At the economic conference “Piecing together a paradigm” in Budapest organized by the Institute for New Economic Thinking (INET) Lord Adair Turner held an important speech that I found to be of more relevance than his discussion of helicopter money together with Richard Koo. In his speech, Lord Turner harshly criticized the foundations of modern macroeconomics. Most macroeconomic models that are nowadays used by Central Banks and other institutions contain highly unrealistic assumptions. William Buiter[1] and others go so far as to suggest that modern macroeconomics is pretty much useless: “…both the New Classical and New Keynesian complete markets macroeconomic theories not only did not allow the key questions about insolvency and illiquidity to be answered. They did not allow such questions to be asked. A new paradigm is needed.”

More specifically, New Keynesian DSGE (Dynamic stochastic general equilibrium) models usually contain a number of features that render them more or less useless for understanding the global financial crisis as well as the subdued recovery later on. The foundations of modern macroeconomics have been built on a number of flawed assumptions, the most important ones being listed below:

Lord Turner points out that new economic thinking, ironically, might involve reading old books. It is a sad state of affairs that an entire discipline seems to have regressed in recent decades, the dark age of macroeconomics, according to Paul Krugman[2]. He refers to the fact that a lot of concepts and old knowledge seems to have forgotten recently in the quest of finding more and more mathematically fancy but relatively useless models of the macroeconomy. The attempt to build all models on solid microfoundations has led the profession astray.

The notion that financial markets are complete is obviously ridiculous once you think a little bit more carefully about the issue. This assumption posits that we can attach a certain probability to all future states of nature and, even more importantly, that we can obtain insurance against all possible contingencies. Macroeconomic models based on Arrow-Debreu’s concept of general equilibium thus completely rule out Knightian uncertainty, the notion that some risk is simply immeasurable and consequently impossible to calculate. There is, of course, no insurance market for immeasurable risk. Financial markets will thus always be incomplete because they simply cannot provide insurance against what Nassim Taleb[3] has dubbed “Black Swans”, low-probablity, high-impact events that randomly shock the global economy.

The rationality of financial markets is, of course, another assumption that must be called into question. Robert Shiller[4] has received the Nobel prize in economics in 2013 for his recent work on speculative bubbles. He has found significant evidence for substantial mispricing of assets in financial markets in times of exuberant speculative behavior. As such, extremely high price to earnings ratios that cannot be explained by economic fundamentals are a good indicator of financial bubbles and even are to a certain extent a predictor of future returns, which should not be the case if the efficient market hyothesis were true.

The field of behavioral economics also has made enormous progress in certain areas, revealing to what extent individuals behave irrationally at times, contrary to the claim of neoclassical economics. Economists like the Nobel prize winner Daniel Kahneman[5] have extensively studied a variety of cognitive biases that indiviuals tend to display in their decision-making process in a great many situations. Unfortunately, the findings of behavioral finance and behavioral economics have not made it so far into the standard framework of macroeconomics. The most obvious problem is that irrational behavior is by definition more or less erratic, which makes it impossible for macreconomists to incorporate it into standard economic models. The solution for the field of macroeconomics so far thus has been to ignore all the aforementioned findings altogether. This, however, is not a feasible strategy for the future if modern macroeconomics wants to remain relevant for the real world instead of merely being a pseudo-science that economists quibble over in their ivory towers of academia.

Earlier generations of economists were, of course, painfully aware of some of these facts. Charles Kindleberger[6] has described in a detailed analysis the history of manias, panics and crashes in financial markets over the last couple of hundred years. Since the creation of modern financial markets in pre-industrial Europe, panics and crashes have indeed been occuring on a regular basis. Unfortunately, humans tend to have a short-term memory, thus creating the possibility for financial cycles. The excesses and the follies of the older generations are simply forgotten as new cohorts take over, believing that “this time truly is different”[7], which of course it isn’t.

The most problematic omission of modern macroeconomics, however, is the elimination of money and credit from standard models. Ever since the work of Friedman and Schwartz[8] if not before, economists have known that a substantial part of the business cycle fluctuations is due to monetary disturbances. Unfortunately, there is a branch of macroeconomics that has developed in recent decades that denies the existence of nominal shocks altogether. Real Business Cycle theory maintains that recessions are the result of technological shocks, or even more ridiculously, an increased preference for leisure. According to this logic, the Great Depression should be renamed the “Great Vacation”.

Amazingly, even the so-called New Keynesian models commonly used by Central Banks, which do not deny the existence of nominal shocks, do not contain any money, at least not explicitly. The only monetary transmission mechanism these models allow come from changes in the interest rate. The interest rate is not the price of money though, it is the price of credit and/or the return of capital (there are obviously many different interest rates in the economy, another omission made by New Keynesian models). The price of money is the inverse of the price level, i.e. how much real resources you can buy with your money. Inflation in the New Keynesian model is is usually determined by two variables only: inflation expectations as well as the size of the output gap. The Central Bank simply adjusts the interest rate in accordance with the Taylor rule, responding to deviations from the inflation target and the natural level of output. The quantity of base money in the economy as well as other broader monetary aggregates are completely left out. Monetary shocks, changes in the demand and supply for money, are thus ruled out by assumption and do not play any role in the determination of wages and prices. Milton Friedman is probably spinning in his grave.

Simple New Keynesian models also abstract from credit and liquidity constraints. This is, of course, highly problematic. “Liquidity kills you quick”, as Perry Mehrlig[9] points out. Even firms and hosueholds that are otherwise solvent can run into trouble in times of crisis if their source of income/funding dries up. During periods of acute financial distress, it might be impossible to sell what are otherwise highy valuable assets because markets are completely frozen. Furthermore, banks and other financial institutions might be unwilling to lend out any money because counterparty risk is perceived as too high. The fundamental property of credit is that it is very similar to money, but that during times of crisis its quality can quickly deteriorate. All debt is not created equal. Debt of advanced economies (which can issue their own money) is regarded as safe as it can get. Corporate debt and household debt, on the other hand, is a different story. This is what makes credit so dangerous. During good times, I might be able to issue an IOU (a debt obligation) worth 1000 dollars in order to buy goods from one merchant. He will accept my IOU if he knows that I am good for my money. More importantly, if this is common knowledge in my town, then the merchant can pass on the IOU to another person. The IOU is now a piece of paper equivalent to money, which circulates in the economy. However, this equilibrium might be fragile. During times of high economic distress people might suddenly question my solvency. The IOU is now worth much less because debt obligations are not accpeted as valid payment anymore. The only thing that now counts is “real money”, pieces of paper issued by the government (or deposits). The last person who accpeted my IOU is now literally the sucker. He can only come back to me. However, during a crisis I might now truly be liquidity constraint or even insolvent, in which case said person is sitting on a piece of paper that does not have any value. As the “quality” of debt quickly deteriorates in periods of financial distress, pieces of paper that were formerly seen as highly liquid and basically equivalent to money might suddenly become practically worthless. In such a case, the Central Bank has to assume its function as lender of last resort. The Central Bank (and the federal government) are now the only entities that can issue safe assets, money and government debt, respectively. They can issue “government money” and lend it out against collateral in order to prevent a liquidty freeze in the financial system and a total meltdown of the economy. This is to a big extent, of course, exactly what the FED did during the financial crisis of 2008/2009, and rightly so. Note, however, that such implications could not be drawn from most modern models of the economy. Instead, the prescription came more or less right out of Walter Bagehot’s[10] “Lombard Street” in which he describes London’s financial panic of 1866 as well as the somewhat tentative response of the Bank of England.

Modern macroeconomics also neglects the fact that banks can create credit “out of thin air”. Banks are obviously profit maximizers and do not operate in a vacuum. Financial instituions have to take economic conditions into account and will not expand their balance sheet ad infinitum. Regardless, the issuance of new credit involves the creation of additional purchasing power, a point that was already well understood by Schumpeter[11]. Minsky[12] wrote extensively about credit and its role in creating an unstable economy by generating a financial cycle: After a period of increasing leverage the financial bubble would burst, followed by a prolonged time of deleveraging after which the cycle would repeat itself. Rising asset prices in the buildup phase would contribute to the issuance of new credit, which in turn further supports the price appreciation of said assets.

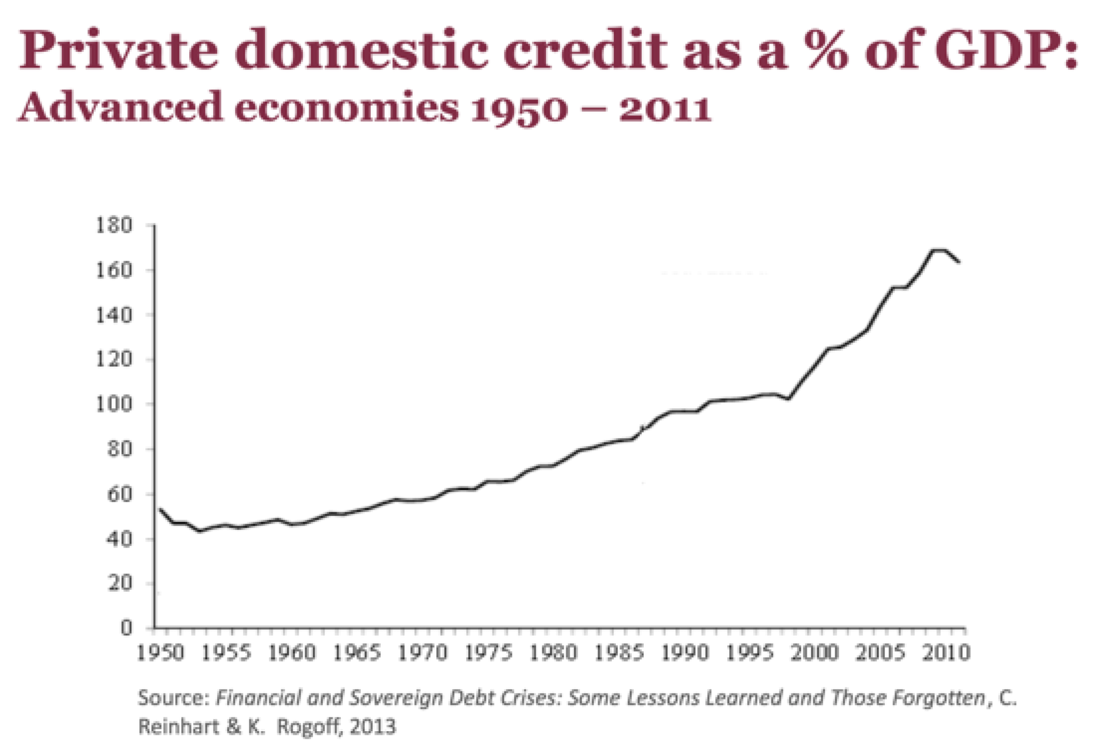

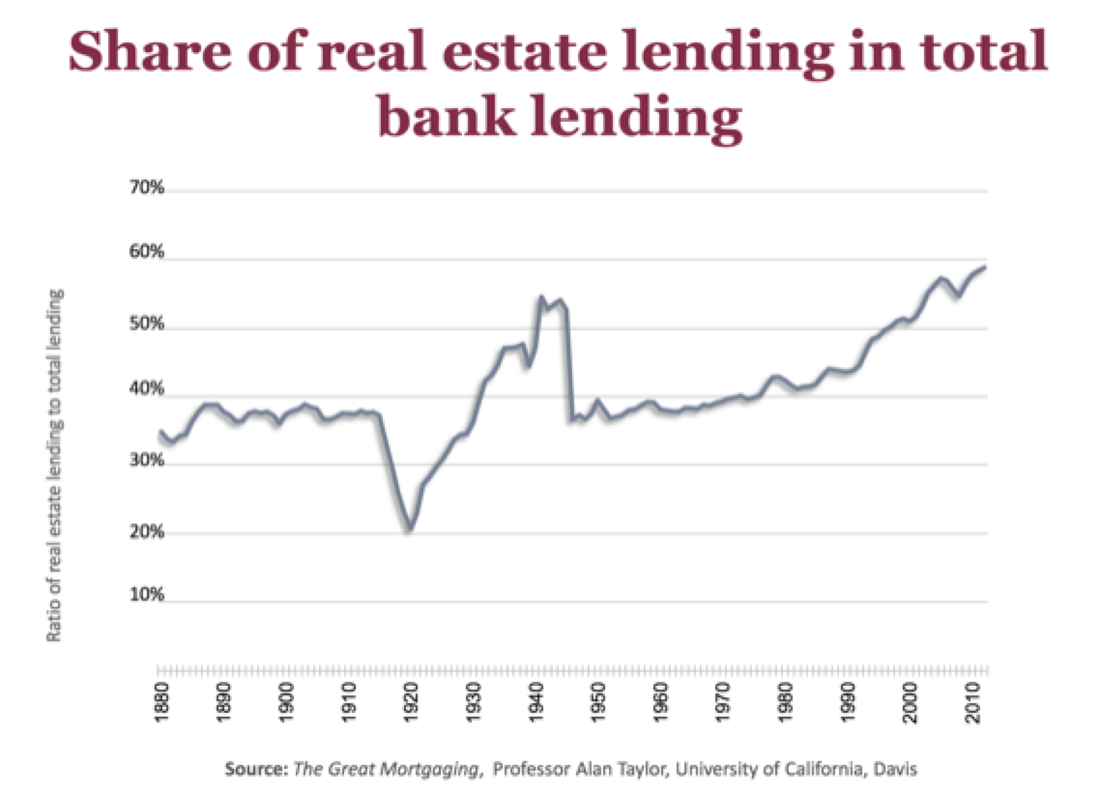

Jordá, Schularick and Taylor[13] (henceforth JST) have recently provided evidence for a long period of leveraging up across OECD countries. The ratio of bank credit to GDP increased in a sample of 17 advanced economies from about 0.5 in the 1930s to more than 1.1 in 2007. Total private domestic credit in advanced economies more than tripled since the 1950s (graph 1). While higher financialization was previously thought to be a positive contributor to economic growth (see Levine)[14], this hypothesis is now increasingly cast into doubt. Knoll, Schularick and Steger[15] have shown that this recent increase in bank credit has come along with large appreciations in housing prices. Contrary to conventional wisdom, housing has historically not been a high-return investment as real housing prices remained relatively stable for almost the entire first part of the 20th century. However, during the second part of the 20th century real housing prices tripled in a sample of 14 advanced economies. Furthermore, JST show that a substantial part of bank lending is now flowing into real estate, almost 60% up from less than 40% in the 1950s (graph 2). This tentative evidence thus suggests a correlation between increased lending and rapidly rising housing prices, a dynamic that has not really been explained by macroeconomists. The profession has also neglected the fact that more than half of bank lending now flows into real estate. Dwellings, of course, provide us with an extremely important service: housing. However, investing into real estate is fundamentally different from investments into other sectors of the economy, especially manufacturing, where large productivity gains resulting from new technology are far more likely (think about robotics, driverless cars, artifical intelligence, etc.). Diverting more than half of bank lending into housing is thus a big deal.

This dynamic might be due to some fundamental structural changes that have taken place in the global economy over the last decades. Agglomeration forces seem to play an increasingly important role. Rural areas and even small towns have lost out in recent decades. The top 30 U.S. cities now produce about 40% of the country’s GDP according to a study by McKinsey[16]. The big metropolitan areas like the Bay Area, L.A. or New York continue to attract a larger population despite the fact that housing prices have become increasingly unaffordable for the middle class.

The nature of investments has also changed in recent decades. First, there has been an increase in desired savings over investment in the global economy as many advanced economies have started to age rapidly. The world is awash in savings with too little investment opportunities, which led to a long-term decline in global real interest rates down to close to 0% nowadays. Investment as a share of GDP has also been declining in many advanced economies. Second, companies in the new economy now require much less investment in physical capital. Take Facebook as an example. The company has little more than 10 000 employees and its physical capital (mostly computers and IT) fits into just a few large office buidlings. Nevertheless, Facebook has a much larger market valuation than a company like General Motors, which has more than 200 000 employees and large manufacturing plants all over the country/world. These two phenomena might be part of the reason for the recent slowdown in global economic growth. This is Lawrence Summers’ hypothesis of “secular stagnation”[17]. Summers[18] also suggested that hysteresis effects might be much more important than commonly assumed. Recessions can thus even affect long-term growth (the trend) via prolonged and elevated levels of unemployment and subdued levels of investment, leading to depreciation of human and physical capital.

Last but not least, macroeconomists have commonly assumed that the factor shares of income, while fluctuating over the business cycle, have stayed relatively constant in the long-run. Recent emperical work by Piketty[19] and Karababournis and Neiman[20], however, has revealed a significant downward trend in the labor share of income over the last couple of decades. This phenomenon is in so far concerning as it exacerbates the recent increases in inequality. Only the very rich derive a substantial part of their income from capital while the middle class and the poor rely almost exclusively on labor income. A fall of the labor share is thus of particular concern because it might reflect stagnating wages as well as a decrease in the bargaining power of labor. Some economists[21] have suggested that the rise in the capital share might be due to increasing monopoly power in the economy, the growing importance of Intellectual Property Rights (IPP) being one example, as well as the substantial appreciation of housing prices, especially in large metropolitan areas.

In his keynote speech in Budapest Lord Turner briefly discussed most of the issues I have raised above. While this blogpost might seem to some as a smashing critique of the economics profession as a whole, this is actually exactly what it is not. It is quite clear that economists like Wicksell, Schumpeter, Kindleberger, Minsky and Co. understood the importance credit and liquidity constraints, the nature of credit and debt, the notion that banks can create purchasing power, and the dynamics of bubbles and financial panics, etc. It is only modern macroeconomic theory that has overlooked many of these aspects by narrowly focusing on mathematically consistent but very abstract theoretical models of the economy.

According to Turner, “new economic thinking” might thus simply involve reading some very old books and bring those ideas back into mainstream macroeconomic theory. This, however, is not the entire story. Some of the aforementioned ideas are relatively new because they reflect economic trends that we have only observed in recent decades. Going forward, I suggest that the following three avenues are of particular importance for macroeconomic research if the goal is to understand recent changes in the global economy:

[1] http://voxeu.org/article/macroeconomics-crisis-irrelevance

[2] http://krugman.blogs.nytimes.com/2009/01/27/a-dark-age-of-macroeconomics-wonkish/

[3] Taleb, Nassim Nicholas. The black swan: The impact of the highly improbable. Random house, 2007.

[4] Shiller, Robert J. Irrational exuberance. Princeton university press, 2015.

[5] Kahneman, Daniel. Thinking, fast and slow. Macmillan, 2011.

[6] Kindleberger, Charles Poor, and Robert O'Keefe. Manias, panics, and crashes. Palgrave Macmillan, 2001.

[7] Reinhart, Carmen M., and Kenneth Rogoff. "This time is different." Eight Centuries of Financial Folly, Princeton University, Princeton and Oxford(2009).

[8] Friedman, Milton, and Anna Jacobson Schwartz. A monetary history of the United States, 1867-1960. Princeton University Press, 2008.

[9] https://barnard.edu/profiles/perry-mehrling

[10] Bagehot, Walter. Lombard Street: A description of the money market. King, 1873.

[11] Schumpeter, Joseph Alois. The theory of economic development: An inquiry into profits, capital, credit, interest, and the business cycle. Vol. 55. Transaction publishers, 1934.

[12] Minsky, Hyman P., and Henry Kaufman. Stabilizing an unstable economy. Vol. 1. New York: McGraw-Hill, 2008.

[13] Jordà, Òscar, Moritz Schularick, and Alan M. Taylor. "The great mortgaging: housing finance, crises and business cycles." Economic Policy 31.85 (2016): 107-152.

[14] Levine, Ross. "Financial development and economic growth: views and agenda." Journal of economic literature 35.2 (1997): 688-726.

[15] http://voxeu.org/article/home-prices-1870

[16] http://www.mckinsey.com/global-themes/urbanization/us-cities-in-the-global-economy

[17] Summers, Laurence H. "Reflections on the ‘New Secular Stagnation Hypothesis’." Secular stagnation: Facts, causes and cures (2014): 27-40.

[18] Fatás, Antonio, and Lawrence H. Summers. "The permanent effects of fiscal consolidations." (2015).

[19] Piketty, Thomas, and L. J. Ganser. "Capital in the twenty-first century." (2014).

[20] Karabarbounis, Loukas, and Brent Neiman. The global decline of the labor share. No. w19136. National Bureau of Economic Research, 2013.

[21] Rognlie, Matthew. "Deciphering the Fall and Rise in the Net Capital Share: Accumulation or Scarcity?." Brookings papers on economic activity 2015.1 (2016): 1-69.

More specifically, New Keynesian DSGE (Dynamic stochastic general equilibrium) models usually contain a number of features that render them more or less useless for understanding the global financial crisis as well as the subdued recovery later on. The foundations of modern macroeconomics have been built on a number of flawed assumptions, the most important ones being listed below:

- The notion that financial markets are complete and efficient.

- The notion that all private agents are always completely rational.

- Most DSGE models only contain homogenous agents. Credit and liquidity constraints of individuals and firms are ruled out by assumption.

- Most DSGE models of the economy do not contain credit, and even more importantly, money. The fact that banks can generate purchasing power by creating credit “out of thin air” is overlooked.

- The notion that fluctuations in the business cycle has no impact on long-run economic growth (the classical dichotomy).

- Modern macroeconomics does not give any importance to land and housing prices.

- Macroeconomics abstracts from changes in the factor shares of income as a result of structural changes in the economy, potentially caused by changes in monopoly power (markups) of firms.

Lord Turner points out that new economic thinking, ironically, might involve reading old books. It is a sad state of affairs that an entire discipline seems to have regressed in recent decades, the dark age of macroeconomics, according to Paul Krugman[2]. He refers to the fact that a lot of concepts and old knowledge seems to have forgotten recently in the quest of finding more and more mathematically fancy but relatively useless models of the macroeconomy. The attempt to build all models on solid microfoundations has led the profession astray.

The notion that financial markets are complete is obviously ridiculous once you think a little bit more carefully about the issue. This assumption posits that we can attach a certain probability to all future states of nature and, even more importantly, that we can obtain insurance against all possible contingencies. Macroeconomic models based on Arrow-Debreu’s concept of general equilibium thus completely rule out Knightian uncertainty, the notion that some risk is simply immeasurable and consequently impossible to calculate. There is, of course, no insurance market for immeasurable risk. Financial markets will thus always be incomplete because they simply cannot provide insurance against what Nassim Taleb[3] has dubbed “Black Swans”, low-probablity, high-impact events that randomly shock the global economy.

The rationality of financial markets is, of course, another assumption that must be called into question. Robert Shiller[4] has received the Nobel prize in economics in 2013 for his recent work on speculative bubbles. He has found significant evidence for substantial mispricing of assets in financial markets in times of exuberant speculative behavior. As such, extremely high price to earnings ratios that cannot be explained by economic fundamentals are a good indicator of financial bubbles and even are to a certain extent a predictor of future returns, which should not be the case if the efficient market hyothesis were true.

The field of behavioral economics also has made enormous progress in certain areas, revealing to what extent individuals behave irrationally at times, contrary to the claim of neoclassical economics. Economists like the Nobel prize winner Daniel Kahneman[5] have extensively studied a variety of cognitive biases that indiviuals tend to display in their decision-making process in a great many situations. Unfortunately, the findings of behavioral finance and behavioral economics have not made it so far into the standard framework of macroeconomics. The most obvious problem is that irrational behavior is by definition more or less erratic, which makes it impossible for macreconomists to incorporate it into standard economic models. The solution for the field of macroeconomics so far thus has been to ignore all the aforementioned findings altogether. This, however, is not a feasible strategy for the future if modern macroeconomics wants to remain relevant for the real world instead of merely being a pseudo-science that economists quibble over in their ivory towers of academia.

Earlier generations of economists were, of course, painfully aware of some of these facts. Charles Kindleberger[6] has described in a detailed analysis the history of manias, panics and crashes in financial markets over the last couple of hundred years. Since the creation of modern financial markets in pre-industrial Europe, panics and crashes have indeed been occuring on a regular basis. Unfortunately, humans tend to have a short-term memory, thus creating the possibility for financial cycles. The excesses and the follies of the older generations are simply forgotten as new cohorts take over, believing that “this time truly is different”[7], which of course it isn’t.

The most problematic omission of modern macroeconomics, however, is the elimination of money and credit from standard models. Ever since the work of Friedman and Schwartz[8] if not before, economists have known that a substantial part of the business cycle fluctuations is due to monetary disturbances. Unfortunately, there is a branch of macroeconomics that has developed in recent decades that denies the existence of nominal shocks altogether. Real Business Cycle theory maintains that recessions are the result of technological shocks, or even more ridiculously, an increased preference for leisure. According to this logic, the Great Depression should be renamed the “Great Vacation”.

Amazingly, even the so-called New Keynesian models commonly used by Central Banks, which do not deny the existence of nominal shocks, do not contain any money, at least not explicitly. The only monetary transmission mechanism these models allow come from changes in the interest rate. The interest rate is not the price of money though, it is the price of credit and/or the return of capital (there are obviously many different interest rates in the economy, another omission made by New Keynesian models). The price of money is the inverse of the price level, i.e. how much real resources you can buy with your money. Inflation in the New Keynesian model is is usually determined by two variables only: inflation expectations as well as the size of the output gap. The Central Bank simply adjusts the interest rate in accordance with the Taylor rule, responding to deviations from the inflation target and the natural level of output. The quantity of base money in the economy as well as other broader monetary aggregates are completely left out. Monetary shocks, changes in the demand and supply for money, are thus ruled out by assumption and do not play any role in the determination of wages and prices. Milton Friedman is probably spinning in his grave.

Simple New Keynesian models also abstract from credit and liquidity constraints. This is, of course, highly problematic. “Liquidity kills you quick”, as Perry Mehrlig[9] points out. Even firms and hosueholds that are otherwise solvent can run into trouble in times of crisis if their source of income/funding dries up. During periods of acute financial distress, it might be impossible to sell what are otherwise highy valuable assets because markets are completely frozen. Furthermore, banks and other financial institutions might be unwilling to lend out any money because counterparty risk is perceived as too high. The fundamental property of credit is that it is very similar to money, but that during times of crisis its quality can quickly deteriorate. All debt is not created equal. Debt of advanced economies (which can issue their own money) is regarded as safe as it can get. Corporate debt and household debt, on the other hand, is a different story. This is what makes credit so dangerous. During good times, I might be able to issue an IOU (a debt obligation) worth 1000 dollars in order to buy goods from one merchant. He will accept my IOU if he knows that I am good for my money. More importantly, if this is common knowledge in my town, then the merchant can pass on the IOU to another person. The IOU is now a piece of paper equivalent to money, which circulates in the economy. However, this equilibrium might be fragile. During times of high economic distress people might suddenly question my solvency. The IOU is now worth much less because debt obligations are not accpeted as valid payment anymore. The only thing that now counts is “real money”, pieces of paper issued by the government (or deposits). The last person who accpeted my IOU is now literally the sucker. He can only come back to me. However, during a crisis I might now truly be liquidity constraint or even insolvent, in which case said person is sitting on a piece of paper that does not have any value. As the “quality” of debt quickly deteriorates in periods of financial distress, pieces of paper that were formerly seen as highly liquid and basically equivalent to money might suddenly become practically worthless. In such a case, the Central Bank has to assume its function as lender of last resort. The Central Bank (and the federal government) are now the only entities that can issue safe assets, money and government debt, respectively. They can issue “government money” and lend it out against collateral in order to prevent a liquidty freeze in the financial system and a total meltdown of the economy. This is to a big extent, of course, exactly what the FED did during the financial crisis of 2008/2009, and rightly so. Note, however, that such implications could not be drawn from most modern models of the economy. Instead, the prescription came more or less right out of Walter Bagehot’s[10] “Lombard Street” in which he describes London’s financial panic of 1866 as well as the somewhat tentative response of the Bank of England.

Modern macroeconomics also neglects the fact that banks can create credit “out of thin air”. Banks are obviously profit maximizers and do not operate in a vacuum. Financial instituions have to take economic conditions into account and will not expand their balance sheet ad infinitum. Regardless, the issuance of new credit involves the creation of additional purchasing power, a point that was already well understood by Schumpeter[11]. Minsky[12] wrote extensively about credit and its role in creating an unstable economy by generating a financial cycle: After a period of increasing leverage the financial bubble would burst, followed by a prolonged time of deleveraging after which the cycle would repeat itself. Rising asset prices in the buildup phase would contribute to the issuance of new credit, which in turn further supports the price appreciation of said assets.

Jordá, Schularick and Taylor[13] (henceforth JST) have recently provided evidence for a long period of leveraging up across OECD countries. The ratio of bank credit to GDP increased in a sample of 17 advanced economies from about 0.5 in the 1930s to more than 1.1 in 2007. Total private domestic credit in advanced economies more than tripled since the 1950s (graph 1). While higher financialization was previously thought to be a positive contributor to economic growth (see Levine)[14], this hypothesis is now increasingly cast into doubt. Knoll, Schularick and Steger[15] have shown that this recent increase in bank credit has come along with large appreciations in housing prices. Contrary to conventional wisdom, housing has historically not been a high-return investment as real housing prices remained relatively stable for almost the entire first part of the 20th century. However, during the second part of the 20th century real housing prices tripled in a sample of 14 advanced economies. Furthermore, JST show that a substantial part of bank lending is now flowing into real estate, almost 60% up from less than 40% in the 1950s (graph 2). This tentative evidence thus suggests a correlation between increased lending and rapidly rising housing prices, a dynamic that has not really been explained by macroeconomists. The profession has also neglected the fact that more than half of bank lending now flows into real estate. Dwellings, of course, provide us with an extremely important service: housing. However, investing into real estate is fundamentally different from investments into other sectors of the economy, especially manufacturing, where large productivity gains resulting from new technology are far more likely (think about robotics, driverless cars, artifical intelligence, etc.). Diverting more than half of bank lending into housing is thus a big deal.

This dynamic might be due to some fundamental structural changes that have taken place in the global economy over the last decades. Agglomeration forces seem to play an increasingly important role. Rural areas and even small towns have lost out in recent decades. The top 30 U.S. cities now produce about 40% of the country’s GDP according to a study by McKinsey[16]. The big metropolitan areas like the Bay Area, L.A. or New York continue to attract a larger population despite the fact that housing prices have become increasingly unaffordable for the middle class.

The nature of investments has also changed in recent decades. First, there has been an increase in desired savings over investment in the global economy as many advanced economies have started to age rapidly. The world is awash in savings with too little investment opportunities, which led to a long-term decline in global real interest rates down to close to 0% nowadays. Investment as a share of GDP has also been declining in many advanced economies. Second, companies in the new economy now require much less investment in physical capital. Take Facebook as an example. The company has little more than 10 000 employees and its physical capital (mostly computers and IT) fits into just a few large office buidlings. Nevertheless, Facebook has a much larger market valuation than a company like General Motors, which has more than 200 000 employees and large manufacturing plants all over the country/world. These two phenomena might be part of the reason for the recent slowdown in global economic growth. This is Lawrence Summers’ hypothesis of “secular stagnation”[17]. Summers[18] also suggested that hysteresis effects might be much more important than commonly assumed. Recessions can thus even affect long-term growth (the trend) via prolonged and elevated levels of unemployment and subdued levels of investment, leading to depreciation of human and physical capital.

Last but not least, macroeconomists have commonly assumed that the factor shares of income, while fluctuating over the business cycle, have stayed relatively constant in the long-run. Recent emperical work by Piketty[19] and Karababournis and Neiman[20], however, has revealed a significant downward trend in the labor share of income over the last couple of decades. This phenomenon is in so far concerning as it exacerbates the recent increases in inequality. Only the very rich derive a substantial part of their income from capital while the middle class and the poor rely almost exclusively on labor income. A fall of the labor share is thus of particular concern because it might reflect stagnating wages as well as a decrease in the bargaining power of labor. Some economists[21] have suggested that the rise in the capital share might be due to increasing monopoly power in the economy, the growing importance of Intellectual Property Rights (IPP) being one example, as well as the substantial appreciation of housing prices, especially in large metropolitan areas.

In his keynote speech in Budapest Lord Turner briefly discussed most of the issues I have raised above. While this blogpost might seem to some as a smashing critique of the economics profession as a whole, this is actually exactly what it is not. It is quite clear that economists like Wicksell, Schumpeter, Kindleberger, Minsky and Co. understood the importance credit and liquidity constraints, the nature of credit and debt, the notion that banks can create purchasing power, and the dynamics of bubbles and financial panics, etc. It is only modern macroeconomic theory that has overlooked many of these aspects by narrowly focusing on mathematically consistent but very abstract theoretical models of the economy.

According to Turner, “new economic thinking” might thus simply involve reading some very old books and bring those ideas back into mainstream macroeconomic theory. This, however, is not the entire story. Some of the aforementioned ideas are relatively new because they reflect economic trends that we have only observed in recent decades. Going forward, I suggest that the following three avenues are of particular importance for macroeconomic research if the goal is to understand recent changes in the global economy:

- The significant appreciation of land and housing prices in large metropolitan areas (agglomeration effects) as well as the interaction between credit and housing prices.

- The decline in the labor share of income, possibly related to housing and increasing monopoly power, and its distributional consequences for society at large.

- The decline in the desired level of investment and the secular fall in real interest rates as well as its impact on asset prices.

[1] http://voxeu.org/article/macroeconomics-crisis-irrelevance

[2] http://krugman.blogs.nytimes.com/2009/01/27/a-dark-age-of-macroeconomics-wonkish/

[3] Taleb, Nassim Nicholas. The black swan: The impact of the highly improbable. Random house, 2007.

[4] Shiller, Robert J. Irrational exuberance. Princeton university press, 2015.

[5] Kahneman, Daniel. Thinking, fast and slow. Macmillan, 2011.

[6] Kindleberger, Charles Poor, and Robert O'Keefe. Manias, panics, and crashes. Palgrave Macmillan, 2001.

[7] Reinhart, Carmen M., and Kenneth Rogoff. "This time is different." Eight Centuries of Financial Folly, Princeton University, Princeton and Oxford(2009).

[8] Friedman, Milton, and Anna Jacobson Schwartz. A monetary history of the United States, 1867-1960. Princeton University Press, 2008.

[9] https://barnard.edu/profiles/perry-mehrling

[10] Bagehot, Walter. Lombard Street: A description of the money market. King, 1873.

[11] Schumpeter, Joseph Alois. The theory of economic development: An inquiry into profits, capital, credit, interest, and the business cycle. Vol. 55. Transaction publishers, 1934.

[12] Minsky, Hyman P., and Henry Kaufman. Stabilizing an unstable economy. Vol. 1. New York: McGraw-Hill, 2008.

[13] Jordà, Òscar, Moritz Schularick, and Alan M. Taylor. "The great mortgaging: housing finance, crises and business cycles." Economic Policy 31.85 (2016): 107-152.

[14] Levine, Ross. "Financial development and economic growth: views and agenda." Journal of economic literature 35.2 (1997): 688-726.

[15] http://voxeu.org/article/home-prices-1870

[16] http://www.mckinsey.com/global-themes/urbanization/us-cities-in-the-global-economy

[17] Summers, Laurence H. "Reflections on the ‘New Secular Stagnation Hypothesis’." Secular stagnation: Facts, causes and cures (2014): 27-40.

[18] Fatás, Antonio, and Lawrence H. Summers. "The permanent effects of fiscal consolidations." (2015).

[19] Piketty, Thomas, and L. J. Ganser. "Capital in the twenty-first century." (2014).

[20] Karabarbounis, Loukas, and Brent Neiman. The global decline of the labor share. No. w19136. National Bureau of Economic Research, 2013.

[21] Rognlie, Matthew. "Deciphering the Fall and Rise in the Net Capital Share: Accumulation or Scarcity?." Brookings papers on economic activity 2015.1 (2016): 1-69.

Source: Lord Turner’s keynote speech at the INET conference in Budapest.

Source: Lord Turner’s keynote speech at the INET conference in Budapest.

RSS Feed

RSS Feed