Central Bankers very often refer to the so-called natural rate of unemployment when making monetary policy. The natural rate is the unemployment rate that is consistent with full employment and price stability.

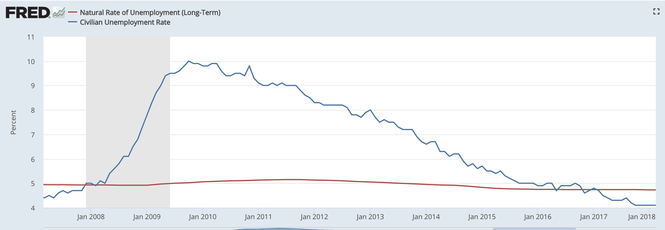

In the graph below, I have plotted the actual unemployment rate for the US as well as estimates for the natural rate. Unemployment last month in the US went down to 3.9%, which is the first time in almost two decades that US unemployment is below 4%. While there is an argument to be made that the US is approaching full employment, the labor force participation rate for prime aged workers is still somewhat depressed compared to the its rate before the financial crisis. Furthermore, despite approaching full employment, wage growth has been relatively timid in recent years. There is a debate raging among macroeconomists at the moment about the Phillips curve and why the theoretical relationship between labor market slack and inflation (or wage growth) has broken down in recent years. The slope of the Phillips curve has become extremely flat, meaning that price and wage growth ahve not picked up despite the fact that the US economy has approached full employment. While this poses some problems for mainstream economics, one can actually show in a standard AS-AD framework (aggregate supply - aggregate demand) why an economy can experience a period of disinflation while approaching full employment. I might have to say something about this another time.

For now, I want to emphasize that most standard estimates of the natural rate of unemployment are still well above 4% (the Fed's own estimate is at 4.5% at the moment). This would imply that the US economy is experiencing quite a boom at the moment and that the labor market is already overheating.

Quite frankly, I find such an assertion relatively strange, given that wage growth is still well below pre-crisis levels. One should be extremely frank about the fact that economists have actually no idea where the natural rate is (or whether it even exists) and therefore it is an extremely poor indicator for monetary policy.

Just a few years ago, economists at the Fed actually believed that they wouldn't be able to push the unemployment below 6% or so. Well, boy were they wrong. Good thing that there were alternative voices at the Fed that ultimately prevailed because otherwise millions of workers would now be without a job if the Fed had tightened monetary policy prematurely. Aiming for full employment is one the best policies to ensure prosperity and reduce inequality as the least skilled workers as well as minorities suffer the most from a weak labor market.

There are usually huge uncertainties (large confidence inetrvals) when it comes to estimating the natural rate of unemployment as well as the natural rate of interest, which implies that they are usually poor guides to policy making.

In his book Prosperity for all, Roger Farmer goes so far as to suggest that the natural rate of unemployment might actually not exist and that there is a range of unemployment rates, which are consistent with price stability. By the way, this knowledge problem also implies that monetary policy makers should rather target nominal GDP instead, which is a well-known quantity and does not rely on unreliable estimates of the natural rate.

All of this suggests that the FED really should not hit on the brakes too soon. During the late 1990s, Greenspan did a great job when he was heading the Fed as he convinced economists that the productivity boom associated with the technology "bubble" also led to an employment boom. Ultimately, the Fed was able to push down the unemployment rate below 4% without creating additional inflation.

Policy makers at the Fed would do well to remember this period. An estimate of the natural rate of about 4.7% looks quite ridiculous now as we have already breached the 4% mark. Ultimately, the natural rate could even be much lower and unemployment might reach a low of maybe 3.5% within the next year or two. This, however, rests on the assumption that the Fed is willing to let the labor market run hot and does not engage in premature tightening.

In the graph below, I have plotted the actual unemployment rate for the US as well as estimates for the natural rate. Unemployment last month in the US went down to 3.9%, which is the first time in almost two decades that US unemployment is below 4%. While there is an argument to be made that the US is approaching full employment, the labor force participation rate for prime aged workers is still somewhat depressed compared to the its rate before the financial crisis. Furthermore, despite approaching full employment, wage growth has been relatively timid in recent years. There is a debate raging among macroeconomists at the moment about the Phillips curve and why the theoretical relationship between labor market slack and inflation (or wage growth) has broken down in recent years. The slope of the Phillips curve has become extremely flat, meaning that price and wage growth ahve not picked up despite the fact that the US economy has approached full employment. While this poses some problems for mainstream economics, one can actually show in a standard AS-AD framework (aggregate supply - aggregate demand) why an economy can experience a period of disinflation while approaching full employment. I might have to say something about this another time.

For now, I want to emphasize that most standard estimates of the natural rate of unemployment are still well above 4% (the Fed's own estimate is at 4.5% at the moment). This would imply that the US economy is experiencing quite a boom at the moment and that the labor market is already overheating.

Quite frankly, I find such an assertion relatively strange, given that wage growth is still well below pre-crisis levels. One should be extremely frank about the fact that economists have actually no idea where the natural rate is (or whether it even exists) and therefore it is an extremely poor indicator for monetary policy.

Just a few years ago, economists at the Fed actually believed that they wouldn't be able to push the unemployment below 6% or so. Well, boy were they wrong. Good thing that there were alternative voices at the Fed that ultimately prevailed because otherwise millions of workers would now be without a job if the Fed had tightened monetary policy prematurely. Aiming for full employment is one the best policies to ensure prosperity and reduce inequality as the least skilled workers as well as minorities suffer the most from a weak labor market.

There are usually huge uncertainties (large confidence inetrvals) when it comes to estimating the natural rate of unemployment as well as the natural rate of interest, which implies that they are usually poor guides to policy making.

In his book Prosperity for all, Roger Farmer goes so far as to suggest that the natural rate of unemployment might actually not exist and that there is a range of unemployment rates, which are consistent with price stability. By the way, this knowledge problem also implies that monetary policy makers should rather target nominal GDP instead, which is a well-known quantity and does not rely on unreliable estimates of the natural rate.

All of this suggests that the FED really should not hit on the brakes too soon. During the late 1990s, Greenspan did a great job when he was heading the Fed as he convinced economists that the productivity boom associated with the technology "bubble" also led to an employment boom. Ultimately, the Fed was able to push down the unemployment rate below 4% without creating additional inflation.

Policy makers at the Fed would do well to remember this period. An estimate of the natural rate of about 4.7% looks quite ridiculous now as we have already breached the 4% mark. Ultimately, the natural rate could even be much lower and unemployment might reach a low of maybe 3.5% within the next year or two. This, however, rests on the assumption that the Fed is willing to let the labor market run hot and does not engage in premature tightening.

US unemployment rate, actual vs. natural

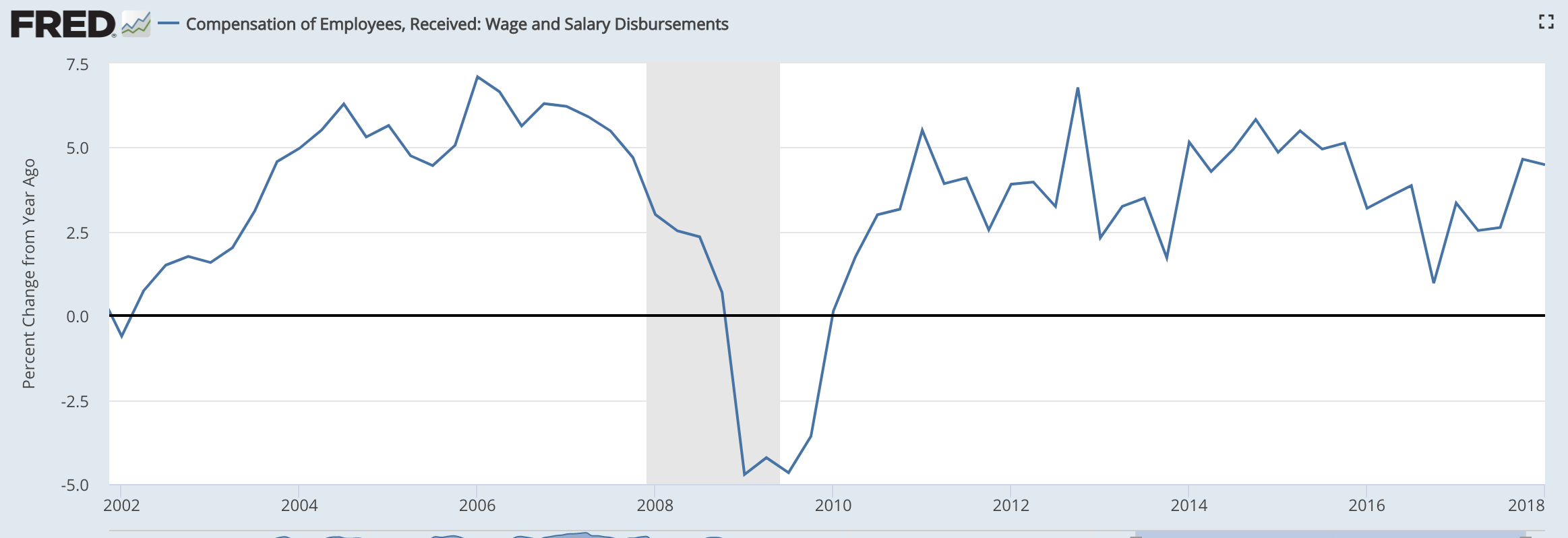

Wage growth still before pre-crisis levels despite labor market tightening

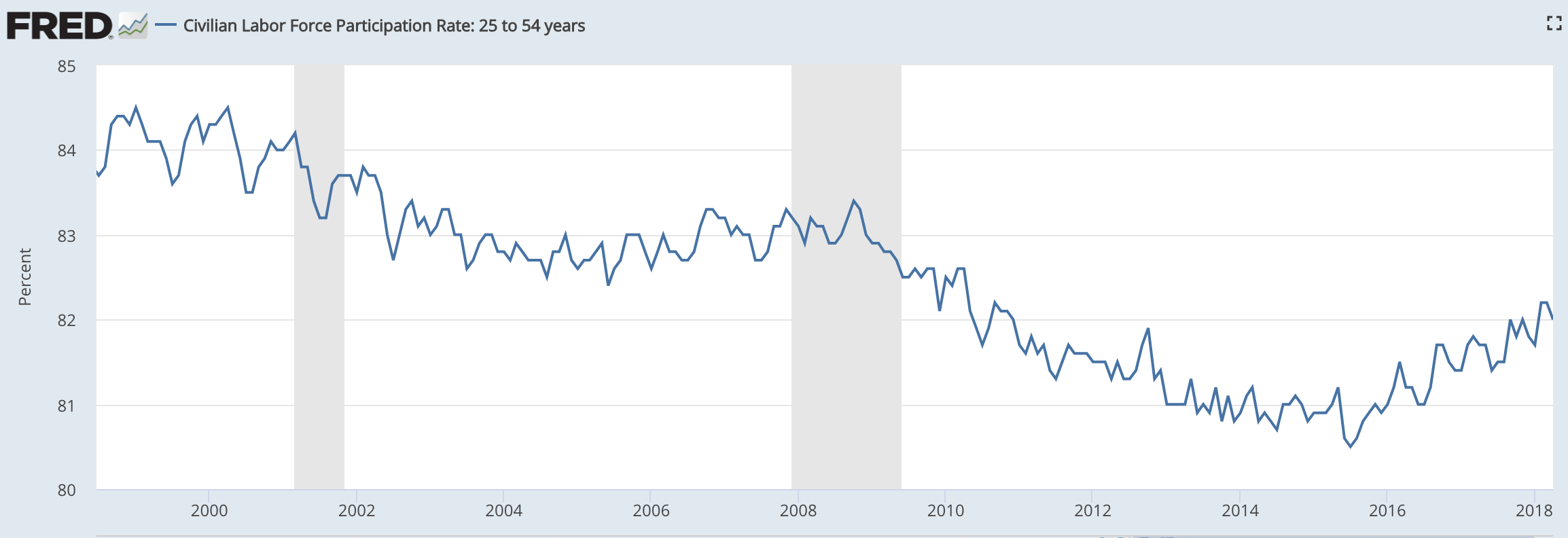

Prime age labor force participation rate still well below pre-crisis levels:

While this could be due to structural forces, the prudent course of action would be to let the labor market run hot and find out whether more people are willing to join the labor force again.

While this could be due to structural forces, the prudent course of action would be to let the labor market run hot and find out whether more people are willing to join the labor force again.

RSS Feed

RSS Feed