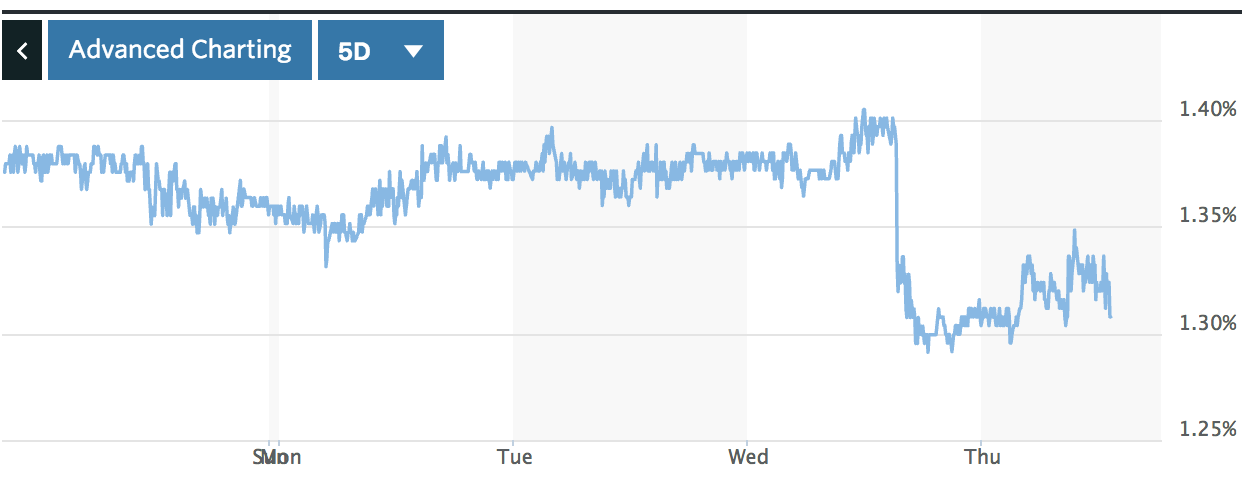

So Goldman's chief economist Jan Hatzius has a similar take on the recent Fed hike than I do. Financial conditions eased across the board with interest rates actually falling across the entire yield curve, the dollar depreciating by more than 0.5%, and stocks are being up as well. Ironically, the reaction to the Fed's rate hike was according to economists at Goldman Sachs equivalent to about a 25 basis point cut in interest rates. Yes, that's right!

Hatzius points out that this was done unintentionally. The Fed eased financial conditions by mere accident. Financial markets at this point in time seem to discount the idea that the Fed might tighten monetary policy at a rapid pace.

Ironically, the easing of financial conditions might actually increase the likelihood of future rate hikes this year. According to Fed officials, the U.S. economy is already close to full employment. This means that they will feel somewhat uncomfortable with what happened in financial markets last week.

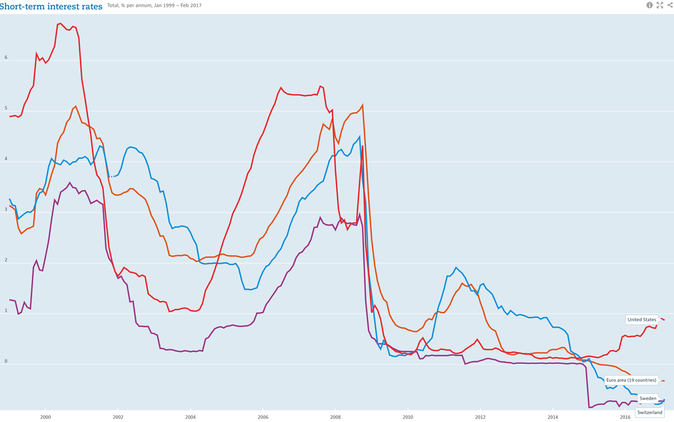

While market participants currently price in only another two rate hikes this year, there is a good chance that the Fed will go for three instead or more, depending on whether economic conditions will warrant further tightening. This means that the short-run interest rate in the U.S. will be very close to 2% by the end of this year. This is in stark contrast with the situation in the Eurozone, Denmark, Sweden, Switzerland and Japan where the Central Banks have implemented a negative interest rate that applies to bank reserves.

As I have argued before, the main monetary event of this year is the monetary decoupling between the U.S. economy and other advanced economies, which remain stuck in a low-interest rate trap. Furthermore, financial markets might actually find that they have not adequately priced in to what extent Fed officials will step up the pace of monetary tightening.

Hatzius points out that this was done unintentionally. The Fed eased financial conditions by mere accident. Financial markets at this point in time seem to discount the idea that the Fed might tighten monetary policy at a rapid pace.

Ironically, the easing of financial conditions might actually increase the likelihood of future rate hikes this year. According to Fed officials, the U.S. economy is already close to full employment. This means that they will feel somewhat uncomfortable with what happened in financial markets last week.

While market participants currently price in only another two rate hikes this year, there is a good chance that the Fed will go for three instead or more, depending on whether economic conditions will warrant further tightening. This means that the short-run interest rate in the U.S. will be very close to 2% by the end of this year. This is in stark contrast with the situation in the Eurozone, Denmark, Sweden, Switzerland and Japan where the Central Banks have implemented a negative interest rate that applies to bank reserves.

As I have argued before, the main monetary event of this year is the monetary decoupling between the U.S. economy and other advanced economies, which remain stuck in a low-interest rate trap. Furthermore, financial markets might actually find that they have not adequately priced in to what extent Fed officials will step up the pace of monetary tightening.

RSS Feed

RSS Feed