I've been engaging myself in Fed bashing on this blog for a couple of years now. For example, I've been extremely concerned about the fact that the Fed has been so eager to start a monetary tightening cycle despite the fact that inflation has been undershooting the target for several years in a row now. Furthermore, given lacklustre nominal wage growth, it seems that the labor market is not back to full employment. However, nobody does the art of Fed bashing better than Brad DeLong who believes just as I that institutional change is needed. A good and credible economic forecast should, on average, overestimate half the time and undershoot half the time. DeLong points out that the Fed has now overestimated the strength of the U.S. economy for 11 years in a row now. If the forecast was a coin toss, we now would have had eleven heads in a row. The odds of this happening is one in 2048. Year after year, the Fed has overestimated the strength of the recovery as well as the pace of the tightening cycle. Back in December 2015, for example, the Fed hiked the interest rate for the first time. Their baseline estimate was that over the subsequent two and a half years they would be able to hike another 8 times so that the federal funds rate would reach about 2.25% by September 2017. Instead, they only managed to pull of three rate hikes instead of 8. In the beginning of this year they finally thought they might manage to pull off four rate hikes this year, but at the current pace of the economic expansion this seems highly doubtful. Market participants (as measured by Fed funds futures) think that there is less than a 40% chance of an interest rate increase at the December meeting this year.

Again, we see that the economy is just not ready for such a rapid tightening phase and inflation continues to undershoot their target.

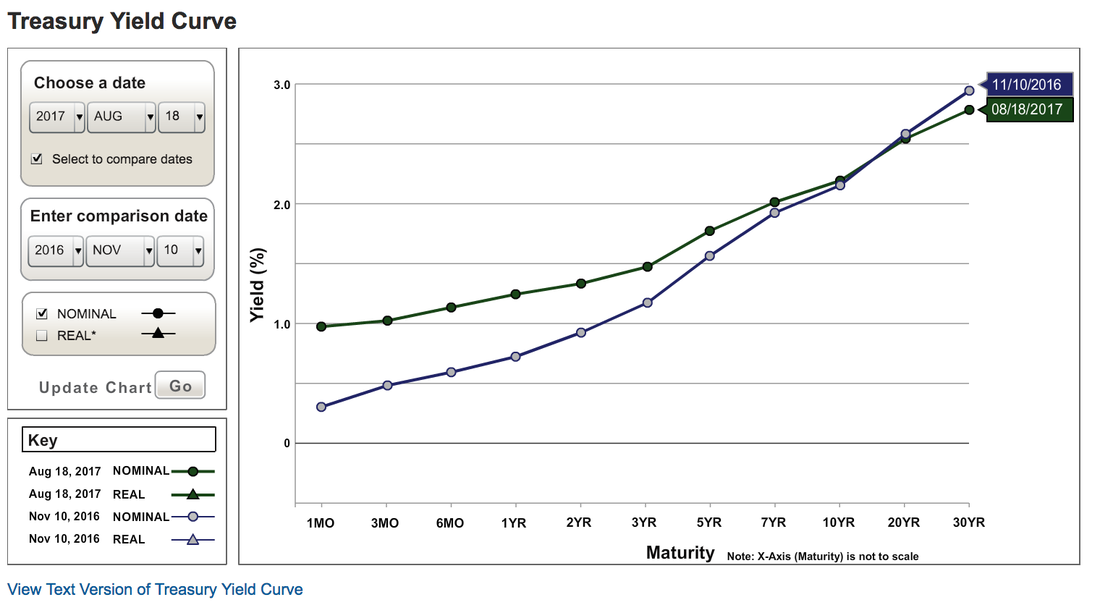

But even if you think that the economy is at full employment and that a tightening cycle should begin, there is a good chance to believe that the Fed is doing the tightening all wrong. The graph below shows the yield curve for U.S. treasuries.

Again, we see that the economy is just not ready for such a rapid tightening phase and inflation continues to undershoot their target.

But even if you think that the economy is at full employment and that a tightening cycle should begin, there is a good chance to believe that the Fed is doing the tightening all wrong. The graph below shows the yield curve for U.S. treasuries.

We can see that the yield curve is substantially flatter than last winter. That is because the Fed hiked rates once, thus raising yields on the short end of the curve. On the other hand, the bond market now believes that the future growth prospect and the inflation outlook for the U.S. economy is somewhat dimmer than just a few months ago, thus lowering yields at the long end of the curve. This is not very surprising given that the Trump administration has proven to be more incompetent than most people had imagined.

The flattening of the yield curve potentially spells trouble ahead. A flat yield curve or even inverted yield curve is one of the best predictors of recessions. Furthermore, a flat yield might also be problematic for the banking sector as it squeezes financial profits. Banks engage in maturity transformation. They borrow short and lend long, making money on the spread. A flat yield curve makes this business unprofitable. Given that the Fed still has a very large balance sheet, it is not entirely clear to me why they want to raise the Federal funds rate first and thus raise short-term rates in the current environment.

If they think that some tightening is needed, then why not leave the Federal funds rate low and sell assets from their balance sheet instead. This would raise yields at the long end and would thus lead to a steeper yield curve.

However, in my humble opinion any tightening at the moment is simply not warranted. Larry Summers secular stagnation hypothesis has so far been proven correct. Most advanced economies find themselves currently in low-growth, low-inflation, and low interest rates regime. Central banks have been adding fuel to the fire by tightening prematurely despite the fact that economic conditions simply do not warrant it.

Update: I wrote this post a while ago. It turns out that over the last few months Fed officials have come around and made it clear that they also want to shrink the balance sheet by selling in the very near future. It is currently expected that some balance sheet action might start this winter. Given the fact that inflation continues to be well below target, some of the doves at the Fed have recently questioned the desirability of further tightening. Finally some good news.

PS: Central Bank incompetence is in my opinion one of the biggest problem of our days. While Trump might do some damage to in the long-run to the U.S. economy, job creation has been exactly the same as under Obama. Presidents have little influence on the economy. the fed determines the rate of inflation in the economy and the pace of job creation. The Fed has also been responsible for the lacklustre recovery. Moreover, most modern recessions have been directly or indirectly caused by the Fed. As Rudi Dornbusch once said:

"Expansions don't die of old age. Every single one of them was murdered by the Fed."

RSS Feed

RSS Feed