From time to time I engage in the art of forecasting on this blog. Obviously, every so often it also occurs that I'm flat out wrong. After the Trump election I predicted that the dollar might soon appreciate and reach parity with the euro. While at first we did see some modest appreciation of the dollar vis-a-vis the Euro, the greenback has now depreciated to almost 1.20 USD (up from about 1.10 USD half a year ago). This obviously begs the question why my prediction was wrong.

Back in the fall of last year I reasoned that the dollar would appreciate based on the following assumptions:

First, I thought that the U.S. economy would grow faster than the Eurozone based on the fact that potential GDP growth in the U.S. should be higher, While this is probably true in the long-run, especially because of more favorable demographics, the Eurozone has been outpacing the U.S. in terms of growth rates. This is mainly due to the fact that the ECB 's monetary policy is still quite accommodative while the Fed has started a tightening cycle about 2 years ago. Output gaps in the Eurozone are also higher. Thus countries like Spain have been enjoying growth rates above 3% over the last couple of years as a result of monetary accommodation by the ECB (Quantitative Easing and negative interest rates).

Second, I thought that given that the Republicans dominate both Congress and the Senate, that there is a decent chance that Trump's infrastructure stimulus plan would go through. It is now obvious that the current administration is the most incompetent administration that country has seen in a very long time. The current U.S. government is completely dysfunctional, which is not very surprising since the Republican party has been hijacked by crooks and hacks a long time ago.

Higher U.S. growth rates combined with the Trump infrastructure plan should have led to a more rapid tightening cycle by the Fed. The divergence between U.S. interest rates and interest rates in the rest of the world should then have led to some further dollar appreciation.

It is now clear that this has not happened. There is good chance that there will basically be no infrastructure stimulus plan under Trump. Furthermore, U.S. growth rates continue to disappoint. As a result, the tightening by the Fed has been anything but rapid, more like glacial.

Last but not least, one should note that the Euro depreciated substantially from about 1.40 USD in 2014 to almost 1.10 USD in early 2015 as a result of the introduction of Quantitiative Easing by the ECB. In accordance with Dornbusch's overshooting model, we should have expected that the Euro depreciated to a lower level than it's long-run equilibrium, which is determined by Purchasing Power Parity (PPP). We should thus have expected that this initial short-run depreciation was larger than required and that in the medium to long-run the Euro would make up some of its losses and revert back to PPP. It seems to me that this is happening now.

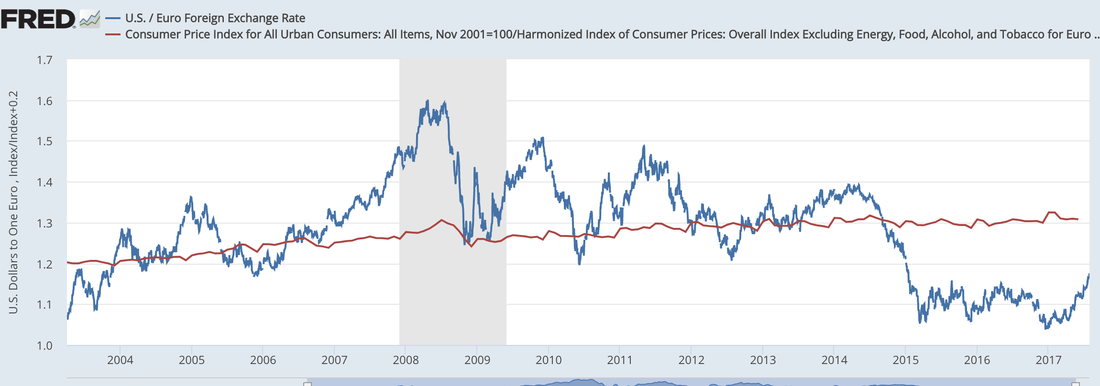

The graph below depicts the US dollar-Euro exchange rate. I also included a line which depicts the ratio of the two price levels, i.e. a measure of Purchasing Power Parity. I simply assumed that PPP was holding around 2004. This is a somewhat arbitrary assumption. However, it seems to me that the PPP line drawn somewhere in the range of 1.2 to 1.3 looks like a good approximation since the exchange rate consistently reverted back to the line for almost a decade.

By that measure, it looks like the euro still seems to be undervalued compared to the dollar even at the current exchange rate of 1.2.

I am currently not in the mood to do another failed prediction, but there is a good case to be made that we will see some further dollar depreciation (vis-a-vis the euro) in the short to medium run based on PPP.

PS: One last piece of advice. Exchange rates pretty much behave like a random walk in the short run, meaning that they are inherently unpredictable: 50% chance of either going up or down, like a coin toss.

Back in the fall of last year I reasoned that the dollar would appreciate based on the following assumptions:

First, I thought that the U.S. economy would grow faster than the Eurozone based on the fact that potential GDP growth in the U.S. should be higher, While this is probably true in the long-run, especially because of more favorable demographics, the Eurozone has been outpacing the U.S. in terms of growth rates. This is mainly due to the fact that the ECB 's monetary policy is still quite accommodative while the Fed has started a tightening cycle about 2 years ago. Output gaps in the Eurozone are also higher. Thus countries like Spain have been enjoying growth rates above 3% over the last couple of years as a result of monetary accommodation by the ECB (Quantitative Easing and negative interest rates).

Second, I thought that given that the Republicans dominate both Congress and the Senate, that there is a decent chance that Trump's infrastructure stimulus plan would go through. It is now obvious that the current administration is the most incompetent administration that country has seen in a very long time. The current U.S. government is completely dysfunctional, which is not very surprising since the Republican party has been hijacked by crooks and hacks a long time ago.

Higher U.S. growth rates combined with the Trump infrastructure plan should have led to a more rapid tightening cycle by the Fed. The divergence between U.S. interest rates and interest rates in the rest of the world should then have led to some further dollar appreciation.

It is now clear that this has not happened. There is good chance that there will basically be no infrastructure stimulus plan under Trump. Furthermore, U.S. growth rates continue to disappoint. As a result, the tightening by the Fed has been anything but rapid, more like glacial.

Last but not least, one should note that the Euro depreciated substantially from about 1.40 USD in 2014 to almost 1.10 USD in early 2015 as a result of the introduction of Quantitiative Easing by the ECB. In accordance with Dornbusch's overshooting model, we should have expected that the Euro depreciated to a lower level than it's long-run equilibrium, which is determined by Purchasing Power Parity (PPP). We should thus have expected that this initial short-run depreciation was larger than required and that in the medium to long-run the Euro would make up some of its losses and revert back to PPP. It seems to me that this is happening now.

The graph below depicts the US dollar-Euro exchange rate. I also included a line which depicts the ratio of the two price levels, i.e. a measure of Purchasing Power Parity. I simply assumed that PPP was holding around 2004. This is a somewhat arbitrary assumption. However, it seems to me that the PPP line drawn somewhere in the range of 1.2 to 1.3 looks like a good approximation since the exchange rate consistently reverted back to the line for almost a decade.

By that measure, it looks like the euro still seems to be undervalued compared to the dollar even at the current exchange rate of 1.2.

I am currently not in the mood to do another failed prediction, but there is a good case to be made that we will see some further dollar depreciation (vis-a-vis the euro) in the short to medium run based on PPP.

PS: One last piece of advice. Exchange rates pretty much behave like a random walk in the short run, meaning that they are inherently unpredictable: 50% chance of either going up or down, like a coin toss.

RSS Feed

RSS Feed