I do not claim to be an expert on the Austrian economics, but I do know enough that the Austrian theory of the business cycle, at least in its crudest form, is seriously flawed. Just to be clear, I am not claiming that misallocations of capital and asset price bubbles cannot occur. I think the housing bubble in the U.S. as well as the housing bubbles in Southern Europe show that asset prices can substantially deviate from fundamentals in the short-run. Moreover, those experiences also reveal that capital can excessively flow into an unproductive sector of the economy because it chases after short-run returns. The Austrian theory puts a lot of emphasis on misaligned incentives, which to some extent is definitely true, as shown by the issuance of so-called “NINJA” loans (no job, no income, no asset), for example. These were loans issued by banks in the U.S. to the poorest members of society, where the house bought with the loan would serve itself as the underlying collateral. This scheme worked out fine as long as house prices were on the rise, but was ultimately doomed once the necessary price correction took place. However, the most important aspect of these asset bubbles, in my opinion, is related to the phenomenon of global imbalances in international capital flows. It is worth noting that those imbalances increased sharply during the decade before the crisis. More specifically, there was an excess savings over investment in South-East Asia and some parts of Northern Europe. The result were increasing capital flows into the US and Europe and the buildup of domestic asset bubbles, especially in housing.

The most incorrect statement one often encounters in Austrian readings is that an economic depression is the necessary adjustment that occurs in response to the previous misallocation of capital. Furthermore, any interference in this natural process is considered to be bad as it simply increases the misallocation of resources further and thus only delays the necessary adjustment mechanism. Not only is this view plain wrong, but also outright dangerous. The Great Recession has shown how costly economic depressions are in terms of economic welfare. Millions of people still suffer from excessive unemployment in the eurozone where economic growth has been abysmal ever since the outbreak of the financial crisis. Macroeconomic stabilization policies are of the upmost importance precisely because recessions are extremely costly.

In his book “The theory of economic development” from 1924, Joseph Schumpeter outlines a theory of economic development in which he describes the mechanism of economic growth. He also briefly discusses recessions, which is in my opinion the weakest part of his book since his views are somewhat similar to the crude Austrian theory described above where an economic downturn is considered to be a natural and healthy process not to be interfered with.

In what follows, I will thus mostly restrict myself to the more interesting points he makes about long-run economic development. Amazingly, some of the processes of economic growth described by Schumpeter in his work from 1924 were only formalized and incorporated into mathematical models by modern growth theorists in the 1980s and 1990s (so-called endogenous growth), that is some 70 years after Schumpeter laid out his original ideas.

At the core of the process of economic development is, according to Schumpeter, the entrepreneur. He is the innovator who pushes the economy forward. He uses his intellect to invent a new method of production or a new product. Even though the notion of “creative destruction”, the idea Schumpeter is arguably most known for, is not mentioned in this book yet, the rough idea is already very much present. Schumpeter argues that old industries are eventually bound to disappear if superior production methods and/or products are invented by the entrepreneur. Economic welfare is bound to increase as entrepreneurs divert resources from outdated production methods to more efficient ones. Innovation is thus the key process producing economic development, pushing the economy away from its old equlibrium towards a new one.

Entrepreneurial profit plays a key part in Schumpeter’s theory of economic development. The profit arises through a temporary position of monopoly power. But in Schumpeter’s analysis, monopoly power is actually desirable. It is a necessity for economic development because it is the lure of large potential economic profits that make entrepreneurs carry out research and development activities in the first place. Over time, monopoly profits eventually erode as other economic agents increasingly enter the markets where such profits are to be found, thereby eliminating the monopoly position that previously existed. This economic mechanism of course provides a rational for patents, which are effectively a monopoly position granted by the state to an entrepreneur for a specified period so that he can reap the financial benefits of his innovation. Patents thus provide individuals an incentive to carry out innovative activities as they assure that the financial reward will not be diluted immediately by copycat behavior.

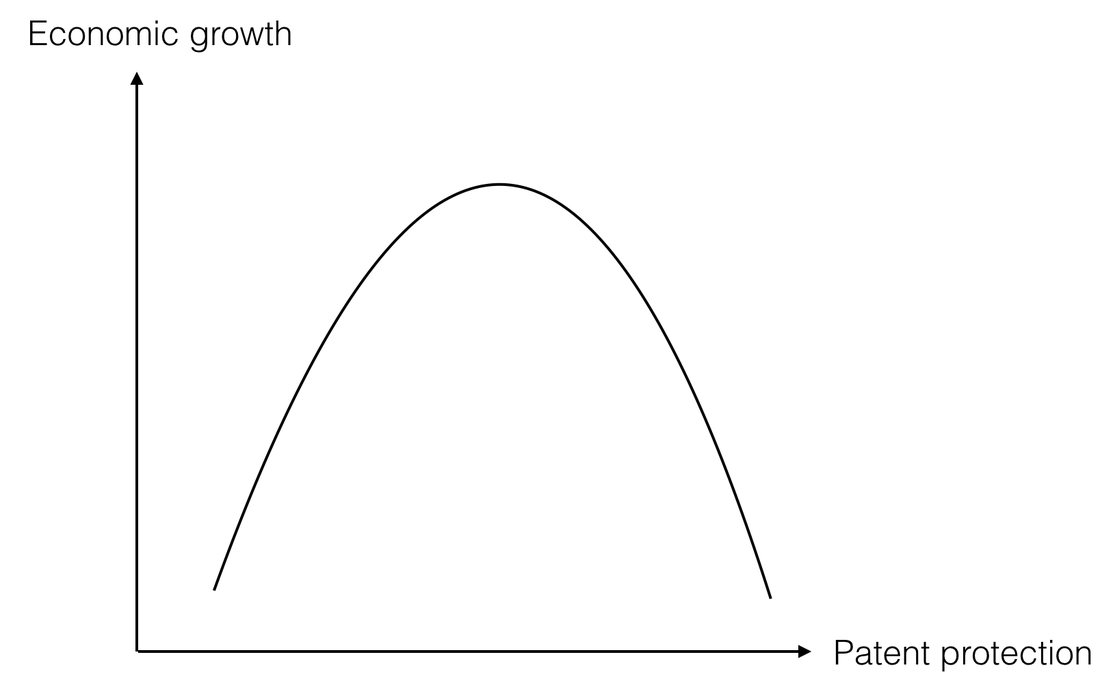

Modern Schumpeterian growth models mimic the process described above: The growth rate is commonly an increasing function of entrepreneurial profit, and thus also indirectly an increasing function of patent protection (see Aghion, Akcigit and and Howitt's research paper on endogenous growth theory http://scholar.harvard.edu/fi les/aghion/files/what_do_we_learn_0.pdf?m=1361377935). In reality, of course, policymakers face a certain trade-off. If the state creates a patent system where protection is extravagant, it effectively grants entrepreneurs the right to create and maintain a monopoly position for an excessively long period. And an economy characterized by a high degree of market power is likely to perform worse in the long-run. If on the other hand patent protection is virtually non-existent, the incentives to carry out innovative activities are reduced, which will also come at the expense of economic growth. For that reason, one can easily imagine an inverse U-shaped relationship between patent protection and economic growth (as depicted below), meaning that policy makers have to find the right balance between a too stingy and too generous patent system. Some modern endogenous growth models have modelled this non-linear relationship between growth and patent right protection (see the paper by Arcs & Sanders, 2012).

The most incorrect statement one often encounters in Austrian readings is that an economic depression is the necessary adjustment that occurs in response to the previous misallocation of capital. Furthermore, any interference in this natural process is considered to be bad as it simply increases the misallocation of resources further and thus only delays the necessary adjustment mechanism. Not only is this view plain wrong, but also outright dangerous. The Great Recession has shown how costly economic depressions are in terms of economic welfare. Millions of people still suffer from excessive unemployment in the eurozone where economic growth has been abysmal ever since the outbreak of the financial crisis. Macroeconomic stabilization policies are of the upmost importance precisely because recessions are extremely costly.

In his book “The theory of economic development” from 1924, Joseph Schumpeter outlines a theory of economic development in which he describes the mechanism of economic growth. He also briefly discusses recessions, which is in my opinion the weakest part of his book since his views are somewhat similar to the crude Austrian theory described above where an economic downturn is considered to be a natural and healthy process not to be interfered with.

In what follows, I will thus mostly restrict myself to the more interesting points he makes about long-run economic development. Amazingly, some of the processes of economic growth described by Schumpeter in his work from 1924 were only formalized and incorporated into mathematical models by modern growth theorists in the 1980s and 1990s (so-called endogenous growth), that is some 70 years after Schumpeter laid out his original ideas.

At the core of the process of economic development is, according to Schumpeter, the entrepreneur. He is the innovator who pushes the economy forward. He uses his intellect to invent a new method of production or a new product. Even though the notion of “creative destruction”, the idea Schumpeter is arguably most known for, is not mentioned in this book yet, the rough idea is already very much present. Schumpeter argues that old industries are eventually bound to disappear if superior production methods and/or products are invented by the entrepreneur. Economic welfare is bound to increase as entrepreneurs divert resources from outdated production methods to more efficient ones. Innovation is thus the key process producing economic development, pushing the economy away from its old equlibrium towards a new one.

Entrepreneurial profit plays a key part in Schumpeter’s theory of economic development. The profit arises through a temporary position of monopoly power. But in Schumpeter’s analysis, monopoly power is actually desirable. It is a necessity for economic development because it is the lure of large potential economic profits that make entrepreneurs carry out research and development activities in the first place. Over time, monopoly profits eventually erode as other economic agents increasingly enter the markets where such profits are to be found, thereby eliminating the monopoly position that previously existed. This economic mechanism of course provides a rational for patents, which are effectively a monopoly position granted by the state to an entrepreneur for a specified period so that he can reap the financial benefits of his innovation. Patents thus provide individuals an incentive to carry out innovative activities as they assure that the financial reward will not be diluted immediately by copycat behavior.

Modern Schumpeterian growth models mimic the process described above: The growth rate is commonly an increasing function of entrepreneurial profit, and thus also indirectly an increasing function of patent protection (see Aghion, Akcigit and and Howitt's research paper on endogenous growth theory http://scholar.harvard.edu/fi les/aghion/files/what_do_we_learn_0.pdf?m=1361377935). In reality, of course, policymakers face a certain trade-off. If the state creates a patent system where protection is extravagant, it effectively grants entrepreneurs the right to create and maintain a monopoly position for an excessively long period. And an economy characterized by a high degree of market power is likely to perform worse in the long-run. If on the other hand patent protection is virtually non-existent, the incentives to carry out innovative activities are reduced, which will also come at the expense of economic growth. For that reason, one can easily imagine an inverse U-shaped relationship between patent protection and economic growth (as depicted below), meaning that policy makers have to find the right balance between a too stingy and too generous patent system. Some modern endogenous growth models have modelled this non-linear relationship between growth and patent right protection (see the paper by Arcs & Sanders, 2012).

Another key part of Schumpeter’s theory is the aspect that economic growth is a non-linear process. Indeed, most neoclassical growth models describe growth as an even and balanced process, a proposition Schumpeter would have vehemently rejected. According to him, innovations usually occur in swarms and are thus not spread out evenly over time. That is because innovative activities are not independent of each other. Entrepreneurs appear in clusters because one innovative activity facilitates the other. Schumpeter thus clearly refers to what in modern economic parlance is called spillover effects, i.e. a type of externality where the productivity of one firm affects the productivity of other firms nearby. There are many real-life examples which show that such factors are of the upmost importance. Silicon Valley would not exist if spillover effects are negligible. Theoretically, high-tech firms could operate from almost anywhere in the industrialized world, given that a a certain amount of infrastructure is provided. As matter of fact though many high-tech firms are founded and choose to operate out of Silicon Valley even though rents and labor costs are excessively high. These negative aspects, however, seem to be outweighed by the advantage of simply being located nearby many other firms in the same industry (ideas still seem to spread locally first despite the phenomenon of globalization), thus also having access to the same kind of infrastructure (lawyers, financiers and a skilled labor pool catered to the specific industry at hand).

Schumpeter’s claim that innovations appear in swarms is also at the core of his explanation for the business cycle. The clustering of innovations produces cycles (waves) of economic development. A boom occurs in a period where many innovations occur at the same time. Bank lending increases as the banking system provides the entrepreneurs with credit. However, the effect of credit creation will also spread to secondary markets (the labor market, consumer markets) that are only loosely related to the innovative sector. The ad-hoc creation of purchasing power by the banking system will be felt economy-wide and puts upward pressure on prices and wages, in general.

In Schumpeter’s theory, the boom is necessarily followed by a bust. There is a general slowdown of innovations and entrepreneurs start to pay back their loans from the income streams they received from previous innovations. This will lead to a credit deflation, the disappearance of previously produced purchasing power. The bust is often accompanied by banking crises and falling asset prices.

I think Schumpeter's analysis of the business cycle is by far the most problematic part of his theory. Standard macroeconomics suggests that the government, or more specifically the Central Banks, can and should tame the business cycle. Indeed, the period of the Great Moderation that lasted from the mid-1980s until the financial crisis is probably the prime example. This era was characterized by very low volatility in both inflation and, more importantly, output growth. The FED essentially tamed the business cycle by ensuring that the economy’s total nominal income would grow along a relatively smooth and stable path. This, of course, would not eliminate cycles in innovation. Central Banks obviously do not have any control over entrepreneurial activity (or at least not in any direct meaningful sense). We would thus still observe wave-like movements in innovation, such as the IT-boom in the 1990s where productivity growth sharply accelerated and the subsequent slowdown in the 2000s. However, in contrast to Schumpeter’s theory, long-term accelerations and decelerations of innovative activity and thus productivity growth should not cause major boom and bust cycles if the macroeconomy is properly managed by the Central Bank, i.e. if stabilization and macroprudential policies are effective (presumably a big IF as we have seen in recent years).

So how should we think about long-term cycles in modern growth models?

There are several different mechanism that can create Schumpeterian waves. One should note that these models should be seen as complimentary to each.

Andergassen and Nardini (2005) suggest a model where cycles arise from innovation waves. These waves are generated because there are spillover effects between different sectors of the economy. Innovations in one sector can clearly generate subsequent rounds of innovations as information and new knowledge spreads throughout the economy. This is clearly in line with Schumpeter’s idea that innovative activities are not independent of each other and that a new innovation often appears in one industry first and then spreads from there. Entrepreneurial activities will therefore appear en masse and this will create the cyclical movements previously mentioned.

Bambi et al. (2014) develop a model that displays Schumpeterian waves because there is an implementation lag between the inception of an idea and the implementation and adoption of the associated innovations. Again, this process is already described in Schumpeter’s writing. He emphasizes that there is a crucial distinction between inventions and innovations. Inventions are irrelevant to economic development if they are not carried out into practice. An innovation on the other hand is the application of a new idea to an economic problem. They are the key driver of economic development. The paper by Bambi et al. (2014) describes a process in which research and development activities are time-consuming. The implementation delay between the development phase of a new innovation and its final implementation creates cyclical movements in economic growth.

Last but not least, cyclical movements can arise through the emergence of a General Purpose Technology (GPT). A GPT is a technology that affects the entire macroeconomy and alters society through its impact on pre-existing economic structures. Electricity and the internet are very good examples. Both technologies have ultimately affected every single sector of the economy. The adoption of a new GPT might actually lead to a a general economic slowdown at first. That is because the old capital stock becomes obsolete with the introduction of the new technology and therefore has to be replaced. Furthermore, workers might have to augment their skills first to adapt to the challenges the new technology poses. The adjustment of the capital stock and the training of the labor force both take some time, meaning that productivity might actually slow down at first once the new technology is introduced. However, eventually the GPT spreads throughout the entire economy. There will be a growth spurt (productivity boom) once the technology is adopted by the majority of industries and businesses. One should note that the cycles that are produced by the invention of GPT play out on a different time horizon. The cyclical movements mentioned previously are rather medium term (5-10 years) whereas GPTs can induce cyclical movements that last for decades. Jovanovic and Rousseau (2005) document a more than decade-long productivity slowdown when electricity was first adopted in the United States around 1900. Productivity acceleration only occurred in the 1920s when the technology started to spread throughout the economy. Internet technologies provide another example that is consistent with the theoretical framework of a GPT technology where one could observe an initial phase of low productivity in the 1980s and subsequent acceleration during the IT boom of the 1990s. So GPTs can produce extremely long cycles which might superimpose themselves on short run and medium-run fluctuations. The IT boom, for example, seems to have petered out over the last decade as global productivity growth has decelerated sharply. This might obviously be only a short-run phenomenon, but there is no way to predict the next major breakthrough in technology and how it will affect future economic growth (and any claims to the contrary should be taken with a grain of salt).

So to conclude, while I disagree with Schumpeter’s analysis of the business cycle, his ideas about long-term economic development remain highly relevant today. Indeed, modern growth economists only managed to incorporate elements like Schumpeterian cycles into modern growth models some 70 years after he initially laid out his thoughts on long-term economic development.

PS: For more information on Schumpeter, this is a very interesting podcaston Econtalk I highly recommend http://www.econtalk.org/archives/2007/10/mccraw_on_schum.html.

Schumpeter’s claim that innovations appear in swarms is also at the core of his explanation for the business cycle. The clustering of innovations produces cycles (waves) of economic development. A boom occurs in a period where many innovations occur at the same time. Bank lending increases as the banking system provides the entrepreneurs with credit. However, the effect of credit creation will also spread to secondary markets (the labor market, consumer markets) that are only loosely related to the innovative sector. The ad-hoc creation of purchasing power by the banking system will be felt economy-wide and puts upward pressure on prices and wages, in general.

In Schumpeter’s theory, the boom is necessarily followed by a bust. There is a general slowdown of innovations and entrepreneurs start to pay back their loans from the income streams they received from previous innovations. This will lead to a credit deflation, the disappearance of previously produced purchasing power. The bust is often accompanied by banking crises and falling asset prices.

I think Schumpeter's analysis of the business cycle is by far the most problematic part of his theory. Standard macroeconomics suggests that the government, or more specifically the Central Banks, can and should tame the business cycle. Indeed, the period of the Great Moderation that lasted from the mid-1980s until the financial crisis is probably the prime example. This era was characterized by very low volatility in both inflation and, more importantly, output growth. The FED essentially tamed the business cycle by ensuring that the economy’s total nominal income would grow along a relatively smooth and stable path. This, of course, would not eliminate cycles in innovation. Central Banks obviously do not have any control over entrepreneurial activity (or at least not in any direct meaningful sense). We would thus still observe wave-like movements in innovation, such as the IT-boom in the 1990s where productivity growth sharply accelerated and the subsequent slowdown in the 2000s. However, in contrast to Schumpeter’s theory, long-term accelerations and decelerations of innovative activity and thus productivity growth should not cause major boom and bust cycles if the macroeconomy is properly managed by the Central Bank, i.e. if stabilization and macroprudential policies are effective (presumably a big IF as we have seen in recent years).

So how should we think about long-term cycles in modern growth models?

There are several different mechanism that can create Schumpeterian waves. One should note that these models should be seen as complimentary to each.

Andergassen and Nardini (2005) suggest a model where cycles arise from innovation waves. These waves are generated because there are spillover effects between different sectors of the economy. Innovations in one sector can clearly generate subsequent rounds of innovations as information and new knowledge spreads throughout the economy. This is clearly in line with Schumpeter’s idea that innovative activities are not independent of each other and that a new innovation often appears in one industry first and then spreads from there. Entrepreneurial activities will therefore appear en masse and this will create the cyclical movements previously mentioned.

Bambi et al. (2014) develop a model that displays Schumpeterian waves because there is an implementation lag between the inception of an idea and the implementation and adoption of the associated innovations. Again, this process is already described in Schumpeter’s writing. He emphasizes that there is a crucial distinction between inventions and innovations. Inventions are irrelevant to economic development if they are not carried out into practice. An innovation on the other hand is the application of a new idea to an economic problem. They are the key driver of economic development. The paper by Bambi et al. (2014) describes a process in which research and development activities are time-consuming. The implementation delay between the development phase of a new innovation and its final implementation creates cyclical movements in economic growth.

Last but not least, cyclical movements can arise through the emergence of a General Purpose Technology (GPT). A GPT is a technology that affects the entire macroeconomy and alters society through its impact on pre-existing economic structures. Electricity and the internet are very good examples. Both technologies have ultimately affected every single sector of the economy. The adoption of a new GPT might actually lead to a a general economic slowdown at first. That is because the old capital stock becomes obsolete with the introduction of the new technology and therefore has to be replaced. Furthermore, workers might have to augment their skills first to adapt to the challenges the new technology poses. The adjustment of the capital stock and the training of the labor force both take some time, meaning that productivity might actually slow down at first once the new technology is introduced. However, eventually the GPT spreads throughout the entire economy. There will be a growth spurt (productivity boom) once the technology is adopted by the majority of industries and businesses. One should note that the cycles that are produced by the invention of GPT play out on a different time horizon. The cyclical movements mentioned previously are rather medium term (5-10 years) whereas GPTs can induce cyclical movements that last for decades. Jovanovic and Rousseau (2005) document a more than decade-long productivity slowdown when electricity was first adopted in the United States around 1900. Productivity acceleration only occurred in the 1920s when the technology started to spread throughout the economy. Internet technologies provide another example that is consistent with the theoretical framework of a GPT technology where one could observe an initial phase of low productivity in the 1980s and subsequent acceleration during the IT boom of the 1990s. So GPTs can produce extremely long cycles which might superimpose themselves on short run and medium-run fluctuations. The IT boom, for example, seems to have petered out over the last decade as global productivity growth has decelerated sharply. This might obviously be only a short-run phenomenon, but there is no way to predict the next major breakthrough in technology and how it will affect future economic growth (and any claims to the contrary should be taken with a grain of salt).

So to conclude, while I disagree with Schumpeter’s analysis of the business cycle, his ideas about long-term economic development remain highly relevant today. Indeed, modern growth economists only managed to incorporate elements like Schumpeterian cycles into modern growth models some 70 years after he initially laid out his thoughts on long-term economic development.

PS: For more information on Schumpeter, this is a very interesting podcaston Econtalk I highly recommend http://www.econtalk.org/archives/2007/10/mccraw_on_schum.html.

Sources:

- Acs, Zoltan J., and Mark Sanders. "Patents, knowledge spillovers, and entrepreneurship." Small Business Economics 39.4 (2012): 801-817. http://link.springer.com/article/10.1007%2Fs11187-011-9322-y

- Andergassen, Rainer, and Franco Nardini. "Endogenous innovation waves and economic growth." Structural Change and Economic Dynamics 16.4 (2005): 522-539. http://www2.dse.unibo.it/wp/446.pdf

- Bambi, Mauro, Fausto Gozzi, and Omar Licandro. "Endogenous growth and wave-like business fluctuations." Journal of Economic Theory 154 (2014): 68-111. http://www.iae.csic.es/investigatorsMaterial/a122510095331archivoPdf1110.pdf

- Aghion, Akcigit and Howitt (2013): What do we learn from Schumpeterian growth theory? http://scholar.harvard.edu/files/aghion/files/what_do_we_learn_0.pdf?m=1361377935

- Jovanovic, Boyan, and Peter L. Rousseau. "General purpose technologies." Handbook of economic growth 1 (2005): 1181-1224.

- Schumpeter, Joseph Alois. The theory of economic development: An inquiry into profits, capital, credit, interest, and the business cycle. Vol. 55. Transaction publishers, 1934.

RSS Feed

RSS Feed