Every now and then it is extremely important to ponder about wrong predictions. Just before the US election I wrote about the fact that from an economic history point of view it would actually make sense for Trump to win the election. The financial crisis of 2008 and its aftermath, the policy mistakes that were made, the rise of populism, all of this bore a striking resemblances to the Great Depression and the nationalism that followed it. And Nate Silver's model at 538 gave Trump actually about a 33% chance of winning the electoral college, which was much higher than what most political pundits predicted at the time. Based on this, I wrote at the time that Trump wining the election might actually make sense while at the same time hoping that I was dead wrong. Well, unfortunately I wasn't.

However, right after the election I made another prediction concerning the value of the dollar. Based on Trump's initial policy proposals, a large infrastructure program and massive tax cuts, I wrote that more expansionary fiscal policy would lead to a faster interest rate normalization by the Federal Reserve, which would push up the value of the dollar.

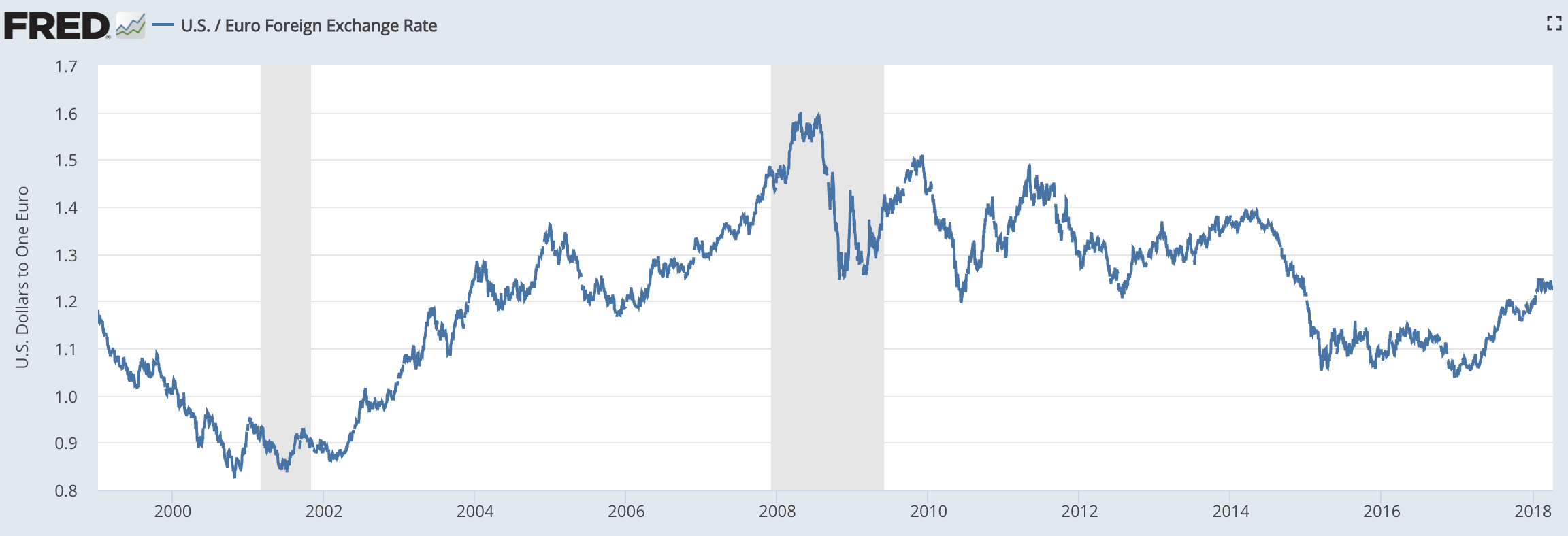

While I was right initially, the dollar did indeed rally right after the election, this forecast doesn't look so great now. Yes, the Federal Reserve has proceeded with its rate hikes as planned. However, the dollar actually declined in value over the last year and was one of the weakest performing currencies of advanced economies (see chart below).

However, right after the election I made another prediction concerning the value of the dollar. Based on Trump's initial policy proposals, a large infrastructure program and massive tax cuts, I wrote that more expansionary fiscal policy would lead to a faster interest rate normalization by the Federal Reserve, which would push up the value of the dollar.

While I was right initially, the dollar did indeed rally right after the election, this forecast doesn't look so great now. Yes, the Federal Reserve has proceeded with its rate hikes as planned. However, the dollar actually declined in value over the last year and was one of the weakest performing currencies of advanced economies (see chart below).

Dollar - Euro exchange rates

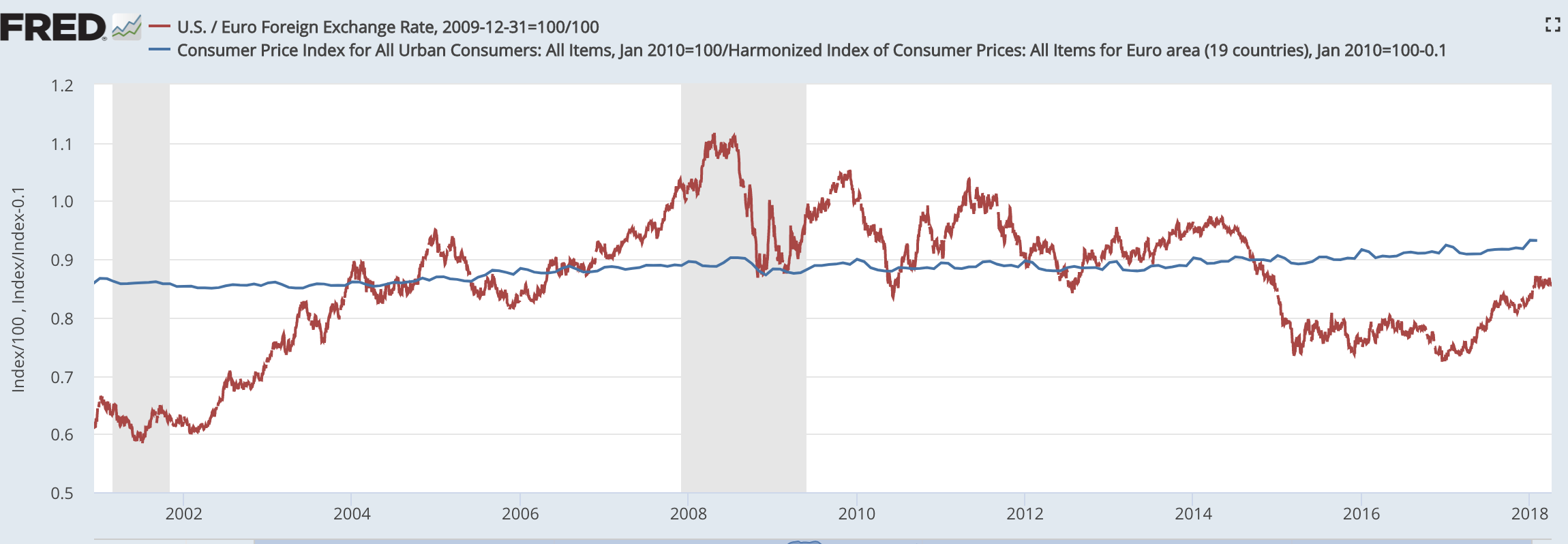

Dollar - Euro exchange rate as an index and the PPP line (Purchasing Power Parity)

So it's worth pondering why this prediction turned out to be wrong. First, it should be noted that currency movements are really hard to forecast, especially in the short-run. Similar to other asset prices, currencies actually tend to behave like a random walk, at least over short time horizons, meaning that a simple coin toss repeatedly performs just as well than more elaborate macroeconomic models.

However, in the long-run we know that Purchasing Power Parity (PPP) must roughly hold. PPP asserts that relative inflation levels will in the medium to long-run dominate international currency movements. This must be true because of international goods arbitrage. More specifically, abstracting from shipping costs, the price of internationally traded goods must be equalized (that is pre-tax, of course) because otherwise arbitrage opportunity exists.

If you think the dollar was roughly in line with PPP in the mid-2000s, i.e. 2004-2006, then one can also see that the Euro was actually quite undervalued in recent years.

In 2014, the ECB finally started its own program of Quantitative Easing (asset purchases) in order to increase aggregate demand in the Eurozone. As a result, the Euro depreciated sharply, which is exactly in accordance with standard monetary theory: Dornbusch's overshooting hypothesis. Given that the dollar was already overvalued on the eve of Trump's election (based on PPP), it would actually have been a stretch to predict continuous appreciation even if some of the factors would actually push up the value of the dollar in the very short-run, such as more rapid monetary policy tightening by the Fed than in Europe combined with expansionary fiscal policy.

In the long-run, however, we should actually expect continuous depreciation of the dollar vis-a-vis the Euro for two reasons. First, one can see in my graph above that the dollar might actually still be slightly undervalued from a PPP perspective. This, however, somewhat depends on the initial equilibrium value of the exchange rate based on PPP in the mid-2000s.

Second, while it now looks like the Fed is fulfilling its mandate of price stability defined as 2% inflation in the medium run, the ECB is still likely to undershoot its inflation target for years to come. This, of course, implies that there will be an inflation differential between the two economies in the decade ahead. With somewhat higher inflation in the US than in the Eurozone, the dollar is expected to depreciate from a PPP perspective by the amount of the inflation differential in the decade to come.

So while some factors initially pointed towards relative dollar strengths in the short-run, which is what I counting on in the aftermath of the election, one shouldn't be surprised by a dollar-euro exchange rate of about 1.25 to 1.4 in the years ahead, which certainly seems to be where we are heading right now.

PS: I just realized that I wrote a very similar blog post already last summer.

macrothoughts.weebly.com/blog/the-current-dollar-depreciation-and-a-wrong-prediction

However, in the long-run we know that Purchasing Power Parity (PPP) must roughly hold. PPP asserts that relative inflation levels will in the medium to long-run dominate international currency movements. This must be true because of international goods arbitrage. More specifically, abstracting from shipping costs, the price of internationally traded goods must be equalized (that is pre-tax, of course) because otherwise arbitrage opportunity exists.

If you think the dollar was roughly in line with PPP in the mid-2000s, i.e. 2004-2006, then one can also see that the Euro was actually quite undervalued in recent years.

In 2014, the ECB finally started its own program of Quantitative Easing (asset purchases) in order to increase aggregate demand in the Eurozone. As a result, the Euro depreciated sharply, which is exactly in accordance with standard monetary theory: Dornbusch's overshooting hypothesis. Given that the dollar was already overvalued on the eve of Trump's election (based on PPP), it would actually have been a stretch to predict continuous appreciation even if some of the factors would actually push up the value of the dollar in the very short-run, such as more rapid monetary policy tightening by the Fed than in Europe combined with expansionary fiscal policy.

In the long-run, however, we should actually expect continuous depreciation of the dollar vis-a-vis the Euro for two reasons. First, one can see in my graph above that the dollar might actually still be slightly undervalued from a PPP perspective. This, however, somewhat depends on the initial equilibrium value of the exchange rate based on PPP in the mid-2000s.

Second, while it now looks like the Fed is fulfilling its mandate of price stability defined as 2% inflation in the medium run, the ECB is still likely to undershoot its inflation target for years to come. This, of course, implies that there will be an inflation differential between the two economies in the decade ahead. With somewhat higher inflation in the US than in the Eurozone, the dollar is expected to depreciate from a PPP perspective by the amount of the inflation differential in the decade to come.

So while some factors initially pointed towards relative dollar strengths in the short-run, which is what I counting on in the aftermath of the election, one shouldn't be surprised by a dollar-euro exchange rate of about 1.25 to 1.4 in the years ahead, which certainly seems to be where we are heading right now.

PS: I just realized that I wrote a very similar blog post already last summer.

macrothoughts.weebly.com/blog/the-current-dollar-depreciation-and-a-wrong-prediction

RSS Feed

RSS Feed