Ever since the beginning of the crisis a lot of so-called experts and policy makers have been asking themselves, looking for various explanations, why the economic recovery has been so slow during the last couple of years. This is a very sad state of affairs since standard macroeconomics can explain the current economic stagnation fairly well.

The economic expansion before 2008 was to some extent driven by the ‘wealth effect’. Very high housing prices in the U.S. and some other countries meant that many households felt wealthier than they really were and went on a largely debt-driven consumption spree. The financial crisis of 2008 and the associated large drop in asset prices implied that the private sector, households and companies alike, had to deleverage and pay back their debts. The private sector thus started to contract as households and companies increased their savings dramatically. For a while governments engaged in fiscal stimulus, but they were only short-lived and rather small in size. Furthermore, debt phobia soon kicked in and governments started to rein in public spending. While the private sector still suffered from enormous debt overhang and continued to deleverage, governments in the Eurozone and the U.S. started to engage in fiscal austerity from 2010 onwards. The obvious consequence was, of course, that the economy as a whole contracted as both private sector and public spending fell.

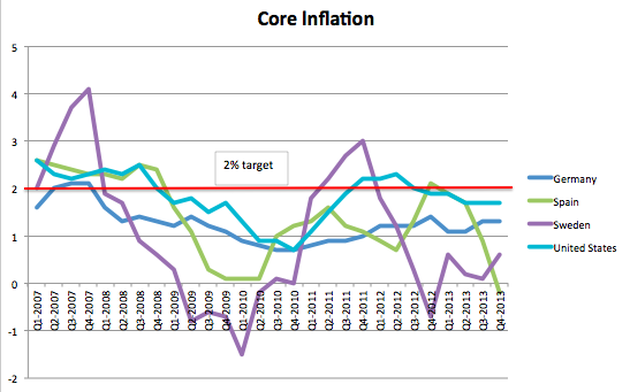

Indeed, it is quite amazing how policy makers in many industrial countries did exactly the opposite of what the standard macro textbook prescribes, with the obvious consequence of economic stagnation. There are effectively two enormous ‘free lunches’ that policy makers have failed to pick up over the last couple of years. For starters, monetary policy has been extremely restrictive in most industrialized countries with inflation largely falling short of the Central Banks’ own target. Notice how core inflation, which excludes energy and food prices, has fallen short of the ECB’s 2% target not only in the troubled economy of Spain but also in Germany (the reason why Central Banks should focus on core inflation only is that energy and food prices are highly volatile in nature and thus very ‘noisy’). This is, of course, highly problematic since low inflation increases the real value of debt and thus further depresses aggregate demand, as consumers have to curb their spending. In fact, many Eurozone countries suffer already from ‘Fisherian debt deflation’. Households and companies, but also governments, have an increasingly hard time to honor their debt obligations, which are in nominal terms, in an environment of falling prices.

The economic expansion before 2008 was to some extent driven by the ‘wealth effect’. Very high housing prices in the U.S. and some other countries meant that many households felt wealthier than they really were and went on a largely debt-driven consumption spree. The financial crisis of 2008 and the associated large drop in asset prices implied that the private sector, households and companies alike, had to deleverage and pay back their debts. The private sector thus started to contract as households and companies increased their savings dramatically. For a while governments engaged in fiscal stimulus, but they were only short-lived and rather small in size. Furthermore, debt phobia soon kicked in and governments started to rein in public spending. While the private sector still suffered from enormous debt overhang and continued to deleverage, governments in the Eurozone and the U.S. started to engage in fiscal austerity from 2010 onwards. The obvious consequence was, of course, that the economy as a whole contracted as both private sector and public spending fell.

Indeed, it is quite amazing how policy makers in many industrial countries did exactly the opposite of what the standard macro textbook prescribes, with the obvious consequence of economic stagnation. There are effectively two enormous ‘free lunches’ that policy makers have failed to pick up over the last couple of years. For starters, monetary policy has been extremely restrictive in most industrialized countries with inflation largely falling short of the Central Banks’ own target. Notice how core inflation, which excludes energy and food prices, has fallen short of the ECB’s 2% target not only in the troubled economy of Spain but also in Germany (the reason why Central Banks should focus on core inflation only is that energy and food prices are highly volatile in nature and thus very ‘noisy’). This is, of course, highly problematic since low inflation increases the real value of debt and thus further depresses aggregate demand, as consumers have to curb their spending. In fact, many Eurozone countries suffer already from ‘Fisherian debt deflation’. Households and companies, but also governments, have an increasingly hard time to honor their debt obligations, which are in nominal terms, in an environment of falling prices.

Unfortunately, the general public is often quite confused about the issue of inflation and falsely believes it benefits from low inflation because it raises real disposable incomes. This, however, is utterly wrong since it confuses real and nominal factors. Low inflation over the last years did not come from the supply side (i.e. lower commodity prices) but from the demand side. Lower energy prices do indeed increase real incomes, all else equal, but the low inflation rates over the last few years are the result of insufficient nominal spending in the economy and are thus a demand-side phenomenon. Were the Central Bank to increase aggregate demand, then prices would rise but so would real GDP, at least as long as the economy operates below potential. The split between higher prices and higher real income depends on the slope of the short-run aggregate supply curve (SRAS). There are reasons to believe that the SRAS curve is relatively flat at low levels of inflation, because of nominal wage rigidity, for example (http://krugman.blogs.nytimes.com/2012/04/08/unemployment-and-inflation/).

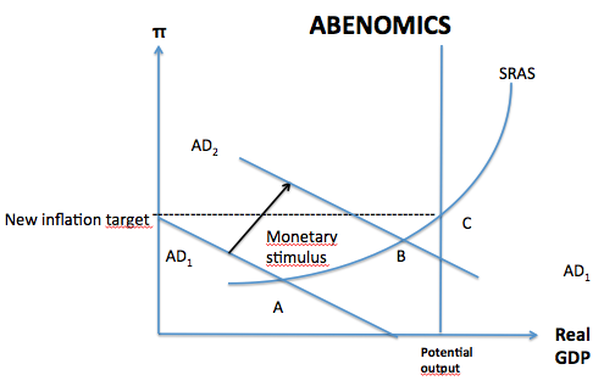

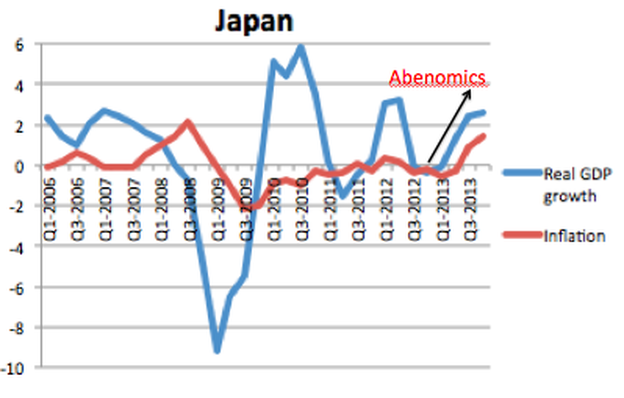

This means that an increase in aggregate demad (AD) will actually greatly increase real income and only somewhat lead to higher rates of inflation. Indeed, this is exactly what we observed in Japan with the introduction of ‘Abenomics’ where the monetary stimulus has been a great success. This magnificent paper by Hausman and Wieland is an investigation into the Bank of Japan’s (BoJ) decision to change their monetary policy regime and finally follows Krugman’s advice, with a delay of roughly 15 years. The paper estimates that the increase in the inflation target to 2% and the initiation to engage in large-scale asset purchases to achieve that target raised Japanese real GDP in 2013 by roughly 1%. Despite its success, the inflation target of 2% is, however, not yet fully credible and Japanese inflation rates still fall somewhat short of target. The Japanese economy is thus likely at point B in my figure below (http://www.brookings.edu/about/projects/bpea/papers/2014/abenomics-preliminary-analysis-and-outlook).

This means that an increase in aggregate demad (AD) will actually greatly increase real income and only somewhat lead to higher rates of inflation. Indeed, this is exactly what we observed in Japan with the introduction of ‘Abenomics’ where the monetary stimulus has been a great success. This magnificent paper by Hausman and Wieland is an investigation into the Bank of Japan’s (BoJ) decision to change their monetary policy regime and finally follows Krugman’s advice, with a delay of roughly 15 years. The paper estimates that the increase in the inflation target to 2% and the initiation to engage in large-scale asset purchases to achieve that target raised Japanese real GDP in 2013 by roughly 1%. Despite its success, the inflation target of 2% is, however, not yet fully credible and Japanese inflation rates still fall somewhat short of target. The Japanese economy is thus likely at point B in my figure below (http://www.brookings.edu/about/projects/bpea/papers/2014/abenomics-preliminary-analysis-and-outlook).

After the economic shock of 2008, many economies operated far below potential. Instead of pursuing extremely tight monetary policy, Central Banks should have at least tried to hit the inflation target, on average. Indeed, there is actually overwhelming rationale for temporary ‘overshooting’ (of the inflation target) to get the economy back to potential as fast as possible because of large hysteresis effects: The shadow that is cast on future potential output as the long-term unemployed become detached from the labor force and as investment rates remain depressed as a result of the crisis. Since printing money is basically costless, monetary stimulus in the face of the biggest shortfall in aggregated demand since the Great Depression in the 1930s is the first big free lunch that policy makers failed to pick up.

The second free lunch has been the inability of policy makers to increase public spending, which easily would have passed any sensible cost-benefit analysis. Consider public investments in infrastructure that governments will have to undertake IN ANY CASE during the next 10 to 20 years. Obviously, it would have made sense to bring these expenditures forward in time and do them right now when most governments can borrow at record-low interest rates rather than delaying these expenditures for a few years. That is because when the economy returns back to normal, interest rates will normalize as well so that the cost of these public investments will actually be much higher. So even in the absence of multiplier and hysteresis effects, investments in public infrastructure would have made sense from a cost-benefit analysis viewpoint. But in addition to that, fiscal multipliers have been estimated to be largely above one in recent years and hysteresis effects prove to be very significant: Once being unemployed for several months, it becomes very difficult and for many even close to impossible to reintegrate in to the labor force and find adequate jobs (http://www.brookings.edu/~/media/Projects/BPEA/Spring%202012/2012a_DeLong.pdf).

The size of the fiscal multiplier and the cast on future output from hysteresis effects imply that any fiscal stimulus in recent years actually could potentially even have been self-financing. In the medium to long-run, the debt-to-GDP ratio would have actually been lower in that case than in the absence of such public expenditures. This somewhat counterintuitive proposition seems to be largely supported by the experience of Southern Europe where austerity measures have increased the debt levels significantly (as a ratio of GDP) instead of reducing them. That is because for every Euro decreased in public expenditures total economic output actually fell by more than 1 Euro. Contraction in the private sector thus also led to contraction in public sector as economy-wide spending fell. Consequently, debt-to-GDP ratios in Southern Europe soared as a result of austerity, and ironically, would actually be lower in the absence of public spending cuts.

So fiscal expansion, that likely would have paid for itself by significantly boosting employment and economic growth and thus also government tax revenues, is the second big free lunch government officials failed to pick up, at the expense of the economy and the well being of the people.

So the economic stagnation in recent years is pretty self-explanatory. The private sector had to deleverage after the financial shock of 2008. Monetary policy, instead of being accommodative and support the economy’s process of rebalancing, was extremely tight in many countries in recent years. Finally, fiscal contraction proved to be final nail in the economy’s coffin, so to speak. Poor economic performance since 2008 can thus mostly be explained by low nominal spending, Many countries suffered from low aggregate demand and were effectively hit by a succession of negative demand shocks since 2008, such as government spending cuts, the ECB’s decision to raise interest rates prematurely in 2011, and so on.

Obviously, at some point in time the economy is expected to normalize even in the presence of continuous negative aggregate demand shocks. The recent recovery in Europe is really not a vindication that austerity has worked, far from it. Standard Macro suggests that the economy will recover eventually. So even without economic stimulus the economy would basically move along the SRAS curve from point A to point C in my figure above and return to potential output in the long run. This adjustment process, however, can be very lengthy and take up to several years. Again, the Eurozone experience is highly consistent with that proposition, thus the need for short-run stabilization policies

In the past, many recessions thus proved to be rather temporary and the economy returns to full employment within several quarters. The current crisis has been much larger in magnitude and duration. However, many observers believe that advanced economies are now quickly recovering, even Eurozone countries start to show signs of growth, and that we will reach potential output and full employment soon. Unfortunately, the very smart Lawrence Summers is more pessimistic on this particular topic. Last November, he gave a very influential and highly controversial speech at an IMF conference in which he put forward the idea that the U.S. economy experiences ‘secular stagnation’. The basic idea behind secular stagnation is that an economy might be permanently demand-constrained and that economic growth might actually be insufficient to reach full employment also in the LONG RUN.

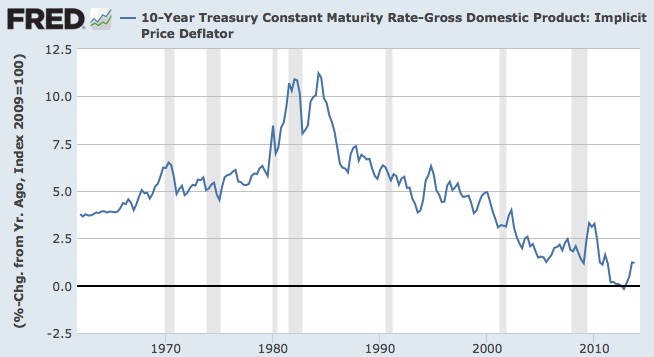

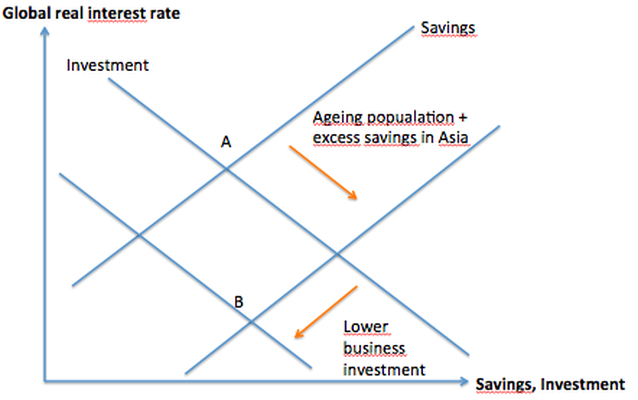

What worries Summers is the global downward trend in real interest rates that has taken place over the last two decades (see figure below in which I plotted the real rate for the U.S., which can be seen as a rough proxy for the global real interest rate since the U.S. is by far the largest economy and capital mobility implies that risk-adjusted returns net of transaction costs are equalized).

The second free lunch has been the inability of policy makers to increase public spending, which easily would have passed any sensible cost-benefit analysis. Consider public investments in infrastructure that governments will have to undertake IN ANY CASE during the next 10 to 20 years. Obviously, it would have made sense to bring these expenditures forward in time and do them right now when most governments can borrow at record-low interest rates rather than delaying these expenditures for a few years. That is because when the economy returns back to normal, interest rates will normalize as well so that the cost of these public investments will actually be much higher. So even in the absence of multiplier and hysteresis effects, investments in public infrastructure would have made sense from a cost-benefit analysis viewpoint. But in addition to that, fiscal multipliers have been estimated to be largely above one in recent years and hysteresis effects prove to be very significant: Once being unemployed for several months, it becomes very difficult and for many even close to impossible to reintegrate in to the labor force and find adequate jobs (http://www.brookings.edu/~/media/Projects/BPEA/Spring%202012/2012a_DeLong.pdf).

The size of the fiscal multiplier and the cast on future output from hysteresis effects imply that any fiscal stimulus in recent years actually could potentially even have been self-financing. In the medium to long-run, the debt-to-GDP ratio would have actually been lower in that case than in the absence of such public expenditures. This somewhat counterintuitive proposition seems to be largely supported by the experience of Southern Europe where austerity measures have increased the debt levels significantly (as a ratio of GDP) instead of reducing them. That is because for every Euro decreased in public expenditures total economic output actually fell by more than 1 Euro. Contraction in the private sector thus also led to contraction in public sector as economy-wide spending fell. Consequently, debt-to-GDP ratios in Southern Europe soared as a result of austerity, and ironically, would actually be lower in the absence of public spending cuts.

So fiscal expansion, that likely would have paid for itself by significantly boosting employment and economic growth and thus also government tax revenues, is the second big free lunch government officials failed to pick up, at the expense of the economy and the well being of the people.

So the economic stagnation in recent years is pretty self-explanatory. The private sector had to deleverage after the financial shock of 2008. Monetary policy, instead of being accommodative and support the economy’s process of rebalancing, was extremely tight in many countries in recent years. Finally, fiscal contraction proved to be final nail in the economy’s coffin, so to speak. Poor economic performance since 2008 can thus mostly be explained by low nominal spending, Many countries suffered from low aggregate demand and were effectively hit by a succession of negative demand shocks since 2008, such as government spending cuts, the ECB’s decision to raise interest rates prematurely in 2011, and so on.

Obviously, at some point in time the economy is expected to normalize even in the presence of continuous negative aggregate demand shocks. The recent recovery in Europe is really not a vindication that austerity has worked, far from it. Standard Macro suggests that the economy will recover eventually. So even without economic stimulus the economy would basically move along the SRAS curve from point A to point C in my figure above and return to potential output in the long run. This adjustment process, however, can be very lengthy and take up to several years. Again, the Eurozone experience is highly consistent with that proposition, thus the need for short-run stabilization policies

In the past, many recessions thus proved to be rather temporary and the economy returns to full employment within several quarters. The current crisis has been much larger in magnitude and duration. However, many observers believe that advanced economies are now quickly recovering, even Eurozone countries start to show signs of growth, and that we will reach potential output and full employment soon. Unfortunately, the very smart Lawrence Summers is more pessimistic on this particular topic. Last November, he gave a very influential and highly controversial speech at an IMF conference in which he put forward the idea that the U.S. economy experiences ‘secular stagnation’. The basic idea behind secular stagnation is that an economy might be permanently demand-constrained and that economic growth might actually be insufficient to reach full employment also in the LONG RUN.

What worries Summers is the global downward trend in real interest rates that has taken place over the last two decades (see figure below in which I plotted the real rate for the U.S., which can be seen as a rough proxy for the global real interest rate since the U.S. is by far the largest economy and capital mobility implies that risk-adjusted returns net of transaction costs are equalized).

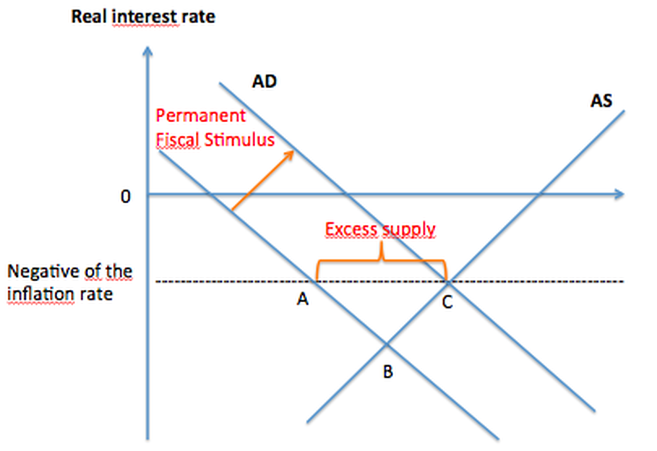

The graph above shows an unambiguous downward trend in the real interest rate, as measured by the 10-year Treasury bill minus the GDP deflator, since the mid-1980s. This is to some extent problematic for the conduct of monetary policy. The real interest rate is evidently the nominal interest rate minus the inflation rate. With Central Banks being constrained by the zero-lower bound over the last few years, the real interest in the economy is then by definition the negative of the inflation rate. It is obvious that many industrialized economies had substantial slack since 2008 and that there was an excess of aggregate supply (insufficient demand). In the U.S. case, for example, it seems that negative interest rates of maybe -4% (implying an inflation rate of 4%) for a few years would have been necessary to match aggregate demand and aggregate supply. However, low inflation rates basically put a lower bound on the negative real interest rate. The FED (and other Central Banks around the world) was unwilling/unable to generate high enough inflation rates that would have led to the negative real interest rate required to match demand and supply, restoring full employment.

SECULAR STAGNATION

The current state of affairs in which countries suffer from an insufficiency of aggregate demand might thus turn out to be of much longer duration than currently expected if the economy permanently needs a relatively large negative real interest to match demand and supply. If Central Bankers continue to oppose somewhat higher inflation and actually undershoot their own inflation target year continuously, then economies like the Eurozone could be permanently demand-constrained and as result face years/decades of stagnation with low growth rates and high unemployment (being stuck at point A in my figure above).

This trend of a falling global real interest rate thus seems to have contributed to the current economic slump and Summers fears that this condition will tend to be rather long lasting. He outlines several phenomena that seem to have contributed to the decrease in global real interest rates.

Before the crisis, Bernanke already put forward the idea of a global ‘savings glut’, as many countries around the world pursued economic polices that resulted in very high saving rates. Different groups of countries, ranging from oil exporters to China, Japan, and other South East Asian countries and also Germany, started to run large current surpluses in the beginning of the 2000s. These countries were thus basically exporting their savings to the rest of world. This phenomenon is likely to continue as populations in nations like Japan and Germany and other advanced economies will age significantly, which most likely means that these countries will have to further increase their savings.

Summers explains that at the same time as saving rates surged in many countries, the demand for investment at a given interest rate seems to have fallen in recent years.

Consider some more ‘old-fashioned’ companies like IBM or Dell, for example. These are gigantic corporations that are employing hundreds of thousands of people. They have large manufactories all around the world, invest large sums of money into R&D and spent billions of dollars in investment activities on a yearly basis. With the emergence of the new technology sector, however, the nature of investment activities has changed significantly. Nowadays, small companies like Twitter, employing less than 3000 people, can have market capitalization that can come close or even exceed the market capitalization of these more old-fashioned large corporations. The big difference though is that a company like Twitter is spending much smaller sums on business investments since it basically only requires some office space and computers for a few hundred people (I obviously oversimplify but the general argument remains valid). Furthermore, the price of capital seems to have fallen significantly over the last two decades. These structural changes imply a lower demand of business investment at a given rate of interest, shifting the investment schedule to the left.

The downward trend in real interest rates thus can be explained by higher savings rates in industrialized countries with quickly ageing populations, an excess of savings in South-East Asia, and lower investment demand from businesses (see my figure below).

This trend of a falling global real interest rate thus seems to have contributed to the current economic slump and Summers fears that this condition will tend to be rather long lasting. He outlines several phenomena that seem to have contributed to the decrease in global real interest rates.

Before the crisis, Bernanke already put forward the idea of a global ‘savings glut’, as many countries around the world pursued economic polices that resulted in very high saving rates. Different groups of countries, ranging from oil exporters to China, Japan, and other South East Asian countries and also Germany, started to run large current surpluses in the beginning of the 2000s. These countries were thus basically exporting their savings to the rest of world. This phenomenon is likely to continue as populations in nations like Japan and Germany and other advanced economies will age significantly, which most likely means that these countries will have to further increase their savings.

Summers explains that at the same time as saving rates surged in many countries, the demand for investment at a given interest rate seems to have fallen in recent years.

Consider some more ‘old-fashioned’ companies like IBM or Dell, for example. These are gigantic corporations that are employing hundreds of thousands of people. They have large manufactories all around the world, invest large sums of money into R&D and spent billions of dollars in investment activities on a yearly basis. With the emergence of the new technology sector, however, the nature of investment activities has changed significantly. Nowadays, small companies like Twitter, employing less than 3000 people, can have market capitalization that can come close or even exceed the market capitalization of these more old-fashioned large corporations. The big difference though is that a company like Twitter is spending much smaller sums on business investments since it basically only requires some office space and computers for a few hundred people (I obviously oversimplify but the general argument remains valid). Furthermore, the price of capital seems to have fallen significantly over the last two decades. These structural changes imply a lower demand of business investment at a given rate of interest, shifting the investment schedule to the left.

The downward trend in real interest rates thus can be explained by higher savings rates in industrialized countries with quickly ageing populations, an excess of savings in South-East Asia, and lower investment demand from businesses (see my figure below).

Furthermore, the global economic crisis reduced the level of aggregate demand at a given interest rate due to debt overhangs in the private sector in many advanced economies. Summers also suggests that the trend towards higher inequality in recent decades might also have reduced the level of demand at a given interest rate since the rich have a lower propensity to consume out of current income.

All these factors make it very likely that the economy is unable to reach full employment since the negative real interest matching aggregate demand and aggregate supply cannot be reached with low levels of inflation. In that case, economies might suffer from long periods of economic stagnation.

What can policy makers do to avoid this undesirable outcome?

The first and by far the least desirable option is that Central Bankers might have to engineer asset price bubbles to restore full employment in the economy. Low real interest rates do naturally increase the value of assets because future returns are discounted by less. However, it is possible that economic agents will try to ‘reach for yield’ and push prices above fundamentals in an economy in which real interest rates are permanently low.

Indeed, Summers suggests that the U.S. economy might have already experienced secular stagnation since the end of the 1990s. He observes that there were two large bubbles that developed in the 2000s, ‘Dot-Com’ first, followed by housing. However, even at the peak of both bubbles, the U.S. did not experience any significant inflationary pressures or labor shortages, implying that the economy did not suffer from significant overheating. Summers puts forward the hypothesis that the U.S. economy actually needed these two gigantic bubbles to reach full employment. Indeed, Krugman actually said back in 2002 that the FED would have to replace ‘Dot-Com’ by a housing bubble. Note that this was obviously not a policy recommendation, but rather a pretty accurate forecast of future events (http://www.nytimes.com/2002/08/02/opinion/dubya-s-double-dip.html).

The second and the most desirable policy option, according to Summers, is to raise demand at a given level of interest rate by permanent fiscal expansion, such as long-run investments into infrastructure. The economic costs of running permanently below potential are likely to be much higher than the additional debt burden resulting from increased fiscal expenditures. Furthermore, with low real interest rates, high hysteresis effects and multiplier effects (at least in the short-run), the additional debt burden is likely to be low, as argued above. Large public expenditures could thus move the economy towards point C in my 'Secular Stagnation' figure.

Finally, another option is for Central Banks to adopt the Blanchard proposal and raise the inflation target to 4% so that the negative real interest rate required to match aggregate demand and supply can be reached (point B). This would also significantly boost the economy in the short-run, especially as long as we are still below potential output. Furthermore, a higher inflation target is actually highly desirable since it reduces the chance of ending up at the zero-lower bound. The benefit from a reduced likelihood of experiencing big and nasty recessions largely seems to outweigh somewhat higher menu costs and greater relative price distortions. Another way to say this is that one big output gap is likely to be much more costly than a lot of small micro inefficiencies. There was never any overwhelming rational for the 2% inflation target anyways. Central Bankers pulled the 2%-number out of their hat in the 1990s even though economic theory suggests that a variety of alternative targets are likely superior, such as a 4% inflation target, nominal GDP target, or even a wage inflation target. See here, for example: http://mainlymacro.blogspot.se/2014/04/targeting-wage-inflation.html.

One should bear in mind that a higher inflation target does obviously not reduce real incomes in the long-run since nominal wages will increase one to one with higher inflation.

All these factors make it very likely that the economy is unable to reach full employment since the negative real interest matching aggregate demand and aggregate supply cannot be reached with low levels of inflation. In that case, economies might suffer from long periods of economic stagnation.

What can policy makers do to avoid this undesirable outcome?

The first and by far the least desirable option is that Central Bankers might have to engineer asset price bubbles to restore full employment in the economy. Low real interest rates do naturally increase the value of assets because future returns are discounted by less. However, it is possible that economic agents will try to ‘reach for yield’ and push prices above fundamentals in an economy in which real interest rates are permanently low.

Indeed, Summers suggests that the U.S. economy might have already experienced secular stagnation since the end of the 1990s. He observes that there were two large bubbles that developed in the 2000s, ‘Dot-Com’ first, followed by housing. However, even at the peak of both bubbles, the U.S. did not experience any significant inflationary pressures or labor shortages, implying that the economy did not suffer from significant overheating. Summers puts forward the hypothesis that the U.S. economy actually needed these two gigantic bubbles to reach full employment. Indeed, Krugman actually said back in 2002 that the FED would have to replace ‘Dot-Com’ by a housing bubble. Note that this was obviously not a policy recommendation, but rather a pretty accurate forecast of future events (http://www.nytimes.com/2002/08/02/opinion/dubya-s-double-dip.html).

The second and the most desirable policy option, according to Summers, is to raise demand at a given level of interest rate by permanent fiscal expansion, such as long-run investments into infrastructure. The economic costs of running permanently below potential are likely to be much higher than the additional debt burden resulting from increased fiscal expenditures. Furthermore, with low real interest rates, high hysteresis effects and multiplier effects (at least in the short-run), the additional debt burden is likely to be low, as argued above. Large public expenditures could thus move the economy towards point C in my 'Secular Stagnation' figure.

Finally, another option is for Central Banks to adopt the Blanchard proposal and raise the inflation target to 4% so that the negative real interest rate required to match aggregate demand and supply can be reached (point B). This would also significantly boost the economy in the short-run, especially as long as we are still below potential output. Furthermore, a higher inflation target is actually highly desirable since it reduces the chance of ending up at the zero-lower bound. The benefit from a reduced likelihood of experiencing big and nasty recessions largely seems to outweigh somewhat higher menu costs and greater relative price distortions. Another way to say this is that one big output gap is likely to be much more costly than a lot of small micro inefficiencies. There was never any overwhelming rational for the 2% inflation target anyways. Central Bankers pulled the 2%-number out of their hat in the 1990s even though economic theory suggests that a variety of alternative targets are likely superior, such as a 4% inflation target, nominal GDP target, or even a wage inflation target. See here, for example: http://mainlymacro.blogspot.se/2014/04/targeting-wage-inflation.html.

One should bear in mind that a higher inflation target does obviously not reduce real incomes in the long-run since nominal wages will increase one to one with higher inflation.

RSS Feed

RSS Feed