That's my prediction at least. There are a lot of people who suggest now that the Democrats are in big trouble because they lost all 4 special elections that took place in recent month. Trump and the Republicans were certainly able to hold on to their base. It must be said though that all 4 elections took place in Congressional districts that were more Repiblican-leaning than the average Republican district. And remember that Trump only got 46% of the popualr vote, holding to the base will not be enough. Furthermore, the data shows that Democrats highly outperformed compared to recent elections. Suddenly Democrats were competitive in races that shouldn't have been up for grabs at all. According to Silver, Democrats outperformed by more than 10 percentage points. If this lead will be maintained, Democrats will be able to take back the House in 2018.

I am not expert enough to be able to foresee whether the Republicans really will repeal the Affordable Care Act. The consequences would be very dire for many Americans indeed. There is not enough known yet about the Republican health care plan,but as far as I know it would leave milllions of Americans without insurance and raise premiums while giving millionaires and billionaires a hefty tax cut. This is class warfare on the poor, plain and simple.

Many Americans in the red states will realize that they got screwed by the Republican party. We should thus expect a pushback in the midterm elections. Voters will want to rein in the Republican's power who curerently hold the presidency and both houses.

It is always important to mark your belief to market. So here some forecasts about things to come:

The current political climate is quite favorable to Democracts. This trend will increase if the Republicans manage to pass their truly horrible healthcare bill. I thus expect that Demcorats will manage to get a majority in Congress after the midterm elections in 2018.

And now to some economic forecasts:

I turned out to be spot on with my early April point forecast of 1.25 real GDP growth for the U.S. for Q1 2017. The real figure came in at 1.2% a little later. I got lucky. Quarterly GDP growth rates are highly volatile. The trick is to take into consideration the range of forecasts provided by the Blue Chip consensus as well as the different GDP Nowcasts, like the one provided by the Atlanta Fed and the New York Fed. It is also important to track how the Nowcasts evolve over time as the quarter goes by. For the second quarter of this year, for example, we can see that the GDP Nowcasts have continuously gone down over the last few months. Incoming data thus suggests that Q2 will not be as good as initially believed in April.

The New York Fed's Nowcast, for example, declined from 3% in March to currently 1.9% while the Atlanta Fed's Nowcast declined from 4% in April to less than 3% right now.

The recent Fed hike was definitely a mistake and will put downward pressure on an economy that is advancing at a very modest pace. So here a probabilistic forecast for real GDP growth Q2:

Below 1.5% 10%

1.5% - 2.0% 20%

2.0% - 2.5% 40%

2.5% - 3.0% 20%

Above 3.0% 10%

My point forecast for Q2 thus would be 2.25%, which is more pessimistic than the Blue Chip consensus, but somehwat more opitmistic than the current Nowcast of the New York Fed. I just found out though that my estimate is exactly in line with the current Nowcast provided by the St. Louis Fed (2.3%).

Concerning U.S. annual GDP for 2017, I think it is fair to say that there is a high probablity (about 70%) that it will be in the range of 1.5% to 2%. Back in April I provided a point forecast of 1.8%. Given the meagre performance of Q1 combined with the fact that Q2 will probably be significantly higher than 2%, I think annual GDP might rather end up being closer to 1.5% than 2%.

Low real GDP figures are the new normal in the 21st century, at least for the foreseeable future. Note that there is a good chance that the Eurozone's real GDP growth rate this year might outperform American real GDP growth, just like in 2016 (note though that the Eurozone underperformed for several years in the beginning of the decade as a result of the Eurozone crisis).

When it comes to interest rate increases, the recent rate hike by the Fed now increasingly looks like a mistake. Incoming economic data is relatively weak. While some Fed officials wanted another two rate hikes this year, this is now completely out of the question. Some of the Fed doves made it abundantly clear that further hikes are only warranted if inflation will finally go back to target. I don't see this happening anytime soon. Inflation data will continue to disappoint (the Phillips curve is dead, more on that in a later blog post). Markets expect only one rate hike by the end of this year with a probability of about 50%. Since I trust market forecasts over Fed forecasts, this is basically where I stand as well.

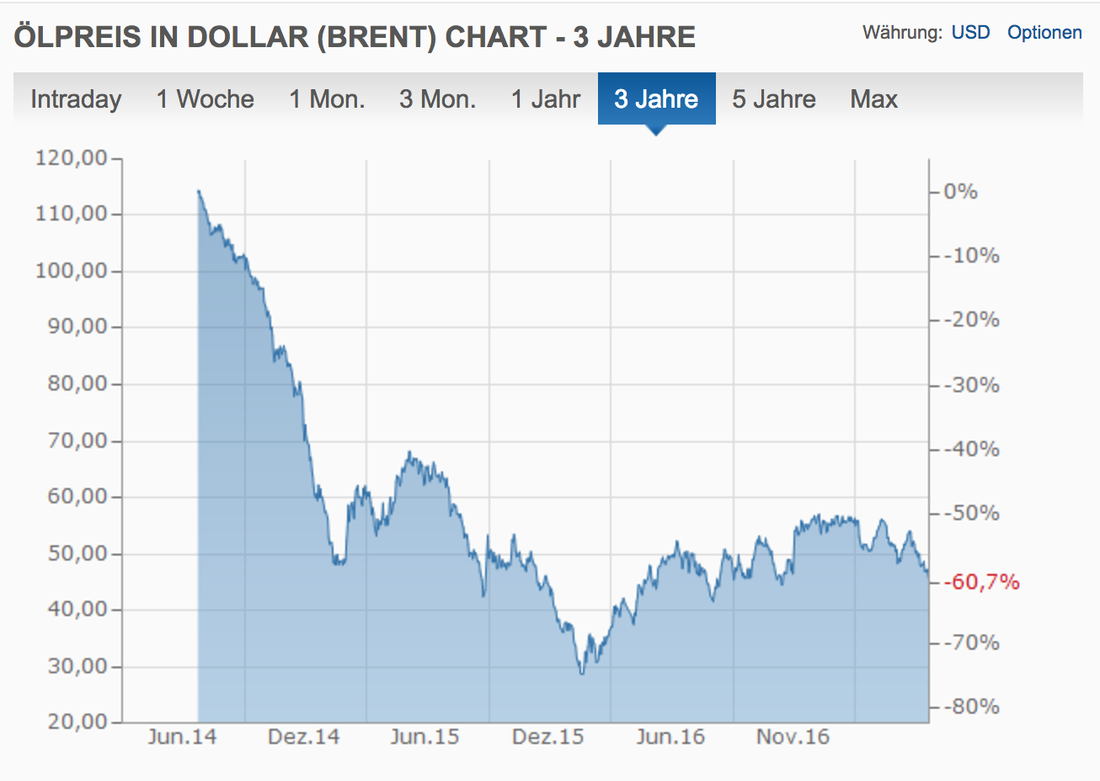

Finally, a note on oil prices. Thanks to the fracking revolution, the U.S. has become one of the largest oil producers in the world in recent years. Furthermore, the oil cartel OPEC has broken down as it has lost in market share. Peak oil was predicted decades ago, but so far all pessimistic forecasts have proved to be unwarranted. The price of Brent just declined below 45$ a barrel (see below), so financial markets do not think that we will run out of oil anytime soon. There is a good chance that we will reach peak oil within the next two decades or so, but it might just as well be related to lower demand than a lack of supply as renewable energies are becoming increasingly competitive. The price of solar panels has plunged in recent years. In the meantime, I expect that fracking will put a ceiling on the price of oil in the range of 50 to 60$ a barrel for the foreseeable future, meaning the next 2-3 years or so. As for what comes after, it's anybody's guess.

I am not expert enough to be able to foresee whether the Republicans really will repeal the Affordable Care Act. The consequences would be very dire for many Americans indeed. There is not enough known yet about the Republican health care plan,but as far as I know it would leave milllions of Americans without insurance and raise premiums while giving millionaires and billionaires a hefty tax cut. This is class warfare on the poor, plain and simple.

Many Americans in the red states will realize that they got screwed by the Republican party. We should thus expect a pushback in the midterm elections. Voters will want to rein in the Republican's power who curerently hold the presidency and both houses.

It is always important to mark your belief to market. So here some forecasts about things to come:

The current political climate is quite favorable to Democracts. This trend will increase if the Republicans manage to pass their truly horrible healthcare bill. I thus expect that Demcorats will manage to get a majority in Congress after the midterm elections in 2018.

And now to some economic forecasts:

I turned out to be spot on with my early April point forecast of 1.25 real GDP growth for the U.S. for Q1 2017. The real figure came in at 1.2% a little later. I got lucky. Quarterly GDP growth rates are highly volatile. The trick is to take into consideration the range of forecasts provided by the Blue Chip consensus as well as the different GDP Nowcasts, like the one provided by the Atlanta Fed and the New York Fed. It is also important to track how the Nowcasts evolve over time as the quarter goes by. For the second quarter of this year, for example, we can see that the GDP Nowcasts have continuously gone down over the last few months. Incoming data thus suggests that Q2 will not be as good as initially believed in April.

The New York Fed's Nowcast, for example, declined from 3% in March to currently 1.9% while the Atlanta Fed's Nowcast declined from 4% in April to less than 3% right now.

The recent Fed hike was definitely a mistake and will put downward pressure on an economy that is advancing at a very modest pace. So here a probabilistic forecast for real GDP growth Q2:

Below 1.5% 10%

1.5% - 2.0% 20%

2.0% - 2.5% 40%

2.5% - 3.0% 20%

Above 3.0% 10%

My point forecast for Q2 thus would be 2.25%, which is more pessimistic than the Blue Chip consensus, but somehwat more opitmistic than the current Nowcast of the New York Fed. I just found out though that my estimate is exactly in line with the current Nowcast provided by the St. Louis Fed (2.3%).

Concerning U.S. annual GDP for 2017, I think it is fair to say that there is a high probablity (about 70%) that it will be in the range of 1.5% to 2%. Back in April I provided a point forecast of 1.8%. Given the meagre performance of Q1 combined with the fact that Q2 will probably be significantly higher than 2%, I think annual GDP might rather end up being closer to 1.5% than 2%.

Low real GDP figures are the new normal in the 21st century, at least for the foreseeable future. Note that there is a good chance that the Eurozone's real GDP growth rate this year might outperform American real GDP growth, just like in 2016 (note though that the Eurozone underperformed for several years in the beginning of the decade as a result of the Eurozone crisis).

When it comes to interest rate increases, the recent rate hike by the Fed now increasingly looks like a mistake. Incoming economic data is relatively weak. While some Fed officials wanted another two rate hikes this year, this is now completely out of the question. Some of the Fed doves made it abundantly clear that further hikes are only warranted if inflation will finally go back to target. I don't see this happening anytime soon. Inflation data will continue to disappoint (the Phillips curve is dead, more on that in a later blog post). Markets expect only one rate hike by the end of this year with a probability of about 50%. Since I trust market forecasts over Fed forecasts, this is basically where I stand as well.

Finally, a note on oil prices. Thanks to the fracking revolution, the U.S. has become one of the largest oil producers in the world in recent years. Furthermore, the oil cartel OPEC has broken down as it has lost in market share. Peak oil was predicted decades ago, but so far all pessimistic forecasts have proved to be unwarranted. The price of Brent just declined below 45$ a barrel (see below), so financial markets do not think that we will run out of oil anytime soon. There is a good chance that we will reach peak oil within the next two decades or so, but it might just as well be related to lower demand than a lack of supply as renewable energies are becoming increasingly competitive. The price of solar panels has plunged in recent years. In the meantime, I expect that fracking will put a ceiling on the price of oil in the range of 50 to 60$ a barrel for the foreseeable future, meaning the next 2-3 years or so. As for what comes after, it's anybody's guess.

RSS Feed

RSS Feed