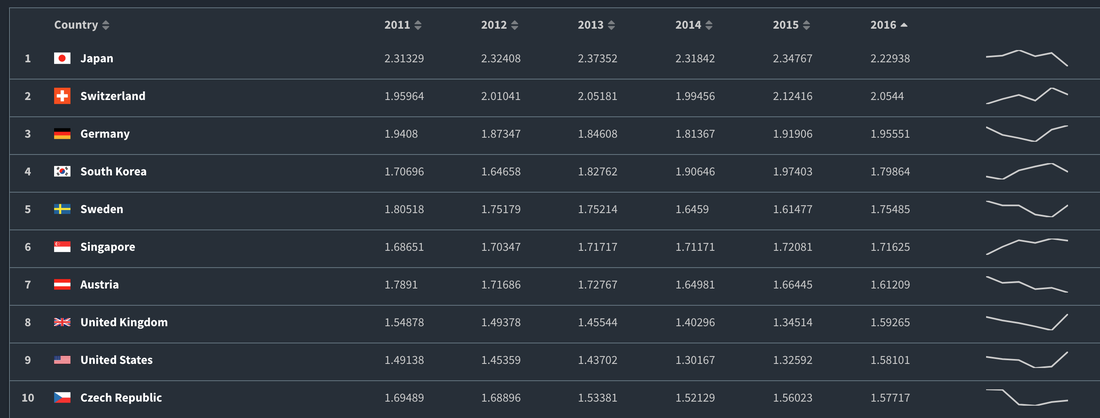

I have recently made a few changes to my blog. I have included here a bunch of economic models and economics data bases that I follow occasionally. This economic trade complexity database is especially interesting. It displays world wide trade flows for countries and breaks down a country’s export by goods and sector. It then creates a ranking for each country to determine a country’s trade complexity, meaning how technologically advanced and diversified a country’s export is. Primary products, commodities and raw materials, are obviously the most basic goods a country can export. The most technologically advanced goods are machines, computers, phones, car parts, etc. The website has produced a ranking for all countries of a certain size, ranking a country’s trade exports by complexity. It should not be a surprise that this measure is also highly correlated with GDP per capita. The richest countries are also the most technologically advanced, thus procuring and exporting the most complex products. In the table below you can find the top 10 countries and here the link for a more complete list. While there are no big surprises, Switzerland, Germany, and the US are all in the top 10, the list also has some notable outliers.

The Czech Republic can be found as number 10 in the list of the most complex exporting countries in the world. This might be somewhat surprising at first. After all, belonging to the Eastern European countries, Czech Republic’s income level is still only at about 70% of the GDP of Western Europe (in PPP terms, meaning adjusted for differences in price levels). However, the country has been catching up quite rapidly in fence decades as it became one of the Eastern European countries that joined the European Union in 2005, this benefiting quite substantially from access to the common market as well as the transfer payments one can enjoy as being a poorer member of the club. It should be noted though that the Czech Republic was initially one of the richer countries in Eastern Europe and has achieved a remarkable amount of convergence to Western Europe.

The fact that the Czech Central Bank has performed really well in the aftermath of the crisis has helped as well as the country was not constrained by the straight jacket of the Euro, a topic I might elaborate on in a future blog post because it is quite interesting how the country escaped the so-called liquidity trap.

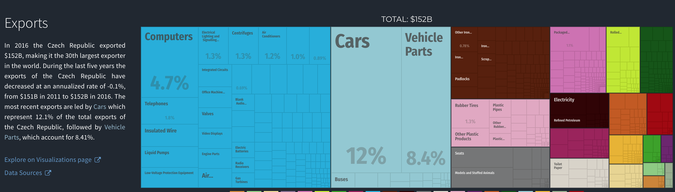

The graph below depicts the goods that Czech Republic is exporting to the rest of the world and you can find many high-tech products among them, especially cars and car parts as the country has become a major automobile producer.

The fact that the Czech Central Bank has performed really well in the aftermath of the crisis has helped as well as the country was not constrained by the straight jacket of the Euro, a topic I might elaborate on in a future blog post because it is quite interesting how the country escaped the so-called liquidity trap.

The graph below depicts the goods that Czech Republic is exporting to the rest of the world and you can find many high-tech products among them, especially cars and car parts as the country has become a major automobile producer.

Just like Slovakia, the Czech Republic has become a major car exporter as many German carmakers have set up their factories in the country, given its favorable geographic location close to Western European markets combined with what was back then still extremely low wages.

While the communist epoch has obviously hindered the country’s economic development for decades, it should ultimately be not that surprising that the Czech Republic has the potential to catch given its economic history.

In fact, during the Austrian-Hungarian empire, Bohemia was one of the most economically developed and industrialized regions of the empire. Given the very clear correlation between the level of trade complexity and GDP per capita, one should expect the Czech Republic to perform well in the future and continue its path of convergence with Western Europe. Note that the country has already caught up with some of Southern European states like Greece and Portugal and of its current trajectory might achieve Western European levels within the next three to four decades or so.

Economic convergence is unfortunately a slow process. The Solow model predicts a speed of convergence of 4%, which empirically has been found to be too high. Even at that rate, the Czech Republic would close half of the gap only every 18 years, thus moving from 70% to 85% of Western European income levels in about two decades.

Note, by the way, that Slovenia and Slovakia are two other Eastern European countries that rank very highly in terms of trade complexity (rank 12 and 16, respectively). Those two countries have also grown very rapidly in comparison to Western Europe in recent years and convergence is very likely to continue.

While the communist epoch has obviously hindered the country’s economic development for decades, it should ultimately be not that surprising that the Czech Republic has the potential to catch given its economic history.

In fact, during the Austrian-Hungarian empire, Bohemia was one of the most economically developed and industrialized regions of the empire. Given the very clear correlation between the level of trade complexity and GDP per capita, one should expect the Czech Republic to perform well in the future and continue its path of convergence with Western Europe. Note that the country has already caught up with some of Southern European states like Greece and Portugal and of its current trajectory might achieve Western European levels within the next three to four decades or so.

Economic convergence is unfortunately a slow process. The Solow model predicts a speed of convergence of 4%, which empirically has been found to be too high. Even at that rate, the Czech Republic would close half of the gap only every 18 years, thus moving from 70% to 85% of Western European income levels in about two decades.

Note, by the way, that Slovenia and Slovakia are two other Eastern European countries that rank very highly in terms of trade complexity (rank 12 and 16, respectively). Those two countries have also grown very rapidly in comparison to Western Europe in recent years and convergence is very likely to continue.

The aberration Down Under

The second large outlier in the trade complexity database is Australia. While the country is generally known for being one of the largest commodity exporters in the world, it is also the only advanced economy that hasn’t had a recession in now almost three decades. This track record is particularly impressive given that commodity prices are quite volatile, meaning that the commodity sector is more prone to boom and bust cycles in general.

One of the big benefits of the country has been its large population growth rate in recent decades, mostly a result of immigration. About every fourth inhabitant was initially not born in Australia. The massive economic expansion the country experienced was thus to some extent a result of a population boom, which allowed for much higher trend growth than many of the other advanced economies. As the country went into the global financial crisis with much higher interest rates, the Central Bank of Australia could cut interest rates to a greater extent without ever facing the zero lower bound that constrained many other Central Banks, thus allowing the country to escape the Great Recession. Unfortunately, the populist wave has reached Down Under as well, meaning that this big bonus point might soon go away.

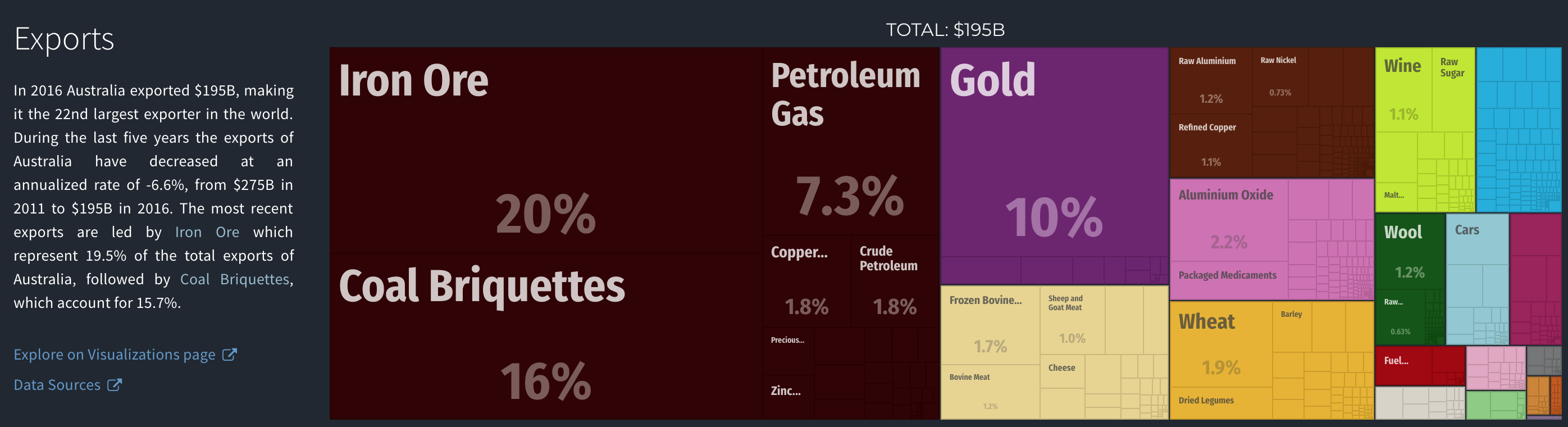

In terms of trade complexity, Australia ranks extremely globally (rank 69) despite being one of the richest countries in the world. The graph below shows that the country is primarily exporting commodities (coal, iron ore, oil, gas, etc.) as well as other primary products (grain, meat). While the global commodity boom of the early 2000s definitely led to an economic boom in Australia, one must keep in mind that in the aftermath of the Great Recession commodity prices plunged for several years. As commodity prices are extremely volatile, the country's track record of almost 3 decades without a recession is all the more impressive. Kudos to the Bank of Australia!

Of course, in recent years the country also experienced an extraordinary housing boom. While some have expected a the burst of the Australian housing bubble for many years, such a prediction never came to fruition. I have written before that I am not a firm believer of the crude bubble theories. Housing prices have appreciated in metropolitan areas around the world across most advanced economies, and it seems to be mostly a story of rising demand facing inelastic supply, at least in the short to medium run (the result of zoning laws, regulations, high constriction costs, etc.).

One big concern, however, is the interaction between rising asset prices and debt. In fact, debt bubbles are much more dangerous. Private sector debt, and especially mortgage debt, has been rising at unprecedented levels: Household debt now exceeds 120% of GDP.

Good macroeconomic policies can make sure that house prices and debt levels do not rise without bounds and the Central Bank of Australia can definitely engineer a soft landing. One concern though is that now even in Australia interest rates barely exceed 1%, thus giving its Central Bank little leeway in the face of an adverse macroeconomic shock.

One of the big benefits of the country has been its large population growth rate in recent decades, mostly a result of immigration. About every fourth inhabitant was initially not born in Australia. The massive economic expansion the country experienced was thus to some extent a result of a population boom, which allowed for much higher trend growth than many of the other advanced economies. As the country went into the global financial crisis with much higher interest rates, the Central Bank of Australia could cut interest rates to a greater extent without ever facing the zero lower bound that constrained many other Central Banks, thus allowing the country to escape the Great Recession. Unfortunately, the populist wave has reached Down Under as well, meaning that this big bonus point might soon go away.

In terms of trade complexity, Australia ranks extremely globally (rank 69) despite being one of the richest countries in the world. The graph below shows that the country is primarily exporting commodities (coal, iron ore, oil, gas, etc.) as well as other primary products (grain, meat). While the global commodity boom of the early 2000s definitely led to an economic boom in Australia, one must keep in mind that in the aftermath of the Great Recession commodity prices plunged for several years. As commodity prices are extremely volatile, the country's track record of almost 3 decades without a recession is all the more impressive. Kudos to the Bank of Australia!

Of course, in recent years the country also experienced an extraordinary housing boom. While some have expected a the burst of the Australian housing bubble for many years, such a prediction never came to fruition. I have written before that I am not a firm believer of the crude bubble theories. Housing prices have appreciated in metropolitan areas around the world across most advanced economies, and it seems to be mostly a story of rising demand facing inelastic supply, at least in the short to medium run (the result of zoning laws, regulations, high constriction costs, etc.).

One big concern, however, is the interaction between rising asset prices and debt. In fact, debt bubbles are much more dangerous. Private sector debt, and especially mortgage debt, has been rising at unprecedented levels: Household debt now exceeds 120% of GDP.

Good macroeconomic policies can make sure that house prices and debt levels do not rise without bounds and the Central Bank of Australia can definitely engineer a soft landing. One concern though is that now even in Australia interest rates barely exceed 1%, thus giving its Central Bank little leeway in the face of an adverse macroeconomic shock.

Some final thoughts on Australia and its missed opportunity

While Australia's track record in recent decades is quite impressive, it feels like the country missed one large opportunity. Given its abundance in resources, Australia could have set up a sovereign wealth fund like Norway to save for a time after the resource boom has ended. While taxes are usually distortionary (because they distort incentives and thus lead to a misallocation of resources), a proportional tax on economic profits from resource extraction is actually efficient. While many developing countries suffer from the resource course, corrupt elites and failed institutions prevent those countries from economic development, there are some notable exceptions. The oil states on the Saudi Arabian Island, the United Arab Emirates, have transformed into the biggest financial center, a popular tourist destination, and a transportation hub in the Middle East.

Norway is known for its Sovereign Wealth fund based on the oil revenues, which has now a value of more than one trillion dollars and holds about 1% of all the stocks in the world.

While the economies of Australia and Canada have certainly benefited from the massive commodity boom in the 2000s, both counties have so far not taken the opportunity to develop their own sovereign wealth fund based on the potential income stream the state could extract from the commodity sector.

While Australia introduced in 2012 the so-called resource super profit tax, the tax was strongly opposed by a lobbying group of Australian and foreign mining companies. The tax was killed just a year later in 2013 by a new government.

An Australian sovereign wealth fund based on the Norwegian model with money coming from the resources Australia wealth is partly based on could ensure the country’s future success for a time when some of those resources will eventually be depleted.

Reference:

AJG Simoes, CA Hidalgo. The Economic Complexity Observatory: An Analytical Tool for Understanding the Dynamics of Economic Development. Workshops at the Twenty-Fifth AAAI Conference on Artificial 2011)

While Australia's track record in recent decades is quite impressive, it feels like the country missed one large opportunity. Given its abundance in resources, Australia could have set up a sovereign wealth fund like Norway to save for a time after the resource boom has ended. While taxes are usually distortionary (because they distort incentives and thus lead to a misallocation of resources), a proportional tax on economic profits from resource extraction is actually efficient. While many developing countries suffer from the resource course, corrupt elites and failed institutions prevent those countries from economic development, there are some notable exceptions. The oil states on the Saudi Arabian Island, the United Arab Emirates, have transformed into the biggest financial center, a popular tourist destination, and a transportation hub in the Middle East.

Norway is known for its Sovereign Wealth fund based on the oil revenues, which has now a value of more than one trillion dollars and holds about 1% of all the stocks in the world.

While the economies of Australia and Canada have certainly benefited from the massive commodity boom in the 2000s, both counties have so far not taken the opportunity to develop their own sovereign wealth fund based on the potential income stream the state could extract from the commodity sector.

While Australia introduced in 2012 the so-called resource super profit tax, the tax was strongly opposed by a lobbying group of Australian and foreign mining companies. The tax was killed just a year later in 2013 by a new government.

An Australian sovereign wealth fund based on the Norwegian model with money coming from the resources Australia wealth is partly based on could ensure the country’s future success for a time when some of those resources will eventually be depleted.

Reference:

AJG Simoes, CA Hidalgo. The Economic Complexity Observatory: An Analytical Tool for Understanding the Dynamics of Economic Development. Workshops at the Twenty-Fifth AAAI Conference on Artificial 2011)

RSS Feed

RSS Feed