Step 1:

The world experiences a period of globalization with rapidly increasing trade flows, more migration, larger capital flows, and increasing financialization. This leads to higher economic growth. However, it also increases the level of inequality on the national level in many countries.

Step 2:

A global financial crisis shocks the system.

Step 3:

Government incompetence, and Central Bank incompetence in particular, lead to a large global economic downturn. Slow economic growth and high levels of unemployment exacerbate inequality.

Step 4:

These trends lead to rising nationalism and rising levels of xenophobia across the globe. Extremist parties gain an increasing part of the vote share and perform much better than expected by the “intellectual elite”.

Step 5:

National policies turn increasingly hostile towards globalization. Isolationism and protectionism are suddenly “en vogue”. More and more countries erect barriers against free trade and further restrict migration.

Step 6:

The middle class rejects the liberal ideas of the “intellectual elite” and more and more voters start to embrace populists with open arms.

Step 7:

Voters in one of the major economies elect such a populist as their leader who believes in Jewish conspiracy theories.

Step 8: …?!

History does not quite repeat itself!!! Nevertheless, a careful study of historical events can often be extremely informative as a reference for current and future events. I think that a lot of people, me included, now have to reassess their priors after this week’s event. In my opinion, we have to revise the probability that “something bad” will happen in the coming years significantly upwards. Stock markets have so far not done as badly I expected, to the contrary. After Brexit and the election outcome another prediction miss of mine. To be fair, S&P 500 futures were down initially by almost 10% and global stock markets fell quite significantly at first before making up all their losses and now actually being higher than before the election. Some of it might probably be because the stock market cannot correctly assess Knightian uncertainty. Furthermore, a Republican government is perceived as business friendly. However, Trump is simply a big unknown factor because nobody knows how a Trump administration will exactly look like and what kind of policies such an administration will pursue. Black swan events (low-probability high-impact events) have become much more likely, thus increasing the chance of Keynesian animal spirits. So world, be on the lookout. I certainly will, and so should you!!!

How could we have prevented to get where we are right now?

I believe that a large part of the rising appeal of populism and xenophobia around the world is driven by the extremely poor economic performance advanced economies have experienced over the last decade. Things would be different right now if the lessons of the Great Depression were truly learnt and if economic policy was driven by reason and not ideology. Below a list of policies that governments should have pursued in the aftermath of the crisis:

Expansionary fiscal policy:

Shortly after the crisis most governments turned towards austerity even though economic theory does not back up in any way that governments have to run surpluses or that debt to GDP ratios were too high. In fact, as Larry Summers points out, governments actually now face an incredible arbitrage opportunity by issuing long-term debt at zero real interest rates and investing the money into infrastructure, research, and education, which all have a substantial positive market return and an even higher social return. This would most likely improve the government’s fiscal position instead of deteriorating it. These investments should be a no-brainer in a world where government bond yields are close to zero and public debt is probably too low. However, dysfunctional politics prevents us from doing the sensible thing. Austerity measures in advanced economies have led to depressed economies and rising inequality and are in my opinion a key driver of the rising populism we experience now.

Expansionary monetary policy:

Central Bankers delivered to some extent and prevented another Great Depression by injecting enough liquidity into the system during the financial crisis to ensure a full-blown collapse economic meltdown. However, monetary policy has been contractionary in the years thereafter. Interest rates are not a good indicator of the stance of monetary policy as real interest rates have declined for more than 3 decades. Central Banks failed to engineer sufficiently high levels of nominal GDP that would have prevented the economic stagnation. The current institutional setup of Central Banks with an obsessive focus on the 2% inflation target is partly to blame, which again is not backed up by economic theory. Macroeconomists suggest that Central Banks should have a different monetary framework altogether. Here are monetary policy targets that would perform substantially better than the one we have in place right now, listed in order of optimality:

The world experiences a period of globalization with rapidly increasing trade flows, more migration, larger capital flows, and increasing financialization. This leads to higher economic growth. However, it also increases the level of inequality on the national level in many countries.

Step 2:

A global financial crisis shocks the system.

Step 3:

Government incompetence, and Central Bank incompetence in particular, lead to a large global economic downturn. Slow economic growth and high levels of unemployment exacerbate inequality.

Step 4:

These trends lead to rising nationalism and rising levels of xenophobia across the globe. Extremist parties gain an increasing part of the vote share and perform much better than expected by the “intellectual elite”.

Step 5:

National policies turn increasingly hostile towards globalization. Isolationism and protectionism are suddenly “en vogue”. More and more countries erect barriers against free trade and further restrict migration.

Step 6:

The middle class rejects the liberal ideas of the “intellectual elite” and more and more voters start to embrace populists with open arms.

Step 7:

Voters in one of the major economies elect such a populist as their leader who believes in Jewish conspiracy theories.

Step 8: …?!

History does not quite repeat itself!!! Nevertheless, a careful study of historical events can often be extremely informative as a reference for current and future events. I think that a lot of people, me included, now have to reassess their priors after this week’s event. In my opinion, we have to revise the probability that “something bad” will happen in the coming years significantly upwards. Stock markets have so far not done as badly I expected, to the contrary. After Brexit and the election outcome another prediction miss of mine. To be fair, S&P 500 futures were down initially by almost 10% and global stock markets fell quite significantly at first before making up all their losses and now actually being higher than before the election. Some of it might probably be because the stock market cannot correctly assess Knightian uncertainty. Furthermore, a Republican government is perceived as business friendly. However, Trump is simply a big unknown factor because nobody knows how a Trump administration will exactly look like and what kind of policies such an administration will pursue. Black swan events (low-probability high-impact events) have become much more likely, thus increasing the chance of Keynesian animal spirits. So world, be on the lookout. I certainly will, and so should you!!!

How could we have prevented to get where we are right now?

I believe that a large part of the rising appeal of populism and xenophobia around the world is driven by the extremely poor economic performance advanced economies have experienced over the last decade. Things would be different right now if the lessons of the Great Depression were truly learnt and if economic policy was driven by reason and not ideology. Below a list of policies that governments should have pursued in the aftermath of the crisis:

Expansionary fiscal policy:

Shortly after the crisis most governments turned towards austerity even though economic theory does not back up in any way that governments have to run surpluses or that debt to GDP ratios were too high. In fact, as Larry Summers points out, governments actually now face an incredible arbitrage opportunity by issuing long-term debt at zero real interest rates and investing the money into infrastructure, research, and education, which all have a substantial positive market return and an even higher social return. This would most likely improve the government’s fiscal position instead of deteriorating it. These investments should be a no-brainer in a world where government bond yields are close to zero and public debt is probably too low. However, dysfunctional politics prevents us from doing the sensible thing. Austerity measures in advanced economies have led to depressed economies and rising inequality and are in my opinion a key driver of the rising populism we experience now.

Expansionary monetary policy:

Central Bankers delivered to some extent and prevented another Great Depression by injecting enough liquidity into the system during the financial crisis to ensure a full-blown collapse economic meltdown. However, monetary policy has been contractionary in the years thereafter. Interest rates are not a good indicator of the stance of monetary policy as real interest rates have declined for more than 3 decades. Central Banks failed to engineer sufficiently high levels of nominal GDP that would have prevented the economic stagnation. The current institutional setup of Central Banks with an obsessive focus on the 2% inflation target is partly to blame, which again is not backed up by economic theory. Macroeconomists suggest that Central Banks should have a different monetary framework altogether. Here are monetary policy targets that would perform substantially better than the one we have in place right now, listed in order of optimality:

- Targeting the level of nominal GDP / targeting the level of nominal wages

- Targeting the price level

- A higher inflation target (3-4%)

Fighting inequality:

This should have been a priority even before the financial crisis and should be have been even higher up the list thereafter, but here again governments failed to deliver and now will now have to face the consequences. While globalization has lifted more than a billion people out of poverty in developing countries and has also benefitted advanced economies, not all groups have shared these gains equally. It turns out that a rising tide does not necessarily lift all boats. Here are some policies that have the potential to halt and maybe even revert the recent trends in inequality we have experienced:

UPDATE:

While Trump definitely had support by the angry middle class, it should be noted that the average Trump voter had a much higher median income than the average Clinton voter (http://fivethirtyeight.com/features/the-mythology-of-trumps-working-class-support). In that sense, the Trump victory represents a continuation of the class warfare that has been taken place in recent times. The first order of business of the Trump administration seems to be to repeal the Affordable Care Act, maybe leaving some 20 million people without health insurance. We can also expect a repeal of Dodd-Frank and a return to more liberalized financial markets, which will be great news for banks. Finally, mining companies also have reason to celebrate since a Trump administration will promote resource exploitation, energy production based on natural resources, and probably repeal existing agreements on climate change. In that sense, the recent stock market rise is maybe not that surprising since a Trump administration is great news for big corporations and top income earners. It is the working class that will suffer the most from this election outcome, not to speak of minorities: Just like in Britain after the Brexit vote, attacks on foreigners are already way up in the U.S. as well. Welcome to age of hatred. The 2010s are the new 1930s.

PS: Everybody should bear in mind that Trump was not elected by a majority of Americans. It is the electoral college that has failed for the 6th time in history, 2nd time since 2000, meaning that a candidate will become president who got less votes than his opponent. It’s institutional failure at its best, no doubt about it. http://www.bradford-delong.com/2016/11/electoral-college-fail-number-six.html#more

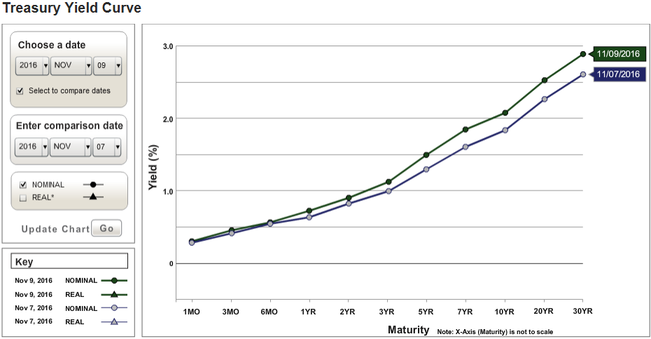

PPS: This is extremely interesting from a financial/macroeconomic point of view. The entire U.S. yield curve has shifted up by a quite significant amount after the Trump win, more so on the long-end of the yield curve (almost 30 basis points for 30-year bonds) than on the short-end (about 10 basis points for 1-year Treasury bills). I am not entirely sure what that exactly means, but note that TIPS spreads are also up by more than 10 basis points. These two facts taken together suggest that financial markets now expect a somewhat higher inflation rate in the years to come. This might actually be good news if the inflation is driven by demand-side factors (i.e. higher nominal spending). It’s obviously bad news if the inflation is driven by supply-side factors. There are reasons to believe that a Trump administration will engage in more military and infrastructure spending, which could actually be mildly stimulatory to the economy, all else equal.

This should have been a priority even before the financial crisis and should be have been even higher up the list thereafter, but here again governments failed to deliver and now will now have to face the consequences. While globalization has lifted more than a billion people out of poverty in developing countries and has also benefitted advanced economies, not all groups have shared these gains equally. It turns out that a rising tide does not necessarily lift all boats. Here are some policies that have the potential to halt and maybe even revert the recent trends in inequality we have experienced:

- Higher marginal tax rates on top income workers

- Higher tax rates on capital income

- Introduction of taxes on land and housing

- Introduction of an inheritance tax

- Introduction of an Earned Income Tax Credit (EITC), basically a wage subsidy for low-income workers: Generally, a well-designed wage subsidy is much preferable to a minimum wage for two reasons. First, an EITC is probably promoting employment at the margin whereas a high enough minimum wage is destroying jobs at the margin. Second, minimum wages are eroded over time with inflation and must therefore be adjusted on a regular basis, but this rarely happens.

- More sensible housing policies: The inelastic supply of housing due to restrictive zoning laws has especially hurt the poor and basically shifted wealth from the bottom to the top by inflating housing prices.

- Subsidize education to a greater extent: Both from an egalitarian point of view as well as in terms of economic efficiency it is highly problematic to live in a world where only the very rich can afford to send their children to top academic institutions because annual tuition fees exceed the yearly income of an average worker.

UPDATE:

While Trump definitely had support by the angry middle class, it should be noted that the average Trump voter had a much higher median income than the average Clinton voter (http://fivethirtyeight.com/features/the-mythology-of-trumps-working-class-support). In that sense, the Trump victory represents a continuation of the class warfare that has been taken place in recent times. The first order of business of the Trump administration seems to be to repeal the Affordable Care Act, maybe leaving some 20 million people without health insurance. We can also expect a repeal of Dodd-Frank and a return to more liberalized financial markets, which will be great news for banks. Finally, mining companies also have reason to celebrate since a Trump administration will promote resource exploitation, energy production based on natural resources, and probably repeal existing agreements on climate change. In that sense, the recent stock market rise is maybe not that surprising since a Trump administration is great news for big corporations and top income earners. It is the working class that will suffer the most from this election outcome, not to speak of minorities: Just like in Britain after the Brexit vote, attacks on foreigners are already way up in the U.S. as well. Welcome to age of hatred. The 2010s are the new 1930s.

PS: Everybody should bear in mind that Trump was not elected by a majority of Americans. It is the electoral college that has failed for the 6th time in history, 2nd time since 2000, meaning that a candidate will become president who got less votes than his opponent. It’s institutional failure at its best, no doubt about it. http://www.bradford-delong.com/2016/11/electoral-college-fail-number-six.html#more

PPS: This is extremely interesting from a financial/macroeconomic point of view. The entire U.S. yield curve has shifted up by a quite significant amount after the Trump win, more so on the long-end of the yield curve (almost 30 basis points for 30-year bonds) than on the short-end (about 10 basis points for 1-year Treasury bills). I am not entirely sure what that exactly means, but note that TIPS spreads are also up by more than 10 basis points. These two facts taken together suggest that financial markets now expect a somewhat higher inflation rate in the years to come. This might actually be good news if the inflation is driven by demand-side factors (i.e. higher nominal spending). It’s obviously bad news if the inflation is driven by supply-side factors. There are reasons to believe that a Trump administration will engage in more military and infrastructure spending, which could actually be mildly stimulatory to the economy, all else equal.

RSS Feed

RSS Feed