And it happened again that I have been reading something that I find very upsetting. In recent times it has become a very popular trend for newspapers to spread the notion that Central Banks are creating asset bubbles everywhere by ‘artificially’ keeping the interest rate low. Not only is this idea very wrong, but also potentially very dangerous as Central Bankers face political pressure to tighten monetary policy prematurely, thus killing off any prospect of economic recovery.

I will not explain in this post why Central Banks actually cannot keep the nominal rate of interest below the natural rate (also called the Wicksellian rate) for a longer period without causing rising inflation, and eventually hyperinflation.

Rather I will focus in this post on the idea of how Central Bankers are supposedly creating new ‘bubbles’.

For this purpose, lets look at how Robert Shiller defines a ‘bubble’. We can rightly assume that he is actually an expert on this topic: Not only for receiving the Nobel Prize for his work on how asset market might indeed sometimes display signs of irrationality, but also for actually correctly identifying both the ‘Dot-Com bubble’ of the early 2000s and the ‘Housing Bubble’ afterwards.

In this post, he gives his formal definition of a bubble (http://www.project-syndicate.org/commentary/the-never-ending-struggle-with-speculative-bubbles-by-robert-j--shiller#Pf4GRqVkxuXi1LYa.99):

I will not explain in this post why Central Banks actually cannot keep the nominal rate of interest below the natural rate (also called the Wicksellian rate) for a longer period without causing rising inflation, and eventually hyperinflation.

Rather I will focus in this post on the idea of how Central Bankers are supposedly creating new ‘bubbles’.

For this purpose, lets look at how Robert Shiller defines a ‘bubble’. We can rightly assume that he is actually an expert on this topic: Not only for receiving the Nobel Prize for his work on how asset market might indeed sometimes display signs of irrationality, but also for actually correctly identifying both the ‘Dot-Com bubble’ of the early 2000s and the ‘Housing Bubble’ afterwards.

In this post, he gives his formal definition of a bubble (http://www.project-syndicate.org/commentary/the-never-ending-struggle-with-speculative-bubbles-by-robert-j--shiller#Pf4GRqVkxuXi1LYa.99):

In the second edition of my book Irrational Exuberance, I tried to give a better definition of a bubble. A “speculative bubble,” I wrote then, is “a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, in the process amplifying stories that might justify the price increase.” This attracts “a larger and larger class of investors, who, despite doubts about the real value of the investment, are drawn to it partly through envy of others’ successes and partly through a gambler’s excitement.”

So according to Shiller, ‘asset bubbles’ are a psychological phenomenon. They occur in a positive economic environment characterized by economic growth and large increases the price of the particular asset that turns out to be ‘bubble’. The average investor is overconfident and there is a high degree of enthusiasm as prices (of the asset) increase continuously. Note that in such an environment, even investors who correctly belief that prices have diverged significantly from fundamentals might find it rational to ride the bubble for two reasons. First, they might think that they are better at timing the market than the average investor, thus being able to leave the party just before the shit hits the fan. Second, going short on the bubble might prove to be a very risky bet as asset prices could further diverge from fundamentals for a longer period of time before eventually falling. In the meantime, any investor going short the particular asset might loose huge amounts of money and eventually run out of liquidity.

So here is my question: Has there been a large degree of enthusiasm or overconfidence in the economy over the last couple of years?

I don’t think so! With unemployment in the Eurozone being above 12%, with nominal GDP below its value in 2007, with Europe’s economic performance now being worse than during the Great Depression in the 1930s, with record-low inflation levels, with basically no signs of recovery, I really do not see an economic environment prone to asset bubbles (or am I missing something?).

Of course, all else equal, lower interest rates by Central Banks imply an increase in asset prices. But this is SUPPOSED to happen. One of the channels of monetary policy is the wealth effect (it is, however, by far not the most important channel!).

Central Banks can affect a variety of asset prices (even at the Zero-lower bound). Higher stock markets and housing prices imply that consumers are wealthier and they will thus increase consumption.

Higher asset prices as a result of lower interest rates, however, do by no means indicate the existence of a bubble! Remember that the fundamental value of a stock is simply the present value of all expected future dividends. A lower (real) interest rate thus implies that all expected future dividends are discounted by less, thus raising the present value of the stock. All else equal, lowering the interest will thus increase stock prices (and this has nothing to do at all with bubbles!) whereas increasing the interest rate will depress the stock market.

Similarly, the ‘user cost’ of housing decreases when the (real) rate of interest falls (that is because the real rate of interest represents the opportunity cost to the house owner). A lower user cost means higher housing demand. With the stock of housing being fixed in the short-run, higher demand implies higher housing prices. All else equal, lowering the rate of interest will thus increase the price of housing (conversely, increasing the rate of interest will decrease the price of housing).

Asset prices such as stocks, bonds, and also houses thus naturally move in the opposite direction as changes in the real interest rate. Lower interest rates thus will increase prices for a variety of assets, but this does not reflect ‘bubbly behavior’ in any way!

Anyone putting forward the idea that low interest rates cause bubbles, such as the author of this article (in German: http://www.spiegel.de/wirtschaft/soziales/notenbanken-henrik-mueller-ueber-die-angst-vor-der-dauerkrise-a-936679.html), must really do the following things:

First, such a person has to put forward an economic model that can explain how bubbles supposedly can be created in an economic environment characterized by low-interest rates (and thus tight money), low economic growth, low confidence, low inflation, and pessimistic expectations about the future.

Second, this person actually has to provide some reasonable empirical evidence that assets are overvalued and that prices have significantly diverged from fundamentals.

So how does it look like when one actually looks at the numbers? Is there any evidence of a potential housing bubble in Germany?

All the following graphs are from the Economist’s house price index, available here:

(http://www.economist.com/blogs/dailychart/2011/11/global-house-prices)

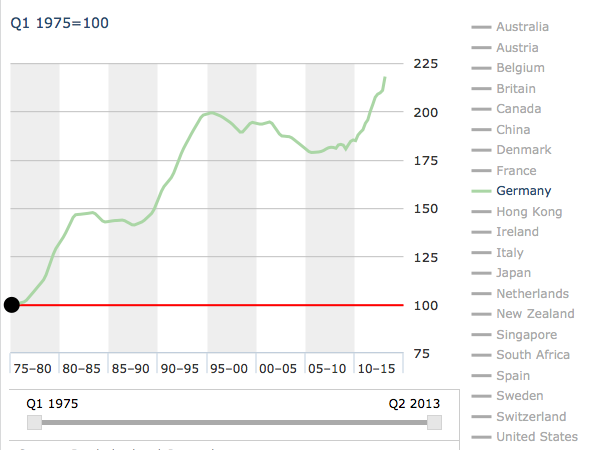

Germany – nominal house prices

So here is my question: Has there been a large degree of enthusiasm or overconfidence in the economy over the last couple of years?

I don’t think so! With unemployment in the Eurozone being above 12%, with nominal GDP below its value in 2007, with Europe’s economic performance now being worse than during the Great Depression in the 1930s, with record-low inflation levels, with basically no signs of recovery, I really do not see an economic environment prone to asset bubbles (or am I missing something?).

Of course, all else equal, lower interest rates by Central Banks imply an increase in asset prices. But this is SUPPOSED to happen. One of the channels of monetary policy is the wealth effect (it is, however, by far not the most important channel!).

Central Banks can affect a variety of asset prices (even at the Zero-lower bound). Higher stock markets and housing prices imply that consumers are wealthier and they will thus increase consumption.

Higher asset prices as a result of lower interest rates, however, do by no means indicate the existence of a bubble! Remember that the fundamental value of a stock is simply the present value of all expected future dividends. A lower (real) interest rate thus implies that all expected future dividends are discounted by less, thus raising the present value of the stock. All else equal, lowering the interest will thus increase stock prices (and this has nothing to do at all with bubbles!) whereas increasing the interest rate will depress the stock market.

Similarly, the ‘user cost’ of housing decreases when the (real) rate of interest falls (that is because the real rate of interest represents the opportunity cost to the house owner). A lower user cost means higher housing demand. With the stock of housing being fixed in the short-run, higher demand implies higher housing prices. All else equal, lowering the rate of interest will thus increase the price of housing (conversely, increasing the rate of interest will decrease the price of housing).

Asset prices such as stocks, bonds, and also houses thus naturally move in the opposite direction as changes in the real interest rate. Lower interest rates thus will increase prices for a variety of assets, but this does not reflect ‘bubbly behavior’ in any way!

Anyone putting forward the idea that low interest rates cause bubbles, such as the author of this article (in German: http://www.spiegel.de/wirtschaft/soziales/notenbanken-henrik-mueller-ueber-die-angst-vor-der-dauerkrise-a-936679.html), must really do the following things:

First, such a person has to put forward an economic model that can explain how bubbles supposedly can be created in an economic environment characterized by low-interest rates (and thus tight money), low economic growth, low confidence, low inflation, and pessimistic expectations about the future.

Second, this person actually has to provide some reasonable empirical evidence that assets are overvalued and that prices have significantly diverged from fundamentals.

So how does it look like when one actually looks at the numbers? Is there any evidence of a potential housing bubble in Germany?

All the following graphs are from the Economist’s house price index, available here:

(http://www.economist.com/blogs/dailychart/2011/11/global-house-prices)

Germany – nominal house prices

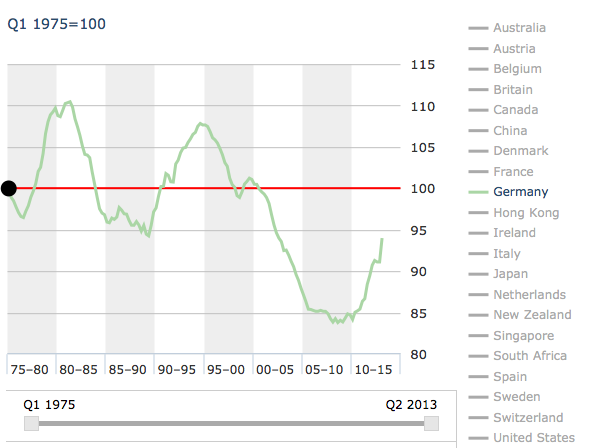

Germany – real house prices

One can see that German house prices have indeed increased both in nominal as well as in real terms (inflation adjusted) since 2010. However, the change in German house prices really does not seem to be that dramatic. On the website of the Economist you can actually check out that Germany is the only country besides Japan in which real house prices are currently lower than in the 1970s! Houses in Germany as an asset class thus did not even manage to protect investors from inflation. Including some other Eurozone countries, one can see that the alleged ‘German housing bubble’ really does not jump out of the picture.

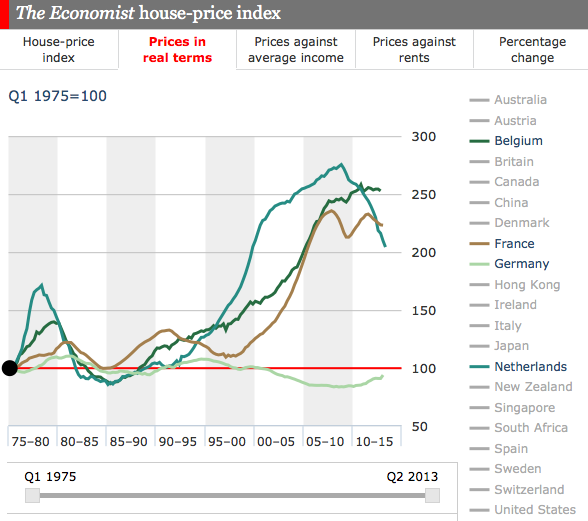

Real house prices

Real house prices

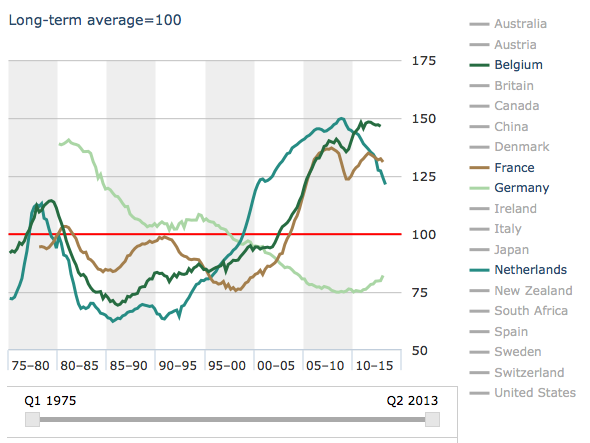

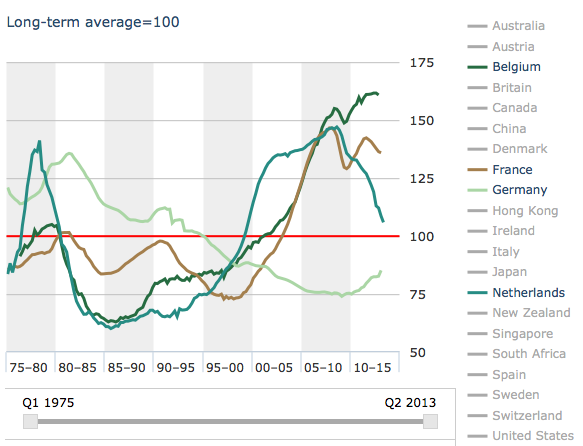

Obviously, house prices can only get us so far and really do not tell us the entire story. We cannot evaluate to what extent house prices actually diverged from fundamentals. The following two measures, however, suggest that house prices in Germany are in general comparatively low. More specifically, we see that German house prices as measured against average income and average rents are actually far lower than in other Eurozone countries.

House prices against average income

House prices against average income

House prices against average rents

All the indices above consider the German housing market as one entire entity. Obviously, this is somewhat false and some of the bigger cities in Germany (Cologne, Berlin, Hamburg, etc.) have indeed seen far bigger rises in the price of housing than rural areas. The figures above nonetheless suggest that the fear of a ‘German housing bubble’ is largely exaggerated.

Note also that all countries that experienced a so-called housing bubble over the last couple of years actually were huge net importers of capital (Spain, Ireland, U.S., etc.). I have explained in an earlier post how Germany has actually been running persistent account surpluses for many years now. Germany is thus a net exporter of capital, again indicating that the fear of excessive inflows of foreign capital fueling a domestic housing bubble cannot be confirmed by the data.

So what about the stock market?

In recent months we have repeatedly been warned that the German DAX is at all-time high and might thus soon drop significantly.

My response to that kind of nonsense is that these doomsayers don’t really know what they are talking about. Stock markets are nominal indices (exactly as nominal GDP). We expect the DAX to be higher today than 20 years ago just as German GDP today is much higher than 20 years. Comparing the nominal value of the DAX today with the nominal value of the DAX in the past and concluding that there is a bubble based on this observation is meaningless!

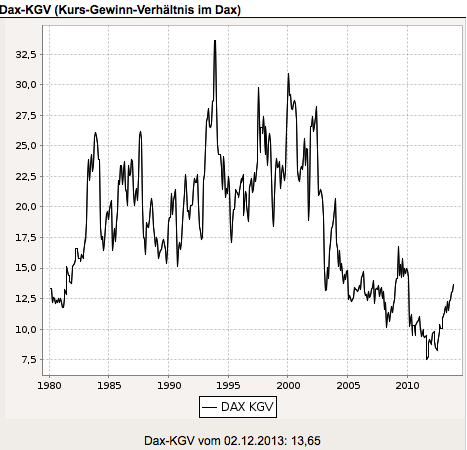

One should rather focus on the Price-earnings (PE) ratio of the DAX to evaluate whether it might be under- or overvalued. The following chart clearly illustrates that the DAX as of today is clearly very cheap in comparison with historical values, despite being at an all-time high (in nominal terms)! The PE ratio is still fairly low and clearly below average when looking at the last 30 years. It is not unreasonable to assume that in the long-run the PE ratio will return to its historical mean. Based on mean-reversion, we should thus expect the PE ratio to increase over the next couple of years. This can only happen in two ways. With earnings per share staying constant, the PE ratio can only rise if the value of the shares increases even further, implying an even higher value of the DAX! Alternatively, the PE ratio could fall with earnings per share decreasing (this could happen if economic conditions deteriorate again).

It should be clear that the DAX is by no means overvalued when evaluated against historical values of the PE ratio. The idea of a bubble thus seems to be more than farfetched.

Note also that all countries that experienced a so-called housing bubble over the last couple of years actually were huge net importers of capital (Spain, Ireland, U.S., etc.). I have explained in an earlier post how Germany has actually been running persistent account surpluses for many years now. Germany is thus a net exporter of capital, again indicating that the fear of excessive inflows of foreign capital fueling a domestic housing bubble cannot be confirmed by the data.

So what about the stock market?

In recent months we have repeatedly been warned that the German DAX is at all-time high and might thus soon drop significantly.

My response to that kind of nonsense is that these doomsayers don’t really know what they are talking about. Stock markets are nominal indices (exactly as nominal GDP). We expect the DAX to be higher today than 20 years ago just as German GDP today is much higher than 20 years. Comparing the nominal value of the DAX today with the nominal value of the DAX in the past and concluding that there is a bubble based on this observation is meaningless!

One should rather focus on the Price-earnings (PE) ratio of the DAX to evaluate whether it might be under- or overvalued. The following chart clearly illustrates that the DAX as of today is clearly very cheap in comparison with historical values, despite being at an all-time high (in nominal terms)! The PE ratio is still fairly low and clearly below average when looking at the last 30 years. It is not unreasonable to assume that in the long-run the PE ratio will return to its historical mean. Based on mean-reversion, we should thus expect the PE ratio to increase over the next couple of years. This can only happen in two ways. With earnings per share staying constant, the PE ratio can only rise if the value of the shares increases even further, implying an even higher value of the DAX! Alternatively, the PE ratio could fall with earnings per share decreasing (this could happen if economic conditions deteriorate again).

It should be clear that the DAX is by no means overvalued when evaluated against historical values of the PE ratio. The idea of a bubble thus seems to be more than farfetched.

The punch line of this post is that people (and Central Banks!) should stop worrying about bubbles. It is very likely that under current circumstances there are really no bubbles out there. Central Banks should thus really focus on bringing our economies back to full employment and stabilizing inflation (at the 2% target). They have neglected both in recent years and the associated economic costs have been enormous.

For a very contrarian view to mine read Roubini (in my opinion nonsense though!): http://www.project-syndicate.org/commentary/nouriel-roubini-warns-that-policymmakers-are-powerless-to-rein-in-frothy-housing-markets-around-the-world

He believes that there are currently signs of housing bubbles everywhere:

For a very contrarian view to mine read Roubini (in my opinion nonsense though!): http://www.project-syndicate.org/commentary/nouriel-roubini-warns-that-policymmakers-are-powerless-to-rein-in-frothy-housing-markets-around-the-world

He believes that there are currently signs of housing bubbles everywhere:

Now, five years later, signs of frothiness, if not outright bubbles, are reappearing in housing markets in Switzerland, Sweden, Norway, Finland, France, Germany, Canada, Australia, New Zealand, and, back for an encore, the UK (well, London). In emerging markets, bubbles are appearing in Hong Kong, Singapore, China, and Israel, and in major urban centers in Turkey, India, Indonesia, and Brazil.

He also repeatedly warned of bubbles both before and after the crisis! Note how these kinds of predictions are totally useless! Of course, sooner or later in one of these countries housing prices will fall, thus “proving him right”. But this is only because this is bound to happen! Any asset will experience sooner or later a fall in its price. It’s like me predicting that by the end of this year it is going to snow somewhere in Germany (I am very confident that my prediction will turn out to be correct)! Asset prices are inherently very volatile. Large price increases with subsequent falls do not in any way prove the existence of bubbles!

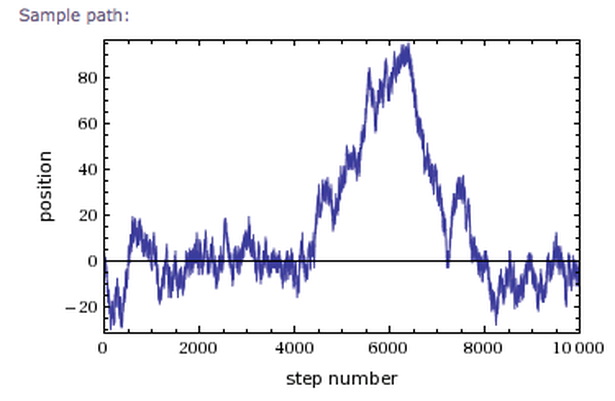

Finally, look at the next two charts. The following is showing a nice bubble, right? Notice the huge increase followed by the subsequent decline?

Finally, look at the next two charts. The following is showing a nice bubble, right? Notice the huge increase followed by the subsequent decline?

Wrong!!! It’s just a random walk with 10 000 steps created on http://www.wolframalpha.com/. Remember how a random walk is designed as having a 50% probability of going either up or down at each step. Then, by design, it cannot be a bubble even though it looks like one to the human eye!

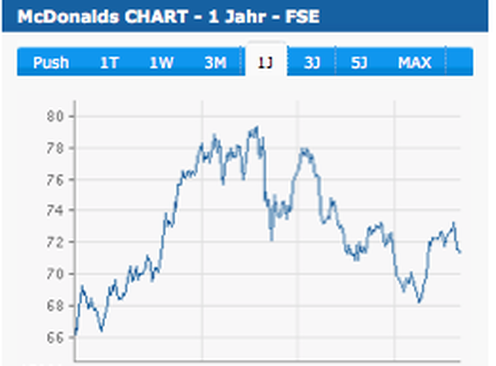

We know that stocks actually behave very similar to random walks (that’s why future stock prices are unpredictable). Compare the random walk above with the stock chart of McDonald’s.

We know that stocks actually behave very similar to random walks (that’s why future stock prices are unpredictable). Compare the random walk above with the stock chart of McDonald’s.

Any single stock, as well the entire index, look very similar to random walks, which can display huge price increases followed by sharp subsequent declines. This, however, just reflects random behavior even though the human eye cannot accept it. My point is that many things that look like bubbles actually are not bubbles. I do not deny here the existence of bubbles, but they are actually much more rare than commonly assumed! Roubini’s assessment of bubbles all over the world is in my view very ridiculous.

If everyone thinks that something is a bubble, there is about a 99.99% chance that it’s actually not a bubble! If, on the other hand, some unusual asset increases SIGNIFICANTLY (let’s just say Dutch Tulips, or stocks of Internet companies that do not yet produce anything, have no business model, etc.), and EVERYONE strongly beliefs that all of the change in price is related to fundamentals, then there is much more reason to actually be concerned!

If everyone thinks that something is a bubble, there is about a 99.99% chance that it’s actually not a bubble! If, on the other hand, some unusual asset increases SIGNIFICANTLY (let’s just say Dutch Tulips, or stocks of Internet companies that do not yet produce anything, have no business model, etc.), and EVERYONE strongly beliefs that all of the change in price is related to fundamentals, then there is much more reason to actually be concerned!

RSS Feed

RSS Feed