In recent years macroeconomists have started to use dynamic factor models as a new tool to predict quarterly GDP figures (and potentially other macroeconomic variables of interest) in real time. These factor models extract information from a large number of macroeconomic variables that are available at a higher frequency, such as industrial production, consumer expenditures, employment numbers, housing starts, etc., to forecast quarterly GDP growth rates. The GDP Nowcast model of the Atlanta Fed and the New York Fed are two examples of such a model. It is thus interesting to track the performance of these two competing models over time and to assess their accuracy, keeping in mind that quarterly growth are extremely volatile and thus also hard to predict. The two GDP Nowcast models also allow us to track the quarterly GDP estimate to be over the course of the quarter as their predictions are getting updated almost on a weekly basis with new incoming macroeconomic data in real time, something which was not possible before.

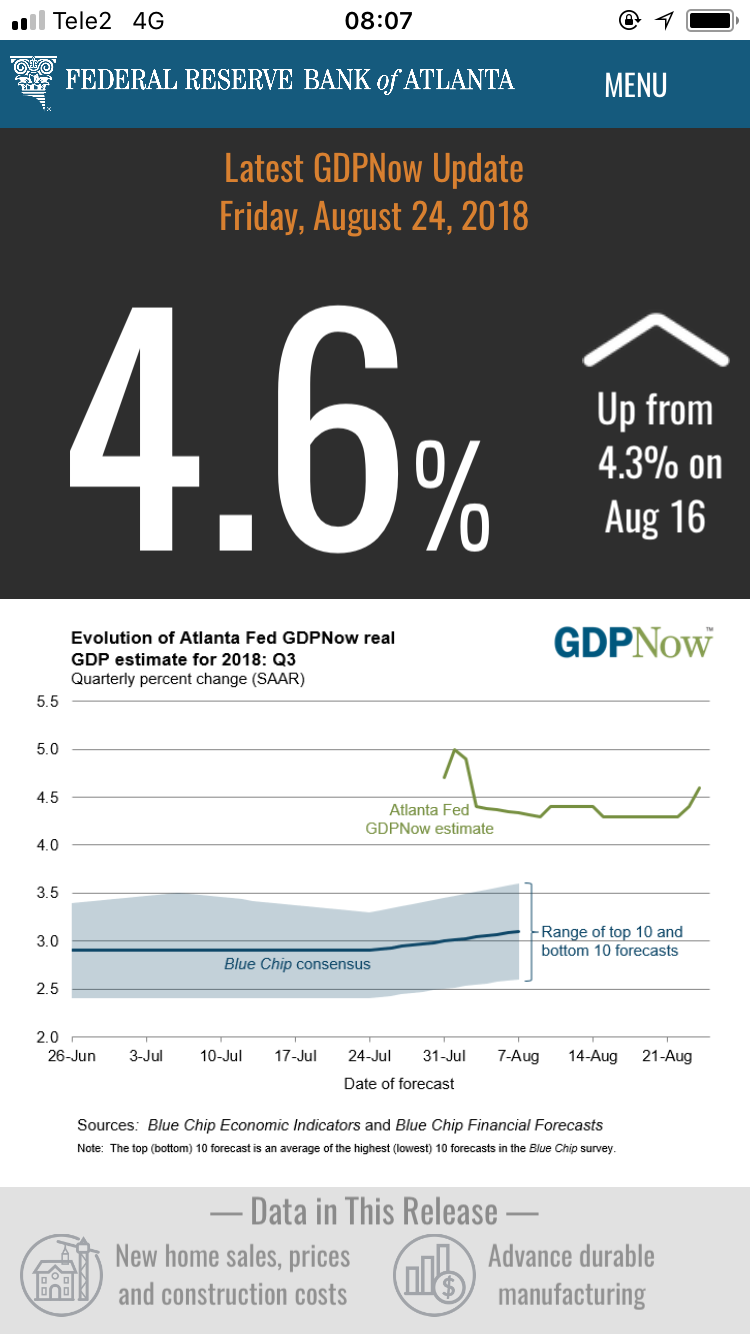

In that light, the recent divergence of the Atlanta Fed Nowcast and the New York Fed Nowcast are extremely interesting, with the former displaying an improved outlook and projecting a quarterly growth rate of now 4.8%, up from about 4.3% at the beginning of the August. The New York Nowcast, on the other hand, has shown a declining growth rate of now just about 2%, down from exactly 3% at the beginning of the quarter.

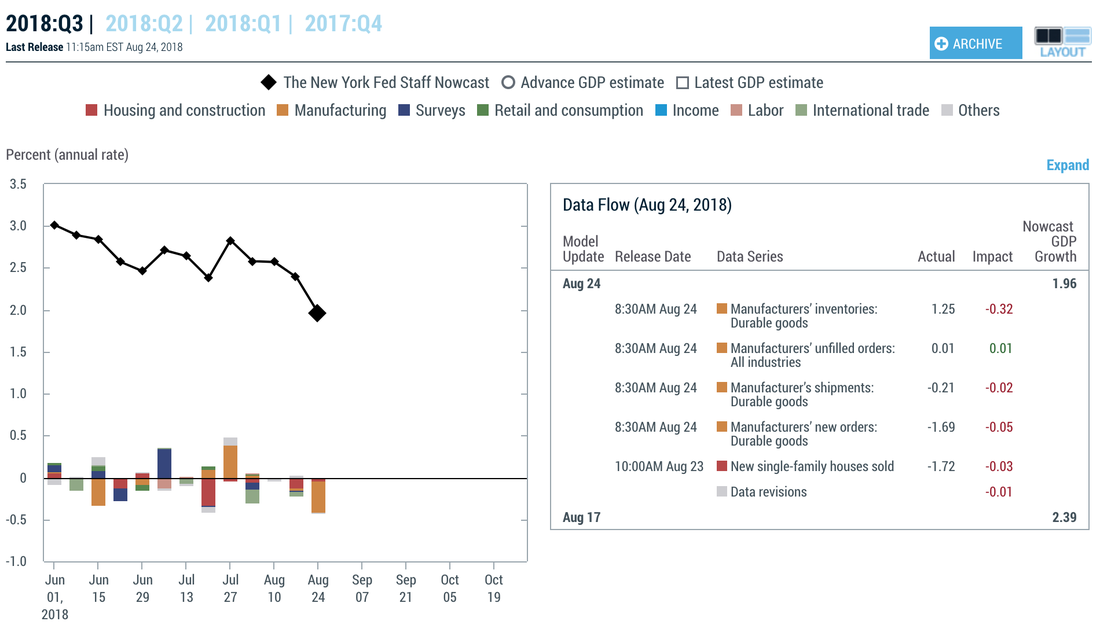

In that light, the recent divergence of the Atlanta Fed Nowcast and the New York Fed Nowcast are extremely interesting, with the former displaying an improved outlook and projecting a quarterly growth rate of now 4.8%, up from about 4.3% at the beginning of the August. The New York Nowcast, on the other hand, has shown a declining growth rate of now just about 2%, down from exactly 3% at the beginning of the quarter.

Atlanta Fed GDP Nowcast

New York Fed GDP Nowcast

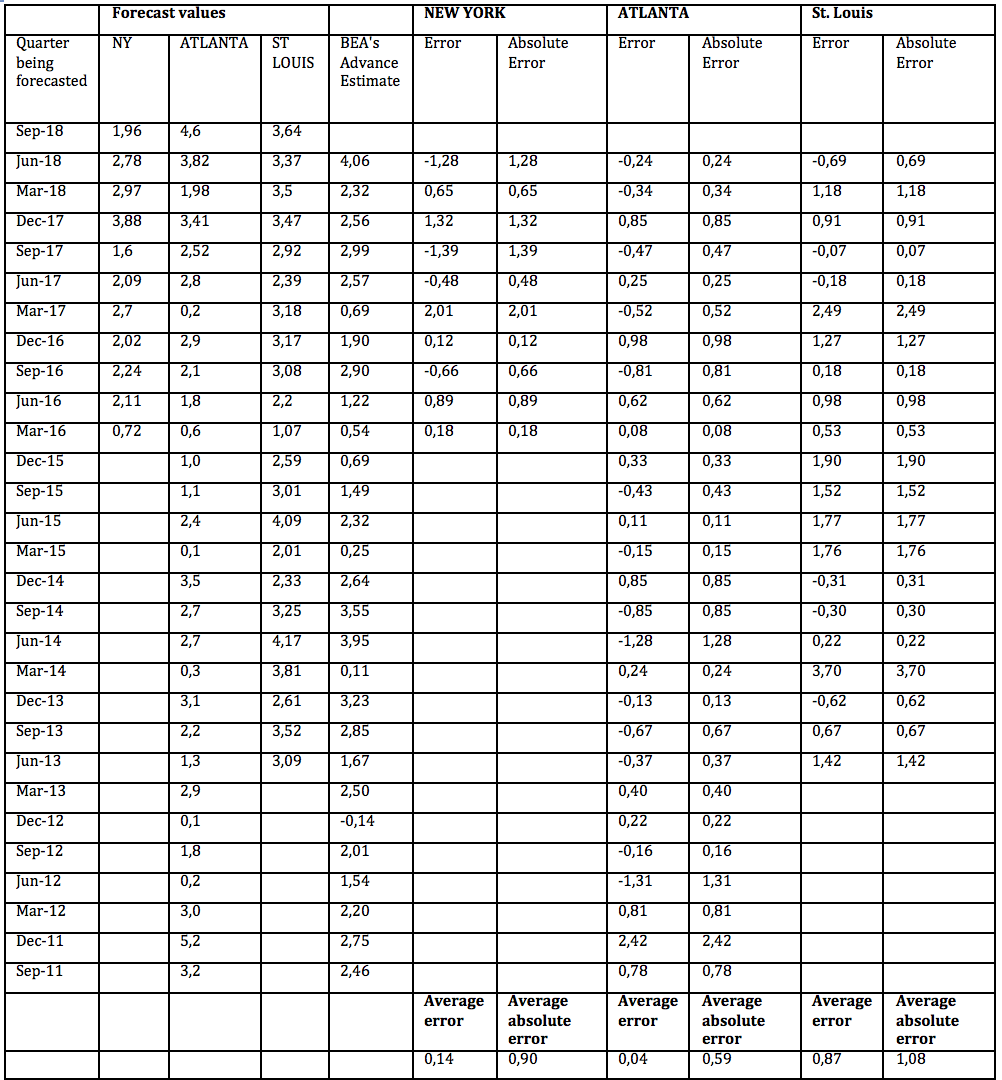

I have updated the table below to track the performance of the models over the last few years. Keeping in mind that these models have not been around for very long yet, thus limiting the data points to just a few years, the Atlanta Fed Nowcast as of now seems to perform better than the New York Nowcast model (while the St Louis model also predicts quarterly GDP, it is based on a different methodology). Not only does the Atlanta model produce unbiased forecasts (the average error is close to zero), but it also produces the most accurate prediction with the smallest absolute forecast error of about 0.6% in absolute values.

The correlation between the forecast error of the Atlanta Fed Nowcast and the NY Nowcast is 33%, meaning that most of the time both models are producing forecast errors in the same direction. The recent divergence of the two models over the last two months is thus especially interesting. Unfortunately, I haven't had the time to dig deeper into the two models and can thus not comment to what extent they differ and what the source of the different prediction for this quarterly GDP figure is.

The correlation between the forecast error of the Atlanta Fed Nowcast and the NY Nowcast is 33%, meaning that most of the time both models are producing forecast errors in the same direction. The recent divergence of the two models over the last two months is thus especially interesting. Unfortunately, I haven't had the time to dig deeper into the two models and can thus not comment to what extent they differ and what the source of the different prediction for this quarterly GDP figure is.

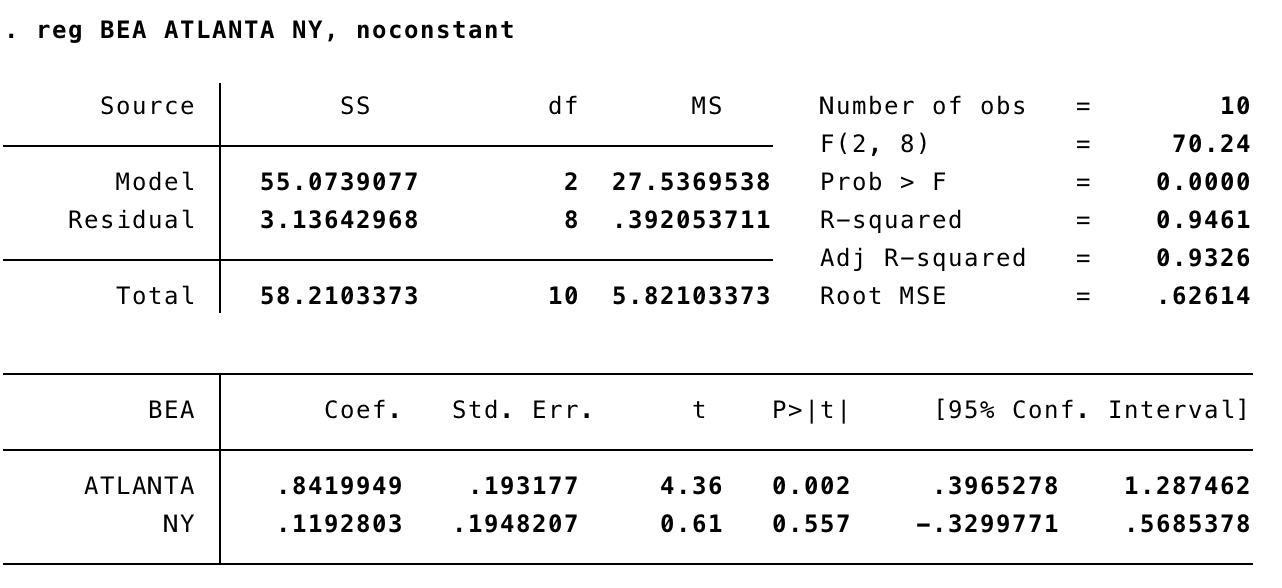

Using a very simple linear regression model with the very little data we have, one can see that the most accurate prediction of quarterly GDP figures is a weighted average of the two Nowcast models, with a much higher weight on the Atlanta model as it is the superior forecast. The New York Nowcast model does not seem to add much explanatory power as the coefficient is statistically insignificant (note that one of the problems though is that there are very little data points). The "error correlation" between the two Nowcast models is surely another reason on why a weighted average between the two models is not vastly superior than just relying on the Atlanta model instead.

Using this weighted average approach, produces a quarterly GDP forecast for Q3 of just a little over 4%, given the current Nowcast values. Trump might get his >3% annual GDP growth for the current year after all, keeping in mind though that most of it is due to extraordinarily policy accommodation as a result of the substantial corporate tax cut, in a way a fiscal stimulus package. With real interest rates still being negative and below the Fed's estimate of neutral, monetary policy is accommodative as well. This effectively means that huge problems are baked in for 2020 when fiscal policy will tighten by necessity at the same time as Fed policy will tighten as well. There is good reason to believe that this could actually produce a recession. Note that the yield curve is most likely to invert, if not with the next rate hike then with the one that follows, with the inversion of course historically being the best recession predictor we have.

PS: Some additional comments

1) The dynamic factor models as a tool for GDP predictions have not been around for very long. They are purely data driven and thus completely differ from the DSGE models Central Banks have used over the last few decades. Many of those DSGE models have failed quite spectacularly during the financial crisis (Not in terms of failing to predict the crisis. Crises are by definition more or less unpredictable. Don't believe anybody who tells you otherwise. But the models failed in predicting some of the important dynamics in the aftermath of the Great Recession, such as the failure of interest rates and inflation to rise, etc.). I have not seen any study so far that compares the accuracy of those DSGE models with the data driven dynamic factor models, but my gut feeling is that the data driven approach can be superior. The DSGE methodology rests on some highly dubious assumptions on how the macroeconomy works. There is no doubt that the core neo-keynesian model is quite flawed, a topic I have written about before. See here, for example.

2) Quarterly GDP figures are highly volatile. One might think that an average forecast error of 0.6% is quite high, but given the state of current macroeconomic models this is at the moment the best macroeconomists can do. Other variables are much more sticky, especially inflation and also interest rates to some extent, at least in recent years, thus making a prediction somewhat easier.

3) Financial markets efficiently aggregate information, at least most of the time. Financial market predictions about the future path of interest rates, the Fed funds future market, has repeatedly turned out to be more accurate than even the Fed's internal forecasts on where interest rates will be in one year's time.

1) The dynamic factor models as a tool for GDP predictions have not been around for very long. They are purely data driven and thus completely differ from the DSGE models Central Banks have used over the last few decades. Many of those DSGE models have failed quite spectacularly during the financial crisis (Not in terms of failing to predict the crisis. Crises are by definition more or less unpredictable. Don't believe anybody who tells you otherwise. But the models failed in predicting some of the important dynamics in the aftermath of the Great Recession, such as the failure of interest rates and inflation to rise, etc.). I have not seen any study so far that compares the accuracy of those DSGE models with the data driven dynamic factor models, but my gut feeling is that the data driven approach can be superior. The DSGE methodology rests on some highly dubious assumptions on how the macroeconomy works. There is no doubt that the core neo-keynesian model is quite flawed, a topic I have written about before. See here, for example.

2) Quarterly GDP figures are highly volatile. One might think that an average forecast error of 0.6% is quite high, but given the state of current macroeconomic models this is at the moment the best macroeconomists can do. Other variables are much more sticky, especially inflation and also interest rates to some extent, at least in recent years, thus making a prediction somewhat easier.

3) Financial markets efficiently aggregate information, at least most of the time. Financial market predictions about the future path of interest rates, the Fed funds future market, has repeatedly turned out to be more accurate than even the Fed's internal forecasts on where interest rates will be in one year's time.

RSS Feed

RSS Feed