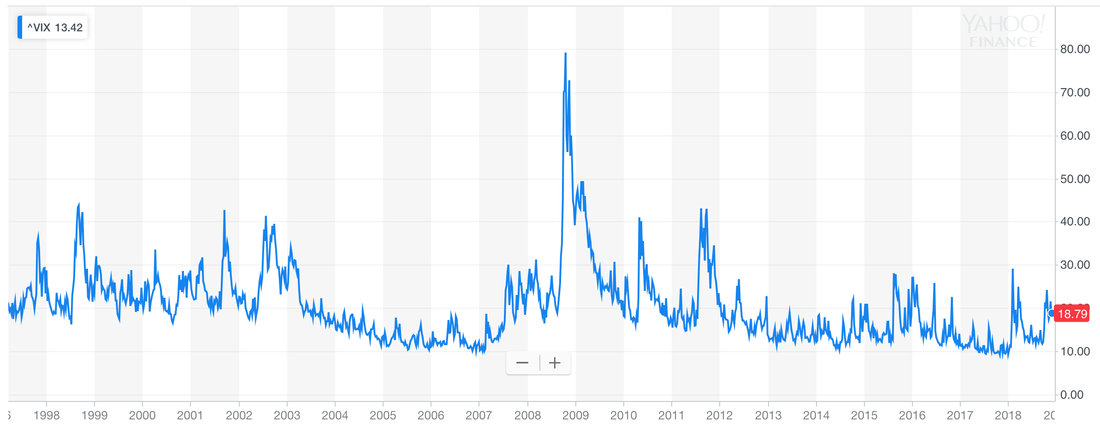

So I was having a look at the VIX recently, which is a measure of volatility of the US stock market (and more specifically the S&P 500). If volatility in the stock market goes up, the VIX increases (see picture below). While the efficient market hypothesis suggest that asset prices are mostly driven by fundamental values, there is a a lot of evidence that asset prices can actually diverge from fundamental values for longer periods of time. This might be especially true for the housing market since it is more difficult to go short housing and bet against price increases. However, as Keynes already noted, the market can stay irrational longer than you can remain solvent. A remark he surely made after loosing quite a bit of money as an investor in financial markets himself. Especially during times of irrational exuberance, it might be very painful to go short the stock market since the time of euphoria might last longer than you can afford to bet against it. In the movie the big short, legendary investor Michael Burry was almost priced out of the market by losing cash flow before his big bet on shorting the housing market eventually market paid off.

While most macro models, including neo-Keynesian macro, assume that the economy is inherently stabilizing, Keynes would probably have dismissed this extremely rigid assumption. He never regarded the economy as returning back to equilibrium after being hit by negative shocks.

Economists like Kindleberger and Minsky have also written extensively about financial panics and crashes as well as about financial instability. According to the financial instability hypothesis suggested by Minsky, financial risks build up endogenously within the system over time. We have a lot of evidence that after large macroeconomic shocks like the Great Depression that affect an entire generation, people change their behavior for many years. They become more risk-averse, stock market participation decreases for many years. Similarly, after long periods of financial stability, individuals, firms, and market participants assume more and more risky positions. Gambling starts to pay off, leverage increases, and ultimately so does fraud. As financial leverage and exposure to risky positions increases, the system becomes more fragile. Then it is ultimately only a matter of time when a shock hits the system, culminating in a large macroeconomic event as the entire house of cards built on leverage and debt crumbles.

It is maybe not a coincidence that the financial crisis of 2008 and the Great Recession that followed was proceeded by the Great Moderation, a time period from the late 1980s spanning to the mid-2000s characterized by relatively high macroeconomic stability, at least across advanced economies. It is still a matter of debate whether the Great Moderation was the result of luck or policy makers like Central Bankers becoming better at their jobs. Regardless, while macroeconomic management was reasonably well, financial risks were starting to build up within the system that went undetected for a long time. It was also mistakenly believed that financial globalization would actually work in favor of stabilizing the system and diversifying risks, an assumption that turned out to be dangerously wrong. Some recent research based on the Macrohistory data suggests that financial globalization has actually increased the correlation between national asset prices and national business cycles across countries. The benefits of global diversification might thus quickly evaporate as financial linkages and global capital flows imply that asset prices across the globe move in the same direction, regardless of fundamentals.

It is thus interesting to see that the VIX was extremely low during the early 2000s, before exploding in 2008 as financial markets froze up during the financial crisis. Similarly, the VIX has been trading at very low levels over the last few years while as of this year it has edged upward quite a bit as a result of much higher volatility in the stock market, surely a result of the escalating trade war by Trump and the Fed tightening monetary policy for the US (and the rest of the globe).

While there have been some attempts to model endogenous financial crisis, I am not aware of any of the research achieving major breakthroughs, to be honest (but happy if proven wrong). The problem is that these kind of endogenous forces are very hard to model. It is easy to understand how after a long period of calm and stability market participants start to forget about the risk, increasingly engage in risky and fraudulent behavior, and also increase their leverage and exposure to bad market events. However, to show that agents systematically behave in a certain way is an entire different thing altogether. There are very few of any good predictors of economic and financial crisis. While policy makers often screw up in one way or the other, again how and why they do so cannot be modelled in any systematic way, thus also making any major economic shock unpredictable. Some recent research has shown that most financial crisis are preceded by asset price bubbles and result from the dangerous interaction between asset price deflation and exposure to debt. However, again these two variables alone cannot help us to predict the exact timing of a bursting bubble, and as a market participant or monetary picky maker, timing is everything.

So where does this leave us ?

Well, I’m afraid that all of this basically means the following. Policy makers and market participants cannot predict bursting bubbles, financial crisis or even economic recessions. The only thing we can do is to make the system more robust so that it can withstand even major economic shocks. Unfortunately, also on this front little progress has been made. Lobbying and other political obstacles mean that higher capital requirements for financial institutions have not been imposed to the extent that it would be necessary to prevent the next financial crisis.

In terms of the VIX, we have sent that a couple of years of really low volatility have now been followed by one year of increased uncertainty, heightened volatility, and the occasion market crash followed by a rebounce. Really hard to say what all of this implies for the future. Since asset prices are mostly unpredictable and economists cannot forecast recessions with any reasonable degree of accuracy, I won’t make any futile attempt to forecast the unknown.

PS: I wrote all of this before yesterday’s market crash. It should be noted that one part of the yield curve inverted today, which has historically been one of the only predictors of a future recession. The risks of a downturn just increased dramatically with the spectacular crash hat happens at the long end of the yield curve. If the Fed continues to tighten aggressively, we can expect a recession in about 12 to 18 months from now.

References:

While most macro models, including neo-Keynesian macro, assume that the economy is inherently stabilizing, Keynes would probably have dismissed this extremely rigid assumption. He never regarded the economy as returning back to equilibrium after being hit by negative shocks.

Economists like Kindleberger and Minsky have also written extensively about financial panics and crashes as well as about financial instability. According to the financial instability hypothesis suggested by Minsky, financial risks build up endogenously within the system over time. We have a lot of evidence that after large macroeconomic shocks like the Great Depression that affect an entire generation, people change their behavior for many years. They become more risk-averse, stock market participation decreases for many years. Similarly, after long periods of financial stability, individuals, firms, and market participants assume more and more risky positions. Gambling starts to pay off, leverage increases, and ultimately so does fraud. As financial leverage and exposure to risky positions increases, the system becomes more fragile. Then it is ultimately only a matter of time when a shock hits the system, culminating in a large macroeconomic event as the entire house of cards built on leverage and debt crumbles.

It is maybe not a coincidence that the financial crisis of 2008 and the Great Recession that followed was proceeded by the Great Moderation, a time period from the late 1980s spanning to the mid-2000s characterized by relatively high macroeconomic stability, at least across advanced economies. It is still a matter of debate whether the Great Moderation was the result of luck or policy makers like Central Bankers becoming better at their jobs. Regardless, while macroeconomic management was reasonably well, financial risks were starting to build up within the system that went undetected for a long time. It was also mistakenly believed that financial globalization would actually work in favor of stabilizing the system and diversifying risks, an assumption that turned out to be dangerously wrong. Some recent research based on the Macrohistory data suggests that financial globalization has actually increased the correlation between national asset prices and national business cycles across countries. The benefits of global diversification might thus quickly evaporate as financial linkages and global capital flows imply that asset prices across the globe move in the same direction, regardless of fundamentals.

It is thus interesting to see that the VIX was extremely low during the early 2000s, before exploding in 2008 as financial markets froze up during the financial crisis. Similarly, the VIX has been trading at very low levels over the last few years while as of this year it has edged upward quite a bit as a result of much higher volatility in the stock market, surely a result of the escalating trade war by Trump and the Fed tightening monetary policy for the US (and the rest of the globe).

While there have been some attempts to model endogenous financial crisis, I am not aware of any of the research achieving major breakthroughs, to be honest (but happy if proven wrong). The problem is that these kind of endogenous forces are very hard to model. It is easy to understand how after a long period of calm and stability market participants start to forget about the risk, increasingly engage in risky and fraudulent behavior, and also increase their leverage and exposure to bad market events. However, to show that agents systematically behave in a certain way is an entire different thing altogether. There are very few of any good predictors of economic and financial crisis. While policy makers often screw up in one way or the other, again how and why they do so cannot be modelled in any systematic way, thus also making any major economic shock unpredictable. Some recent research has shown that most financial crisis are preceded by asset price bubbles and result from the dangerous interaction between asset price deflation and exposure to debt. However, again these two variables alone cannot help us to predict the exact timing of a bursting bubble, and as a market participant or monetary picky maker, timing is everything.

So where does this leave us ?

Well, I’m afraid that all of this basically means the following. Policy makers and market participants cannot predict bursting bubbles, financial crisis or even economic recessions. The only thing we can do is to make the system more robust so that it can withstand even major economic shocks. Unfortunately, also on this front little progress has been made. Lobbying and other political obstacles mean that higher capital requirements for financial institutions have not been imposed to the extent that it would be necessary to prevent the next financial crisis.

In terms of the VIX, we have sent that a couple of years of really low volatility have now been followed by one year of increased uncertainty, heightened volatility, and the occasion market crash followed by a rebounce. Really hard to say what all of this implies for the future. Since asset prices are mostly unpredictable and economists cannot forecast recessions with any reasonable degree of accuracy, I won’t make any futile attempt to forecast the unknown.

PS: I wrote all of this before yesterday’s market crash. It should be noted that one part of the yield curve inverted today, which has historically been one of the only predictors of a future recession. The risks of a downturn just increased dramatically with the spectacular crash hat happens at the long end of the yield curve. If the Fed continues to tighten aggressively, we can expect a recession in about 12 to 18 months from now.

References:

- “Òscar Jordà, Moritz Schularick, and Alan M. Taylor. 2017. “Macrofinancial History and the New Business Cycle Facts.” in NBER Macroeconomics Annual 2016, volume 31, edited by Martin Eichenbaum and Jonathan A. Parker. Chicago: University of Chicago Press."

- Keynes, John Maynard. The general theory of employment, interest, and money. Springer, 2018.

- Kindleberger, Charles P. "Manis, 1978. Panics and Crashes: A History of Financial Crisis."

- Minsky, Hyman P. "The financial instability hypothesis." (1992).

- Shiller, Robert C. "Irrational exuberance." Philosophy & Public Policy Quarterly 20, no. 1 (2000): 18-23.

THE VIX

RSS Feed

RSS Feed