Rules vs. discretion

Ever since the beginning of the Financial Crisis, Central Bankers all around the world have been acting highly discretionary. The FED, for example, pursued massive amounts of Quantitative Easing (QE) over the last few years, that is purchases of government bonds and other financial assets. The QE3 program started out with monthly asset purchases in the amount of 85$ billion dollars in December 2012. Due to the tapering, this amount has been steadily reduced over the last year, but still remains at currently 35 billion $ per month as of July 2014. There is overwhelming evidence that these decisive actions initiated by the FED have been highly stimulative to the U.S. economy. Consequently, the U.S. avoided a second Great Depression and the recovery has been much more robust than in the Eurozone despite similar amounts of fiscal austerity.

Other Central Banks, such as the Bank of Japan (BOJ) and the Bank of England, also have been highly accommodative and provided similar programs of monetary easing to stimulate their economies. The first pillar of Abenomics, the monetary stimulus program enacted by the BOJ, has also been highly successful. The Japanese economy suffered from two decades of very low inflation and even deflation after the burst of the two bubbles (stocks and real estate) in the beginning of the 90s. By finally deciding on a ‘whatever it takes’ approach, basically following Paul Krugman’s advice two decades after he gave it, the Bank of Japan started to initiate a very large asset purchase program (large compared to the size of the Japanese economy) in order to end deflation and stimulate the economy. Consequently, Japan was the fastest growing large industrialized country in the world with a real GDP growth rate of 1.4% and 1.5% in 2012 and 2013, respectively. The stimulus was only potent, of course, because Japan suffered from a very large output gap (the difference between actual and potential GDP) after the financial crisis. Once the economy closes in on potential output, monetary stimulus will become ineffective in boosting real growth and will only lead to higher prices. A somewhat higher inflation rate will, however, not be a bad thing and is actually desperately needed in Japan to erode somewhat the real burden of government debt, which is the highest in the world with about 240% of GDP.

There should be no doubt that monetary stimulus was desperately needed in most industrialized countries over the last few years as most industrialized countries suffered from enormous output gaps. Central Bankers have enormous powers as monetary policy potentially influences the life of millions of people. This is made painfully clear when comparing the economic performance of the Eurozone with that of the U.S. in recent years. Given the importance of monetary policy, there is reasonable room for debate on whether monetary policy really should be left at the discretion of the Central Banker. Some macroeconomists thus have argued in recent years that monetary policy should be ‘rule-based’ rather than discretionary, that is, Central Bankers strictly would have to follow some kind of monetary policy rule without the authority to deviate from it.

The idea of ‘rule-based’ monetary policy is actually relatively old. Milton Friedman proposed constant money growth rule: the Central Bank would simply increase the monetary base by the same percentage increase year after year (let’s say 6%, for example). Assuming a constant money multiplier (the ratio between base money and the broader money supply), Friedman’s rule would ensure a stable growth rate of the broader money supply, which includes bank deposits. Alternatively, Central Banks could target directly broader measures of money instead of the monetary base.

The German Bundesbank actually adopted a money-targeting regime in the 1970s. However, it never adhered to this regime in the very strict sense and rather focused on inflation rates when the price changes and money growth changes were incompatible. That is because Friedman’s proposal solely ensures a stable supply of money as he assumed that the demand for money is relatively stable. However, money demand can indeed fluctuate substantially. This is especially the case in time of crises such as after 2007. A constant money growth rule thus does not manage to stabilize nominal income (nominal GDP) when the demand for money is unstable.

An alternative proposal that has enormously gained momentum over the last few years is ‘nominal GDP level targeting’ (NGDPLT). NGDPLT is a rule-based policy under which the Central Bank would simply target nominal income around a certain trend level, such as a 5% increase on a yearly basis. The idea behind this proposal is, of course, to eliminate fluctuations in aggregate demand. There are a lot of theoretical reasons, which suggest that a NGDP targeting regime would significantly outperform the current practice of inflation targeting with respect to the management of the business cycle.

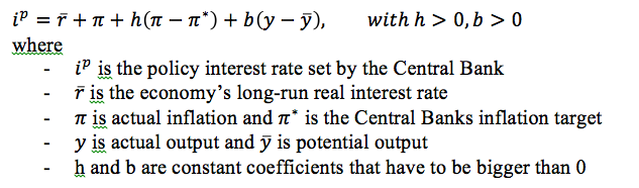

Another big adherent of rule-based monetary policy is John Taylor from Stanford University who favors the so-called ‘Taylor rule’ named after him. According to the Taylor rule, Central Banks should adjust their interest rates in reaction to observed deviations of inflation and output from target. Mathematically, the Taylor rule can be expressed as follows:

Ever since the beginning of the Financial Crisis, Central Bankers all around the world have been acting highly discretionary. The FED, for example, pursued massive amounts of Quantitative Easing (QE) over the last few years, that is purchases of government bonds and other financial assets. The QE3 program started out with monthly asset purchases in the amount of 85$ billion dollars in December 2012. Due to the tapering, this amount has been steadily reduced over the last year, but still remains at currently 35 billion $ per month as of July 2014. There is overwhelming evidence that these decisive actions initiated by the FED have been highly stimulative to the U.S. economy. Consequently, the U.S. avoided a second Great Depression and the recovery has been much more robust than in the Eurozone despite similar amounts of fiscal austerity.

Other Central Banks, such as the Bank of Japan (BOJ) and the Bank of England, also have been highly accommodative and provided similar programs of monetary easing to stimulate their economies. The first pillar of Abenomics, the monetary stimulus program enacted by the BOJ, has also been highly successful. The Japanese economy suffered from two decades of very low inflation and even deflation after the burst of the two bubbles (stocks and real estate) in the beginning of the 90s. By finally deciding on a ‘whatever it takes’ approach, basically following Paul Krugman’s advice two decades after he gave it, the Bank of Japan started to initiate a very large asset purchase program (large compared to the size of the Japanese economy) in order to end deflation and stimulate the economy. Consequently, Japan was the fastest growing large industrialized country in the world with a real GDP growth rate of 1.4% and 1.5% in 2012 and 2013, respectively. The stimulus was only potent, of course, because Japan suffered from a very large output gap (the difference between actual and potential GDP) after the financial crisis. Once the economy closes in on potential output, monetary stimulus will become ineffective in boosting real growth and will only lead to higher prices. A somewhat higher inflation rate will, however, not be a bad thing and is actually desperately needed in Japan to erode somewhat the real burden of government debt, which is the highest in the world with about 240% of GDP.

There should be no doubt that monetary stimulus was desperately needed in most industrialized countries over the last few years as most industrialized countries suffered from enormous output gaps. Central Bankers have enormous powers as monetary policy potentially influences the life of millions of people. This is made painfully clear when comparing the economic performance of the Eurozone with that of the U.S. in recent years. Given the importance of monetary policy, there is reasonable room for debate on whether monetary policy really should be left at the discretion of the Central Banker. Some macroeconomists thus have argued in recent years that monetary policy should be ‘rule-based’ rather than discretionary, that is, Central Bankers strictly would have to follow some kind of monetary policy rule without the authority to deviate from it.

The idea of ‘rule-based’ monetary policy is actually relatively old. Milton Friedman proposed constant money growth rule: the Central Bank would simply increase the monetary base by the same percentage increase year after year (let’s say 6%, for example). Assuming a constant money multiplier (the ratio between base money and the broader money supply), Friedman’s rule would ensure a stable growth rate of the broader money supply, which includes bank deposits. Alternatively, Central Banks could target directly broader measures of money instead of the monetary base.

The German Bundesbank actually adopted a money-targeting regime in the 1970s. However, it never adhered to this regime in the very strict sense and rather focused on inflation rates when the price changes and money growth changes were incompatible. That is because Friedman’s proposal solely ensures a stable supply of money as he assumed that the demand for money is relatively stable. However, money demand can indeed fluctuate substantially. This is especially the case in time of crises such as after 2007. A constant money growth rule thus does not manage to stabilize nominal income (nominal GDP) when the demand for money is unstable.

An alternative proposal that has enormously gained momentum over the last few years is ‘nominal GDP level targeting’ (NGDPLT). NGDPLT is a rule-based policy under which the Central Bank would simply target nominal income around a certain trend level, such as a 5% increase on a yearly basis. The idea behind this proposal is, of course, to eliminate fluctuations in aggregate demand. There are a lot of theoretical reasons, which suggest that a NGDP targeting regime would significantly outperform the current practice of inflation targeting with respect to the management of the business cycle.

Another big adherent of rule-based monetary policy is John Taylor from Stanford University who favors the so-called ‘Taylor rule’ named after him. According to the Taylor rule, Central Banks should adjust their interest rates in reaction to observed deviations of inflation and output from target. Mathematically, the Taylor rule can be expressed as follows:

Empirically, it has been found that many Central Banks, such as the FED, have followed a Taylor rule very closely during the ‘Great Moderation’, the period from the mid-1980s up to 2007. This period was characterized by high economic stability, that is, low output and low inflation variability. Obviously, society cares about high variability of inflation and output. Central Bankers successfully managed to keep inflation and output deviations from target within reasonable limits exactly because they roughly acted in accordance with a Taylor rule, so the narrative. The Taylor rule approach thus led to a de facto stabilization of nominal GDP and prices.

However, some economists now question whether the ‘Great Moderation’ has really been a period of high economic stability thanks to competent Central Bankers or whether we just got lucky. Indeed, there is some evidence that the U.S. (and other countries) experienced rather small supply and demand shocks from the late 80s onwards. According to this view, inflation targeting or even a Taylor rule approach was only successful because economies experienced a period of high stability without being exposed to large exogenous shocks (supply or demand). Read this paper for more: http://mercatus.org/publication/inflation-targeting-monetary-policy-regime-whose-time-has-come-and-gone.

In fact, since the mid-2000s, both supply and demand shocks have become more frequent and larger in amplitude (relatively high oil prices in 2008 and 2011, financial crisis, Eurozone crisis, etc.). These events have forcefully demonstrated that Central Banks were unable to respond to these shocks appropriately. Over the last few years it has become rather evident that pure inflation targeting is a suboptimal monetary regime if the ultimate goal is the smoothening of the business cycle. A nominal GDP target is likely to be far superior in that respect for various reasons.

Even a Taylor rule approach, reacting to deviations of both output and inflation from target, is likely to run into problems when exogenous shocks are large. Furthermore, the Taylor rule is subject to the various difficulties on which I will elaborate below.

Problems with the Taylor rule

The first problem associated with the Taylor rule is that it is impossible to accurately measure potential output, the economy’s long-run capacity to produce at stable prices. There are various methods, some more elaborate than others, which economists can use to estimate potential output, but there can be substantial disagreement.

It is now clear that most industrialized countries have been operating substantially below potential since 2008, meaning that both monetary and fiscal stimulus would have been highly effective in boosting output and employment without creating significant inflationary pressures. There was, however, some debate over how large the output gap really was. The inflation hawks at the FED (and the ECB) have argued over the last few years that the economy has been operating close to potential, and have so far been proven wrong. However, there is no doubt that the output gap, if still existent, will soon be closed since it cannot persist indefinitely. The inactivity of European policy makers over the last few years might imply that that potential output might be consistent with 10-12% unemployment in the Eurozone. Due to hysteresis effects, this scenario is likely to be the new normal as policy makers did next to nothing to prevent the now 6-year long and ongoing economic slump.

The second problem also arises from measurement difficulties. It is impossible to directly measure the natural rate of interest (long run real interest rate).

There is significant evidence that the world economy’s real interest rate has been declining quite substantially over the last two decades or so. There are some phenomena that have contributed to that tendency. Most of them are related to Mr. Summers’ ‘secular stagnation’ hypothesis (see here: http://macrothoughts.weebly.com/blog/free-lunches-and-secular-stagnation).

However, some economists now question whether the ‘Great Moderation’ has really been a period of high economic stability thanks to competent Central Bankers or whether we just got lucky. Indeed, there is some evidence that the U.S. (and other countries) experienced rather small supply and demand shocks from the late 80s onwards. According to this view, inflation targeting or even a Taylor rule approach was only successful because economies experienced a period of high stability without being exposed to large exogenous shocks (supply or demand). Read this paper for more: http://mercatus.org/publication/inflation-targeting-monetary-policy-regime-whose-time-has-come-and-gone.

In fact, since the mid-2000s, both supply and demand shocks have become more frequent and larger in amplitude (relatively high oil prices in 2008 and 2011, financial crisis, Eurozone crisis, etc.). These events have forcefully demonstrated that Central Banks were unable to respond to these shocks appropriately. Over the last few years it has become rather evident that pure inflation targeting is a suboptimal monetary regime if the ultimate goal is the smoothening of the business cycle. A nominal GDP target is likely to be far superior in that respect for various reasons.

Even a Taylor rule approach, reacting to deviations of both output and inflation from target, is likely to run into problems when exogenous shocks are large. Furthermore, the Taylor rule is subject to the various difficulties on which I will elaborate below.

Problems with the Taylor rule

The first problem associated with the Taylor rule is that it is impossible to accurately measure potential output, the economy’s long-run capacity to produce at stable prices. There are various methods, some more elaborate than others, which economists can use to estimate potential output, but there can be substantial disagreement.

It is now clear that most industrialized countries have been operating substantially below potential since 2008, meaning that both monetary and fiscal stimulus would have been highly effective in boosting output and employment without creating significant inflationary pressures. There was, however, some debate over how large the output gap really was. The inflation hawks at the FED (and the ECB) have argued over the last few years that the economy has been operating close to potential, and have so far been proven wrong. However, there is no doubt that the output gap, if still existent, will soon be closed since it cannot persist indefinitely. The inactivity of European policy makers over the last few years might imply that that potential output might be consistent with 10-12% unemployment in the Eurozone. Due to hysteresis effects, this scenario is likely to be the new normal as policy makers did next to nothing to prevent the now 6-year long and ongoing economic slump.

The second problem also arises from measurement difficulties. It is impossible to directly measure the natural rate of interest (long run real interest rate).

There is significant evidence that the world economy’s real interest rate has been declining quite substantially over the last two decades or so. There are some phenomena that have contributed to that tendency. Most of them are related to Mr. Summers’ ‘secular stagnation’ hypothesis (see here: http://macrothoughts.weebly.com/blog/free-lunches-and-secular-stagnation).

Potential output and the natural rate of interest are only concepts in the mind of economists and they cannot be observed directly. However, the Taylor rule also relies on the availability of estimates of economic variables (GDP, inflation, etc.) in real time.

Especially, GDP estimates are, however, often substantially revised and the final figure for one quarter is often only available half a year later, or so. This implies that Central Bankers have to use unreliable estimates when making decisions in real-time and are often behind the curve when relying on a Taylor rule approach. This was made painfully clear in the fall of 2008 when the FED was worried about inflation due to temporary high oil prices. The economy, however, was already in free fall and stimulus was desperately needed, but not provided, because of inflation phobia. Forward-looking indicators, such as the stock market, made painfully clear that a big recession was ahead (and the U.S. was actually already in recession in 2008 even though policy makers at the time knew little about it because of data unavailability). The TIPS spread (the difference in yields between inflation-indexed and non-indexed government bonds) indicated that investors in 2008 expected inflation to be far below 2% for the coming years, and this expectation proved to be accurate. For that reason, monetary policy should ultimately be forward-looking. Central Bankers should largely rely on a variety of indicators, which are available in real-time and which can show where the economy is heading and not where it has been.

Last but not least, the Taylor rule becomes useless as guide for economic policy once the economy is hit by very large demand shocks as in 2008.

In the aftermath the financial crisis, the Talor rule prescribed a negative nominal interest for the U.S. and also for the Eurozone for a prolonged period given the large negative output gaps and low rates of inflation (deviation from the 2% target). Obviously, the Central Bank can only reduce its policy rate to zero (the zero lower bound). The Taylor rule is thus useless as a policy guide in times of enormous economic distress. A rule is really not any good if it only provides a policy guideline when the economy functions smoothly. Consequently, the Taylor rule should not be adopted by Central Banks as a strict rule. Policy makers can rely on it as a guideline, but it should not be followed rigidly.

Especially, GDP estimates are, however, often substantially revised and the final figure for one quarter is often only available half a year later, or so. This implies that Central Bankers have to use unreliable estimates when making decisions in real-time and are often behind the curve when relying on a Taylor rule approach. This was made painfully clear in the fall of 2008 when the FED was worried about inflation due to temporary high oil prices. The economy, however, was already in free fall and stimulus was desperately needed, but not provided, because of inflation phobia. Forward-looking indicators, such as the stock market, made painfully clear that a big recession was ahead (and the U.S. was actually already in recession in 2008 even though policy makers at the time knew little about it because of data unavailability). The TIPS spread (the difference in yields between inflation-indexed and non-indexed government bonds) indicated that investors in 2008 expected inflation to be far below 2% for the coming years, and this expectation proved to be accurate. For that reason, monetary policy should ultimately be forward-looking. Central Bankers should largely rely on a variety of indicators, which are available in real-time and which can show where the economy is heading and not where it has been.

Last but not least, the Taylor rule becomes useless as guide for economic policy once the economy is hit by very large demand shocks as in 2008.

In the aftermath the financial crisis, the Talor rule prescribed a negative nominal interest for the U.S. and also for the Eurozone for a prolonged period given the large negative output gaps and low rates of inflation (deviation from the 2% target). Obviously, the Central Bank can only reduce its policy rate to zero (the zero lower bound). The Taylor rule is thus useless as a policy guide in times of enormous economic distress. A rule is really not any good if it only provides a policy guideline when the economy functions smoothly. Consequently, the Taylor rule should not be adopted by Central Banks as a strict rule. Policy makers can rely on it as a guideline, but it should not be followed rigidly.

RSS Feed

RSS Feed