It is truly amazing how many of the so-called ‘very serious people’ have proclaimed in recent years that money has been extremely easy and that hyperinflation was lurking around every corner. Of course, they couldn’t have been more wrong. Economists like Krugman, who knew about the liquidity trap, warned early on that inflation would be the least of our worries and that more inflation would actually be highly desirable.

It is thus a mystery how journalists, policy makers and Wall Street continue to claim that monetary policy is too expansionary, especially since we have had record-low inflation rates in the U.S. over the last couple of years and while the Eurozone finds itself flirting with deflation at the moment. The most common fallacy is obviously to associate low nominal interest rates with easy money. Furthermore, Central Banks around the world, especially the FED, have been pumping trillions of dollars into markets with the initiation of the various QE programs (Quantitative Easing) in the U.S. and elsewhere ever since the crisis started. So people just assume that monetary policy must be highly accommodative since nominal interest rates are low and since Central Banks currently print a lot of money. But nothing could be further from the truth.

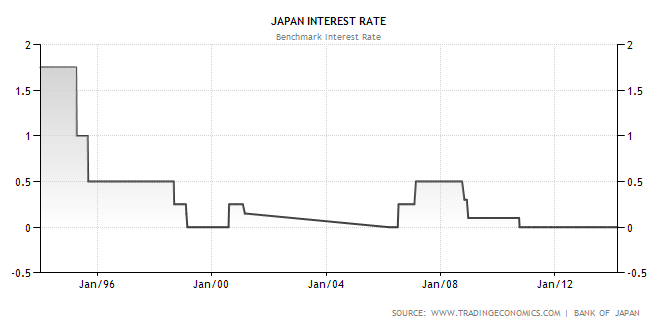

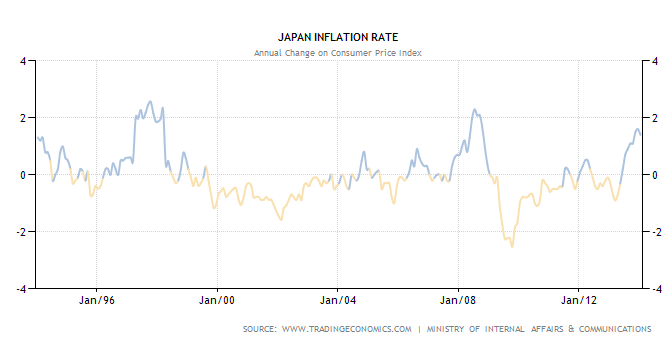

First, nominal interest rates are according to Milton Friedman a terrible indicator of the stance of monetary policy. Japan has had zero or close to zero nominal interest rates for almost two decades. They also tried QE in the late 1990s and early 2000s, but with only very limited success. But instead of suffering from hyperinflation as some pundits would have predicted, Japan actually experienced two decades of record-low inflation levels and even deflationary periods.

Below are nominal interest rates and inflation rates in Japan over the last 20 years:

It is thus a mystery how journalists, policy makers and Wall Street continue to claim that monetary policy is too expansionary, especially since we have had record-low inflation rates in the U.S. over the last couple of years and while the Eurozone finds itself flirting with deflation at the moment. The most common fallacy is obviously to associate low nominal interest rates with easy money. Furthermore, Central Banks around the world, especially the FED, have been pumping trillions of dollars into markets with the initiation of the various QE programs (Quantitative Easing) in the U.S. and elsewhere ever since the crisis started. So people just assume that monetary policy must be highly accommodative since nominal interest rates are low and since Central Banks currently print a lot of money. But nothing could be further from the truth.

First, nominal interest rates are according to Milton Friedman a terrible indicator of the stance of monetary policy. Japan has had zero or close to zero nominal interest rates for almost two decades. They also tried QE in the late 1990s and early 2000s, but with only very limited success. But instead of suffering from hyperinflation as some pundits would have predicted, Japan actually experienced two decades of record-low inflation levels and even deflationary periods.

Below are nominal interest rates and inflation rates in Japan over the last 20 years:

I will just reproduce what Milton Friedman had to say about nominal interest rates and the stance of monetary policy, a quote that I also used in my last post. But it is really important since most people seem to be utterly confused about this issue. Here is Friedman:

After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die.

So nominal interest rates were actually falling instead of rising when the FED aggressively fought inflation in the 1980s. Usually, low interest rates are a sign that monetary policy is extremely tight. The Japanese malaise, the Great Depression and the current recession in the Eurozone are all proof of that.

So the question remains what exactly are reliable indicators of easy or tight money. Monetarists in the 1980s focused on monetary aggregates. This, however, turned out to be a failure. As Krugman has put it once: we don’t really know anymore what ‘money’ is. The distinction between money and very close substitutes has become increasingly blurry. So it is not entirely clear which monetary aggregate one should actually focus on: M1, M2 or M3. It also has become very difficult for officials to actually measure the money stock in the economy. The FED does not even publish M3 figures anymore ever since 2006 since data collection has become too difficult.

The monetarists’ emphasis on monetary aggregates in the 1980s relied largely on the belief that stable money growth would lead to stable growth in nominal GDP (NGDP). The underlying assumption was of course that the velocity of money, the frequency in which money changes hands, is relatively constant. From the quantity equation, we know that:

M*V = NGDP where M is the money stock and V is the velocity of money

If V is constant, then the growth rate of NGDP must equal the growth rate of the money stock. But we know that the assumption of constant velocity is untrue. Velocity tends to fluctuate and is in fact highly unstable in times of crises. This is indeed what happened during the financial crisis of 2008. Even as Central Banks significantly increased the money stock, the demand for money surged. Money velocity thus plummeted as people stopped spending on goods and services. So if huge increases in the money stock are offset by large enough decreases in money velocity, then NGDP (aggregate demand) will actually fall and this exactly what happened in the U.S. in 2008.

According to Ben Bernanke, the only reliable indicators of the stance of monetary policy are actually the inflation rate and nominal GDP growth, which is by definition equal to the money stock times money velocity. Monetarists in the 1980s solely focused on M to determine the stance of monetary policy whereas they should have focused on M*V=NGDP.

An example of easy money:

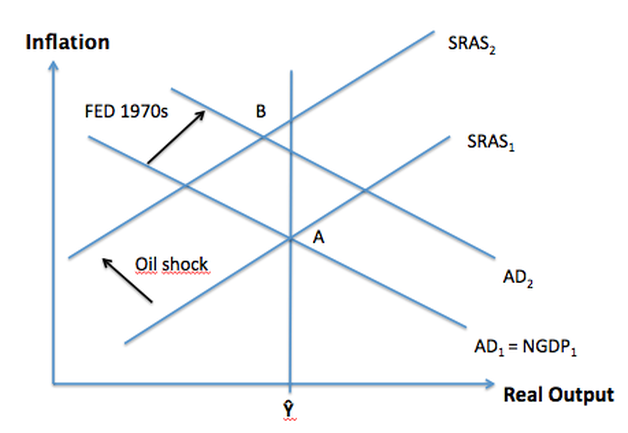

The 1970s are the common example of a period where money was too easy. Contrary to common belief, the oil shocks were not the cause of high inflation rates at that time, at least not directly. Instead, it was the response of incompetent Central Bankers that caused excessive inflation in the 1970s. Advanced economies suffered from relatively low growth and rising unemployment at that time and Central Bankers tried to address these problems by printing money.

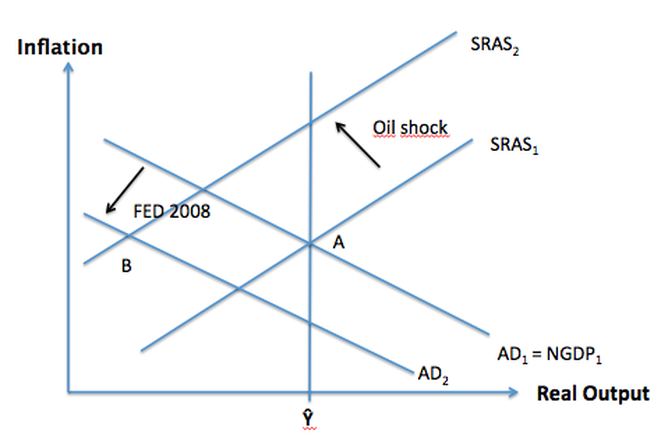

This was obviously a fatal mistake. Printing money is the correct response when facing a negative aggregate demand shock (AD), which is a nominal shock. But the oil shocks were a real shock (supply shock), which cannot be addressed by stimulating aggregate demand.

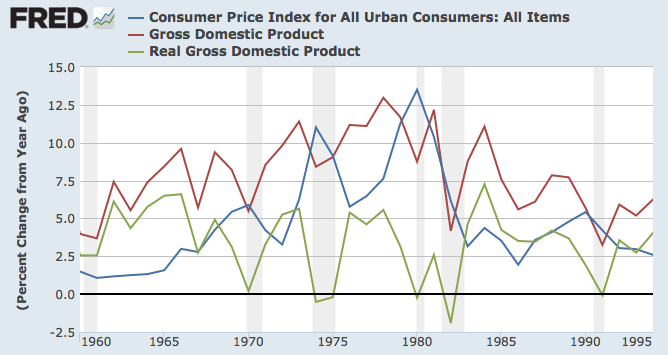

The graph below shows how real GDP growth for the U.S. was lower in the 1970s than before (especially in 1970 and 1975). This was obviously the direct result of rapidly rising oil prices, which can be interpreted as a productivity shock to the U.S. economy.

So the question remains what exactly are reliable indicators of easy or tight money. Monetarists in the 1980s focused on monetary aggregates. This, however, turned out to be a failure. As Krugman has put it once: we don’t really know anymore what ‘money’ is. The distinction between money and very close substitutes has become increasingly blurry. So it is not entirely clear which monetary aggregate one should actually focus on: M1, M2 or M3. It also has become very difficult for officials to actually measure the money stock in the economy. The FED does not even publish M3 figures anymore ever since 2006 since data collection has become too difficult.

The monetarists’ emphasis on monetary aggregates in the 1980s relied largely on the belief that stable money growth would lead to stable growth in nominal GDP (NGDP). The underlying assumption was of course that the velocity of money, the frequency in which money changes hands, is relatively constant. From the quantity equation, we know that:

M*V = NGDP where M is the money stock and V is the velocity of money

If V is constant, then the growth rate of NGDP must equal the growth rate of the money stock. But we know that the assumption of constant velocity is untrue. Velocity tends to fluctuate and is in fact highly unstable in times of crises. This is indeed what happened during the financial crisis of 2008. Even as Central Banks significantly increased the money stock, the demand for money surged. Money velocity thus plummeted as people stopped spending on goods and services. So if huge increases in the money stock are offset by large enough decreases in money velocity, then NGDP (aggregate demand) will actually fall and this exactly what happened in the U.S. in 2008.

According to Ben Bernanke, the only reliable indicators of the stance of monetary policy are actually the inflation rate and nominal GDP growth, which is by definition equal to the money stock times money velocity. Monetarists in the 1980s solely focused on M to determine the stance of monetary policy whereas they should have focused on M*V=NGDP.

An example of easy money:

The 1970s are the common example of a period where money was too easy. Contrary to common belief, the oil shocks were not the cause of high inflation rates at that time, at least not directly. Instead, it was the response of incompetent Central Bankers that caused excessive inflation in the 1970s. Advanced economies suffered from relatively low growth and rising unemployment at that time and Central Bankers tried to address these problems by printing money.

This was obviously a fatal mistake. Printing money is the correct response when facing a negative aggregate demand shock (AD), which is a nominal shock. But the oil shocks were a real shock (supply shock), which cannot be addressed by stimulating aggregate demand.

The graph below shows how real GDP growth for the U.S. was lower in the 1970s than before (especially in 1970 and 1975). This was obviously the direct result of rapidly rising oil prices, which can be interpreted as a productivity shock to the U.S. economy.

A productivity shock shifts the Aggregate Supply Curve to the left and this would lead to lower real output and somewhat higher inflation (see my figure below). However, a real shock does not affect aggregate demand if the Central Bank is determined to keep nominal GDP stable (note that I use AD and NGDP interchangeably since they are the same thing). The graph above, however, also shows that NGDP for the U.S. was much higher in the late 1970s than before. The FED thus reacted to the negative supply shock of rising oil prices by stimulating aggregate demand (the rightward shift of the AD curve), which led to a further rise in the inflation rate.

Modern Central Banks would probably have done the opposite and the FED of 2008 is actually proof of that. I described in my last post how the FED officials are largely responsible for the economic crisis since they allowed a huge drop in aggregate demand because of temporarily higher inflation rates as result of the 2008 oil shock (see here: http://macrothoughts.weebly.com/1/post/2014/02/youre-right-we-did-it-twice.html).

This was obviously a large mistake. Many economists belief that Central Banks should stabilize NGDP. In recent years, there has actually been a rising endorsement in academia for the idea that Central Banks should target NGDP growth instead of targeting inflation rates. The economic downturn both in the U.S. and in the Eurozone has been so severe because these economies experienced the largest fall in NGDP ever since the Great Depression.

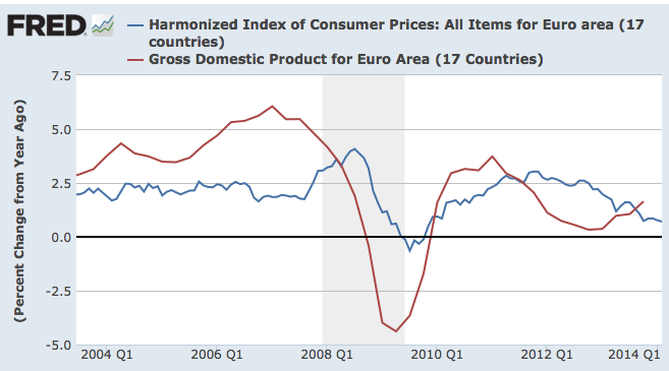

Note that the large drop in NGDP cannot be explained by structural problems even though many European policy-makers like to suggest so. Structural problems, such as reductions in productivity and the like, would shift the AS curve to the left, or possibly even reduce long-run potential output of the economy. This would lead to an increase in inflation and reduce real output but should (mainly) not affect aggregate demand. However, ever since 2008 the Eurozone has experienced low inflation rates and low NGDP growth. Record unemployment and low growth rates in the Eurozone can perfectly be explained by a reduction in nominal spending: Both the private sector and the public sector reduce their expenditures and both sectors contract. This leads to higher unemployment and falling asset prices, which reduces expenditures even further and the vicious cycle continues. This reduction in nominal spending on goods and service is for the most part totally unrelated to structural problems.

Note that the large drop in NGDP cannot be explained by structural problems even though many European policy-makers like to suggest so. Structural problems, such as reductions in productivity and the like, would shift the AS curve to the left, or possibly even reduce long-run potential output of the economy. This would lead to an increase in inflation and reduce real output but should (mainly) not affect aggregate demand. However, ever since 2008 the Eurozone has experienced low inflation rates and low NGDP growth. Record unemployment and low growth rates in the Eurozone can perfectly be explained by a reduction in nominal spending: Both the private sector and the public sector reduce their expenditures and both sectors contract. This leads to higher unemployment and falling asset prices, which reduces expenditures even further and the vicious cycle continues. This reduction in nominal spending on goods and service is for the most part totally unrelated to structural problems.

Inflation rates and NGDP growth rates depicted in the graph below tell us a clear story, namely that money has been extremely tight in the Eurozone over the last couple of years. The ECB is mainly responsible for keeping aggregate demand stable but clearly failed to do so. The economic downturn in the Eurozone should be attributed to incompetent policy-makers who focused on structural problems while the actual problem was always the large reduction in AD.

So what should be done?

First of all, policy-makers in Europe should finally realize that austerity was a complete and utter failure. There was never any (reasonable) economic theory according to which government spending cuts would make sense when the economy faces a negative AD shock. The IMF apologized and estimated ex-post that fiscal multipliers in Southern Europe could have been close to 2 in recent years. This means that with every Euro the government decides to save, not only does the public sector contract by one Euro but the private sector contracts by one Euro as well, so that the entire economy would actually contract by two Euros. In such a case austerity is clearly self-defeating and could never reduce government debt. That is because the economy’s GDP actually shrinks at a faster rate than government spending, so that the debt-to-GDP ratio rises. This is of course exactly what happened in the Eurozone. Government debt ratios in Southern Europe are higher than ever before and, ironically, debt-to-GDP ratios would have been lower if the governments had not implemented all these austerity measures. With a fiscal multiplier of 2, government spending is even likely to be self-financing and might in extreme cases actually reduce the debt burden (even though the Central Bank’s reaction function is crucial for this assumption).

All of this was predictable, and was in fact predicted by people like Krugman and DeLong.

But it is even more important to finally set the ECB straight, which has been running a policy of extremely tight money at the expense of economic growth and employment ever since 2008.

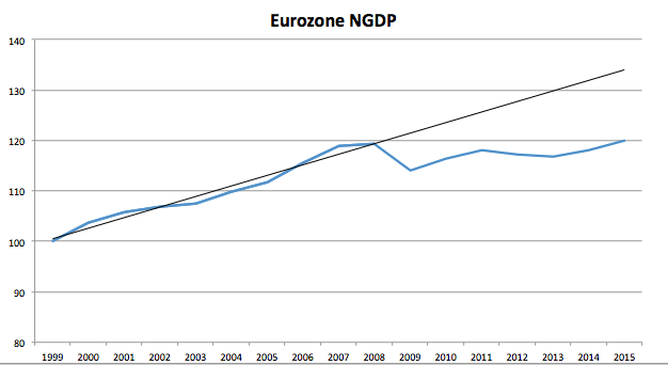

The following graph shows actual Eurozone NGDP, including the forecast for 2014 and 2015, and the pre-2009 trend line. As of 2013, the difference between this trend and actual NGDP is 10%. That means that the Eurozone should have produced roughly 855 BILLION Euros more in goods and services than it actually did. Furthermore, the gap between the trend and actual NGDP is still widening since economic growth for the coming years remain rather weak. The projected difference for 2015 is roughly 12%. So according to the pre-2009 trend line, Eurozone production of goods and services in 2015 should be higher by about an additional 1 TRILLION Euros than actual production! Most of this shortfall in NGDP is to be blamed on the ECB, which failed to stabilize aggregate demand.

First of all, policy-makers in Europe should finally realize that austerity was a complete and utter failure. There was never any (reasonable) economic theory according to which government spending cuts would make sense when the economy faces a negative AD shock. The IMF apologized and estimated ex-post that fiscal multipliers in Southern Europe could have been close to 2 in recent years. This means that with every Euro the government decides to save, not only does the public sector contract by one Euro but the private sector contracts by one Euro as well, so that the entire economy would actually contract by two Euros. In such a case austerity is clearly self-defeating and could never reduce government debt. That is because the economy’s GDP actually shrinks at a faster rate than government spending, so that the debt-to-GDP ratio rises. This is of course exactly what happened in the Eurozone. Government debt ratios in Southern Europe are higher than ever before and, ironically, debt-to-GDP ratios would have been lower if the governments had not implemented all these austerity measures. With a fiscal multiplier of 2, government spending is even likely to be self-financing and might in extreme cases actually reduce the debt burden (even though the Central Bank’s reaction function is crucial for this assumption).

All of this was predictable, and was in fact predicted by people like Krugman and DeLong.

But it is even more important to finally set the ECB straight, which has been running a policy of extremely tight money at the expense of economic growth and employment ever since 2008.

The following graph shows actual Eurozone NGDP, including the forecast for 2014 and 2015, and the pre-2009 trend line. As of 2013, the difference between this trend and actual NGDP is 10%. That means that the Eurozone should have produced roughly 855 BILLION Euros more in goods and services than it actually did. Furthermore, the gap between the trend and actual NGDP is still widening since economic growth for the coming years remain rather weak. The projected difference for 2015 is roughly 12%. So according to the pre-2009 trend line, Eurozone production of goods and services in 2015 should be higher by about an additional 1 TRILLION Euros than actual production! Most of this shortfall in NGDP is to be blamed on the ECB, which failed to stabilize aggregate demand.

As a first step towards economic recovery, the ECB should finally reduce interest rates to zero. Like the other major Central Banks, it should also initiate some form of forward-guidance or forward-commitment: Basically, the ECB should promise that interest rates remain at zero until the recovery is well on its way.

Furthermore, there is clearly a need for the ECB to change its mandate. Over the last couple of years it has become abundantly clear that a 2% inflation target is really not optimal, even when it is symmetric (that is, if undershooting occurs as frequently on average as overshooting). However, inflation targets have been highly asymmetric in recent years: Central Banks frequently undershot the target and rather saw the 2% as an upper bound than as an average. The ECB should in my opinion follow the advice Bernanke gave to the Japanese in the early 2000s and adopt a Price-level target.

I think that a price-level target with 2.5% year-on-year inflation or maybe even 3% inflation would be a good idea for the Eurozone. The table below illustrates how such a policy would work. With a 3% level target and an initial price level of 100, the Central Bank tries to reach a price level of 100*1.03=103 after one year, 103*1.03=106.1 after two years, and so on.

If actual inflation during year one, however, is only 1%, then the actual price level is only 101. The Central Bank then has to make up for its mistake and needs an inflation rate of 5.1% to reach its target price level of 106.1. The crucial difference between an inflation target and a price-level target is that under the latter the Central Bank has to correct past mistakes. Obviously, if the Central Bank were to overshoot its target in one year, then it would also have to make up for it with lower inflation in the subsequent year. The policy is thus supposed to be completely symmetrical.

Furthermore, there is clearly a need for the ECB to change its mandate. Over the last couple of years it has become abundantly clear that a 2% inflation target is really not optimal, even when it is symmetric (that is, if undershooting occurs as frequently on average as overshooting). However, inflation targets have been highly asymmetric in recent years: Central Banks frequently undershot the target and rather saw the 2% as an upper bound than as an average. The ECB should in my opinion follow the advice Bernanke gave to the Japanese in the early 2000s and adopt a Price-level target.

I think that a price-level target with 2.5% year-on-year inflation or maybe even 3% inflation would be a good idea for the Eurozone. The table below illustrates how such a policy would work. With a 3% level target and an initial price level of 100, the Central Bank tries to reach a price level of 100*1.03=103 after one year, 103*1.03=106.1 after two years, and so on.

If actual inflation during year one, however, is only 1%, then the actual price level is only 101. The Central Bank then has to make up for its mistake and needs an inflation rate of 5.1% to reach its target price level of 106.1. The crucial difference between an inflation target and a price-level target is that under the latter the Central Bank has to correct past mistakes. Obviously, if the Central Bank were to overshoot its target in one year, then it would also have to make up for it with lower inflation in the subsequent year. The policy is thus supposed to be completely symmetrical.

I belief that the ECB would indeed be able to achieve higher inflation rates consistent with such a price level target if it were to engage in Quantitative Easing (anything in between 40 and 80 billion Euros a month might be sufficient). I especially liked the proposal by Jeffrey Frankel. He suggested that instead of buying European government bonds, which could be seen as bailing out specific European nations, the ECB should buy American government bonds instead. This would also lead to a lower value of the Euro, which is desperately needed to restore competiveness of the periphery countries (see here: http://www.project-syndicate.org/commentary/jeffrey-frankel-urges-the-ecb-to-buy-us-treasuries-to-expand-the-monetary-base).

So the ECB should finally act and achieve a higher inflation rate in the Eurozone. Note that when I (or Ben Bernanke for that matter) call for higher prices, then what I obviously want is higher aggregate demand. It is extremely important for the health of the Eurozone that the ECB responds to the fall in NGDP, which is the main culprit of the economic crisis. Unfortunately, I don’t see it happening. The last couple of months made it abundantly clear that the ECB does not care about falling AD or even price stability, which is a clear violation of its mandate. The Bank of Japan pursued tight monetary policy for almost two decades and the ECB seems to be all too eager to follow in their footsteps.

So the ECB should finally act and achieve a higher inflation rate in the Eurozone. Note that when I (or Ben Bernanke for that matter) call for higher prices, then what I obviously want is higher aggregate demand. It is extremely important for the health of the Eurozone that the ECB responds to the fall in NGDP, which is the main culprit of the economic crisis. Unfortunately, I don’t see it happening. The last couple of months made it abundantly clear that the ECB does not care about falling AD or even price stability, which is a clear violation of its mandate. The Bank of Japan pursued tight monetary policy for almost two decades and the ECB seems to be all too eager to follow in their footsteps.

RSS Feed

RSS Feed