Below is a link to a very interesting video that features several presentations about monetary policy and the economic slump since 2008.

http://economistsview.typepad.com/economistsview/2013/08/inet-hong-kong-video-the-future-of-central-banking-goodhart-koo-mingkang-and-posen.html

In what follows I will focus on the presentation by the Taiwanese-American economist Richard Koo (minutes 28 to 50 in the video) who is famous for coining the expression ‘Balance Sheet Recession’.

Balance Sheet Recessions

The great economic slump in Japan in the 1990s, the recent recession in the U.S. as well as the Eurozone crisis, for example, can be described as a balance sheet recession. Some economists are very fond of Koo’s invention whereas others rather dislike. I myself find the expression useful because it encourages us to think in terms of assets and liabilities. Specifically, it is of interest how an economic crisis affects the balance sheets of the private sector, that is, households and firms.

A balance sheet recession is an economic slump characterized by a situation in which households and/or firms end up with negative equity, meaning that their assets are worth less than their liabilities. This was the case for Japanese corporations in the early 90s after the burst of the housing and stock market bubble. Similarly, the burst of the housing bubble in the U.S. in 2007/2008 meant that a large number of households ended up ‘underwater’, that is, with negative equity.

Imagine a household with a mortgage of $150.000 on a house currently worth $200.000. Due to the burst of the bubble, the house price drops by 50% to $100.000, which implies that the household ends up with negative equity (the liability exceeds the household’s asset by $50.000).

This is exactly what happened to many households in the U.S. when housing prices collapsed in 2007. Ending up with negative equity, such households had a huge incentive to default on their loans. Thanks to U.S. law, they ‘simply’ walked away from their debt obligation and left their house (the collateral) to the respective creditor. Obviously, this only shifted the problem to the banks, which now ended up with balance sheet problems on their own. In our example, the bank started with an asset worth $150.000 (the credit it gave to the household) but ended up with the collateral, i.e. the house valued at only $100.000. As a result of the households default on the mortgage the bank’s balance sheet deteriorated by $50.000.

This example hopefully makes clear why the huge fall in housing prices in 2007 in the U.S. as well as the collapse of the stock markets had large implications for households, financial institutions, and firms, whose balance sheets deteriorated significantly and at a rapid pace.

A balance sheet recession is thus a situation in which the burst of a bubble leads to the collapse of asset prices while liabilities remain, leaving many private sector balance sheets underwater. As a consequence, the ultimate goal of the private sector, following the collapse of asset prices, is to repair its balance sheets. Households and firms thus increase their savings drastically as they start to deleverage. Unfortunately, the ‘fallacy of composition’ kicks in: what is true for the individual is not true for the economy as a whole. This is Keynes’ ‘paradox of thrift’ and Minsky’s related ‘paradox of deleveraging’: One single individual can start to save more and thus decrease consumption in order to have more in the future, but clearly the entire private sector cannot. That is because for the economy as a whole income is equal to expenditure. If everybody reduces their expenditures, incomes across the board will fall as well. The private sector’s attempt to deleverage will thus reduce aggregate demand and the economy will experience a nasty recession. This reduction in demand further depresses asset prices. The private sector’s attempt to deleverage thus becomes self-defeating as balance sheets deteriorate by even more. This, in turn, induces a further fall in aggregate demand and the economy experiences a downward spiral of falling incomes and asset prices.

Monetary policy ineffective?

Koo’s assessment of a balance sheet recession is that monetary policy is mainly ineffective. Consumption as well as investment might be very inelastic with respect to changes in the real interest rate when the private sector deleverages. In that case even large decreases in the Central Bank’s interest rate might only have a marginal impact on consumption and investment. Furthermore, sooner or later the Central Bank unavoidably hits the Zero-Lower Bound (ZLB) on nominal interest rates. Central Bankers thus face enormous difficulties reviving the economy in a balance sheet recession.

Koo thus thinks that balance sheet recession can only be resolved with large fiscal stimulus programs in order to increase aggregate demand, which cannot be achieved by monetary policy for the reasons given above. This is the part where I strongly disagree with his analysis and where recent events have definitely proven that Koo is wrong on this particular point. Part of the problem lies with Central Bankers themselves. Historically, Central Banks have in fact regulated economic activity by buying (and selling) a variety of assets in the economy. Only during the last decades, the Great Moderation, Central Bankers became accustomed to using the interest rate as the main tool of monetary policy. This is a problem insofar as Central Bankers did not know what to do once interest rates hit the ZLB in many industrialized countries after the crisis in 2007 (and already in the 90s in Japan).

The various policies initiated by the FED (such as QE) in the U.S. and ‘Abenomics’ in Japan, however, have demonstrated that monetary policy can still be highly effective even during balance sheet recessions, contrary to Koo’s belief. Monetary policy mainly works through affecting expectations. The regime change of the Bank of Japan (BOJ) roughly one year ago provided a huge boost to the Japanese economy by increasing inflation expectations à la Krugman. That is, the BOJ ‘credibly promised to be irresponsible’: It convinced the public that it will increase Japanese inflation ‘no matter what’ in order to end two decades of economic stagnation and deflation/low inflation. The result is very promising and Japan has been one of the fastest growing industrialized countries in 2013 with an estimated real growth rate of 2.1%. For comparison: the Eurozone -0.4%, Germany 0.4%, the UK 1.3%, and the U.S. 1.6% (By the way, ranking these countries in terms of 2013 real GDP growth and ranking them in terms of how expansionary their monetary policy has been last year leads to a 1-to-1 correspondence).

Similarly, the various QE programs in the U.S. over the last few years have proven to be highly effective in stimulating aggregate demand and reducing unemployment. QE has mainly worked by positively changing inflation expectations and expectations about future incomes. It also worked by affecting a variety of asset prices. Furthermore, QE provided markets a strong signal that the FED would be engaged in monetary stimulus for a long period.

All the empirical evidence gathered over the last few years thus points towards the fact that countries with more expansionary monetary policy have fared much better since 2007. Monetary stimulus thus has been highly effective in stimulating aggregate demand in Japan and in the U.S. and this is in direct contradiction with Koo’s claim that only fiscal policy can address the shortfall in demand in balance sheet recession.

The Eurozone and the German balance sheet recession of the 2000s

Nonetheless, Koo is definitely right with his assessment that balance sheet recession can have huge economic impacts and that fiscal policy might be necessary in case Central Banks are unable/unwilling to offset the entire shortfall in aggregate demand. The last years have shown that even in the U.S. monetary policy was by far not expansionary enough even though the FED was very aggressive (at least in comparison to the ultra-conservative ECB). In this case, fiscal policy and monetary policy should be complementary in addressing the demand shortfall. Unfortunately, fiscal policy has been highly contractionary in the U.S., the UK and in the Eurozone in recent years and thus exacerbated the economic slump instead of alleviating it.

Despite being wrong on the efficacy of monetary policy during a balance sheet recession, Richard Koo is definitely spot-on when analyzing the dilemma the Eurozone is facing. The ECB has been completely unable to offset the shortfall in demand that occurred as a result of the financial crisis and the Eurozone crisis. Furthermore, it turns out that the institutional setup of the Eurozone makes member countries vulnerable to demand shocks and balance sheet recession, which I will explain below.

More specifically, Koo’s analysis suggests that the largest Eurozone country, Germany, actually experienced a balance sheet recession shortly after the creation of the common currency area. The German economy fell into a deep recession after the burst of the Dot-Com Bubble in the early 2000s.

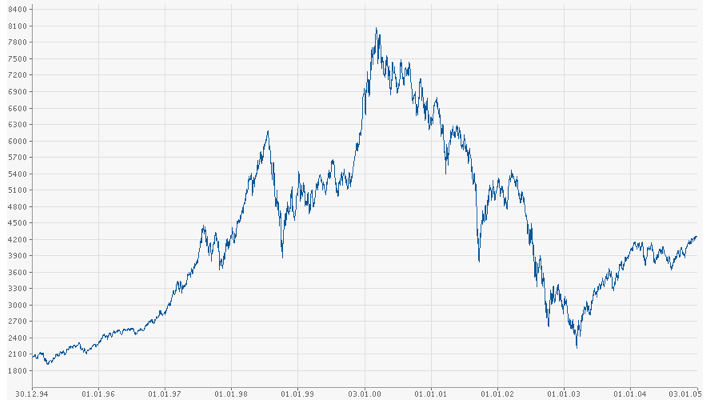

The chart below displays the DAX from 1995 to 2005. The index fell from an all-time high of more than 8000 points in the year 2000 to less than 2500 points within 2 years (a decline of roughly 70%).

http://economistsview.typepad.com/economistsview/2013/08/inet-hong-kong-video-the-future-of-central-banking-goodhart-koo-mingkang-and-posen.html

In what follows I will focus on the presentation by the Taiwanese-American economist Richard Koo (minutes 28 to 50 in the video) who is famous for coining the expression ‘Balance Sheet Recession’.

Balance Sheet Recessions

The great economic slump in Japan in the 1990s, the recent recession in the U.S. as well as the Eurozone crisis, for example, can be described as a balance sheet recession. Some economists are very fond of Koo’s invention whereas others rather dislike. I myself find the expression useful because it encourages us to think in terms of assets and liabilities. Specifically, it is of interest how an economic crisis affects the balance sheets of the private sector, that is, households and firms.

A balance sheet recession is an economic slump characterized by a situation in which households and/or firms end up with negative equity, meaning that their assets are worth less than their liabilities. This was the case for Japanese corporations in the early 90s after the burst of the housing and stock market bubble. Similarly, the burst of the housing bubble in the U.S. in 2007/2008 meant that a large number of households ended up ‘underwater’, that is, with negative equity.

Imagine a household with a mortgage of $150.000 on a house currently worth $200.000. Due to the burst of the bubble, the house price drops by 50% to $100.000, which implies that the household ends up with negative equity (the liability exceeds the household’s asset by $50.000).

This is exactly what happened to many households in the U.S. when housing prices collapsed in 2007. Ending up with negative equity, such households had a huge incentive to default on their loans. Thanks to U.S. law, they ‘simply’ walked away from their debt obligation and left their house (the collateral) to the respective creditor. Obviously, this only shifted the problem to the banks, which now ended up with balance sheet problems on their own. In our example, the bank started with an asset worth $150.000 (the credit it gave to the household) but ended up with the collateral, i.e. the house valued at only $100.000. As a result of the households default on the mortgage the bank’s balance sheet deteriorated by $50.000.

This example hopefully makes clear why the huge fall in housing prices in 2007 in the U.S. as well as the collapse of the stock markets had large implications for households, financial institutions, and firms, whose balance sheets deteriorated significantly and at a rapid pace.

A balance sheet recession is thus a situation in which the burst of a bubble leads to the collapse of asset prices while liabilities remain, leaving many private sector balance sheets underwater. As a consequence, the ultimate goal of the private sector, following the collapse of asset prices, is to repair its balance sheets. Households and firms thus increase their savings drastically as they start to deleverage. Unfortunately, the ‘fallacy of composition’ kicks in: what is true for the individual is not true for the economy as a whole. This is Keynes’ ‘paradox of thrift’ and Minsky’s related ‘paradox of deleveraging’: One single individual can start to save more and thus decrease consumption in order to have more in the future, but clearly the entire private sector cannot. That is because for the economy as a whole income is equal to expenditure. If everybody reduces their expenditures, incomes across the board will fall as well. The private sector’s attempt to deleverage will thus reduce aggregate demand and the economy will experience a nasty recession. This reduction in demand further depresses asset prices. The private sector’s attempt to deleverage thus becomes self-defeating as balance sheets deteriorate by even more. This, in turn, induces a further fall in aggregate demand and the economy experiences a downward spiral of falling incomes and asset prices.

Monetary policy ineffective?

Koo’s assessment of a balance sheet recession is that monetary policy is mainly ineffective. Consumption as well as investment might be very inelastic with respect to changes in the real interest rate when the private sector deleverages. In that case even large decreases in the Central Bank’s interest rate might only have a marginal impact on consumption and investment. Furthermore, sooner or later the Central Bank unavoidably hits the Zero-Lower Bound (ZLB) on nominal interest rates. Central Bankers thus face enormous difficulties reviving the economy in a balance sheet recession.

Koo thus thinks that balance sheet recession can only be resolved with large fiscal stimulus programs in order to increase aggregate demand, which cannot be achieved by monetary policy for the reasons given above. This is the part where I strongly disagree with his analysis and where recent events have definitely proven that Koo is wrong on this particular point. Part of the problem lies with Central Bankers themselves. Historically, Central Banks have in fact regulated economic activity by buying (and selling) a variety of assets in the economy. Only during the last decades, the Great Moderation, Central Bankers became accustomed to using the interest rate as the main tool of monetary policy. This is a problem insofar as Central Bankers did not know what to do once interest rates hit the ZLB in many industrialized countries after the crisis in 2007 (and already in the 90s in Japan).

The various policies initiated by the FED (such as QE) in the U.S. and ‘Abenomics’ in Japan, however, have demonstrated that monetary policy can still be highly effective even during balance sheet recessions, contrary to Koo’s belief. Monetary policy mainly works through affecting expectations. The regime change of the Bank of Japan (BOJ) roughly one year ago provided a huge boost to the Japanese economy by increasing inflation expectations à la Krugman. That is, the BOJ ‘credibly promised to be irresponsible’: It convinced the public that it will increase Japanese inflation ‘no matter what’ in order to end two decades of economic stagnation and deflation/low inflation. The result is very promising and Japan has been one of the fastest growing industrialized countries in 2013 with an estimated real growth rate of 2.1%. For comparison: the Eurozone -0.4%, Germany 0.4%, the UK 1.3%, and the U.S. 1.6% (By the way, ranking these countries in terms of 2013 real GDP growth and ranking them in terms of how expansionary their monetary policy has been last year leads to a 1-to-1 correspondence).

Similarly, the various QE programs in the U.S. over the last few years have proven to be highly effective in stimulating aggregate demand and reducing unemployment. QE has mainly worked by positively changing inflation expectations and expectations about future incomes. It also worked by affecting a variety of asset prices. Furthermore, QE provided markets a strong signal that the FED would be engaged in monetary stimulus for a long period.

All the empirical evidence gathered over the last few years thus points towards the fact that countries with more expansionary monetary policy have fared much better since 2007. Monetary stimulus thus has been highly effective in stimulating aggregate demand in Japan and in the U.S. and this is in direct contradiction with Koo’s claim that only fiscal policy can address the shortfall in demand in balance sheet recession.

The Eurozone and the German balance sheet recession of the 2000s

Nonetheless, Koo is definitely right with his assessment that balance sheet recession can have huge economic impacts and that fiscal policy might be necessary in case Central Banks are unable/unwilling to offset the entire shortfall in aggregate demand. The last years have shown that even in the U.S. monetary policy was by far not expansionary enough even though the FED was very aggressive (at least in comparison to the ultra-conservative ECB). In this case, fiscal policy and monetary policy should be complementary in addressing the demand shortfall. Unfortunately, fiscal policy has been highly contractionary in the U.S., the UK and in the Eurozone in recent years and thus exacerbated the economic slump instead of alleviating it.

Despite being wrong on the efficacy of monetary policy during a balance sheet recession, Richard Koo is definitely spot-on when analyzing the dilemma the Eurozone is facing. The ECB has been completely unable to offset the shortfall in demand that occurred as a result of the financial crisis and the Eurozone crisis. Furthermore, it turns out that the institutional setup of the Eurozone makes member countries vulnerable to demand shocks and balance sheet recession, which I will explain below.

More specifically, Koo’s analysis suggests that the largest Eurozone country, Germany, actually experienced a balance sheet recession shortly after the creation of the common currency area. The German economy fell into a deep recession after the burst of the Dot-Com Bubble in the early 2000s.

The chart below displays the DAX from 1995 to 2005. The index fell from an all-time high of more than 8000 points in the year 2000 to less than 2500 points within 2 years (a decline of roughly 70%).

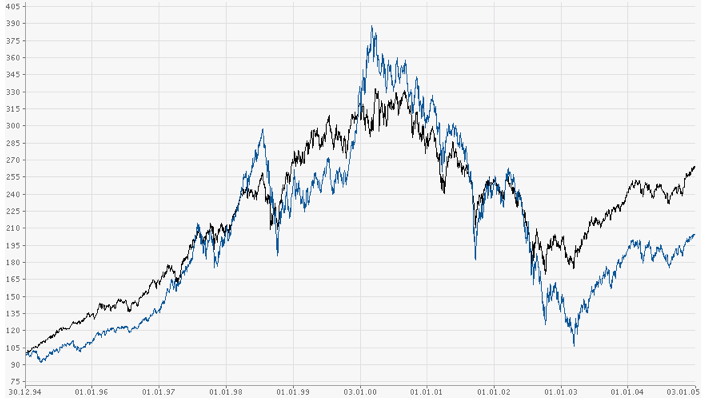

A comparison with the S&P 500 shows that the DAX actually increased by more than the American index during the Dot-Com Bubble and subsequently also showed a larger decline.

DAX (blue) vs. S&P 500 (black)

DAX (blue) vs. S&P 500 (black)

The private sector as a whole in Germany experienced a huge shock in confidence as the result of the burst of the bubble and the associated drop in asset prices in the early 2000s. Subsequently, both firms and consumers increased their savings and started to deleverage as asset prices fell significantly. As a result, aggregate demand decreased significantly as the German private sector sharply increased its savings in the early 2000s.

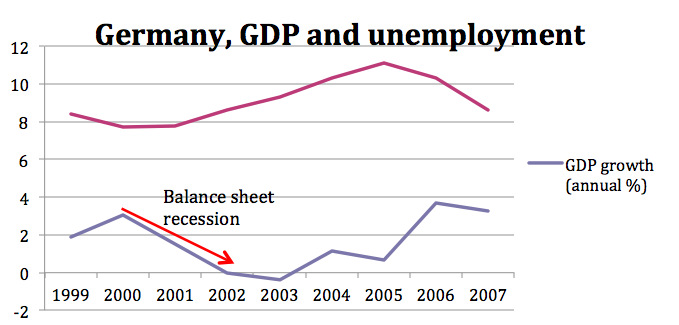

The chart below displays Germany’s real GDP growth rate and the unemployment rate. It is visible how GDP growth declined in 2000/2001 and the recession occurred in 2002/2003. Unemployment basically responded with a lag of one to two years and reached its all-time high of roughly 11% only in 2005 when real GDP growth started to pick up again.

The chart below displays Germany’s real GDP growth rate and the unemployment rate. It is visible how GDP growth declined in 2000/2001 and the recession occurred in 2002/2003. Unemployment basically responded with a lag of one to two years and reached its all-time high of roughly 11% only in 2005 when real GDP growth started to pick up again.

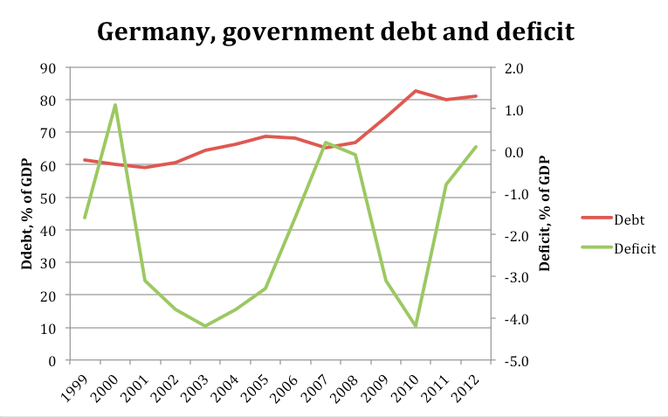

The fall in aggregate demand, the associated recession and the high unemployment rate could have been prevented, or at least mitigated, by expansionary monetary or fiscal policy, which could have prevented such a big shortfall in demand from occurring in the first place. Unfortunately, the Eurozone system is particularly mal-equipped to address idiosyncratic (country-specific) demand shocks. In the German case, the Maastricht criteria prevented the government from engaging in expansionary fiscal policy because Germany already exceeded the government deficit threshold of 3% as well as the debt threshold of 60% (see below). Furthermore, recent times have shown that governments often are unwilling to step in and stimulate demand when the private sector is reducing its expenditures.

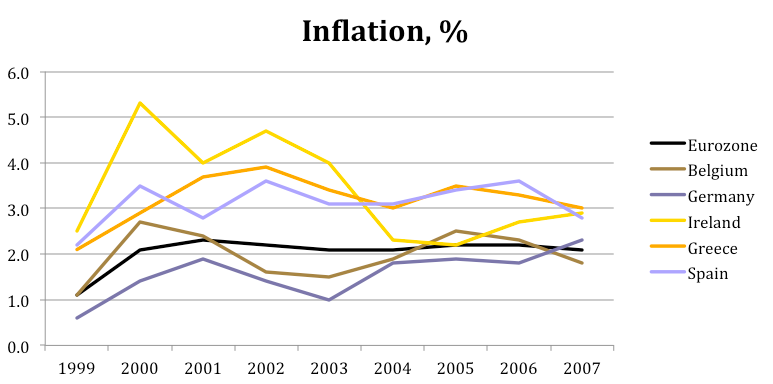

Monetary policy, on the other hand, is made for the Eurozone as a whole. The ECB is (supposedly) a strict inflation-targeter (even though it has undershot its 2% inflation target repeatedly in recent years). One should note though that the ECB targets a Eurozone inflation rate of 2%, which is obviously a weighted-average of the inflation rates of the member countries. The chart below shows how the ECB actually managed to keep Eurozone inflation very close to its target of 2% in between 1999 and 2007. However, inflation rates differed significantly in between Eurozone member countries.

The implications for policy makers in the Eurozone are severe. Consider a small member country like Finland, for example. Were Finland faced with a negative aggregate demand shock, this would have barely any impact on Eurozone inflation and the ECB would thus not react. Consequently, the country would have to rely solely on fiscal policy to counter the negative demand shock.

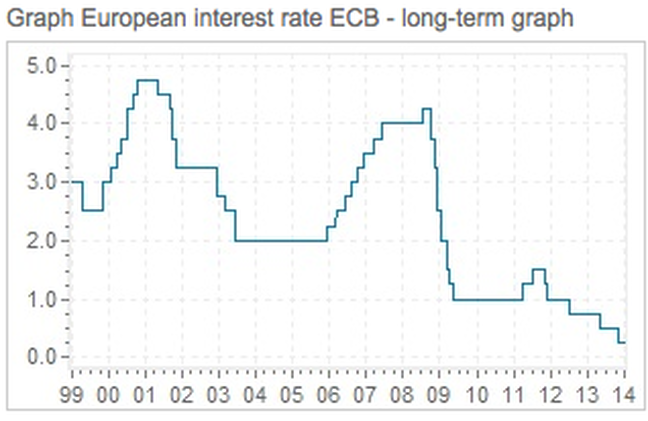

Germany, on the other hand, is by far the largest Eurozone member in terms of GDP. The burst of the Dot-Com bubble temporarily led to slower growth in world output and the German balance sheet recession also affected Eurozone growth and inflation. The following graph shows that the ECB reacted relatively strongly by cutting its interest rate from almost 5% in 2001 to 2% in 2003.

Germany, on the other hand, is by far the largest Eurozone member in terms of GDP. The burst of the Dot-Com bubble temporarily led to slower growth in world output and the German balance sheet recession also affected Eurozone growth and inflation. The following graph shows that the ECB reacted relatively strongly by cutting its interest rate from almost 5% in 2001 to 2% in 2003.

Unfortunately, the change in interest rates initiated by the ECB affected Eurozone member countries very differently. The German private sector continued to deleverage and have high savings rate. German consumption and investment were thus highly irresponsive to the ECB’s rate cut. The story was, however, completely different for the European periphery where the interest rate cut created excessive aggregate demand. The so-called ‘PIIGS’ countries (Portugal, Ireland, Italy, Greece, Spain) thus experienced booming economies during the mid-2000s.

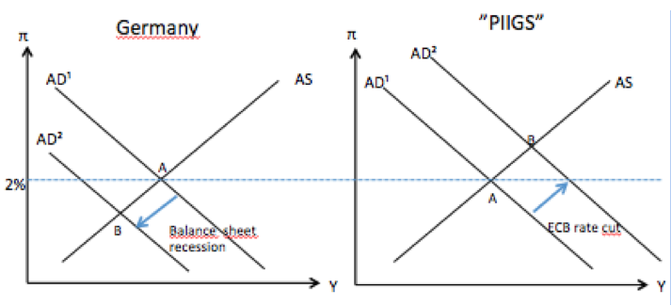

In terms of the AS-AD model, both Germany and the European periphery countries start at a point A where inflation is (roughly) in accordance with the ECB’s 2% inflation target. As a result of Germany’s balance sheet recession in the mid-2000s, the aggregate demand curve shifts to the left and Germany experienced lower inflation (Pi) and lower real output (Y). Subsequently, the ECB’s interest rate cut failed to affect German aggregate demand and the country stays at point B in the diagram. However, the ECB’s policy was highly stimulative to the economies at the European periphery. They experienced excessive aggregate demand (left part of the diagram) with higher output and higher inflation, thus moving from point A to B.

In terms of the AS-AD model, both Germany and the European periphery countries start at a point A where inflation is (roughly) in accordance with the ECB’s 2% inflation target. As a result of Germany’s balance sheet recession in the mid-2000s, the aggregate demand curve shifts to the left and Germany experienced lower inflation (Pi) and lower real output (Y). Subsequently, the ECB’s interest rate cut failed to affect German aggregate demand and the country stays at point B in the diagram. However, the ECB’s policy was highly stimulative to the economies at the European periphery. They experienced excessive aggregate demand (left part of the diagram) with higher output and higher inflation, thus moving from point A to B.

One should note that higher inflation in the European periphery and lower inflation in Germany, even though not desired, is not in contradiction with the ECB’s mandate, which targets a 2% inflation rate for the Eurozone as a whole.

Unfortunately, the dynamics described in the AS-AS framework above were one of the causes of the Eurozone Crisis. Many economists are nowadays in agreement that global imbalances have played a significant role in causing the financial crisis of 2007. More specifically, the ‘competitiveness problem’ of the PIIGS countries is to a great extent not the result of structural factors. Instead, the European periphery experienced excessive aggregate demand in the mid-2000s, leading to high inflation rates and wages, whereas wages and prices remained low in the stagnating German economy.

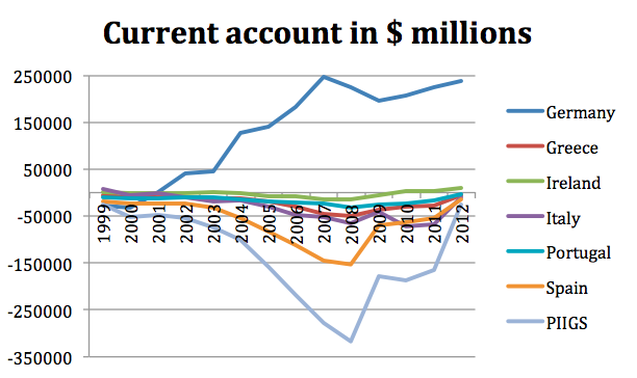

Furthermore, the German balance sheet recession and the following ECB interest rate cut also led to significant imbalances within the Eurozone in terms of the Current Account (CA). One should remember that the Current Account is the difference between domestic savings and investment: CA = S – I.

The German CA thus massively increased in the mid-2000s when the private sector started to deleverage and increased its savings rate significantly (see graph below). Germany thus experienced big CA surpluses not because domestic firms are so highly competitive but rather because of domestic savings/investment decisions. German’s excess savings were then channeled abroad and these capital flows mainly went into the European periphery. The ‘PIIGS’, already suffering from excessive aggregate demand as the result of the ECB’s rate cut, now additionally started to experience massive capital inflows, which further stimulated the economic boom in that region. The European periphery countries were thus forced to run CA deficits as they received large inflows of capital that mainly went into housing and thus caused the bubble.

Unfortunately, the dynamics described in the AS-AS framework above were one of the causes of the Eurozone Crisis. Many economists are nowadays in agreement that global imbalances have played a significant role in causing the financial crisis of 2007. More specifically, the ‘competitiveness problem’ of the PIIGS countries is to a great extent not the result of structural factors. Instead, the European periphery experienced excessive aggregate demand in the mid-2000s, leading to high inflation rates and wages, whereas wages and prices remained low in the stagnating German economy.

Furthermore, the German balance sheet recession and the following ECB interest rate cut also led to significant imbalances within the Eurozone in terms of the Current Account (CA). One should remember that the Current Account is the difference between domestic savings and investment: CA = S – I.

The German CA thus massively increased in the mid-2000s when the private sector started to deleverage and increased its savings rate significantly (see graph below). Germany thus experienced big CA surpluses not because domestic firms are so highly competitive but rather because of domestic savings/investment decisions. German’s excess savings were then channeled abroad and these capital flows mainly went into the European periphery. The ‘PIIGS’, already suffering from excessive aggregate demand as the result of the ECB’s rate cut, now additionally started to experience massive capital inflows, which further stimulated the economic boom in that region. The European periphery countries were thus forced to run CA deficits as they received large inflows of capital that mainly went into housing and thus caused the bubble.

Consequences:

The analysis above demonstrates that the German balance sheet recession of the mid-2000s ultimately might have led to some of the dynamics that caused the Eurozone crisis. The conclusion is unfortunately not very encouraging. It seems that the Eurozone is so diverse that it is hard for the ECB to properly manage well-balanced aggregate demand within the entire currency area. This implies that fiscal policy might have a much larger role to play for aggregate demand management. Germany, for example, should have strengthened economic activity in the mid-2000s with a fiscal stimulus program. This would have increased GDP and reduced unemployment. It also would have decreased the current account surplus, thus reducing the capital flows to Southern Europe that turned out to be a key ingredient for the Euro Crisis. Furthermore, the PIIGS countries should have pursued more contractionary fiscal policies during that time in order to cool down their overheated economies. A fiscal contraction could have somewhat reduced their high current account deficits and maybe even mitigated the buildup of the housing bubble in these economies. More aggregate demand in Germany and less aggregate demand in the PIIGS also would have reduced the price and wage differential that built up in the 2000s and that now turns out be the main source of uncompetitiveness these countries face today.

Unfortunately, governments pursue the wrong kind of policies most of the time. Fiscal policy in the Eurozone has been highly procyclical since its creation and thus amplified the Business Cycle instead of dampening it. It is true that money is roughly neutral in the long-run. The exchange rate regime should thus be of no importance for long-run economic growth. However, countries with a very smooth Business Cycle also tend to have a better economic performance in the long-run. It is thus entirely conceivable that the institutional setup of the Eurozone will lead to a worse performance of Eurozone countries over a longer time horizon because member states will experience higher fluctuations in the Business Cycle as a result of procyclical government policies. This will obviously impose large economic costs on Eurozone residents. Furthermore, the Japanese experience taught us that countries could get trapped in a permanent state of weak aggregate demand for years if stimulative policies are not pursued. Recent indicators now show weak growth for the Eurozone as whole in 2014 (1%) but serious downside-risk remains. Specifically, a phenomenon called debt-deflation by Irving Fisher is a real possibility (explained here: http://macrothoughts.weebly.com/1/post/2013/10/how-the-great-depression-was-mainly-caused-by-france-and-the-us.html).

Further Link:

Richard Koo: “The world in balance sheet recession: causes, cure, and politics”

http://www.paecon.net/PAEReview/issue58/Koo58.pdf

The analysis above demonstrates that the German balance sheet recession of the mid-2000s ultimately might have led to some of the dynamics that caused the Eurozone crisis. The conclusion is unfortunately not very encouraging. It seems that the Eurozone is so diverse that it is hard for the ECB to properly manage well-balanced aggregate demand within the entire currency area. This implies that fiscal policy might have a much larger role to play for aggregate demand management. Germany, for example, should have strengthened economic activity in the mid-2000s with a fiscal stimulus program. This would have increased GDP and reduced unemployment. It also would have decreased the current account surplus, thus reducing the capital flows to Southern Europe that turned out to be a key ingredient for the Euro Crisis. Furthermore, the PIIGS countries should have pursued more contractionary fiscal policies during that time in order to cool down their overheated economies. A fiscal contraction could have somewhat reduced their high current account deficits and maybe even mitigated the buildup of the housing bubble in these economies. More aggregate demand in Germany and less aggregate demand in the PIIGS also would have reduced the price and wage differential that built up in the 2000s and that now turns out be the main source of uncompetitiveness these countries face today.

Unfortunately, governments pursue the wrong kind of policies most of the time. Fiscal policy in the Eurozone has been highly procyclical since its creation and thus amplified the Business Cycle instead of dampening it. It is true that money is roughly neutral in the long-run. The exchange rate regime should thus be of no importance for long-run economic growth. However, countries with a very smooth Business Cycle also tend to have a better economic performance in the long-run. It is thus entirely conceivable that the institutional setup of the Eurozone will lead to a worse performance of Eurozone countries over a longer time horizon because member states will experience higher fluctuations in the Business Cycle as a result of procyclical government policies. This will obviously impose large economic costs on Eurozone residents. Furthermore, the Japanese experience taught us that countries could get trapped in a permanent state of weak aggregate demand for years if stimulative policies are not pursued. Recent indicators now show weak growth for the Eurozone as whole in 2014 (1%) but serious downside-risk remains. Specifically, a phenomenon called debt-deflation by Irving Fisher is a real possibility (explained here: http://macrothoughts.weebly.com/1/post/2013/10/how-the-great-depression-was-mainly-caused-by-france-and-the-us.html).

Further Link:

Richard Koo: “The world in balance sheet recession: causes, cure, and politics”

http://www.paecon.net/PAEReview/issue58/Koo58.pdf

RSS Feed

RSS Feed