary monetary injections of base money, on the other hand, will have very little effect on monetary aggregates and thus also macroeconomic conditions in general. Ultimately, the only reliable indicator for the stance of monetary policy is the rate of inflation, or even better nominal GDP growth.

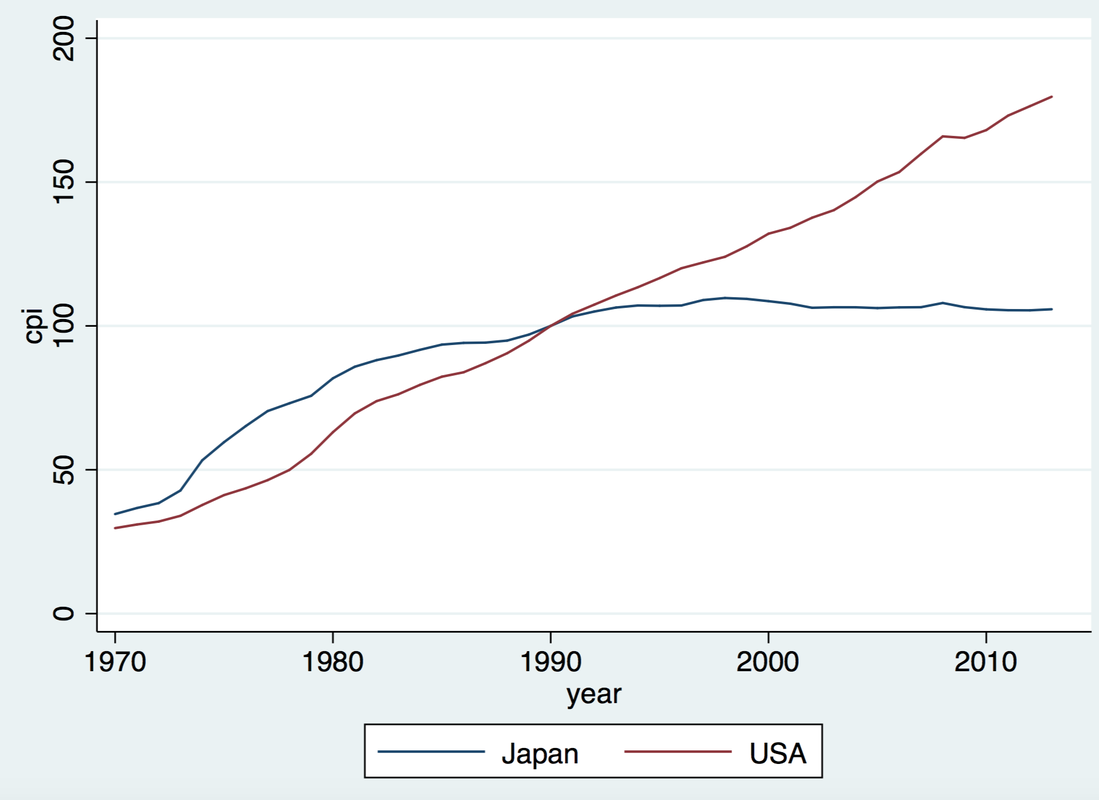

The graph below shows the Consumer Price Index for the U.S. and Japan from 1970 to 2013. The data is from the Macroeconomic History database by Jorda, Schularick, and Taylor. The CPI is expressed as an index, which assumes the value of 100 in 1990 for both countries.

As Friedman has noted a long time ago, interest rates are an extremely poor indicator of monetary policy. The same goes for the amount of base money that Central Banks inject into the economy (such as Q.E.). Krugman and others have shown that monetary injections at the zero-lower bound will only affect the price level and thus nominal GDP if they are perceived as being permanent. Temporary monetary injections of base money, on the other hand, will have very little effect on monetary aggregates and thus also macroeconomic conditions in general. Ultimately, the only reliable indicator for the stance of monetary policy is the rate of inflation, or even better nominal GDP growth.

The graph below shows the Consumer Price Index for the U.S. and Japan from 1970 to 2013. The data is from the Macroeconomic History database by Jorda, Schularick, and Taylor. The CPI is expressed as an index, which assumes the value of 100 in 1990 for both countries.

The CPI for the US has a value of about 30 in 1970 and a value of 180 in 2016. Consumer prices in the US thus increased exactly by a factor of 6 during the 43 years in question, which corresponds to an average inflation rate of 4.25%. This value is relatively high because it includes the inflationary episode of the 1970s. Average inflation would have been lower if I had started in 1980 instead.

In Japan, on the other hand, the CPI increased from about 35 to 106 over the same time period, which almost exactly corresponds to an increase by a factor of 3.

While US prices increased 6-fold, Japanese prices only increased 3-fold from 1970 to 2013, meaning that the Japanese inflation rate was on average 2.58%. Again, this value would have been much lower if I had started with the analysis one or two decades later: As one can see from the graph, Japanese prices stayed more or less constant from 1990 to 2010, implying an average inflation rate of about 0% during those two decades.

The average inflation differential between the two countries corresponds to about 1.7% over the entire time period under consideration. In the long-run, we expect Purchasing Power Parity (PPP) to hold, meaning that traded goods in different countries must have the same price (abstracting from shipping costs and other barriers that might prove to be an obstacle to international goods arbitrage). PPP must be true in the long-run because if it was not firms would be able to make an arbitrage profit.

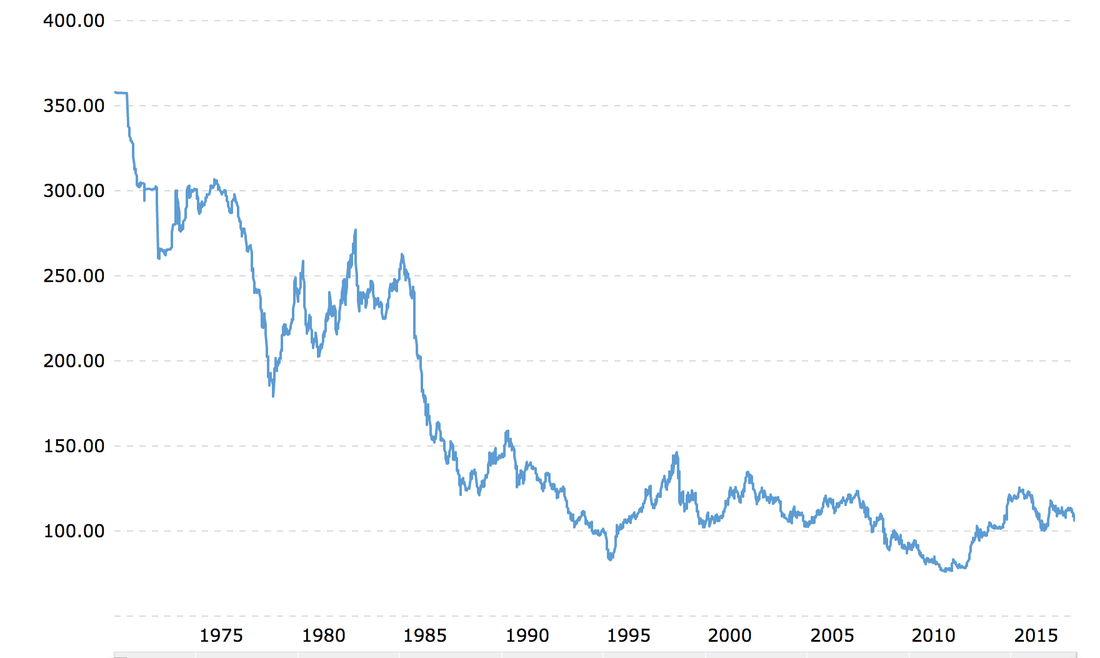

Based on the average inflation differential of 1.7% between the US and Japan on annual basis, we thus expect the Japanese Yen to appreciate by the same amount in the long-run, corresponding to an appreciation of about 106% over the 43 years in question based on PPP. The graph below shows the Yen-Dollar exchange rate. As a lower value thus implies a stronger Yen (Yen appreciation), one can see that the Yen has really appreciated by roughly the same amount over the last 4 decades.

In Japan, on the other hand, the CPI increased from about 35 to 106 over the same time period, which almost exactly corresponds to an increase by a factor of 3.

While US prices increased 6-fold, Japanese prices only increased 3-fold from 1970 to 2013, meaning that the Japanese inflation rate was on average 2.58%. Again, this value would have been much lower if I had started with the analysis one or two decades later: As one can see from the graph, Japanese prices stayed more or less constant from 1990 to 2010, implying an average inflation rate of about 0% during those two decades.

The average inflation differential between the two countries corresponds to about 1.7% over the entire time period under consideration. In the long-run, we expect Purchasing Power Parity (PPP) to hold, meaning that traded goods in different countries must have the same price (abstracting from shipping costs and other barriers that might prove to be an obstacle to international goods arbitrage). PPP must be true in the long-run because if it was not firms would be able to make an arbitrage profit.

Based on the average inflation differential of 1.7% between the US and Japan on annual basis, we thus expect the Japanese Yen to appreciate by the same amount in the long-run, corresponding to an appreciation of about 106% over the 43 years in question based on PPP. The graph below shows the Yen-Dollar exchange rate. As a lower value thus implies a stronger Yen (Yen appreciation), one can see that the Yen has really appreciated by roughly the same amount over the last 4 decades.

Starting in the early 1970s, the Yen-dollar exchange rate was about 300. Based on the inflation differential of 1.7% between the two countries, we would expect the Japanese Yen to appreciate by about the same amount on a yearly basis in the long-run. The graph above shows that this is basically what has happened.

Using a Yen-dollar exchange rate of 300 as a starting point, the PPP exchange rate is expected to be at 144 in 2013. However, maybe the Yen was a little overvalued in the early 1970s. Remember that the period just before corresponds to the Bretton-Woods arrangement where all major currencies were pegged to the dollar. Using an exchange rate of 250 as a starting point leads to a PPP exchange rate of 120, which basically corresponds to the actual value of the Yen-dollar in 2014. Purchasing power parity holds in the long-run!

Scott recently noted that the 30-year forward Yen-dollar exchange rate implied a value of a little more than 60 yen to the dollar in 30 years, thus implying continuous Yen appreciation coming forward. While the Yen-forward is maybe not a very liquid financial market, this forward rate is ultimately not very surprising.

Let's assume that the Bank of Japan has lost all its credibility and that it will not be able to reach its inflation target of 2% in the near future. If the current inflation differential between the US and Japan persists at about 1.7%, this implies a 30-year forward Yen-dollar exchange rate of 65 based on PPP. We can thus expect continuous Yen appreciation in the future.

What about interest rates?

Well, in the long-run we expect the interest rate parity to hold. If the Yen appreciates by about 1.7% to the dollar on an annual basis, nominal Japanese interest rates must be lower by roughly the same amount so that real returns are roughly equalized across countries, otherwise financial arbitrage opportunities will exist (abstracting from country-specific risk premiums, illiquid financial markets, etc.).

Over the last two years, we have seen a global uptick in economic activity with a higher synchronized growth rate across all advanced economies (bar the UK). The Fed was thus able to increase their short-run rate as the U.S. economy is approaching full employment. We can expect Eurozone interest rates to increase as well in the coming years as the Eurozone economies are starting to recover. A global synchronized increase in interest rates might thus also imply eventually somewhat higher interest rates in Japan, but don't hold your breath for too long. Given the substantial inflation differential, one should expect nominal interest rates in Japan to remain low going forward, and as noted above, the Yen is expected to continue its long-run appreciation vis-a-vis the dollar based on PPP.

What about yield-curve control?

About a year ago, I was quite sympathetic to the argument that pegging the long-run 10-year Japanese bond yield at zero was an aggressive policy move and implied substantial monetary easing. It allowed the Bank of Japan (BOJ) to keep long-run interest rates very low without buying a substantial amount of Japanese bonds: with about 50% of the bond market already on the balance sheet of the BOJ the fear was that they might ultimately run out of government bonds to buy and/ or create major market distortions. But I have revised my opinion now about this policy and I am starting to think that it was a major mistake. Low nominal interest rates imply continuous Yen appreciation in the future, which is ultimately a contractionary move.

I think that the BOJ needs to follow Lars Svensson's approach of escaping the liquidity trap. They must devalue the Yen versus the dollar. This would ultimately translate into a higher rate of inflation and they would thus be able to escape the current zero-interest rate environment. Given the PPP condition, a dollar peg would imply a long-run inflation rate similar to the Fed's target of 2%, Japan would ultimately "import" US inflation and thus finally reach their target. The only question is whether they would want to peg the Yen at the current spot rate, or whether they would want to devalue it first by let's say 10% and then peg it to the dollar. It all boils down to whether the current exchange rate is roughly in line with PPP or whether it is somewhat overvalued (or undervalued). The question on what exactly the equilibrium exchange rate is supposed to be is, however, not that easy to determine.

While such a peg to the dollar is probably not feasible from a political point of view, there is no question that the BOJ could actually pursue such a regime and prevent the Yen from appreciating in the future. If they run out of domestic government bonds to buy, they can always resort to buying U.S. government bonds instead. However, if the peg is credible just as it is with the Danish peg to the Euro, then they probably do not need to buy a lot of financial assets at all in order to prevent an appreciation of the Yen from happening in the first place. Ultimately, it all boils down to Central Bank credibility.

Using a Yen-dollar exchange rate of 300 as a starting point, the PPP exchange rate is expected to be at 144 in 2013. However, maybe the Yen was a little overvalued in the early 1970s. Remember that the period just before corresponds to the Bretton-Woods arrangement where all major currencies were pegged to the dollar. Using an exchange rate of 250 as a starting point leads to a PPP exchange rate of 120, which basically corresponds to the actual value of the Yen-dollar in 2014. Purchasing power parity holds in the long-run!

Scott recently noted that the 30-year forward Yen-dollar exchange rate implied a value of a little more than 60 yen to the dollar in 30 years, thus implying continuous Yen appreciation coming forward. While the Yen-forward is maybe not a very liquid financial market, this forward rate is ultimately not very surprising.

Let's assume that the Bank of Japan has lost all its credibility and that it will not be able to reach its inflation target of 2% in the near future. If the current inflation differential between the US and Japan persists at about 1.7%, this implies a 30-year forward Yen-dollar exchange rate of 65 based on PPP. We can thus expect continuous Yen appreciation in the future.

What about interest rates?

Well, in the long-run we expect the interest rate parity to hold. If the Yen appreciates by about 1.7% to the dollar on an annual basis, nominal Japanese interest rates must be lower by roughly the same amount so that real returns are roughly equalized across countries, otherwise financial arbitrage opportunities will exist (abstracting from country-specific risk premiums, illiquid financial markets, etc.).

Over the last two years, we have seen a global uptick in economic activity with a higher synchronized growth rate across all advanced economies (bar the UK). The Fed was thus able to increase their short-run rate as the U.S. economy is approaching full employment. We can expect Eurozone interest rates to increase as well in the coming years as the Eurozone economies are starting to recover. A global synchronized increase in interest rates might thus also imply eventually somewhat higher interest rates in Japan, but don't hold your breath for too long. Given the substantial inflation differential, one should expect nominal interest rates in Japan to remain low going forward, and as noted above, the Yen is expected to continue its long-run appreciation vis-a-vis the dollar based on PPP.

What about yield-curve control?

About a year ago, I was quite sympathetic to the argument that pegging the long-run 10-year Japanese bond yield at zero was an aggressive policy move and implied substantial monetary easing. It allowed the Bank of Japan (BOJ) to keep long-run interest rates very low without buying a substantial amount of Japanese bonds: with about 50% of the bond market already on the balance sheet of the BOJ the fear was that they might ultimately run out of government bonds to buy and/ or create major market distortions. But I have revised my opinion now about this policy and I am starting to think that it was a major mistake. Low nominal interest rates imply continuous Yen appreciation in the future, which is ultimately a contractionary move.

I think that the BOJ needs to follow Lars Svensson's approach of escaping the liquidity trap. They must devalue the Yen versus the dollar. This would ultimately translate into a higher rate of inflation and they would thus be able to escape the current zero-interest rate environment. Given the PPP condition, a dollar peg would imply a long-run inflation rate similar to the Fed's target of 2%, Japan would ultimately "import" US inflation and thus finally reach their target. The only question is whether they would want to peg the Yen at the current spot rate, or whether they would want to devalue it first by let's say 10% and then peg it to the dollar. It all boils down to whether the current exchange rate is roughly in line with PPP or whether it is somewhat overvalued (or undervalued). The question on what exactly the equilibrium exchange rate is supposed to be is, however, not that easy to determine.

While such a peg to the dollar is probably not feasible from a political point of view, there is no question that the BOJ could actually pursue such a regime and prevent the Yen from appreciating in the future. If they run out of domestic government bonds to buy, they can always resort to buying U.S. government bonds instead. However, if the peg is credible just as it is with the Danish peg to the Euro, then they probably do not need to buy a lot of financial assets at all in order to prevent an appreciation of the Yen from happening in the first place. Ultimately, it all boils down to Central Bank credibility.

RSS Feed

RSS Feed