So a couple of months ago Boston Fed president Eric Rosengreen confidently declared that the Fed should hike the interest rate 4 times this year. Again, we will surely find out that this was way too optimistic. As Brad DeLong points out, back in December 2015 when the Fed started its tightening cycle and finally escaped the zero-lower bound, the median expectation was that they would hike about 9 times in the subsequent 2.5 years to end up in mid-2017 with an interest rate of slightly above 2%. Reality, however, played out differently. Instead of undertaking nine 25 basis points hikes, economic conditions saw to it that they only undertook 3 interest rate hikes.

The current Federal funds rate is now at just slightly under 1%. Of course, there are some people who always want higher rates, no matter what. They confidently declare that the U.S. economy is now aproaching full employment and that inflationary pressures will soon start to build up.

Except for the fact that:

1) Prime age labor force participation rate is still about 2 percentage points below pre-crisis levels (chart 1).

2) First quarter GDP growth was far from spectacular. Even though in all fairness it must be said that Q1 GDP growth has been horrible for years and that there is usually a rebounce in Q2.

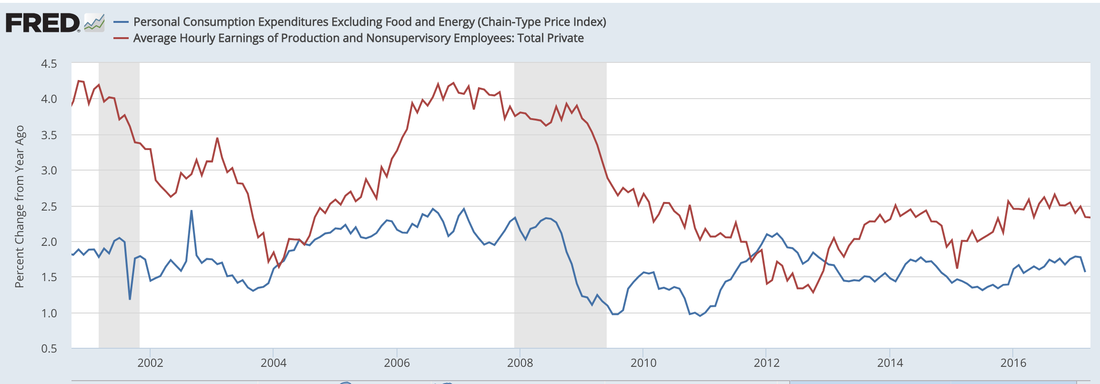

3) Nominal wage growth is still below pre-crisis levels.

4) The Fed undershot its 2% inflation target for many consecutive years, basically since the financial crisis with the exception of 2012.

5) Financial markets expect that the Fed will continue to undershoot its inflation target in the years to come. Tips spreads currently suggest that the CPI will only average about 1.8% over the next decade (chart 3). However, the Fed actually targets a different measure of inflation, PCE (Personal Consumption Expenditure), which usually tends to be 20-30 basis points lower, meaning that the deviation from target in terms of undershooting might end up being even larger.

6) The so-called Trump reflation trade has already come to an early end. Long-term bond yields have fallen again, which probably implies that financial markets expect lower real growth and/or lower inflation rates for the foreseeable future than just a few months ago.

The current Federal funds rate is now at just slightly under 1%. Of course, there are some people who always want higher rates, no matter what. They confidently declare that the U.S. economy is now aproaching full employment and that inflationary pressures will soon start to build up.

Except for the fact that:

1) Prime age labor force participation rate is still about 2 percentage points below pre-crisis levels (chart 1).

2) First quarter GDP growth was far from spectacular. Even though in all fairness it must be said that Q1 GDP growth has been horrible for years and that there is usually a rebounce in Q2.

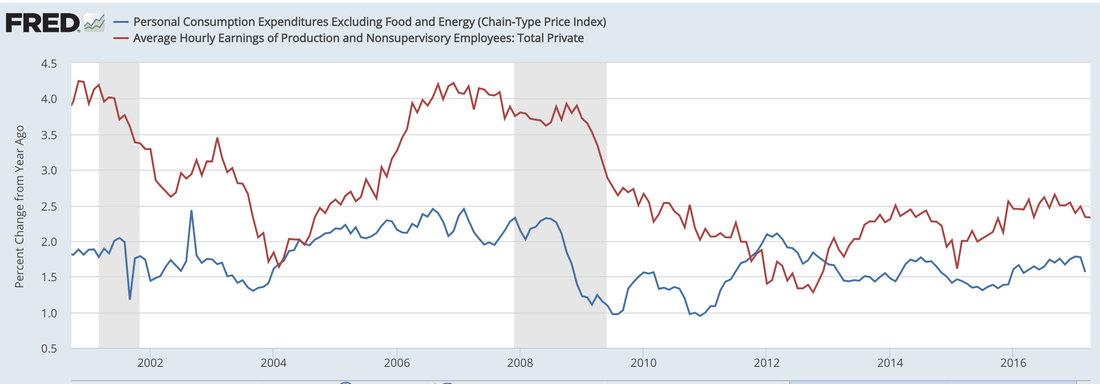

3) Nominal wage growth is still below pre-crisis levels.

4) The Fed undershot its 2% inflation target for many consecutive years, basically since the financial crisis with the exception of 2012.

5) Financial markets expect that the Fed will continue to undershoot its inflation target in the years to come. Tips spreads currently suggest that the CPI will only average about 1.8% over the next decade (chart 3). However, the Fed actually targets a different measure of inflation, PCE (Personal Consumption Expenditure), which usually tends to be 20-30 basis points lower, meaning that the deviation from target in terms of undershooting might end up being even larger.

6) The so-called Trump reflation trade has already come to an early end. Long-term bond yields have fallen again, which probably implies that financial markets expect lower real growth and/or lower inflation rates for the foreseeable future than just a few months ago.

It is beyond me that officials at the Federal Reserve have not accepted yet the reality of secular stagnation. Every year since the beginning of the crisis they have overestimated the strength of the recovery in terms of growth rates, inflation rates, and the path of interest rates. We live in a world where global real interest rates have fallen to unprecedented low levels and are expected to remain extremely low for the foreseeable future. In this world Central Banks have been facing the opposite credibility problem they were used to in the 1970s, namely the inability to push up inflation back to target. As Bernanke explains, this has been to some extent a problem of self-induced paralysis. Central Banks in advanced economies should have and could have resorted to much more expansionary policies in the face of the biggest economic downturn since the Great Depression of the 1930s. The 2% inflation target has turned out to be the biggest constraint, especially since some Central Banks treat it as more as a ceiling than a symmetric target. It is incredible that almost 10 years after the crisis there still is a case to be amde that some of North Atlantic economies are still suffering from a shortage of aggregate demand/low expected nominal GDP growth. In a world where the natural interest rate has decreased to very low levels the risk of hitting the zero-lower bound is much higher than previously estimated. DeLong and Summers already noted back in the 1990s that the 2% inflation target might be too low and history proved them right. There is now overwhelming evidence that Central Banks would be better off with a price level target, or even better, a nominal GDP level target. But none of the Central Banks have even considered a regime change. For them it's just business as usual despite the fact that Central Bank performance has been extraordinarily poor since the financial crisis. This is institutional failure par excellence. Unless Fed official accept the new economic reality of secular stagnation, they will find themselves surprised over and over again that economic conditions and financial markets will not warrant further tightening. I also do not understand the Fed's obsession with shrinking its balance sheet. The risks associated with a large balance sheet seem to be quite manageable. Unwinding the balance sheet just seems like a really bad idea insofar as it would imply a further tightening of monetary conditions. In the beginning of the year I thought that the Fed might be able to hike four times. given how the first half of the year has played out, I will revise my opinion now. They managed to pull off one hike in March. As the Trump reflation trade has come to an early end, however, they might be able to pull of another two hikes at best, but even this seems to be a little of a stretch to me. I'm happy to be proved wrong , but I really can't see how they can start unwinding their balance on top of a couple of rate hikes sheet this year without causing some turmoil in the markets and/or causing a growth slowdown. The overoptimism at the Fed is quite concerning and leaves me troubled, I must say. Also the unwillingness to let the labor market run hot for a little while after years of disappointing wage growth is staggering. So it looks like the job destroyers at the Fed will strike another two times this year because they are desperate to "normalize" rates, whatever that means.

RSS Feed

RSS Feed