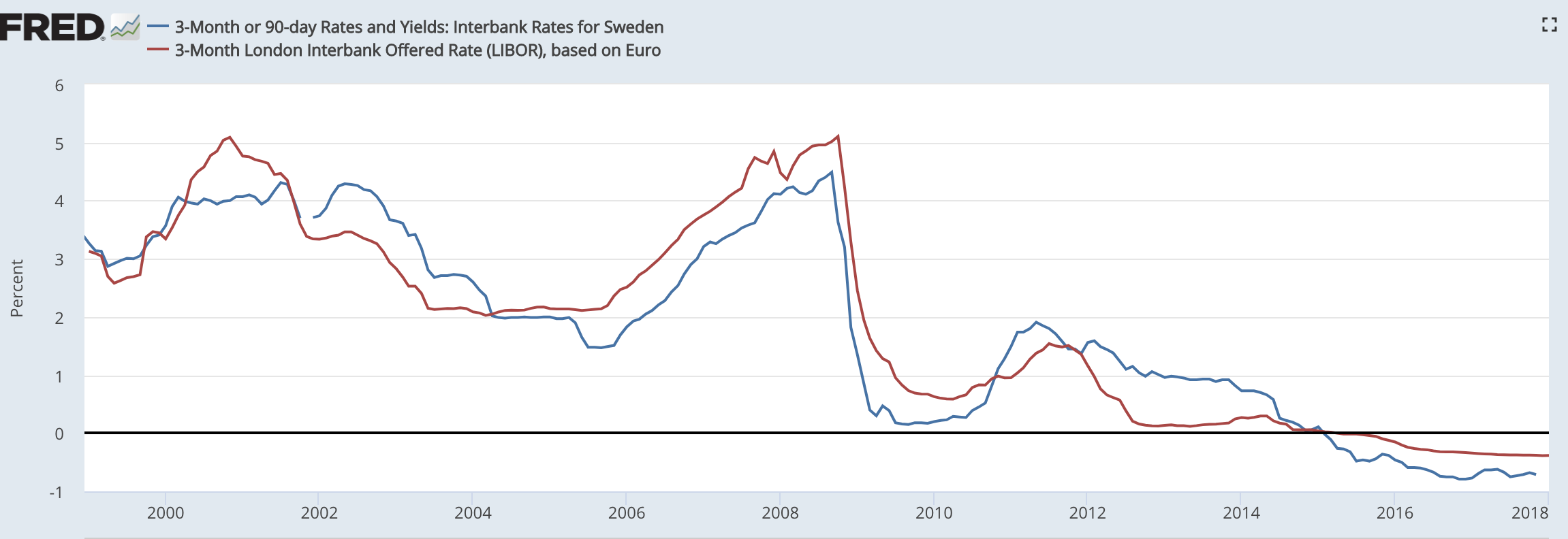

I am currently doing some work on real interest rates, trying to figure out to what extent real interest rates are determined by international macroeconomic conditions instead of domestic factors. The answer, not very surprisingly, is that especially nowadays in times of relatively high capital mobility real interest rates are mostly determined by international factors. The chart below shows the 3-month interbank rate for Swedish banks as well as the similar rate for Eurozone banks. The two interest rates show an enormous amount of co-movement. In fact, the correlation coefficient between the two time series is more than 93%.

Central Banks say that they set interest rates and financial news commonly make a similar claim. In reality, however, that is not really what's going on. Yes, on any given day the ECB has the control to increase its benchmark rate by let's say 25 basis points or more. However, in reality the interest rate is determined by macroeconomic conditions, domestic factors but also international factors, especially in the case of a small open economy like Sweden.

So saying that Central Banks have kept down their benchmark interest rate close to zero or even negative for almost a decade in the aftermath of the crisis is actually quite misleading. The Fed, the ECB, and the BOJ really had no other choice than to reduce their benchmark rate to such low rates and to keep it there for many years as economic conditions simply did not warrant a premature tightening.

It is now quite clear that the US business cycle is in a more mature stage than the European recovery and economic conditions allowed the Fed to increase its interest rate to about 1.25% as of now. Moreover, financial markets are actually pricing in some 3 to 4 more rate hikes this year, meaning that interest rates will approach about 2% by the end of 2018 while they are effectively still below zero in Europe as of right now. However, as I have argued earlier, interest rates are partially determined by international factors and Eurozone interest rates cannot decouple forever. It seems quite likely that after the end of QE, which is supposedly ending in September of this year, the ECB will also be able to start its tightening cycle in 2019. Expect the Swedish Riksbank to follow the ECB's rate rate decision quite closely. To sum up, while Central Banks have quite powerful control of domestic nominal demand, i.e. NGDP, they actually have little control over real interest rates, which are endogenous to domestic and international macroeconomic conditions.

So saying that Central Banks have kept down their benchmark interest rate close to zero or even negative for almost a decade in the aftermath of the crisis is actually quite misleading. The Fed, the ECB, and the BOJ really had no other choice than to reduce their benchmark rate to such low rates and to keep it there for many years as economic conditions simply did not warrant a premature tightening.

It is now quite clear that the US business cycle is in a more mature stage than the European recovery and economic conditions allowed the Fed to increase its interest rate to about 1.25% as of now. Moreover, financial markets are actually pricing in some 3 to 4 more rate hikes this year, meaning that interest rates will approach about 2% by the end of 2018 while they are effectively still below zero in Europe as of right now. However, as I have argued earlier, interest rates are partially determined by international factors and Eurozone interest rates cannot decouple forever. It seems quite likely that after the end of QE, which is supposedly ending in September of this year, the ECB will also be able to start its tightening cycle in 2019. Expect the Swedish Riksbank to follow the ECB's rate rate decision quite closely. To sum up, while Central Banks have quite powerful control of domestic nominal demand, i.e. NGDP, they actually have little control over real interest rates, which are endogenous to domestic and international macroeconomic conditions.

RSS Feed

RSS Feed