Explainer: why some current account imbalances are fine but others are catastrophic

In the recent economic crises in Turkey and Argentina, there was much talk about how current account deficits played a big part in their problems. Nothing unusual in that, of course: many economic crises are associated with such deficits. It’s one reason why the business press focuses on the current account as one of the key measures of a country’s macroeconomic performance.

The current account balance is primarily the difference between a country’s total exports and imports of goods and services, usually measured as a share of GDP. Surpluses tend to be reported as “good” or “healthy”, while deficits are often regarded as “bad”. While the deficits run up in Turkey and Argentina certainly did cause problems, this way of looking at current accounts is fundamentally flawed.

Most people probably tend to think of exports and imports in terms of products being bought and sold by a country. In reality, they also refer to the amount of capital flowing in and out to finance government and business spending. When a country has a current account surplus, it is exporting capital to the rest of the world. Consequently, it is a net lender. Countries with deficits are the opposite: they import capital from the rest of the world and are net borrowers.

The point is that being a net borrower or net lender is not usually bad in itself – it depends on what is happening to the money. Take the US and Australia, whose current accounts as a percentage of GDP since 1980 are in the chart below. The US has been running persistent deficits for almost the entire period.

US and Australia current accounts

The US deficit peaked at about 5% of GDP in the mid-2000s, just before the outbreak of the global financial crisis. Yet US economic growth has been comparable or better than that of many other large economies for much of this period.

While that is true, some economists argue that deficits are not sustainable in the long run. The US, they say, has only been able to run one for so long because of the unique role of the US dollar as the international reserve currency.

Yet what about Australia? The Australian dollar has no such special status and that country has been running more sizeable deficits than the US over the same time period. Australia finances this by selling domestic assets to foreigners, such as wealthy Chinese families buying expensive apartments in Sydney. Australia clearly has enough space to build more and more real estate to keep financing its imports. Whether this is socially desirable is a different question, of course.

Surplus troubles

In some situations, running excessive imbalances over a prolonged period of time might be more problematic. Some economists believe that the long-term imbalances in the world economy that were partly thanks to America’s deficits caused the financial crisis and the great recession that followed.

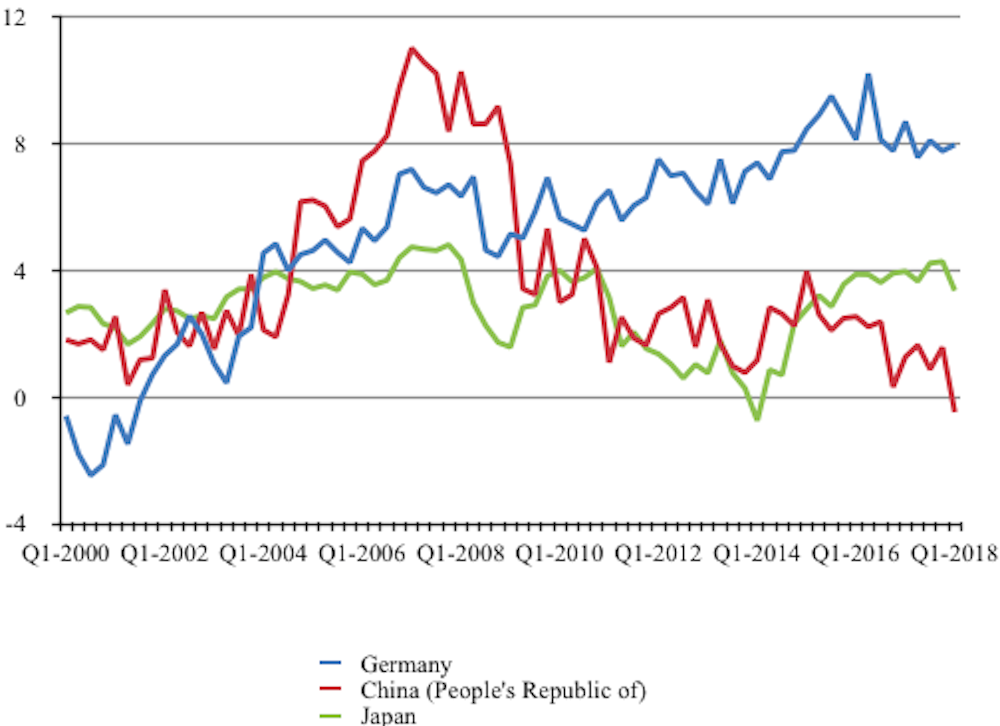

Yet surpluses can be troublesome, too. The world’s biggest surplus countries in recent years have been China, Germany and Japan. Germany has seen a large increase in its current account surplus in recent years and has been criticised by the likes of the IMF for not investing enough at home. The country is currently exporting capital of more than €250 billion a year to the rest of the world, helping to finance unstable imbalances elsewhere, while Germany’s infrastructure seems to be in dire need of additional funding.

Leading surplus offenders

China started running a massive surplus in excess of 8% in the early 2000s after becoming more integrated with the world economy and exporting goods heavily on the back of ultra-low manufacturing costs. China, too, came under international pressure for helping to cause global imbalances. While China’s trading position has now swung almost towards being balanced, it still has a substantial surplus with the US, which explains Donald Trump’s recent trade war with Beijing.

Turkish blight

Current account deficits are more dangerous if the inflow of capital does not represent productive long-term investments, but rather short-term “hot money”. Capital flows can rapidly reverse as foreign lenders abruptly start withdrawing their money. This can make the country’s currency plummet, culminating in a financial crisis if domestic banks, businesses and even consumers have been borrowing in foreign currency and the repayments are suddenly beyond their reach.

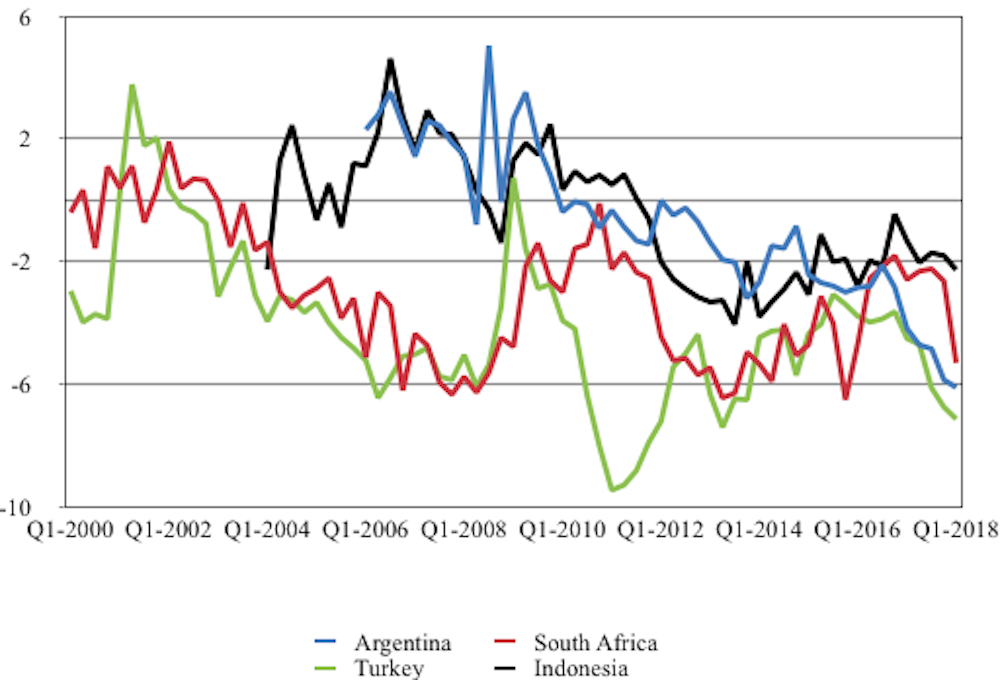

This is exactly what has happened in Argentina and Turkey this year. Turkey’s persistent deficits were a sign of the country’s reliance on foreign borrowing to fuel its domestic consumption boom under the Erdoğan regime, which came unstuck as the West called time on quantitative easing and started raising interest rates.

Emerging economy deficits

Indonesia and South Africa are two more emerging markets whose current account balances have been shifting. Both the Indonesian rupiah and South African rand have depreciated by about 10% against the US dollar over the last year.

While economists mostly agree that floating exchange rates and mild depreciations can be rather helpful in absorbing macroeconomic shocks, both countries look potentially vulnerable in a similar way to Turkey and Argentina – particularly if the rand or rupiah were to experience a “run” similar to the one on the Turkish lira. Unfortunately, just like a banking panic, currency crises and financial contagion are usually unpredictable beforehand.

At any rate, it’s important to be more accurate about current account imbalances. Large and continuous deficits or surpluses can either be totally benign or the result of some underlying economic problem. Still, some people persist in seeing only the bad in deficits. Donald Trump is a good example: he promised to eliminate America’s deficit during the presidential campaign and believes his massive tax cut will produce a growth surge that will achieve that goal in the years ahead. The irony, of course, is that in all probability it will achieve precisely the opposite.

Julius Probst, Doctoral Researcher in Economic History, Lund University

This article was originally published on The Conversation. Read the original article.

RSS Feed

RSS Feed