U.S. GDP growth has accelerated last year amidst a global economic recovery that is also taken place in Europe and in emerging market. Consequently, global economic growth has been reaching 4% again for the first time ever since the financial crisis. U.S. GDP growth figures for the 4th quarter of 2017 will be released by the BEA tomorrow. I have written before how several branches of the U.S. Federal Reserve, most notable the Atlanta Fed and the New York Fed, are now using so-called Nowcast model to estimate actual GDP growth figures with current economic data as the quarter goes along. The Atlanta Fed is predicting growth of 3.4% for Q4 2017 while the New York Fed is predicting even stronger growth of about 3.94%.

Based on previous forecasts, I did a quick and dirty regression and estimated that the "best forecast" is a weighted average of the two models with weights of 66% and 25%, respectively. This would lead to the following estimate:

0.78 * 3.4% + 0.2 * 3.94% = 3.45%

So my regression predicts a slightly higher growth rate than the Atlanta model, which has proven to be a relatively accurate forecast methodology for quarterly GDP figures, which are historically quite volatile. U.S. GDP growth has been extremely robust so far last year with the following quarterly growth rates:

Q1: 1.2%

Q2: 3.1%

Q3: 3.2%

Q4: 3.5% ?

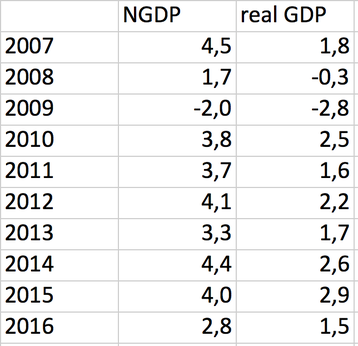

Note that this would lead to an annual real growth rate of about 2.8%. This would be the second strongest years since the financial crisis:

Based on previous forecasts, I did a quick and dirty regression and estimated that the "best forecast" is a weighted average of the two models with weights of 66% and 25%, respectively. This would lead to the following estimate:

0.78 * 3.4% + 0.2 * 3.94% = 3.45%

So my regression predicts a slightly higher growth rate than the Atlanta model, which has proven to be a relatively accurate forecast methodology for quarterly GDP figures, which are historically quite volatile. U.S. GDP growth has been extremely robust so far last year with the following quarterly growth rates:

Q1: 1.2%

Q2: 3.1%

Q3: 3.2%

Q4: 3.5% ?

Note that this would lead to an annual real growth rate of about 2.8%. This would be the second strongest years since the financial crisis:

By the way, I am on record saying that the chance of above 2.5% growth for the U.S. for the 2017 is below 5% (with the chance of growth coming in at 2 to 2.5% at about 20%). Not a great prediction! However, I was not alone there as many other institutions, including the IMF and quite a few Central Banks recently had to raise their forecasts for last year as well.

I was counting on growth being roughly similar to the previous years, with average growth rates in the decade after the financial crisis barely reaching 2%. The "secular stagnation outcome" that was revived as an idea by Lawrence Summers a few years ago.

This only shows how macroeconomic forecasts are notoriously difficult. Past performance is does not always seem to be a good predictor of the future.

Here are two factors I have not been counting on. First, there is currently a global economy on its way. Even the severely depressed Eurozone has been experiencing very high growth rates over the last 2 to 3 years. A rising tide lifts all boats!

Second, while the Trump tax cut is mainly a gift to the rich and super rich, it will boost the economy's growth rate in the very short run. However, this will by far not be enough to make the tax cut self-financing as many conservatives have claimed. Self-financing supply side tax cuts are a zombie idea that should have died a long time... But you know how it is with zombies, they'll always come back from the dead.

I was counting on growth being roughly similar to the previous years, with average growth rates in the decade after the financial crisis barely reaching 2%. The "secular stagnation outcome" that was revived as an idea by Lawrence Summers a few years ago.

This only shows how macroeconomic forecasts are notoriously difficult. Past performance is does not always seem to be a good predictor of the future.

Here are two factors I have not been counting on. First, there is currently a global economy on its way. Even the severely depressed Eurozone has been experiencing very high growth rates over the last 2 to 3 years. A rising tide lifts all boats!

Second, while the Trump tax cut is mainly a gift to the rich and super rich, it will boost the economy's growth rate in the very short run. However, this will by far not be enough to make the tax cut self-financing as many conservatives have claimed. Self-financing supply side tax cuts are a zombie idea that should have died a long time... But you know how it is with zombies, they'll always come back from the dead.

RSS Feed

RSS Feed