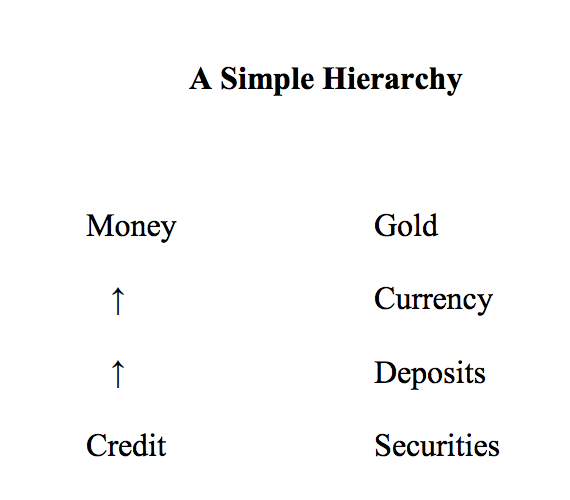

Perry Mehrling at INET has two fantastic courses on money and banking at Coursera, which I highly recommend. One of the main themes of the course evolves around the hierarchy of money depicted in the graph below.

During the time of the gold standard, gold was the ultimate money because it was the internationally accepted means of payment. Central Banks domestically issued currency, which was backed up by gold. In that sense, national currencies were a sort of credit in the sense that they represented a promise to pay gold on demand.

Next in line in the hierarchy of money are normal bank deposits. Of course, nowadays everybody assumes that deposits can be redeemed at par value into national currency. This, however, is mostly a result of modern deposit insurance, which provides a safeguard against bank runs and bank failures. In the case of a bank failure, deposits will probably not be redeemed at par, meaning that deposits are not quite as money-like as hard currency.

One of the main features of modern finance is the property of the private sector to issue credit and money-like assets. Money and credit allow for the production and private exchange of goods and services to take place that would otherwise not be feasible under a pure barter system. While the elasticity of credit is one of the main features of the modern economy, it might also be the source of economic and financial instability, a point that Minsky has raised numerous times but has been somewhat neglected by mainstream macroeconomics.

During the boom one can usually detect an expansion of private sector credit. Corporations and private individuals can issue IOUs, money-like assets, which enter the circular flow. Those IOUs can be accepted as means of payment as long as the issuer is deemed to be creditworthy and trustworthy.

The main problem with private sector credit, however, is that during a time of a financial panic all those privately issued IOUs might suddenly not be deemed as safe anymore. When asset markets like stocks and housing tumble and everybody is scrambling for safe assets, including banks, as liquidity freezes up, suddenly all those money-like assets are not liquid anymore. All that counts now is the hard money, meaning gold and currency when countries where on the gold standard, with today's equivalent being Central Bank reserves as well as safe government bonds.

This effect could also be observed during the financial crisis of 2008. Even though the financial crisis originated in the US, the dollar actually sharply appreciated as investors from all over the world were looking for a safe haven and put their money into US Treasuries and other US-dollar denominated safe investments (As a side note: the strong dollar appreciation was also a result of tight US monetary policy). Meanwhile, other money-like assets were completely freezing up during the fall of 2008. One such example are money market funds, basically investment vehicles that were holding short-term debt securities, such as US Treasuries but also, and more importantly, commercial papers (short-term IOUs). While those money market funds were widely regarded as safe, the key difference was that in contrast to bank deposits they were actually not backed up by the Federal Government.

The crisis of 2008 turned into a liquidity crunch in the fall of that year as some money market funds experienced the equivalent of a bank run. Furthermore, companies started to experience increasing financial difficulties as investors refused to roll over commercial papers. This is the key aspect of liquidity: Financial markets giveth, and financial markets taketh away. During the crisis of 2008, suddenly a bunch of money-like assets froze up with with hard currency and Treasuries suddenly being the only and ultimate safe haven.

As the elasticity of credit can disappear very quickly, the Central Bank must step in as a lender of last resort and provide all the liquidity that has suddenly evaporated from the system if it wants to restore sanity in financial markets again. Moreover, financial disruptions can have large negative macroeconomic effects, disrupting the economy for even years to come, which is why Central Bank intervention is desperately needed (while there is some truth to the moral hazard argument, it really does not justify creating a second Great Depression in order to punish bad-behaving banks or investors).

Now a personal story about money and liquidity

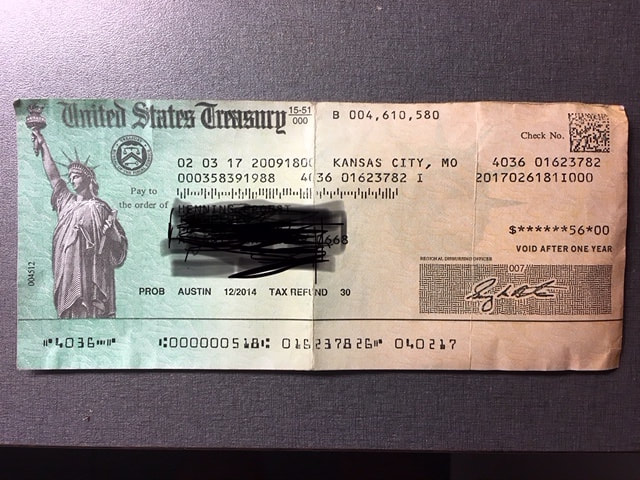

Last but not least, a short personal story about money-like assets. My father received a couple of month ago the following check from the US Treasury, 56 USD worth (for obvious reasons I made my Dad's address unreadable):

Now here is where it gets interesting. The check from the US Treasury should rather be one of the safest and more liquid money-like assets in the world. It is a dollar denominated IOU from the US Treasury, not very much unlike a US government bond in a way (except that it does not pay interest). Now here is where it gets interesting. Commercial banks in Germany have stopped a couple of years ago accepting foreign currency denominated checks. I am not entirely sure of why that is, but I can think of at least two reasons. First, checks are simply not used as a means of payment in Germany anymore. Second, transaction costs are just too high.

A few years ago I actually worked as an intern in a regional bank in Germany (Volksbank Paderborn) in their "foreign sales department". Back then some customers would still receive foreign currency denominated checks. So if a customer presented us a foreign currency denominated check in British pounds, let's say from the Barclays in the UK, then Volksbank Paderborn would deposit the Euro-equivalent amount (minus a transaction fee) into that customer's bank account at the Volksbank. However, this is not the end of the story. Volksbank Paderborn now also has to mail the check to the UK to a British partner bank (let's say for simplicity that the UK partner bank is also Barclays) so that Barclays can deposit the British pound amount (minus a small transaction fee, maybe) of the check at one of the Volksbank's foreign denominated currency accounts at Barclays. So depositing a foreign currency check involves currency conversion, up to two transaction fees, as well as mailing the actual check back to the country from where it was issued in the first place. Given this somewhat complicated procedure and the fact that almost nobody uses checks anymore in Germany, it is quite understandable that banks refuse to accept foreign denominated checks.

I just travelled to the US and took my father's check with me. However, since it was signed by him, banks refused to cash out the check to me. In essence, I was carrying around a "worthless" piece of paper issued by the US Treasury, which is rather ironic !!!

The broader point I am trying to make obviously is that there are a bunch of money-like assets, money market funds, checks, commercial paper, IOUs, etc., and all of these assets can serve as money and are almost equivalent to money in one state of the world. However, there are other states of the world, a financial panic where suddenly everybody is scrambling for safety as companies, investors, and private individuals alike are defaulting on their debts. In a financial panic all those money-like assets might suddenly freeze up and loose their money-like status, becoming more or less worthless, and in the end it is only hard currency and Central Bank reserves that can be considered as the ultimate money.

A few years ago I actually worked as an intern in a regional bank in Germany (Volksbank Paderborn) in their "foreign sales department". Back then some customers would still receive foreign currency denominated checks. So if a customer presented us a foreign currency denominated check in British pounds, let's say from the Barclays in the UK, then Volksbank Paderborn would deposit the Euro-equivalent amount (minus a transaction fee) into that customer's bank account at the Volksbank. However, this is not the end of the story. Volksbank Paderborn now also has to mail the check to the UK to a British partner bank (let's say for simplicity that the UK partner bank is also Barclays) so that Barclays can deposit the British pound amount (minus a small transaction fee, maybe) of the check at one of the Volksbank's foreign denominated currency accounts at Barclays. So depositing a foreign currency check involves currency conversion, up to two transaction fees, as well as mailing the actual check back to the country from where it was issued in the first place. Given this somewhat complicated procedure and the fact that almost nobody uses checks anymore in Germany, it is quite understandable that banks refuse to accept foreign denominated checks.

I just travelled to the US and took my father's check with me. However, since it was signed by him, banks refused to cash out the check to me. In essence, I was carrying around a "worthless" piece of paper issued by the US Treasury, which is rather ironic !!!

The broader point I am trying to make obviously is that there are a bunch of money-like assets, money market funds, checks, commercial paper, IOUs, etc., and all of these assets can serve as money and are almost equivalent to money in one state of the world. However, there are other states of the world, a financial panic where suddenly everybody is scrambling for safety as companies, investors, and private individuals alike are defaulting on their debts. In a financial panic all those money-like assets might suddenly freeze up and loose their money-like status, becoming more or less worthless, and in the end it is only hard currency and Central Bank reserves that can be considered as the ultimate money.

RSS Feed

RSS Feed