Nope, this is not some kind of nationalist slogan to buy American products only. Instead, it is an endorsement of Jeffrey Frankel’s extremely thoughtful proposition that the ECB should buy U.S. government bonds, and preferably lots of them.

(http://www.project-syndicate.org/commentary/jeffrey-frankel-urges-the-ecb-to-buy-us-treasuries-to-expand-the-monetary-base).

But before I elaborate, I will quote Brad DeLong who explains what most people, including some economists, don’t understand, namely what a demand-side recession really is:

(http://www.project-syndicate.org/commentary/jeffrey-frankel-urges-the-ecb-to-buy-us-treasuries-to-expand-the-monetary-base).

But before I elaborate, I will quote Brad DeLong who explains what most people, including some economists, don’t understand, namely what a demand-side recession really is:

As any monetarist will tell you (whether you want them to or not), an economic recession is an episode in which less money is supplied than the economy’s decision-makers wish to hold at full employment. In such a case, the consequence is a “general glut”: a critical mass attempt to cut their total spending below their incomes as they try to build up their money balances with no counterbalancing mass trying to spend more than their incomes, but such my spending is your income the result is depression. An excess demand for money accompanied, by virtue of Walras’s Law, by an excess supply of pretty much everything else. This process can be interrupted only if the system “prints” the extra money decision-makers want to hold. The banking system can print “inside” money–if it dares, and if decision-makers trust it enough to classify transferable banking-sector liabilities as means of payment. The central bank can print “outside” money. Or we can wait, mired in depression, until price levels fall enough to raise real balances supplied to a sufficient level.

A demand-side recession is thus a period in which there is an excess demand for money. Private agents wish to increase their money balances and thus decrease their spending on goods and services, which are just two sides of the same coin. Obviously, the result is a recession if a sufficient number of agents decrease their spending simultaneously. This is in effect simply a coordination failure on the macroeconomic level, which can be fixed rather easily by the government. The Central Bank can simply resolve this technical failure and print the additional money that economic agents wish to hold in order to stop the decrease in nominal spending that occurs in the economy (monetary policy).

Alternatively, the government can stop the shortfall in spending by simply increasing its own expenditures in order to offset the decrease in private sector spending (fiscal policy).

Finally, a combination of monetary and fiscal policy is obviously also possible, and sometimes the most desirable option. It certainly would have helped in recent years on both sides of the Atlantic (U.S. and Eurozone).

Note how a demand-side recession has nothing to do with any of the factors that European policy makers have so far identified as the main culprits of the current Eurozone crisis. There is no need for negative productivity shocks, decreases in competitiveness, slowdown in technological change, and the like. A recession can simply occur if a critical mass of private agents suddenly has an increased preference for money balances, resulting in a decrease in nominal spending in the economy.

This is exactly what happened in the Eurozone where spending has been extremely low for years, leading to below target inflation rates. This is especially a problem for the Southern European countries, which suffer from serious debt overhangs (both the public and the private sector). Somewhat higher inflation rates would be extremely helpful to reduce the burden of debt, increase aggregate demand and reduce mass unemployment. For that reason, the ECB should implement a Quantitative Easing program, buying U.S. government bonds in the order of magnitude of around 30 to 60 billion Euros, potentially. This would also drive down the value of the Euro and positively affect aggregate demand and the inflation rate in the Eurozone. The current strength of the Euro comes from its scarcity, i.e. high demand relative to supply, and the ECB is the only one who can and should resolve this situation. Indeed, it has actually an obligation to fulfill its mandate of price stability (defined as 2% inflation), which for some reason it violated in recent years.

In what follows, I will use the fairly technical portfolio balance model, as expounded in Pilbeam’s textbook ‘International Finance’, to demonstrate why a purchase of U.S. government securities might be preferable to buying domestic bonds from Eurozone member states.

The fundamental assumption of the portfolio balance model is that foreign and domestic bonds are not perfect substitutes. There must be a perceived difference in risk between foreign and domestic bonds and investors are required to be risk-averse. Both assumptions are very likely to hold in practice. Even within the Eurozone, we have seen large differences in government bond yields over the last couple of years due to the existence of a risk premium (consider the yield difference between German and Spanish bonds, for example). The same reasoning obviously applies to differences in between Spanish (or any other European government bond) and U.S. bonds.

In what follows, I will treat the Eurozone as ‘home’ and the U.S. as ‘foreign’. The exchange rate S is measured in units of domestic currency per unit of foreign currency (i.e. €/$). A higher S thus implies a depreciation of the euro.

The existence of a risk premium implies the following equation for returns:

Alternatively, the government can stop the shortfall in spending by simply increasing its own expenditures in order to offset the decrease in private sector spending (fiscal policy).

Finally, a combination of monetary and fiscal policy is obviously also possible, and sometimes the most desirable option. It certainly would have helped in recent years on both sides of the Atlantic (U.S. and Eurozone).

Note how a demand-side recession has nothing to do with any of the factors that European policy makers have so far identified as the main culprits of the current Eurozone crisis. There is no need for negative productivity shocks, decreases in competitiveness, slowdown in technological change, and the like. A recession can simply occur if a critical mass of private agents suddenly has an increased preference for money balances, resulting in a decrease in nominal spending in the economy.

This is exactly what happened in the Eurozone where spending has been extremely low for years, leading to below target inflation rates. This is especially a problem for the Southern European countries, which suffer from serious debt overhangs (both the public and the private sector). Somewhat higher inflation rates would be extremely helpful to reduce the burden of debt, increase aggregate demand and reduce mass unemployment. For that reason, the ECB should implement a Quantitative Easing program, buying U.S. government bonds in the order of magnitude of around 30 to 60 billion Euros, potentially. This would also drive down the value of the Euro and positively affect aggregate demand and the inflation rate in the Eurozone. The current strength of the Euro comes from its scarcity, i.e. high demand relative to supply, and the ECB is the only one who can and should resolve this situation. Indeed, it has actually an obligation to fulfill its mandate of price stability (defined as 2% inflation), which for some reason it violated in recent years.

In what follows, I will use the fairly technical portfolio balance model, as expounded in Pilbeam’s textbook ‘International Finance’, to demonstrate why a purchase of U.S. government securities might be preferable to buying domestic bonds from Eurozone member states.

The fundamental assumption of the portfolio balance model is that foreign and domestic bonds are not perfect substitutes. There must be a perceived difference in risk between foreign and domestic bonds and investors are required to be risk-averse. Both assumptions are very likely to hold in practice. Even within the Eurozone, we have seen large differences in government bond yields over the last couple of years due to the existence of a risk premium (consider the yield difference between German and Spanish bonds, for example). The same reasoning obviously applies to differences in between Spanish (or any other European government bond) and U.S. bonds.

In what follows, I will treat the Eurozone as ‘home’ and the U.S. as ‘foreign’. The exchange rate S is measured in units of domestic currency per unit of foreign currency (i.e. €/$). A higher S thus implies a depreciation of the euro.

The existence of a risk premium implies the following equation for returns:

If domestic bonds (eurozone) are regarded as more risky than foreign bonds and if the domestic interest rate is 5%, the foreign interest rate (U.S.) 2%, and the expected depreciation of the Euro is 2%, then there is 1% risk premium on the domestic currency, i.e. the Euro.

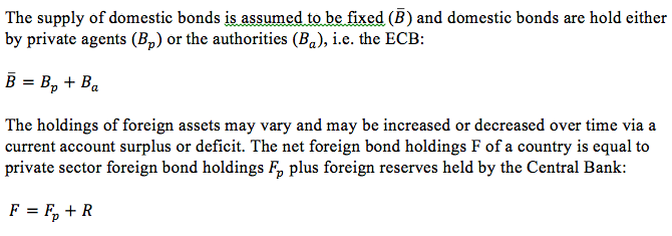

The model assumes that there are three different assets that are hold in the portfolio of private agents and authorities: domestic monetary base M, domestic bonds denoted in domestic currency B, and foreign bonds denoted in foreign currency F.

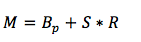

For the Central Bank, just as for any other bank, assets must equal liabilities. The domestic monetary base liability of the Central Bank must thus be equal to its domestic bond holdings plus foreign reserves, valued at market exchange rate S:

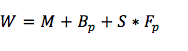

Total private sector financial wealth W at any point in time is given by total bond holdings (both domestic and foreign) plus domestic monetary base:

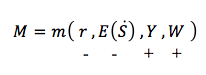

We now come to the demand functions for the different asset classes. Private sector demand for money, domestic bonds, and foreign bonds are given by the following functions, respectively:

The private sector demand for money is a function of the domestic interest rate, the expected rate of depreciation, domestic nominal income Y, and domestic financial wealth. Money demand is negatively related to the interest rate and the expected return of foreign assets, and positively related to domestic income and wealth. An increase in the interest or the expected return on foreign bonds thus decreases money demand (higher opportunity costs) whereas higher income and wealth increase money demand (higher transaction demand).

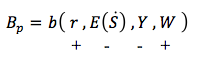

The demand to hold domestic bonds as a proportion of private wealth is positively related to the domestic interest rate and domestic wealth, and negatively related to the expected return on foreign bonds and domestic income:

The demand to hold domestic bonds as a proportion of private wealth is positively related to the domestic interest rate and domestic wealth, and negatively related to the expected return on foreign bonds and domestic income:

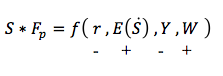

The demand to hold foreign bonds as a proportion of private wealth is positively related to the expected return on foreign bonds and domestic wealth, and negatively related to the domestic interest rate and nominal income:

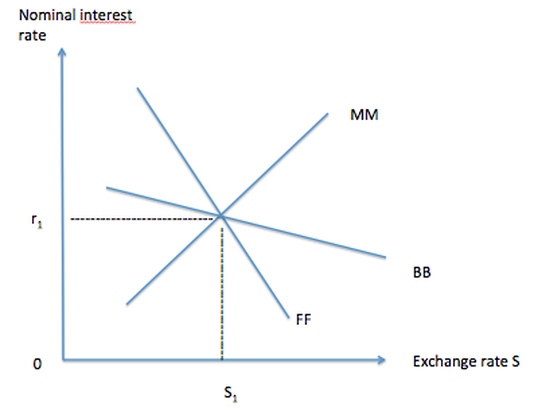

Given these three demand functions for the different asset classes, it is possible to mathematically derive the money market schedule MM, the bond market schedule BB, and the foreign bond market schedule FF, which I will not do here. The graphical analysis is shown below:

The money market schedule MM depicts all possible combinations of the exchange rate and interest rate in which the money market is in equilibrium, i.e. money demand equals money supply. Similarly, the BB schedule and the FF schedule depict all possible combinations of the exchange rate and interest rate in which the domestic bond market and the foreign bond market are in equilibrium (demand = supply), respectively.

The economy is in equilibrium at point A when all three asset markets clear at the appropriate domestic interest rate and exchange rate.

The MM curve is upward sloping. An increase of the exchange rates (depreciation) raises financial wealth and thus increases the demand for money. For a given stock of money, this increased demand can only be offset by a higher interest rate.

The BB curve is downward sloping. A depreciation of the currency raises financial wealth and thus increases the demand for domestic bonds. Given the existing stock of domestic bonds, the increased demand can only be offset by a lower interest rate to make the bonds less attractive to investors.

Finally, the FF curve is also downward sloping. An increase in domestic interest rates makes foreign bonds relatively less attractive. Investors will thus sell off foreign bonds to purchase domestic bonds, leading to an appreciation of the domestic currency (a fall in the exchange rate S).

The difference in the slope of the BB and FF schedule reflects the fact that private agents regard domestic bonds and foreign bonds as imperfect substitutes. The demand for domestic bonds is responsive to changes in the interest rate than the demand for foreign bonds.

With the setup of the model, it is now finally possible to analyze the short-run effect of three different operations the Central Bank can engage in:

1. Open market operation (OMO):

Buying or selling domestic bonds.

2. Foreign exchange operation (FXO):

Buying or selling foreign bonds.

3. Sterilized foreign exchange operation (SFXO):

Buying or selling domestic bonds while selling or buying foreign bonds at the same time to leave the Central Bank’s total monetary base liability unchanged.

Open Market Operation (OMO):

With an expansionary OMO, the Central Bank buys domestic bonds. It thus increases the private sector holdings of money and decreases its holdings of domestic bonds by an equivalent amount. For a given exchange rate, a higher stock of money requires a fall in the domestic interest rate to be willingly held, leading to a rightward shift of the MM curve. A lower stock of domestic bonds at a given exchange rate also requires a fall in the interest rate, leading to a leftward shift of the BB curve.

An expansionary OMO creates an excess supply of money in agents’ portfolios, which leads to an increased demand for both domestic and foreign bonds. This, in turn, lowers the domestic interest rate and leads to a depreciation of the currency (see below).

The economy is in equilibrium at point A when all three asset markets clear at the appropriate domestic interest rate and exchange rate.

The MM curve is upward sloping. An increase of the exchange rates (depreciation) raises financial wealth and thus increases the demand for money. For a given stock of money, this increased demand can only be offset by a higher interest rate.

The BB curve is downward sloping. A depreciation of the currency raises financial wealth and thus increases the demand for domestic bonds. Given the existing stock of domestic bonds, the increased demand can only be offset by a lower interest rate to make the bonds less attractive to investors.

Finally, the FF curve is also downward sloping. An increase in domestic interest rates makes foreign bonds relatively less attractive. Investors will thus sell off foreign bonds to purchase domestic bonds, leading to an appreciation of the domestic currency (a fall in the exchange rate S).

The difference in the slope of the BB and FF schedule reflects the fact that private agents regard domestic bonds and foreign bonds as imperfect substitutes. The demand for domestic bonds is responsive to changes in the interest rate than the demand for foreign bonds.

With the setup of the model, it is now finally possible to analyze the short-run effect of three different operations the Central Bank can engage in:

1. Open market operation (OMO):

Buying or selling domestic bonds.

2. Foreign exchange operation (FXO):

Buying or selling foreign bonds.

3. Sterilized foreign exchange operation (SFXO):

Buying or selling domestic bonds while selling or buying foreign bonds at the same time to leave the Central Bank’s total monetary base liability unchanged.

Open Market Operation (OMO):

With an expansionary OMO, the Central Bank buys domestic bonds. It thus increases the private sector holdings of money and decreases its holdings of domestic bonds by an equivalent amount. For a given exchange rate, a higher stock of money requires a fall in the domestic interest rate to be willingly held, leading to a rightward shift of the MM curve. A lower stock of domestic bonds at a given exchange rate also requires a fall in the interest rate, leading to a leftward shift of the BB curve.

An expansionary OMO creates an excess supply of money in agents’ portfolios, which leads to an increased demand for both domestic and foreign bonds. This, in turn, lowers the domestic interest rate and leads to a depreciation of the currency (see below).

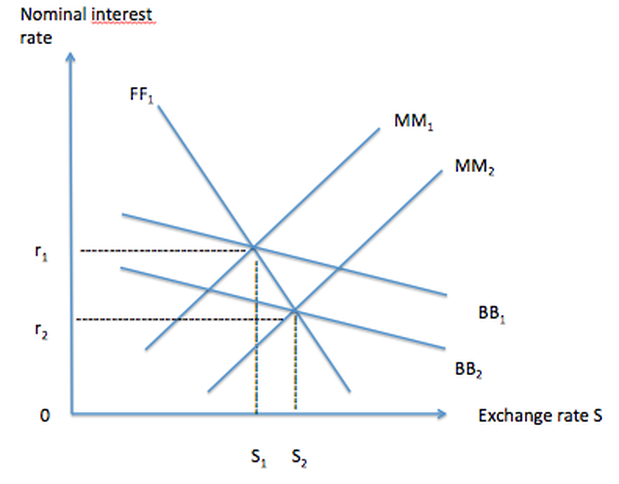

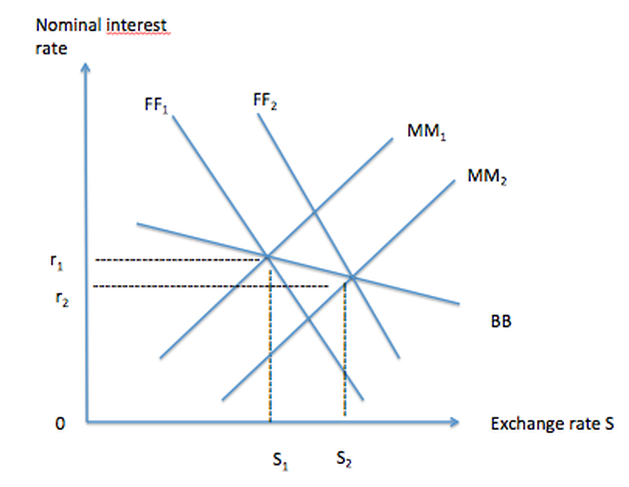

Foreign exchange Operation (FXO):

With an expansionary FXO, the Central Bank increases the stock of currency by buying foreign bonds. For a given exchange rate, a decrease in the supply of foreign bonds requires an increase in the domestic interest rate for foreign bonds to be willingly held, implying a rightward shift of the FF schedule. An expansionary FXO thus creates an excess supply of money and a shortage of foreign bonds in agents’ portfolios, requiring a fall in the interest rate and a depreciation of the exchange rate (see below).

With an expansionary FXO, the Central Bank increases the stock of currency by buying foreign bonds. For a given exchange rate, a decrease in the supply of foreign bonds requires an increase in the domestic interest rate for foreign bonds to be willingly held, implying a rightward shift of the FF schedule. An expansionary FXO thus creates an excess supply of money and a shortage of foreign bonds in agents’ portfolios, requiring a fall in the interest rate and a depreciation of the exchange rate (see below).

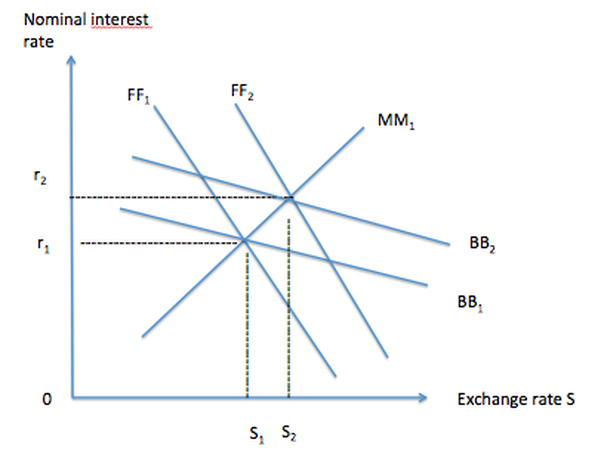

Sterilized Foreign Exchange Intervention (SFXO):

In a SFXO, the Central Bank buys (or sells) foreign bonds while selling (buying) domestic bonds so that the monetary base is unchanged. Since the Central Bank does not change the monetary stock, the MM curve does not shift. If the Central Bank buys foreign bonds and sells domestic bonds, both the FF curve and the BB curve will shift to the right. The Central bank thus creates a shortage of foreign bonds in agents’ portfolios, which requires a depreciation of the exchange rate to achieve the desired foreign bond holdings. The excess supply of domestic bonds requires a rise of the domestic interest rate to make the bonds more attractive to investors so that they are willingly held (see below).

In a SFXO, the Central Bank buys (or sells) foreign bonds while selling (buying) domestic bonds so that the monetary base is unchanged. Since the Central Bank does not change the monetary stock, the MM curve does not shift. If the Central Bank buys foreign bonds and sells domestic bonds, both the FF curve and the BB curve will shift to the right. The Central bank thus creates a shortage of foreign bonds in agents’ portfolios, which requires a depreciation of the exchange rate to achieve the desired foreign bond holdings. The excess supply of domestic bonds requires a rise of the domestic interest rate to make the bonds more attractive to investors so that they are willingly held (see below).

Comparison of OMO, FXO and SFXO:

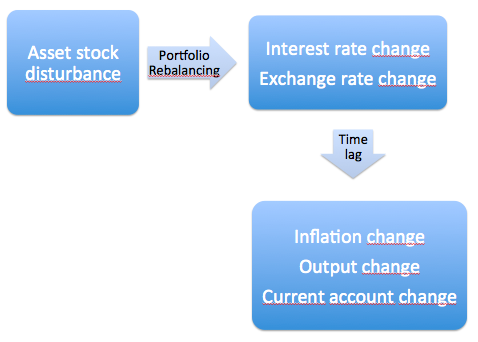

Any of these three operations a Central Bank can engage in will lead to an asset stock disturbance in financial markets. As the Central Bank buys or sells domestic or foreign bonds, private agents will rebalance their asset portfolio and buy or sell bonds (domestic or foreign) on their own. It is this rebalancing of portfolios which immediately affects the domestic interest rate and the exchange rate. However, the process does not stop there. Changes in the interest rate and exchange rate will also affect other economic variables with a time lag, such as the inflation rate, real economic output and the current account, for example.

Any of these three operations a Central Bank can engage in will lead to an asset stock disturbance in financial markets. As the Central Bank buys or sells domestic or foreign bonds, private agents will rebalance their asset portfolio and buy or sell bonds (domestic or foreign) on their own. It is this rebalancing of portfolios which immediately affects the domestic interest rate and the exchange rate. However, the process does not stop there. Changes in the interest rate and exchange rate will also affect other economic variables with a time lag, such as the inflation rate, real economic output and the current account, for example.

The sterilized foreign exchange operation (SFXO) is likely to have the smallest effect on economic output and inflation. That is because the Central Bank leaves domestic money stock unchanged. For that reason, the exchange rate will also depreciate by less than if the Central Bank were only buying foreign bonds without selling domestic bonds (i.e. doing a foreign exchange operation). Furthermore, the impact on inflation and economic output of a SFXO is ambiguous. That is because the rise in domestic interest rate is contractionary whereas the depreciation is expansionary by making domestic goods more competitive.

The open market operation (OMO) and the foreign exchange operation (SFXO) affect the domestic interest rate and the exchange rate in the same direction. The OMO leads to larger fall in domestic interest rates whereas the SFXO leads to a larger fall in the exchange rate. Both of these effects are expansionary. Which of these two operations has a more expansionary effect on output (and inflation) will depend on whether domestic output is more responsive to changes in the interest rate or changes in the exchange rate. Interest rate changes primarily affect investment whereas exchange rate changes will affect the current account.

The Eurozone suffers at the moment from extremely low inflation rates and the ECB’s interest rate is already close to zero. Under current conditions, it is likely that the FXO will have a more expansionary effect. The portfolio balance model illustrates that a purchase of foreign bonds (U.S. government bonds, for example) will have a bigger effect on the exchange rate compared to a purchase of domestic bonds in the same order of magnitude. A large deprecation of the Euro will lead to a higher rate of inflation, thus bringing about a decrease in the real interest rate, which will have an expansionary effect on output.

Jeffrey Frankel’s proposal to buy U.S. bonds (instead of Japanese bonds, for example) stems from the fact that the U.S. bond market is the largest and most liquid market in the world. This is necessary since the ECB likely has to purchase a significant quantity of bonds (in the order of magnitude of dozens of billions of Euros per month) to induce significant changes in the exchange rate and economic output.

Furthermore, buying American bonds has also has the obvious advantage that the ECB can avoid all the political discourse that is associated with buying some European government bonds. Since Eurobonds do not exist, the ECB would have to decide on which European government bonds it should buy and in what quantities. Buying peripheral debt will lead to large opposition from Germany (and others), which will bring the issue of debt monetization and moral hazard. This can hopefully be avoided by buying U.S. debt instead. The ECB should thus engage in a large foreign exchange operation so that it can finally fulfill its mandate of price stability, which it has so forcefully neglected in recent years.

The open market operation (OMO) and the foreign exchange operation (SFXO) affect the domestic interest rate and the exchange rate in the same direction. The OMO leads to larger fall in domestic interest rates whereas the SFXO leads to a larger fall in the exchange rate. Both of these effects are expansionary. Which of these two operations has a more expansionary effect on output (and inflation) will depend on whether domestic output is more responsive to changes in the interest rate or changes in the exchange rate. Interest rate changes primarily affect investment whereas exchange rate changes will affect the current account.

The Eurozone suffers at the moment from extremely low inflation rates and the ECB’s interest rate is already close to zero. Under current conditions, it is likely that the FXO will have a more expansionary effect. The portfolio balance model illustrates that a purchase of foreign bonds (U.S. government bonds, for example) will have a bigger effect on the exchange rate compared to a purchase of domestic bonds in the same order of magnitude. A large deprecation of the Euro will lead to a higher rate of inflation, thus bringing about a decrease in the real interest rate, which will have an expansionary effect on output.

Jeffrey Frankel’s proposal to buy U.S. bonds (instead of Japanese bonds, for example) stems from the fact that the U.S. bond market is the largest and most liquid market in the world. This is necessary since the ECB likely has to purchase a significant quantity of bonds (in the order of magnitude of dozens of billions of Euros per month) to induce significant changes in the exchange rate and economic output.

Furthermore, buying American bonds has also has the obvious advantage that the ECB can avoid all the political discourse that is associated with buying some European government bonds. Since Eurobonds do not exist, the ECB would have to decide on which European government bonds it should buy and in what quantities. Buying peripheral debt will lead to large opposition from Germany (and others), which will bring the issue of debt monetization and moral hazard. This can hopefully be avoided by buying U.S. debt instead. The ECB should thus engage in a large foreign exchange operation so that it can finally fulfill its mandate of price stability, which it has so forcefully neglected in recent years.

RSS Feed

RSS Feed