Paul Krugman is in my opinion one of the best economists in the field of international economics/macroeconomics. During his entire career, Krugman has shown a unique capability to produce rather simple economic models that are not overly sophisticated in terms of Mathematics, but that can still explain a lot of the patterns we observe in the real world.

He revolutionized Trade Theory as he was the first one to model intra-industry trade and the impact of increasing returns to scale on trade patterns. His trade theory papers actually led to the emergence of two new fields within economics: New Trade Theory and New Economic Geography.

Secondly, he was one of the few to understand the significance of the Japanese experience. He studied the Japan of the 1990s after the burst of the bubbles (real estate and stocks) and produced a nice little model of the liquidity trap, which is highly relevant because as of 2008 all of us are more or less “Japanese” (in the sense that we are constrained by the zero lower-bound on interest rates and that we experience right now a “lost decade” of our own).

Finally, he contributed significantly to the understanding of exchange rate crises. He produced one so-called first generation model. After this one proved to be inadequate to describe the Asian crisis of 1997/98, he came up with another slightly more sophisticated model, a so-called 3rd generation model, that could better explain the dynamics of the events in South-East Asia at that time (Two friends of mine and I, we actually wrote a very nice, short paper about the Asian crisis and the three generations of models on exchange rate crises).

Anyways, very recently Krugman wrote a very interesting article with yet another small but very insightful model. In his paper “Currency Regimes, Capital Flows, and Crises“ presented at the IMF, Krugman (2013) explains why countries having their own currency and borrowing in their own currency cannot experience a “Greek-style” debt crisis.

A loss in confidence in Greek debt will obviously be contractionary for Greece. However, under current liquidity trap conditions, a loss in confidence in American debt will be expansionary for the U.S.! That is because the American $ would depreciate if the Chinese decided to dump all American debt and this would actually boost American GDP (Krugman, 2013).

This result seems very counterintuitive. One should remember, however, that under current economic conditions some normal rules do not apply anymore. In what follows I will describe Krugman’s model in more detail.

The privilege of printing your own money

The first thing one should realize is that a government borrowing on its own currency technically never has to default. Countries in the Eurozone, however, clearly might have to. Greece can run out of cash just as the city of Detroit in the U.S. The American federal government, however, can always print its greenbacks to pay back debt. Obviously, debt monetization would normally result in high inflation levels. Nonetheless, this does not change the basic fact that a country like the U.S. never has to default unless it decides for some reason to so (like it almost happened several weeks ago).

Furthermore, countries without their own Central Bank lack a lender of last resort (the ECB was clearly unwilling to step in and assume this role in the recent crisis). This is a huge problem because countries, just as banks, may be subject to multiple equilibria and self-fulfilling prophecies. Just as healthy banks can experience a bank-run and fail if no lender of last resort steps in, countries without excessive debt levels might nonetheless experience a loss of confidence. Countries such as Spain might then just end up in a bad equilibrium, not because their debt levels are unsustainable but because of self-fulfilling prophecies.

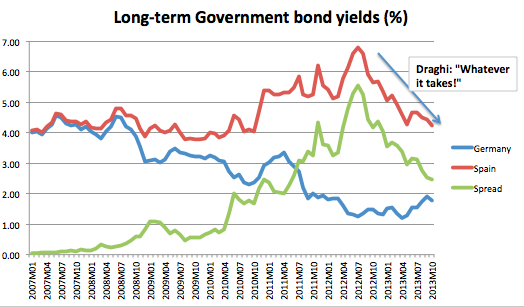

It turns out that the evidence for these claims is substantial. The following graph depicts German and Spanish long-term government bond yields.

He revolutionized Trade Theory as he was the first one to model intra-industry trade and the impact of increasing returns to scale on trade patterns. His trade theory papers actually led to the emergence of two new fields within economics: New Trade Theory and New Economic Geography.

Secondly, he was one of the few to understand the significance of the Japanese experience. He studied the Japan of the 1990s after the burst of the bubbles (real estate and stocks) and produced a nice little model of the liquidity trap, which is highly relevant because as of 2008 all of us are more or less “Japanese” (in the sense that we are constrained by the zero lower-bound on interest rates and that we experience right now a “lost decade” of our own).

Finally, he contributed significantly to the understanding of exchange rate crises. He produced one so-called first generation model. After this one proved to be inadequate to describe the Asian crisis of 1997/98, he came up with another slightly more sophisticated model, a so-called 3rd generation model, that could better explain the dynamics of the events in South-East Asia at that time (Two friends of mine and I, we actually wrote a very nice, short paper about the Asian crisis and the three generations of models on exchange rate crises).

Anyways, very recently Krugman wrote a very interesting article with yet another small but very insightful model. In his paper “Currency Regimes, Capital Flows, and Crises“ presented at the IMF, Krugman (2013) explains why countries having their own currency and borrowing in their own currency cannot experience a “Greek-style” debt crisis.

A loss in confidence in Greek debt will obviously be contractionary for Greece. However, under current liquidity trap conditions, a loss in confidence in American debt will be expansionary for the U.S.! That is because the American $ would depreciate if the Chinese decided to dump all American debt and this would actually boost American GDP (Krugman, 2013).

This result seems very counterintuitive. One should remember, however, that under current economic conditions some normal rules do not apply anymore. In what follows I will describe Krugman’s model in more detail.

The privilege of printing your own money

The first thing one should realize is that a government borrowing on its own currency technically never has to default. Countries in the Eurozone, however, clearly might have to. Greece can run out of cash just as the city of Detroit in the U.S. The American federal government, however, can always print its greenbacks to pay back debt. Obviously, debt monetization would normally result in high inflation levels. Nonetheless, this does not change the basic fact that a country like the U.S. never has to default unless it decides for some reason to so (like it almost happened several weeks ago).

Furthermore, countries without their own Central Bank lack a lender of last resort (the ECB was clearly unwilling to step in and assume this role in the recent crisis). This is a huge problem because countries, just as banks, may be subject to multiple equilibria and self-fulfilling prophecies. Just as healthy banks can experience a bank-run and fail if no lender of last resort steps in, countries without excessive debt levels might nonetheless experience a loss of confidence. Countries such as Spain might then just end up in a bad equilibrium, not because their debt levels are unsustainable but because of self-fulfilling prophecies.

It turns out that the evidence for these claims is substantial. The following graph depicts German and Spanish long-term government bond yields.

Notice how the spread between German and Spanish bonds was practically non-existent before 2007. Ever since the beginning of the crisis, the spread widened to very large levels and reached a record high of 555 basis points (5.55%) in July 2012. In this exact month, Draghi gave his famous “The ECB will do whatever it takes to save the Euro” speech and spreads between government bonds of the so-called PIIGS countries (Portugal, Ireland, Italy, Spain & Greece) and Germany fell immediately. In fact, the spread between Spanish and German government bonds fell by roughly 200 basis points within months. This suggests that the PIIGS countries were indeed caught up in a bad equilibrium and that the ECB could thus have prevented all the painful austerity in Southern Europe if it had assumed its role of lender of last resort.

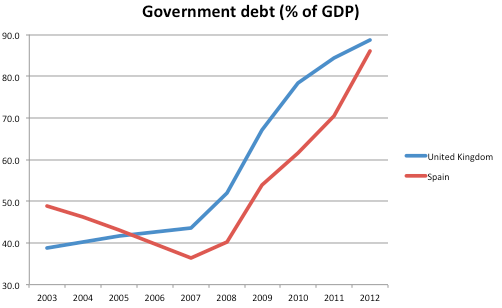

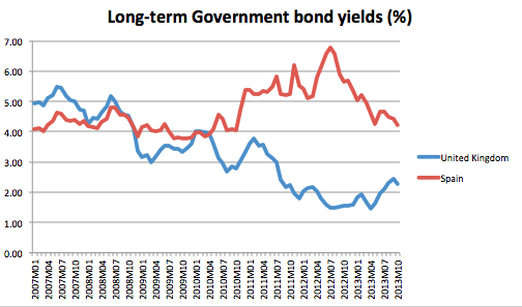

The following two graphs should make it painfully clear how having your own currency MIGHT make a huge difference. Notice how Spain entered the crisis with much lower debt levels than the U.K. In fact, the Spanish fiscal outlook was better than the British in the first years and only very recently the situation reversed. Obviously, Spanish fiscal sustainability clearly deteriorated over the last few years with falling levels of output and mass unemployment. Notice, however, how Spain had to pay much higher interest rates on its debt compared to the U.K. ever since 2007 despite having a very similar fiscal outlook. This suggests that countries that can print their own currency are far less crisis-prone. Self-fulfilling prophecies are less likely to occur because the Central Bank can step in as the lender of last resort.

The following two graphs should make it painfully clear how having your own currency MIGHT make a huge difference. Notice how Spain entered the crisis with much lower debt levels than the U.K. In fact, the Spanish fiscal outlook was better than the British in the first years and only very recently the situation reversed. Obviously, Spanish fiscal sustainability clearly deteriorated over the last few years with falling levels of output and mass unemployment. Notice, however, how Spain had to pay much higher interest rates on its debt compared to the U.K. ever since 2007 despite having a very similar fiscal outlook. This suggests that countries that can print their own currency are far less crisis-prone. Self-fulfilling prophecies are less likely to occur because the Central Bank can step in as the lender of last resort.

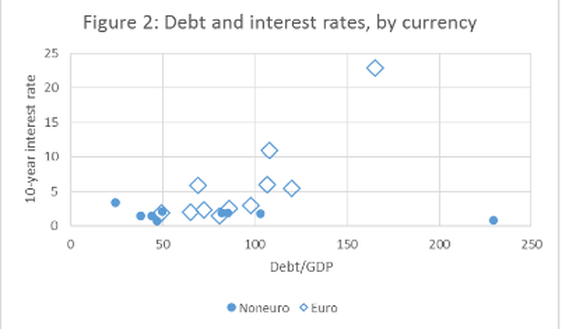

The following graph from Krugman (2013) makes this painfully clear. Using a sample of advanced nations, the graph shows how there is no relationship between the debt-to-GDP ratio and interest rates on government bonds for Non-Euro. Euro-countries on the other hand clearly exhibit a positive relationship between the debt ratio and interest rates.

Notice how the diamond in the upper right corner is Greece. The blue dot to the right is obviously Japan. Actually, hedge funds and finance guys have bet for years now on rising Japanese interest rates and lost billions of $ in the process. This particular trade thus became to be known as the “widowmaker”.

Notice how the diamond in the upper right corner is Greece. The blue dot to the right is obviously Japan. Actually, hedge funds and finance guys have bet for years now on rising Japanese interest rates and lost billions of $ in the process. This particular trade thus became to be known as the “widowmaker”.

Source: Krugman (2013)

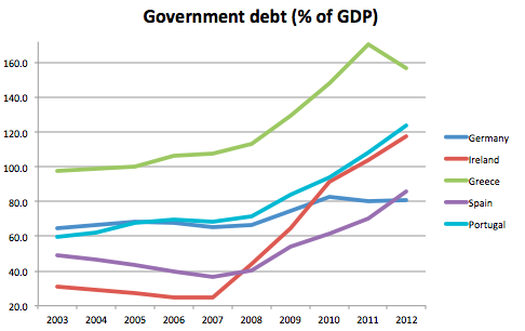

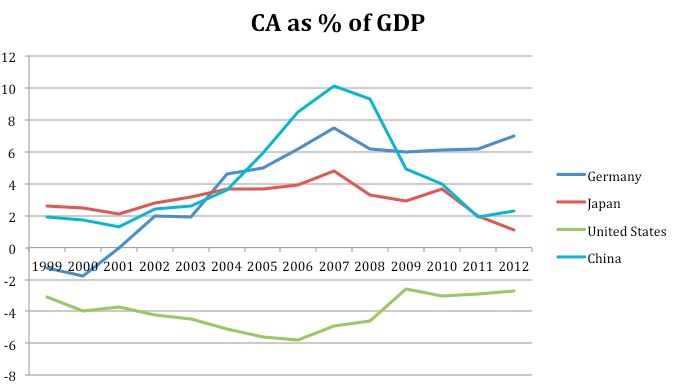

Finally, one should notice that most of the PIIGS countries started actually with relatively low levels of government debt with the exception of Greece (and Italy – not in the graph). Compared to some Northern European countries like Germany, the level of government debt was actually very low in Spain and Ireland before 2007. In that sense, the Eurozone crisis never has been a government debt crisis. Obviously most European policy makers and especially the German government never understood that government debt never was the real problem in the first place. Since they misidentified the nature of the crisis, the so-called cures (i.e. austerity) never could work because they did not address the real problem (obviously, now government debt is much higher in the PIIGS countries but that is the result of the crisis and not the cause of it).

Finally, one should notice that most of the PIIGS countries started actually with relatively low levels of government debt with the exception of Greece (and Italy – not in the graph). Compared to some Northern European countries like Germany, the level of government debt was actually very low in Spain and Ireland before 2007. In that sense, the Eurozone crisis never has been a government debt crisis. Obviously most European policy makers and especially the German government never understood that government debt never was the real problem in the first place. Since they misidentified the nature of the crisis, the so-called cures (i.e. austerity) never could work because they did not address the real problem (obviously, now government debt is much higher in the PIIGS countries but that is the result of the crisis and not the cause of it).

Balance of Payments Crisis

Instead of being a government debt crisis, the Eurozone crisis is to a big extent just a good old-fashioned Balance of Payment crisis. The Eurozone periphery countries experienced large amounts of capital inflows as the result of the creation of the common currency. These capital inflows led to domestic asset bubbles (mainly in housing) and also eroded the competitiveness of these countries because they experienced higher inflation rates and wage increases (I described this dynamic in more detail in my previous blog post).

The crisis is the direct result of an abrupt end of capital flows, a so-called “sudden stop”. Countries that were receiving large capital inflows suddenly had to rebalance their economies as the capital inflows suddenly dried up. This is exactly what happened to Southern Europe. The rebalancing process of the economy, however, crucially depends on the currency regime. We will see that countries with fixed exchange rates (or members of a currency union for that matter) face a very different adjustment mechanism than countries with flexible exchange rates when confronted by a sudden stop.

Krugman (2013) starts with an equation determining the demand for domestic goods or output (y), which is equal to the sum of domestic spending (A) plus net exports (NX):

(1) y = A(r) + NX(y, e)

Domestic spending is a function of the interest rate r: A higher interest rate lowers domestic spending. Net exports is a function of output y and the exchange rate e: Lower output reduces imports and thus increases net exports, the depreciation of the currency also increases net exports.

The second equation is the Balance of Payment (BOP) condition.

(2) K(r,e) + NX(y,e) = 0

This condition says that the sum of the capital account and the current account (net exports) must equal to 0. Capital inflows K are a function of the interest rate and the exchange rate: A higher domestic interest rate will attract more funds from abroad. Furthermore, capital tends to flow into countries with seemingly undervalued currencies, out of countries with seemingly overvalued currencies.

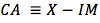

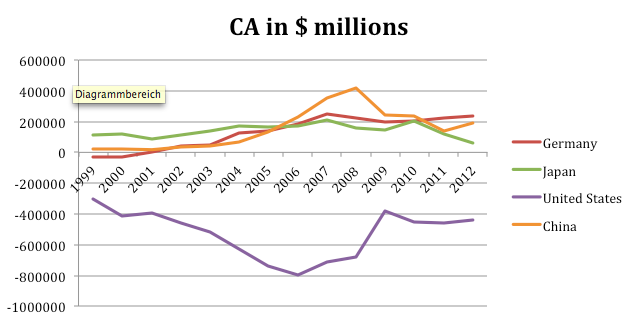

The BOP condition tells us that countries receiving capital inflows have to run a corresponding current account deficit (imports > exports). This was essentially true for the entire Eurozone periphery before 2007 (whereas the Eurozone core countries were mostly running Current Account surpluses).

In 2008, however, all Southern European countries were suddenly confronted by a freeze-up of capital inflows, the “sudden stop”. The huge reduction in capital inflows (K) must be offset by an equivalent increase in net exports (NX) since the BOP condition must hold. Being part of the Eurozone, however, rules out that the adjustment takes place via a depreciation of the currency. Instead, the domestic interest rate must rise to restore equilibrium. The rise of the domestic interest rate attracts capital inflows, but it also depresses domestic spending. Import demand decreases since the economy is deeply depressed, leading to a surge in net exports, thus restoring the BOP condition.

For a country with a fixed exchange rate or a currency union member, the sudden stop will thus play out like a Greek-style debt crisis: An increase in the interest rate, an improvement in the current account, and a deeply depressed economy. Note that the surge in interest rates also implies that people are less willing to hold money. The money supply will thus contract.

Instead of being a government debt crisis, the Eurozone crisis is to a big extent just a good old-fashioned Balance of Payment crisis. The Eurozone periphery countries experienced large amounts of capital inflows as the result of the creation of the common currency. These capital inflows led to domestic asset bubbles (mainly in housing) and also eroded the competitiveness of these countries because they experienced higher inflation rates and wage increases (I described this dynamic in more detail in my previous blog post).

The crisis is the direct result of an abrupt end of capital flows, a so-called “sudden stop”. Countries that were receiving large capital inflows suddenly had to rebalance their economies as the capital inflows suddenly dried up. This is exactly what happened to Southern Europe. The rebalancing process of the economy, however, crucially depends on the currency regime. We will see that countries with fixed exchange rates (or members of a currency union for that matter) face a very different adjustment mechanism than countries with flexible exchange rates when confronted by a sudden stop.

Krugman (2013) starts with an equation determining the demand for domestic goods or output (y), which is equal to the sum of domestic spending (A) plus net exports (NX):

(1) y = A(r) + NX(y, e)

Domestic spending is a function of the interest rate r: A higher interest rate lowers domestic spending. Net exports is a function of output y and the exchange rate e: Lower output reduces imports and thus increases net exports, the depreciation of the currency also increases net exports.

The second equation is the Balance of Payment (BOP) condition.

(2) K(r,e) + NX(y,e) = 0

This condition says that the sum of the capital account and the current account (net exports) must equal to 0. Capital inflows K are a function of the interest rate and the exchange rate: A higher domestic interest rate will attract more funds from abroad. Furthermore, capital tends to flow into countries with seemingly undervalued currencies, out of countries with seemingly overvalued currencies.

The BOP condition tells us that countries receiving capital inflows have to run a corresponding current account deficit (imports > exports). This was essentially true for the entire Eurozone periphery before 2007 (whereas the Eurozone core countries were mostly running Current Account surpluses).

In 2008, however, all Southern European countries were suddenly confronted by a freeze-up of capital inflows, the “sudden stop”. The huge reduction in capital inflows (K) must be offset by an equivalent increase in net exports (NX) since the BOP condition must hold. Being part of the Eurozone, however, rules out that the adjustment takes place via a depreciation of the currency. Instead, the domestic interest rate must rise to restore equilibrium. The rise of the domestic interest rate attracts capital inflows, but it also depresses domestic spending. Import demand decreases since the economy is deeply depressed, leading to a surge in net exports, thus restoring the BOP condition.

For a country with a fixed exchange rate or a currency union member, the sudden stop will thus play out like a Greek-style debt crisis: An increase in the interest rate, an improvement in the current account, and a deeply depressed economy. Note that the surge in interest rates also implies that people are less willing to hold money. The money supply will thus contract.

Source: Krugman (2013)

Why would a country with its own currency engineer a sharp contraction in the money supply when faced with a “sudden stop”?

And the answer is that it wouldn’t. Countries with their own currency face a very different adjustment mechanism because the Central Bank sets the domestic interest rate. They do not experience the loss in output and the contraction in the money supply when faced by a sudden stop. Instead, the loss of confidence (i.e. a sharp reduction in capital inflows) leads to a sharp depreciation of the currency, which increases net exports, ensuring that the BOP condition holds.

Krugman (2013) uses the IS-MP model to illustrate the effect of a sudden stop on countries with their own currency. The model is very similar to the well-known IS-LM model. However, the LM curve is replaced by the MP curve because Central Banks don’t think in terms of money supply anymore, but rather in terms of a Taylor rule: The Central Banks sets the interest rate to respond to divergences of actual output to potential output and actual inflation to the desired inflation target, subject to the zero lower bound (ZLB).

The Central Bank’s reaction function can then be described as follows:

(3) r = Max[0, T(y,e)]

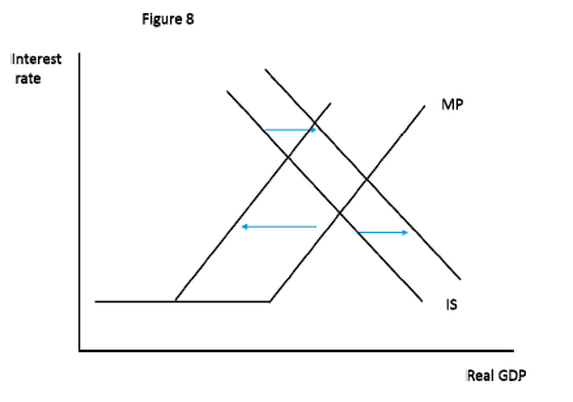

The effects of a sudden stop can thus be represented in the IS-MP model (see below). The depreciation of the domestic currency leads to a boost in exports (the rightward shift of the IS curve). The Central Bank, however, will tighten monetary policy (it cares about the exchange rate "e" in its reaction function) since the depreciation of the currency leads to higher domestic inflation. This will shift the MP curve to the left. Consequently, domestic interest rates rise and output might actually fall if monetary policy becomes overly tight.

Why would a country with its own currency engineer a sharp contraction in the money supply when faced with a “sudden stop”?

And the answer is that it wouldn’t. Countries with their own currency face a very different adjustment mechanism because the Central Bank sets the domestic interest rate. They do not experience the loss in output and the contraction in the money supply when faced by a sudden stop. Instead, the loss of confidence (i.e. a sharp reduction in capital inflows) leads to a sharp depreciation of the currency, which increases net exports, ensuring that the BOP condition holds.

Krugman (2013) uses the IS-MP model to illustrate the effect of a sudden stop on countries with their own currency. The model is very similar to the well-known IS-LM model. However, the LM curve is replaced by the MP curve because Central Banks don’t think in terms of money supply anymore, but rather in terms of a Taylor rule: The Central Banks sets the interest rate to respond to divergences of actual output to potential output and actual inflation to the desired inflation target, subject to the zero lower bound (ZLB).

The Central Bank’s reaction function can then be described as follows:

(3) r = Max[0, T(y,e)]

The effects of a sudden stop can thus be represented in the IS-MP model (see below). The depreciation of the domestic currency leads to a boost in exports (the rightward shift of the IS curve). The Central Bank, however, will tighten monetary policy (it cares about the exchange rate "e" in its reaction function) since the depreciation of the currency leads to higher domestic inflation. This will shift the MP curve to the left. Consequently, domestic interest rates rise and output might actually fall if monetary policy becomes overly tight.

Source: Krugman (2013)

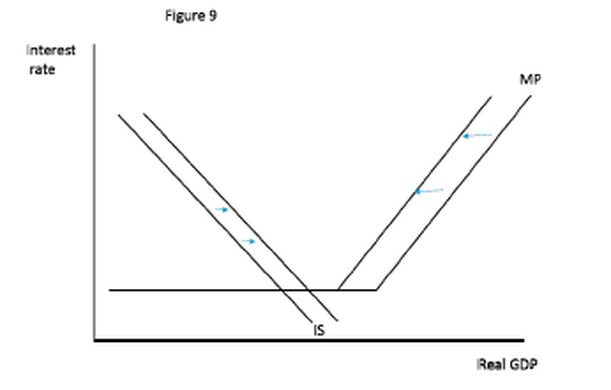

However, ever since 2007/2008 most industrialized countries have been stuck at the ZLB on interest rates (the flat part of the MP curve). Under current conditions, a loss in confidence would lead to the aforementioned shift in the IS curve as net exports go up and this will lead to an increase in domestic output.

However, ever since 2007/2008 most industrialized countries have been stuck at the ZLB on interest rates (the flat part of the MP curve). Under current conditions, a loss in confidence would lead to the aforementioned shift in the IS curve as net exports go up and this will lead to an increase in domestic output.

Source: Krugman (2013)

The implications of this entire discussion are quite severe. Not only can a country like the U.S. not experience a Greek-style debt crisis, but also contrary to popular belief, the Chinese would actually do the U.S. a favor if they were to dump all their holdings of American government debt.

How realistic is the model?

According to Krugman (2013), it is historically close to impossible to find examples of countries that print and borrow in their own currency and experienced a Greek-style debt crisis! It just didn’t happen. All past crises involved countries being on some kind of fixed exchange rate regime (e.g. the gold standard) and/or borrowing excessively in foreign currency (e.g. Asia 1997/1998).

Krugman (2013) mentions France of the 1920s as one example of a country that experienced a massive loss in confidence by foreign investors. France was politically unstable and in ruins as a result of World War I. However, nothing similar to the Greek experience happened. Instead, capital flights led to a massive depreciation of the FRANC and despite high levels of domestic inflation, France experienced strong output growth. Note how this is very much in accordance with the model!

One should also note how the result from above does NOT apply to countries borrowing in foreign currency. This happened, for example, in South East Asia in 1997/1998 where debt levels exploded as the result of the depreciation of the currency. The adverse balance sheet effects were far more severe in the short-run than the boost in exports and output levels fell dramatically. Again, nothing like this can happen to countries like the U.S., the U.K., Japan, which do borrow in their own currency. Notice how American balance sheets actually improve when the $ depreciates because American liabilities are denoted in $ but foreign asset are denoted in foreign currency and increase in value.

Finally, one way to think about the monetary policy implemented by the Bank of Japan since the start of Abenomics is that they basically try to engineer a run out of Japanese government debt. Japan complained in 2010 how China bought too much Japanese government debt, driving up the value of the Yen and imposing deflation on Japan (Krugman, 2013)! Abenomics is basically an attempt to convince investors that the value of Japanese bonds will be eroded by higher inflation. One of the byproducts of the monetary expansion is thus a flight out of Japanese bonds by foreigners, driving down the value of the Yen, which is expansionary for Japan!

Recently, many people have feared that the U.S. will experience a loss of confidence, but the Japanese experience tells us that there is really nothing to be concerned about under current economic conditions! The entire discussion above thus implies that anyone claiming that the U.S. or the U.K could become the “next Greece” really is generally clueless!

Sources:

The paper at hand with a video of Krugman’s presentation at the IMF:

Krugman, Paul, 2013, “Currency Regimes, Capital Flows, and Crises,” Mundell‐ Fleming Lecture, Jacques Polak Research Conference, International Monetary Fund, Washington DC, November.

Video: http://www.imf.org/external/mmedia/view.aspx?vid=2820747172001

IS-MP model:

Romer, David (2013), “Short-run fluctuations,” mimeo, Berkeley.

Since I mentioned some of Krugman’s work in the introduction, I will provide the reference of 3 other great papers that are also related to the topic at hand (especially the 2 papers on exchange rate crises):

1st generation model of exchange rate crisis:

Krugman, Paul (1979), “A model of balance of payments crises,” Journal of Money, Credit, and Banking

3rd generation model of exchange rate crisis:

Krugman, Paul (1999), “Balance sheets, the transfer problem, and financial crises,” International Tax and Public Finance.

Japan’s liquidty trap:

Krugman, Paul (1998), “It’s baaack: Japan’s slump and the return of the liquidity trap,” Brookings Papers on Economic Activity.

The implications of this entire discussion are quite severe. Not only can a country like the U.S. not experience a Greek-style debt crisis, but also contrary to popular belief, the Chinese would actually do the U.S. a favor if they were to dump all their holdings of American government debt.

How realistic is the model?

According to Krugman (2013), it is historically close to impossible to find examples of countries that print and borrow in their own currency and experienced a Greek-style debt crisis! It just didn’t happen. All past crises involved countries being on some kind of fixed exchange rate regime (e.g. the gold standard) and/or borrowing excessively in foreign currency (e.g. Asia 1997/1998).

Krugman (2013) mentions France of the 1920s as one example of a country that experienced a massive loss in confidence by foreign investors. France was politically unstable and in ruins as a result of World War I. However, nothing similar to the Greek experience happened. Instead, capital flights led to a massive depreciation of the FRANC and despite high levels of domestic inflation, France experienced strong output growth. Note how this is very much in accordance with the model!

One should also note how the result from above does NOT apply to countries borrowing in foreign currency. This happened, for example, in South East Asia in 1997/1998 where debt levels exploded as the result of the depreciation of the currency. The adverse balance sheet effects were far more severe in the short-run than the boost in exports and output levels fell dramatically. Again, nothing like this can happen to countries like the U.S., the U.K., Japan, which do borrow in their own currency. Notice how American balance sheets actually improve when the $ depreciates because American liabilities are denoted in $ but foreign asset are denoted in foreign currency and increase in value.

Finally, one way to think about the monetary policy implemented by the Bank of Japan since the start of Abenomics is that they basically try to engineer a run out of Japanese government debt. Japan complained in 2010 how China bought too much Japanese government debt, driving up the value of the Yen and imposing deflation on Japan (Krugman, 2013)! Abenomics is basically an attempt to convince investors that the value of Japanese bonds will be eroded by higher inflation. One of the byproducts of the monetary expansion is thus a flight out of Japanese bonds by foreigners, driving down the value of the Yen, which is expansionary for Japan!

Recently, many people have feared that the U.S. will experience a loss of confidence, but the Japanese experience tells us that there is really nothing to be concerned about under current economic conditions! The entire discussion above thus implies that anyone claiming that the U.S. or the U.K could become the “next Greece” really is generally clueless!

Sources:

The paper at hand with a video of Krugman’s presentation at the IMF:

Krugman, Paul, 2013, “Currency Regimes, Capital Flows, and Crises,” Mundell‐ Fleming Lecture, Jacques Polak Research Conference, International Monetary Fund, Washington DC, November.

Video: http://www.imf.org/external/mmedia/view.aspx?vid=2820747172001

IS-MP model:

Romer, David (2013), “Short-run fluctuations,” mimeo, Berkeley.

Since I mentioned some of Krugman’s work in the introduction, I will provide the reference of 3 other great papers that are also related to the topic at hand (especially the 2 papers on exchange rate crises):

1st generation model of exchange rate crisis:

Krugman, Paul (1979), “A model of balance of payments crises,” Journal of Money, Credit, and Banking

3rd generation model of exchange rate crisis:

Krugman, Paul (1999), “Balance sheets, the transfer problem, and financial crises,” International Tax and Public Finance.

Japan’s liquidty trap:

Krugman, Paul (1998), “It’s baaack: Japan’s slump and the return of the liquidity trap,” Brookings Papers on Economic Activity.

RSS Feed

RSS Feed