I will start this post with a quote from former FED chair Ben Bernanke.

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve System. I would like to say to Milton and Anna: Regarding the Great Depression. You're right, we did it. We're very sorry. But thanks to you, we won't do it again.

(http://en.wikiquote.org/wiki/Ben_Bernanke)

This is what Bernanke said on a conference to Milton Friedman in 2002. With this statement, he obviously refers to Friedman’s extensive studies on U.S. monetary policy during the Great Depression. Friedman asserted, correctly, that the Great Depression was the result of badly designed monetary policy. More specifically, the FED became increasingly worried about a bubble in the stock market in 1928. FED officials thus decided to increase the interest rate sharply in 1928 to curb stock market speculations. The increase in interest rates led to sharp decline in the overall money stock. As a result, the U.S. experienced a downward spiral of falling prices and reductions in aggregate demand (a phenomenon which Irving Fisher dubbed ‘debt deflation’). The plunge in asset prices and the fall in aggregate demand also led to bank failures all over the country. The FED, however, did not prevent these occurrences from happening and neglected its role as lender of last resort.

Friedman’s studies mainly focused on the Great Depression in the U.S. and he neglected the international origin of the Great Depression. In particular, two countries, the U.S. and France started to hoard massive amounts of gold in the late 1920s. This gold hoarding by two Central Banks was the main causes of global deflation during the Great Depression as most countries were on the gold standard at that time (more on that here: http://macrothoughts.weebly.com/1/post/2013/10/how-the-great-depression-was-mainly-caused-by-france-and-the-us.html).

Despite this omission, Friedman was spot on in claiming that the Great Depression in the U.S. was ‘engineered’ by the FED. The economic downturn was the result of a series of policy failures and could have been mostly prevented with superior monetary policy. It turns out that something similar can be said with regard to the Great Recession starting in 2008.

Bernanke was actually one of the leading academics worldwide on monetary policy and the Great Depression before being appointed as chairman of the FED in 2006. Given his expertise and the remarkable quote to Friedman in 2002, it is astonishing that the ‘Bernanke FED’ in 2008 repeated some of the policy mistakes and greatly exacerbated the economic downturn in the U.S. experienced after the financial crisis.

It is standard procedure for the FED to publish the transcripts of the meetings of the Open Market Committee (the board that decides on monetary policy issues) with a five-year delay. A lot of fuss has been made in the last couple of days about these transcripts, and rightly so! I actually had a quick peek at some of the transcripts myself. Some of the reading is quite astonishing, but in a bad way! It turns out that many board members in 2008 were excessively concerned about inflation but did not worry enough about the slowdown in economic activity and the instability in financial markets that occurred at that time.

It is obvious that it is always easier to assess policies in retrospect. Furthermore, macroeconomic data, such as unemployment numbers, real GDP, inflation, etc., always comes in with serious time lags. The FED, however, has to make decisions in real time and is thus seriously constrained by this lack of information. However, the publication of the FED transcripts only shows what many already suspected in the first place. Specifically, many members of the committee did not have a clear understanding of what was going on in 2008 and greatly underestimated the impact the financial crisis would have on the real economy. There was a general belief shared by many FED officials that the economic downturn would turn out to be rather mild.

By contrast, other persons were already much more pessimistic at that time. This is Krugman in January 2008 (http://krugman.blogs.nytimes.com/2008/01/22/deep-maybe-long-probably/?_php=true&_&_r=0&gwh=ABA146B35DFC4F68B917167A93E75A03&gwt=pay):

This is what Bernanke said on a conference to Milton Friedman in 2002. With this statement, he obviously refers to Friedman’s extensive studies on U.S. monetary policy during the Great Depression. Friedman asserted, correctly, that the Great Depression was the result of badly designed monetary policy. More specifically, the FED became increasingly worried about a bubble in the stock market in 1928. FED officials thus decided to increase the interest rate sharply in 1928 to curb stock market speculations. The increase in interest rates led to sharp decline in the overall money stock. As a result, the U.S. experienced a downward spiral of falling prices and reductions in aggregate demand (a phenomenon which Irving Fisher dubbed ‘debt deflation’). The plunge in asset prices and the fall in aggregate demand also led to bank failures all over the country. The FED, however, did not prevent these occurrences from happening and neglected its role as lender of last resort.

Friedman’s studies mainly focused on the Great Depression in the U.S. and he neglected the international origin of the Great Depression. In particular, two countries, the U.S. and France started to hoard massive amounts of gold in the late 1920s. This gold hoarding by two Central Banks was the main causes of global deflation during the Great Depression as most countries were on the gold standard at that time (more on that here: http://macrothoughts.weebly.com/1/post/2013/10/how-the-great-depression-was-mainly-caused-by-france-and-the-us.html).

Despite this omission, Friedman was spot on in claiming that the Great Depression in the U.S. was ‘engineered’ by the FED. The economic downturn was the result of a series of policy failures and could have been mostly prevented with superior monetary policy. It turns out that something similar can be said with regard to the Great Recession starting in 2008.

Bernanke was actually one of the leading academics worldwide on monetary policy and the Great Depression before being appointed as chairman of the FED in 2006. Given his expertise and the remarkable quote to Friedman in 2002, it is astonishing that the ‘Bernanke FED’ in 2008 repeated some of the policy mistakes and greatly exacerbated the economic downturn in the U.S. experienced after the financial crisis.

It is standard procedure for the FED to publish the transcripts of the meetings of the Open Market Committee (the board that decides on monetary policy issues) with a five-year delay. A lot of fuss has been made in the last couple of days about these transcripts, and rightly so! I actually had a quick peek at some of the transcripts myself. Some of the reading is quite astonishing, but in a bad way! It turns out that many board members in 2008 were excessively concerned about inflation but did not worry enough about the slowdown in economic activity and the instability in financial markets that occurred at that time.

It is obvious that it is always easier to assess policies in retrospect. Furthermore, macroeconomic data, such as unemployment numbers, real GDP, inflation, etc., always comes in with serious time lags. The FED, however, has to make decisions in real time and is thus seriously constrained by this lack of information. However, the publication of the FED transcripts only shows what many already suspected in the first place. Specifically, many members of the committee did not have a clear understanding of what was going on in 2008 and greatly underestimated the impact the financial crisis would have on the real economy. There was a general belief shared by many FED officials that the economic downturn would turn out to be rather mild.

By contrast, other persons were already much more pessimistic at that time. This is Krugman in January 2008 (http://krugman.blogs.nytimes.com/2008/01/22/deep-maybe-long-probably/?_php=true&_&_r=0&gwh=ABA146B35DFC4F68B917167A93E75A03&gwt=pay):

I still keep reading articles asserting that the last two recessions were brief and shallow. Formally, that’s true. But both were followed by prolonged “jobless recoveries” that felt like continuing recessions. Below is the employment-population ratio since 1989, with shading showing the official recessions. In both cases the employment slump went on for a long time after the recession was supposedly over.

There’s every reason to think that the same thing will happen this time.

There was definitely information available at that time suggesting rapidly increasing distress in financial markets and a general slowdown of economic activity. Krugman’s statement makes clear that the danger was evident from the data. Despite that, many members of the committee obsessively focused on the upside risk of inflation.

Unfortunately, despite entering a recession in December 2007, inflation did not significantly slow down in 2008 even though real economic activity slowed down at a rapid pace. The main reason for that is that global commodity prices were in general at an all time high in 2007/2008 and only fell significantly thereafter once the U.S. economic downturn spread to the rest of the world. The U.S. economy thus also experienced a negative supply shock in 2008 while simultaneously facing a negative aggregate demand shock.

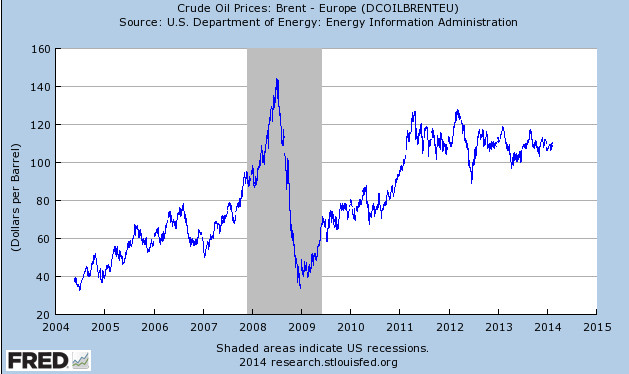

The graph below shows the dollar price of oil (per barrel). The oil price peak is exactly when the U.S. experiences the worst recession since the Great Depression in the 1930s. Talk about bad luck.

Unfortunately, despite entering a recession in December 2007, inflation did not significantly slow down in 2008 even though real economic activity slowed down at a rapid pace. The main reason for that is that global commodity prices were in general at an all time high in 2007/2008 and only fell significantly thereafter once the U.S. economic downturn spread to the rest of the world. The U.S. economy thus also experienced a negative supply shock in 2008 while simultaneously facing a negative aggregate demand shock.

The graph below shows the dollar price of oil (per barrel). The oil price peak is exactly when the U.S. experiences the worst recession since the Great Depression in the 1930s. Talk about bad luck.

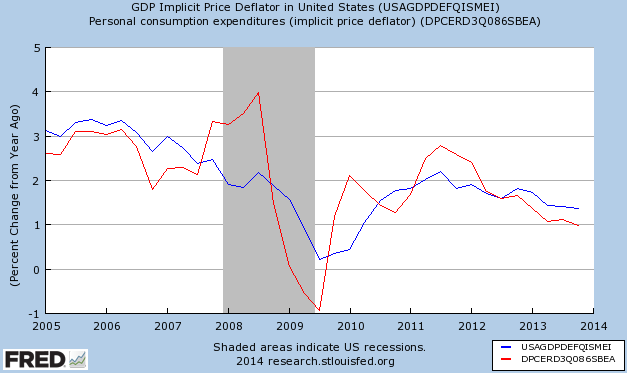

It is true that inflation remained relatively high in 2008 even though the U.S. was in a severe recession at that time. Monetary policy should, however, put little weight on commodity prices since they are really volatile by nature. The following graph shows that inflation increased quite a bit in 2008 despite the fact that the U.S. was already in a recession. The spike in the GDP price deflator (red line) mainly comes from record commodity prices during that year. But I also included in the graph an alternative measure of inflation (blue line), which shows a clear downward trend since the end of 2006. The FED should have ignored the rise in commodity prices and focused instead on such alternative price indices, which made abundantly clear that economic activity was slowing down significantly since the beginning of 2007.

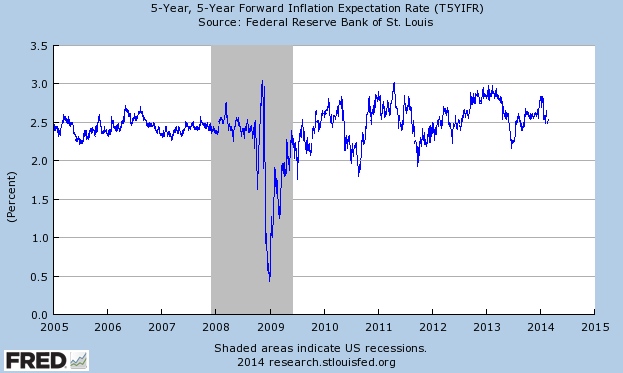

In general, there were a large variety of economic indicators available to the FED in real time that showed that the economic outlook was quite bad. Inflation expectations, for example, were falling rapidly over the course of 2008:

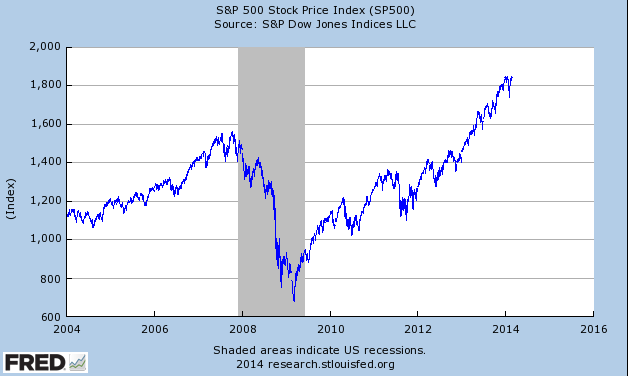

Asset prices also started to fall significantly in 2008. Housing obviously comes to mind. The burst of the bubble led, in general, to a sharp reduction in housing prices all over the country. Stock markets, shown below, also became increasingly bearish once the recession started. The decline in asset prices fed back into the real economy by reducing aggregate demand, which then led to a further decrease in asset prices, and so on.

Financial markets were thus increasingly under distress as asset prices fell sharply and aggregate demand started to slow down at a rapid pace. All these facts were known to the FED in real time. Based on the same information, Krugman and others suggested already much earlier that the recession could turn into a very deep and long economic slump.

It seems, however, that the FED largely underestimated the impact that plunging asset prices and financial distress would have on the real economy. FED officials mostly ignored all these warnings and monetary policy became increasingly tight over the course of 2008. Instead of easing monetary conditions aggressively, the FED only reduced its interest rate stepwise and at a relatively slow pace at that. There are two meetings in particular that stand out. The first one took place on September 16th one day after the bankruptcy of Lehman brothers. The fall of 2008 was effectively the peak of the financial crisis in the U.S. and several institutions had to be bailed out by the Treasury and the FED. For a variety of reasons, some of them were legal constraints, Lehman was not saved and filed for bankruptcy on September 15th. Financial markets, already under enormous distress, completely froze up. It should have been clear to the officials at the FED that bold action was needed at that time. However, the committee decided to leave interest rates unchanged the day after the Lehman failure. Markets, however, clearly expected the FED to be more expansionary. Since the FED did less than what market participants expected, this effectively meant that monetary policy became very tight. Indeed, the month of September turned out to be one of the worst in terms of performance for the Dow Jones index, which experienced two of the largest drops in recent history: 4.4% on September 15th and an astonishing 7% on September 29th. The sharp decline in U.S. and the financial distress spread to financial markets all around the globe. Stock markets tumbled around the world and within a matter of weeks, wealth in magnitude of several trillions of U.S.-$ was wiped out. The associated negative wealth effects led to a further depression of aggregate demand, which in turn reinforced the plunge in asset prices.

With the reading of the FED transcript, there is no doubt that monetary policy was excessively tight in the fall of 2008. Nominal interest rate were only at 2%, down from 4.25% in December 2007. Interest rates are, however, a lousy indicator of the stance of monetary policy. The only reliable indicators showing the easiness or tightness of monetary policy are inflation and nominal GDP growth (NGDP). Bernanke should have known all this since he wrote the following back in 2003:

It seems, however, that the FED largely underestimated the impact that plunging asset prices and financial distress would have on the real economy. FED officials mostly ignored all these warnings and monetary policy became increasingly tight over the course of 2008. Instead of easing monetary conditions aggressively, the FED only reduced its interest rate stepwise and at a relatively slow pace at that. There are two meetings in particular that stand out. The first one took place on September 16th one day after the bankruptcy of Lehman brothers. The fall of 2008 was effectively the peak of the financial crisis in the U.S. and several institutions had to be bailed out by the Treasury and the FED. For a variety of reasons, some of them were legal constraints, Lehman was not saved and filed for bankruptcy on September 15th. Financial markets, already under enormous distress, completely froze up. It should have been clear to the officials at the FED that bold action was needed at that time. However, the committee decided to leave interest rates unchanged the day after the Lehman failure. Markets, however, clearly expected the FED to be more expansionary. Since the FED did less than what market participants expected, this effectively meant that monetary policy became very tight. Indeed, the month of September turned out to be one of the worst in terms of performance for the Dow Jones index, which experienced two of the largest drops in recent history: 4.4% on September 15th and an astonishing 7% on September 29th. The sharp decline in U.S. and the financial distress spread to financial markets all around the globe. Stock markets tumbled around the world and within a matter of weeks, wealth in magnitude of several trillions of U.S.-$ was wiped out. The associated negative wealth effects led to a further depression of aggregate demand, which in turn reinforced the plunge in asset prices.

With the reading of the FED transcript, there is no doubt that monetary policy was excessively tight in the fall of 2008. Nominal interest rate were only at 2%, down from 4.25% in December 2007. Interest rates are, however, a lousy indicator of the stance of monetary policy. The only reliable indicators showing the easiness or tightness of monetary policy are inflation and nominal GDP growth (NGDP). Bernanke should have known all this since he wrote the following back in 2003:

The imperfect reliability of money growth as an indicator of monetary policy is unfortunate, because we don’t really have anything satisfactory to replace it. As emphasized by Friedman . . . nominal interest rates are not good indicators of the stance of policy . . . The real short-term interest rate . . . is also imperfect . . . Ultimately, it appears, one can check to see if an economy has a stable monetary background only by looking at macroeconomic indicators such as nominal GDP growth and inflation.

(retrieved from http://www.themoneyillusion.com/?p=13576)

Inflation and inflation expectations were plunging in the fall of 2008 and, more importantly, so was nominal GDP. Monetary policy was thus extremely tight during that period. It is mysterious why many members of the FED, Bernanke included, did not realize this (Note that there were a few who understood the gravity of the situation. Janet Yellen, the current FED chair, was actually amongst them).

Consequently, the economic downturn after the financial crisis can partly be attributed to the FED. It failed to ease monetary conditions sufficiently in the later part of 2008 and NGDP plunged as a result while unemployment rose to record levels in 2009. The economic slump could have been largely mitigated with more expansionary monetary policy earlier on.

Despite the massive policy failure in 2008, the FED was in general much more aggressive than other Central Banks over the last couple of years. Bernanke managed to overrule various inflation hawks at the FED and managed to push through various policies such as QE1 to QE3 and forward guidance. As a result, the U.S. economy outperformed by far its peers (the U.K. and the Eurozone) since the beginning of the crisis. U.S. unemployment is now much lower than in the Eurozone and American growth rates are likely to exceed Eurozone growth also in the next couple of years.

In general, the Bernanke FED performed quite poorly, especially in 2008 when it stood by and let the economy freeze up. However, compared to other Central Banks, such as the ECB or the Bank of Japan in the 1990s, the FED did a much better job in stimulating economic activity after the crisis. Despite a very mixed performance in absolute terms, the FED did really well in relative terms. The U.S. can count itself lucky that Bernanke, an expert on the Great Depression and the Japanese malaise, was head of the FED in recent years. Many other so-called ‘experts’ would have done a far worse job with enormous consequences for the U.S and world economy. The FED transcripts are actually proof of that since they show that some members had a poor understanding of what was going on in 2008. Many FED officials would have preferred to tighten monetary policy even more in the end of 2008 as well as over the last couple of years. The U.S. thus dodged a bullet with having Bernanke running the FED while Europe has been stuck with a very incompetent ECB, which repeated the policy mistakes of the Bank of Japan but on a grander scale (and is still doing so).

Inflation and inflation expectations were plunging in the fall of 2008 and, more importantly, so was nominal GDP. Monetary policy was thus extremely tight during that period. It is mysterious why many members of the FED, Bernanke included, did not realize this (Note that there were a few who understood the gravity of the situation. Janet Yellen, the current FED chair, was actually amongst them).

Consequently, the economic downturn after the financial crisis can partly be attributed to the FED. It failed to ease monetary conditions sufficiently in the later part of 2008 and NGDP plunged as a result while unemployment rose to record levels in 2009. The economic slump could have been largely mitigated with more expansionary monetary policy earlier on.

Despite the massive policy failure in 2008, the FED was in general much more aggressive than other Central Banks over the last couple of years. Bernanke managed to overrule various inflation hawks at the FED and managed to push through various policies such as QE1 to QE3 and forward guidance. As a result, the U.S. economy outperformed by far its peers (the U.K. and the Eurozone) since the beginning of the crisis. U.S. unemployment is now much lower than in the Eurozone and American growth rates are likely to exceed Eurozone growth also in the next couple of years.

In general, the Bernanke FED performed quite poorly, especially in 2008 when it stood by and let the economy freeze up. However, compared to other Central Banks, such as the ECB or the Bank of Japan in the 1990s, the FED did a much better job in stimulating economic activity after the crisis. Despite a very mixed performance in absolute terms, the FED did really well in relative terms. The U.S. can count itself lucky that Bernanke, an expert on the Great Depression and the Japanese malaise, was head of the FED in recent years. Many other so-called ‘experts’ would have done a far worse job with enormous consequences for the U.S and world economy. The FED transcripts are actually proof of that since they show that some members had a poor understanding of what was going on in 2008. Many FED officials would have preferred to tighten monetary policy even more in the end of 2008 as well as over the last couple of years. The U.S. thus dodged a bullet with having Bernanke running the FED while Europe has been stuck with a very incompetent ECB, which repeated the policy mistakes of the Bank of Japan but on a grander scale (and is still doing so).

RSS Feed

RSS Feed