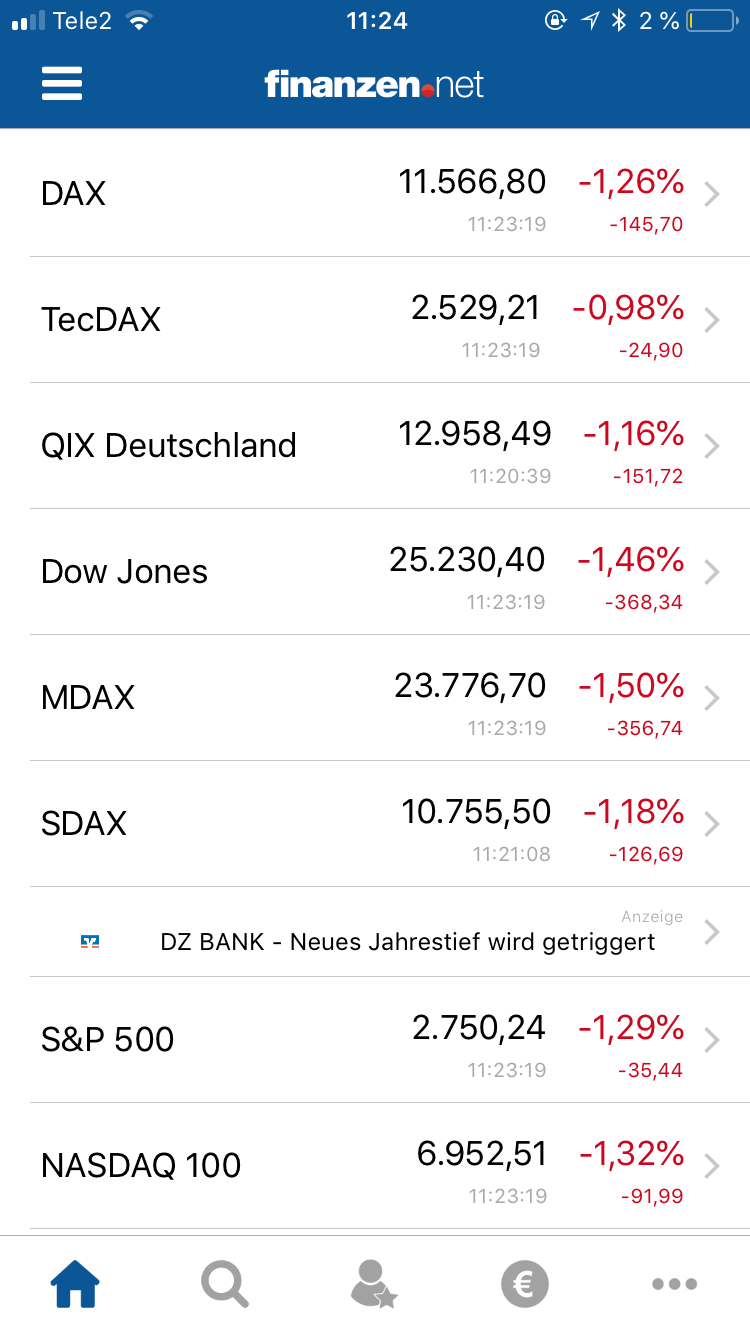

Stock markets took a really big hit yesterday with the Dow Jones and S&P 500 falling by more than 3%. Stock markets also fell in Asia and Europe and are in the red today again across most advanced economies (see below).

It is not entirely clear to me what exactly precipitated this selloff. The first thing to remember is that the stock market is not the economy. Equities can crash without dragging the macroeconomy down with them like in 1987. However, it helps if the Central Bank does its job and stabilizes aggregate demand. In that case, a more accommodative monetary policy can offset all the negative effects of a market selloff.

The projections for quarterly GDP for the US economy for the third quarter look extremely good with the Atlanta GDP Nowcast now forecasting a growth rate of just about 4%. While the New York Fed's Nowcast model predicts only 2.8%, the Atlanta model has historically been more accurate. Moreover, most private forecasters now expect a growth rate of more than 3% as well.

While the Fed was widely expected to raise rates one more time by the end of the year, the current stock market turmoil might actually lead to a different path of rate hikes now. However, this is far from certain. A significant portion of the stock market is hold by the top 10%, who have a very low marginal propensity to consume.

Ultimately, a temporary selloff will only have very limited effects on the macroeconomy since it is not supposed to affect consumption or investment decisions in any significant matter. While there is a case to be made that American equities were already highly valued, please don't buy into the popular bubble theories since most of them are wrong. In the world of low global real interest rates we live in, asset prices are supposed to be high, even from a fundamental value perspective, since all future cash flows are discounted at a very low rate. Furthermore, even ex-post, it is not always easy to identify bubbles.

Of course now, after one decade, the US interest rates are finally starting to edge higher, both at the short end as well as at the long end of the yield curve. Part of this has to do with Trump's 1 trillion dollar tax cut, which has led to a significant increase in yields of US treasuries. This massive economic stimulus, while leading to somewhat higher growth in the very short-run, has forced the Fed to raise rates at a faster rate to offset the effect since they do not want to be in charge of an overheating economy.

It is feasible that the concerns about rising interest rates and the flattening of the yield curve combined with high equity valuations to begin with have now lead to market jitters. Ultimately, only time can tell how this selloff will affect the macroeconomy. Note that US Treasury yields are down from just a few days ago. The price of Bitcoin has declined as well, pointing towards a risk-off moment in financial markets.

While the Fed has ample room to counter a negative macroeconomic shock, there is some concern that they might not be willing to do so, given that they just recently managed to raise interest rates for the first time in a decade. Regardless, as of right now, the growth projections for quarter 3 and quarter 4 for the US economy still look extremely solid, and so does the labor market. This is definitely not the time to worry yet. My best guess is that this selloff will be relatively benign, just as the stock market jitters we had in the beginning of the year. But only time will tell.

It is not entirely clear to me what exactly precipitated this selloff. The first thing to remember is that the stock market is not the economy. Equities can crash without dragging the macroeconomy down with them like in 1987. However, it helps if the Central Bank does its job and stabilizes aggregate demand. In that case, a more accommodative monetary policy can offset all the negative effects of a market selloff.

The projections for quarterly GDP for the US economy for the third quarter look extremely good with the Atlanta GDP Nowcast now forecasting a growth rate of just about 4%. While the New York Fed's Nowcast model predicts only 2.8%, the Atlanta model has historically been more accurate. Moreover, most private forecasters now expect a growth rate of more than 3% as well.

While the Fed was widely expected to raise rates one more time by the end of the year, the current stock market turmoil might actually lead to a different path of rate hikes now. However, this is far from certain. A significant portion of the stock market is hold by the top 10%, who have a very low marginal propensity to consume.

Ultimately, a temporary selloff will only have very limited effects on the macroeconomy since it is not supposed to affect consumption or investment decisions in any significant matter. While there is a case to be made that American equities were already highly valued, please don't buy into the popular bubble theories since most of them are wrong. In the world of low global real interest rates we live in, asset prices are supposed to be high, even from a fundamental value perspective, since all future cash flows are discounted at a very low rate. Furthermore, even ex-post, it is not always easy to identify bubbles.

Of course now, after one decade, the US interest rates are finally starting to edge higher, both at the short end as well as at the long end of the yield curve. Part of this has to do with Trump's 1 trillion dollar tax cut, which has led to a significant increase in yields of US treasuries. This massive economic stimulus, while leading to somewhat higher growth in the very short-run, has forced the Fed to raise rates at a faster rate to offset the effect since they do not want to be in charge of an overheating economy.

It is feasible that the concerns about rising interest rates and the flattening of the yield curve combined with high equity valuations to begin with have now lead to market jitters. Ultimately, only time can tell how this selloff will affect the macroeconomy. Note that US Treasury yields are down from just a few days ago. The price of Bitcoin has declined as well, pointing towards a risk-off moment in financial markets.

While the Fed has ample room to counter a negative macroeconomic shock, there is some concern that they might not be willing to do so, given that they just recently managed to raise interest rates for the first time in a decade. Regardless, as of right now, the growth projections for quarter 3 and quarter 4 for the US economy still look extremely solid, and so does the labor market. This is definitely not the time to worry yet. My best guess is that this selloff will be relatively benign, just as the stock market jitters we had in the beginning of the year. But only time will tell.

RSS Feed

RSS Feed