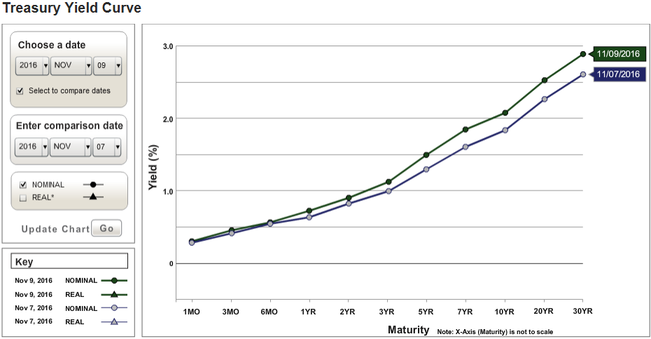

I recently wrote an article for The Conversation on how the yield curve has historically been one of the more reliable predictors of an upcoming recession, especially for the US economy. An inversion of the yield curve means that interest rates on long-term bonds have fallen below short-term interest rates, which tends to happen about one or two years before an economic downturn in the US. For other advanced economies, yield curve inversions also seem to happen before economic slowdowns, but the signal might not be as strong as for the US.

I just saw on Scott Sumner's blog The money illusion a very interesting chart on the US yield curve pre-World War II.

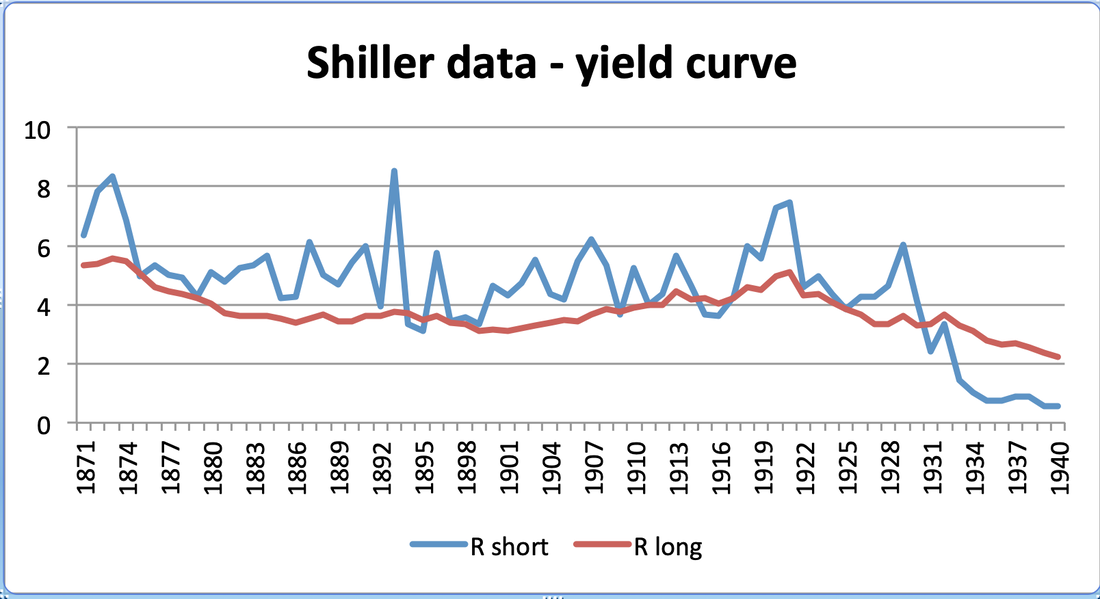

Using Robert Shiller's data, I have reproduced the US yield curve for that time period. And indeed the data suggests that long-term rates were usually below short-term rates for almost the entire time period. While long-term government bonds were available for the entire time period, short-term government bonds didn't exist until the 1930s. For the time period before, interest rates on commercial paper were the best proxy for short-rates. And herein already lies the first problem. Commercial paper is obviously much riskier than short-term government debt, meaning that there can be a substantial risk premium at times, which might explain why short-rates were substantially higher than long-rates for the mentioned time period.

I just saw on Scott Sumner's blog The money illusion a very interesting chart on the US yield curve pre-World War II.

Using Robert Shiller's data, I have reproduced the US yield curve for that time period. And indeed the data suggests that long-term rates were usually below short-term rates for almost the entire time period. While long-term government bonds were available for the entire time period, short-term government bonds didn't exist until the 1930s. For the time period before, interest rates on commercial paper were the best proxy for short-rates. And herein already lies the first problem. Commercial paper is obviously much riskier than short-term government debt, meaning that there can be a substantial risk premium at times, which might explain why short-rates were substantially higher than long-rates for the mentioned time period.

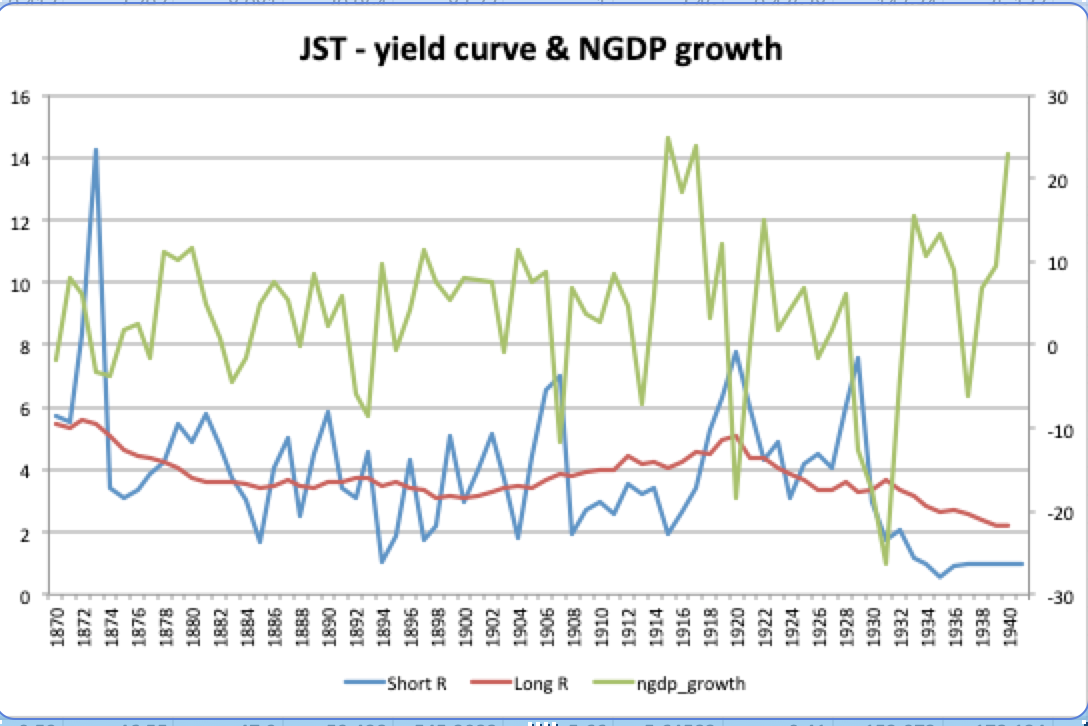

In order to double check this result, I also calculated the US risk premium based on the Jorda, Schularick, and Taylor (JST) Macrohistory database. And big surprise, I get vastly different results. I also included yearly NGDP growth in the chart (axis on the right-hand side).

The chart shows that NGDP growth was highly volatile before WWII and that recessions were a quite common phenomenon. According to the JST, the yield did invert relatively often, but certainly not as often as in the previous data set.

One can see that the long-term interest rate by Shiller and JST are similar, based on historic long-term government bond yields. The short-term rate, on the other hand, is extremely different. There are some 32 inversions during those 70 years in the JST data. While this is still extremely frequent, one should also note that recessions were extremely common at the time and the also featured 21 years of negative nominal GDP growth (real GDP growth might still have been positive at times since the US economy and other advanced economies also experienced moderate deflation during parts of the late 19th century).

While I am not exactly sure to why the two data sources have strikingly different data, there are several potential explanations. First, it might be that one of the series is simply "wrong", meaning an error in the raw data itself. This would be actually quite worrying because I have used the JST data for my own research, such as for my article on global interest rate from 1870 to today. What is more likely though is that the authors have simply used different data sources and different methodologies to construct the short-term interest rate series. While I do not have time for a detailed analysis right now, a more careful study of the appendices of the two data sets would surely reveal why there is such a striking difference. Based on a first look at the data, it looks like JST have used deposit rates for historic short-term interest rates whereas Shiller's data is based on interest rates of commercial paper, which might very well explain the difference.

For now, suffice it to say that you should be extremely careful using macroeconomic data in general, and macroeconomic history data in particular! The quality of the data is arguably extremely poor at times, which is obviously not very surprising.

One can see that the long-term interest rate by Shiller and JST are similar, based on historic long-term government bond yields. The short-term rate, on the other hand, is extremely different. There are some 32 inversions during those 70 years in the JST data. While this is still extremely frequent, one should also note that recessions were extremely common at the time and the also featured 21 years of negative nominal GDP growth (real GDP growth might still have been positive at times since the US economy and other advanced economies also experienced moderate deflation during parts of the late 19th century).

While I am not exactly sure to why the two data sources have strikingly different data, there are several potential explanations. First, it might be that one of the series is simply "wrong", meaning an error in the raw data itself. This would be actually quite worrying because I have used the JST data for my own research, such as for my article on global interest rate from 1870 to today. What is more likely though is that the authors have simply used different data sources and different methodologies to construct the short-term interest rate series. While I do not have time for a detailed analysis right now, a more careful study of the appendices of the two data sets would surely reveal why there is such a striking difference. Based on a first look at the data, it looks like JST have used deposit rates for historic short-term interest rates whereas Shiller's data is based on interest rates of commercial paper, which might very well explain the difference.

For now, suffice it to say that you should be extremely careful using macroeconomic data in general, and macroeconomic history data in particular! The quality of the data is arguably extremely poor at times, which is obviously not very surprising.

RSS Feed

RSS Feed