China’s economic growth over the last couple of decades was based on what I would label as an export-led growth model. The Chinese currency has been pegged to the dollar at an artificially low level for a long period of time. The People’s Bank of China (PBoC) had to intervene continuously in the foreign exchange market to prevent the Yuan from appreciating. As a result of such interventions, Chinese goods were more competitive on global markets and this allowed the country to industrialize on a large scale. I would argue that this process of industrialization combined with rapid urbanization has been the main engine of the Chinese growth miracle, which lifted millions of people out of poverty over the last couple of decades.

Government officials in Western countries, of course, have cried foul for many years because they regarded said Chinese currency manipulation as unfair. It is true that the rapid industrialization process in Southeast Asia, and China in particular, has been accompanied by a decline in manufacturing in many advanced economies and that it is quite safe to assume that there is a causal link between those two (There are other maybe more important factors, such as rapid automation, that have led to a decline in manufacturing jobs in advanced economies, but industrialization in Southeast Asia probably played a part in it). On the other hand, we should always be aware of the fact that there are a very little free lunches in economics, and so it is also in this case.

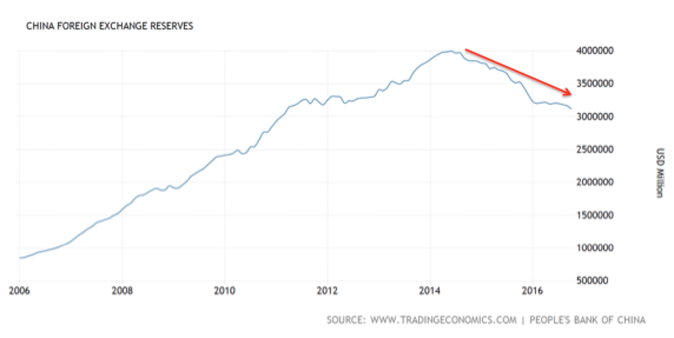

The flip side of China’s attempt to manipulate the currency has been, of course, that the country accumulated a massive amount of foreign reserves (Chinese authorities depressed the value of the Yuan by buying foreign currencies with domestic currency in the foreign exchange market). As a result, the PBoC was holding foreign currency reserves in the amount of about 4 trillion US dollars by 2014 (see graph). Expert opinion is that maybe 3 trillion dollars of these reserves were in U.S. dollars, the rest being a wide range of other key currencies, such as the Euro, the Yen, the British pound, and the Swiss Franc.

Now it is not entirely clear that this former arrangement was a bad deal for the U.S. once you think more carefully about it. After all, the U.S. was issuing money and debt in U.S. dollars and used it to buy industrial goods from China. But China didn’t use the proceeds to buy American goods and services. Instead, it decided to hold on to those U.S. liabilities. Now imagine the scenario that China will hold on to said currency reserves forever. This basically means that U.S. citizens were able to buy goods and services in the amount of 3 trillion dollars more than in a world where China would not have decided to hoard massive amounts of foreign reserves. In other words, the U.S. consumes more than it produces simply because foreigners display an extreme tendency to hold on to small green papers with faces of dead presidents. This is not a bad deal! Of course, it is possible that one day China will redeem the U.S. liabilities and acquire U.S. goods and services. However, average U.S. inflation rates are about 2% on a yearly basis. So redeeming 1 trillion of reserves in let’s say 5 years of now will buy you less stuff in real terms. (I have abstracted from the fact that Chinese reserves are mostly U.S. bonds instead of actual currency, which means that China earns interest rate payments each year. However, this does not change the fact that issuing pieces of paper to buy goods is a good deal for the time being).

But now to the punch line. While it is true that Chinese authorities have artificially depressed their currency for many years in the way I have described above, one cannot say that this is still the case right now, far from it actually. As the graph below shows, the PBoC has lost about 1 trillion in reserves since the beginning of 2014. Chinese economic growth rates in the excess of 10% were due to unsustainable investment rates in the long-run and a slowdown had to occur eventually, especially since the possibilities of catch-up growth are exhausted as the economy grows richer. The Chinese authorities currently try to shift the country from an investment-led to a more consumption-driven model. As the Chinese economy has been slowing down over the last couple of years, there has been some significant downward pressure on its currency. Over the last two years Chinese officials have used abut 1 trillion in foreign exchange reserves to prop up the Chinese Yuan. Trump’s remarks are thus totally out of place in the current context. To the contrary, he should be highly supportive of the current policy. If China were to abandon its dollar peg, the Yuan would depreciate by quite a bit since it is undervalued at the moment, which would make Chinese goods even more competitive. As a consequence, the U.S. trade deficit would increase even further and even more of those manufacturing jobs Trump swore to protect would be displaced.

I actually expect that this might happen to some extent regardless. Trump’s current economic policy proposals are a massive stimulus plan on infrastructure in the amount of 1 trillion dollars combined with a massive tax cut on corporations and the rich. This will blow a huge hole into the U.S. budget deficit and it will also exacerbate inequality even further. The package will turn out to be mildly stimulatory to the U.S. economy. However, monetary policy trumps fiscal policy (sorry, Trump). In the face of an economy operating at full capacity, the Fed will raise interest rates to prevent overheating and accelerating inflation (the first rate hike is expected to come this December). Many advanced economies, however, are still stuck at zero interest rates whereas the U.S. economy is decoupling. Higher yields in the U.S. will put upward pressure on the dollar as money will chase for higher returns. My best guess is that Trump’s economic economic policies, if implemented, lead to a further appreciation of the dollar. A dollar-euro parity could not be out of sight in the near future. It is, of course, mostly U.S. manufacturing that will suffer from a strengthening currency (employment will shift into services and construction instead), meaning that Trump’s policies will damage the same exact sector he is so eager to protect.

Update:

One should note that the Chinese peg to the dollar is more of a “soft peg”. I wrote this yesterday. Today Bloomberg reports that the Yuan has reached its lowest level since December 2008 despite the fact that Chinese authorities have recently taken measures to prop up the currency. Trump’s policy anouncements reduce the allure of emerging markets, thus putting downward pressure on their currrencies, including the Chinese Yuan, which is ironically exactly the opposite Trump is trying to achieve since a strong dollar will weigh on American manufacturing.

http://www.bloomberg.com/news/articles/2016-11-16/china-s-yuan-tumbles-to-eight-year-low-as-banks-weaken-forecasts

Government officials in Western countries, of course, have cried foul for many years because they regarded said Chinese currency manipulation as unfair. It is true that the rapid industrialization process in Southeast Asia, and China in particular, has been accompanied by a decline in manufacturing in many advanced economies and that it is quite safe to assume that there is a causal link between those two (There are other maybe more important factors, such as rapid automation, that have led to a decline in manufacturing jobs in advanced economies, but industrialization in Southeast Asia probably played a part in it). On the other hand, we should always be aware of the fact that there are a very little free lunches in economics, and so it is also in this case.

The flip side of China’s attempt to manipulate the currency has been, of course, that the country accumulated a massive amount of foreign reserves (Chinese authorities depressed the value of the Yuan by buying foreign currencies with domestic currency in the foreign exchange market). As a result, the PBoC was holding foreign currency reserves in the amount of about 4 trillion US dollars by 2014 (see graph). Expert opinion is that maybe 3 trillion dollars of these reserves were in U.S. dollars, the rest being a wide range of other key currencies, such as the Euro, the Yen, the British pound, and the Swiss Franc.

Now it is not entirely clear that this former arrangement was a bad deal for the U.S. once you think more carefully about it. After all, the U.S. was issuing money and debt in U.S. dollars and used it to buy industrial goods from China. But China didn’t use the proceeds to buy American goods and services. Instead, it decided to hold on to those U.S. liabilities. Now imagine the scenario that China will hold on to said currency reserves forever. This basically means that U.S. citizens were able to buy goods and services in the amount of 3 trillion dollars more than in a world where China would not have decided to hoard massive amounts of foreign reserves. In other words, the U.S. consumes more than it produces simply because foreigners display an extreme tendency to hold on to small green papers with faces of dead presidents. This is not a bad deal! Of course, it is possible that one day China will redeem the U.S. liabilities and acquire U.S. goods and services. However, average U.S. inflation rates are about 2% on a yearly basis. So redeeming 1 trillion of reserves in let’s say 5 years of now will buy you less stuff in real terms. (I have abstracted from the fact that Chinese reserves are mostly U.S. bonds instead of actual currency, which means that China earns interest rate payments each year. However, this does not change the fact that issuing pieces of paper to buy goods is a good deal for the time being).

But now to the punch line. While it is true that Chinese authorities have artificially depressed their currency for many years in the way I have described above, one cannot say that this is still the case right now, far from it actually. As the graph below shows, the PBoC has lost about 1 trillion in reserves since the beginning of 2014. Chinese economic growth rates in the excess of 10% were due to unsustainable investment rates in the long-run and a slowdown had to occur eventually, especially since the possibilities of catch-up growth are exhausted as the economy grows richer. The Chinese authorities currently try to shift the country from an investment-led to a more consumption-driven model. As the Chinese economy has been slowing down over the last couple of years, there has been some significant downward pressure on its currency. Over the last two years Chinese officials have used abut 1 trillion in foreign exchange reserves to prop up the Chinese Yuan. Trump’s remarks are thus totally out of place in the current context. To the contrary, he should be highly supportive of the current policy. If China were to abandon its dollar peg, the Yuan would depreciate by quite a bit since it is undervalued at the moment, which would make Chinese goods even more competitive. As a consequence, the U.S. trade deficit would increase even further and even more of those manufacturing jobs Trump swore to protect would be displaced.

I actually expect that this might happen to some extent regardless. Trump’s current economic policy proposals are a massive stimulus plan on infrastructure in the amount of 1 trillion dollars combined with a massive tax cut on corporations and the rich. This will blow a huge hole into the U.S. budget deficit and it will also exacerbate inequality even further. The package will turn out to be mildly stimulatory to the U.S. economy. However, monetary policy trumps fiscal policy (sorry, Trump). In the face of an economy operating at full capacity, the Fed will raise interest rates to prevent overheating and accelerating inflation (the first rate hike is expected to come this December). Many advanced economies, however, are still stuck at zero interest rates whereas the U.S. economy is decoupling. Higher yields in the U.S. will put upward pressure on the dollar as money will chase for higher returns. My best guess is that Trump’s economic economic policies, if implemented, lead to a further appreciation of the dollar. A dollar-euro parity could not be out of sight in the near future. It is, of course, mostly U.S. manufacturing that will suffer from a strengthening currency (employment will shift into services and construction instead), meaning that Trump’s policies will damage the same exact sector he is so eager to protect.

Update:

One should note that the Chinese peg to the dollar is more of a “soft peg”. I wrote this yesterday. Today Bloomberg reports that the Yuan has reached its lowest level since December 2008 despite the fact that Chinese authorities have recently taken measures to prop up the currency. Trump’s policy anouncements reduce the allure of emerging markets, thus putting downward pressure on their currrencies, including the Chinese Yuan, which is ironically exactly the opposite Trump is trying to achieve since a strong dollar will weigh on American manufacturing.

http://www.bloomberg.com/news/articles/2016-11-16/china-s-yuan-tumbles-to-eight-year-low-as-banks-weaken-forecasts

RSS Feed

RSS Feed