So I have seen some articles recently suggesting that Canada's house price bubble is finally deflating. While house prices are mostly about supply and demand in regional markets, there is no doubt that excessive leverage and financial credit can lead to inflating real estate prices in the short and medium run, especially since house supply is extremely inelastic: It takes time for construction to adjust to rising prices. Moreover, the problem of limited supply is exacerbated by zoning restrictions.

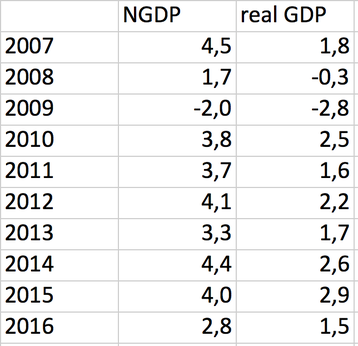

Many people have argued, falsely in my opinion, that the bursting of the housing bubble ultimately led to the financial crisis and the Great Recession in the US. While falling prices were surely one factor, other factors were of far more importance. It is now more or less accepted that monetary policy was far too restrictive in 2008 as the Fed was much more worried about high commodity prices, oil in particular, than falling aggregate demand. Housing prices had been stagnating or already falling for a couple of years before the crisis without having too much of an impact on the broader economy. It was only once the economic downturn became much more severe, that price falls exacerbated, thus leading to a financial crisis and asset price crash, all of which could have been prevented with more expansionary policy in 2008.

One of the main problems with macroeconomics and also the social sciences in general is obviously that we cannot run experiments. Being a student of economic history, one can try to compare historical episodes to each other that are of great similarity and try to reach some conclusions from such a comparative study. For example, the global financial crisis of 2008 was in many ways quite similar to the Great Depression in the 1930s, including its aftermath with many advanced economies suffering from years of economic stagnation (partly due to misguided austerity measures), which ultimately translated into a rise of populism and fascism.

So now it looks like house prices in Canada are falling. As of now, the phenomenon seems to be limited to the big metropolitan areas like Toronto and Vancouver, which have also seen the largest price appreciations in recent years. Average house prices in Toronto, for example, seem to be roughly 15% lower than their peak about 1.5 years ago. Will a nation-wide or even regional house price crash lead to a financial crisis and an economic downturn? Maybe, but I will argue that it's rather unlikely.

Let's consider some necessary conditions for a house price crash to become systemically relevant:

1) Banks are highly leveraged and undercapitalized, meaning that a big asset price crash can easily wipe out their capital. Moreover, as house price owners start to default on their mortgages, banks are seeing a further deterioration of their balance sheet. A financial crisis and a tightening of credit and liquidity can rapidly bring down the economy. The financial system is like the cardiovascular system of the economy. every individual, household and firm relies on the free flow of money and credit for our daily transactions. If the system is clogged, you have a problem: "Liquidity kills you quick!", as Perry Mehrling at INET likes to say.

2) House price owners are highly leveraged, meaning that a large fall in prices wipes out their entire equity.

3) The wealth effect is large: As asset prices decrease, households are cutting back their spending, either by necessity as they were overleveraged or as a precaution (precautionary savings), which translates into a further decline in aggregate demand.

4) There is a high degree of correlation among asset classes, meaning that a large house price correction might also bring about a stock market crash. This can simply be the result of contagion effects or alternatively an effect of the decline in economic activity itself.

5) Monetary policy is either constrained or just falling behind the curve as policy makers might not show the necessary resolve to prevent a large fall in aggregate demand.

Note that all these five conditions were satisfied in the US in 2008. Both households and the financial system were highly leveraged. People were just assuming that the party would go on forever. The Fed was extremely complacent in the beginning of the crisis, thus greatly exacerbating and even causing the downturn. Finally, many households quickly cut back their spending in response to the crisis as millions of jobs quickly evaporated and economy-wide spending went into free fall, which also brought about a spectacular decline in stock market prices.

Now, why do I think that Canada will not suffer a similar fate even if house prices continue to their decline. For starters, note that the Canadian financial system was already much more resilient 10 years ago. Canada was one of the few large advanced economies that did not have a financial crisis even though the economy was affected by the global downturn regardless.

Furthermore, many countries have made sure that the banking system has gradually become more resilient over time as policy makers have imposed higher capital requirements and are stress-testing the banks on a regular basis. Insofar as the house price decline at the moment is affecting the wealthiest parts of the country where the previous house price appreciations have also been the highest over the last decade, falling prices might translate only in a very small decline in aggregate spending if at all (a low wealth effect).

Last but not least, the Bank of Canada should reverse any decline in aggregate spending with a more expansionary monetary policy. While there is some concern that the policy rate right now is only at 1.25%, many studies have shown that alternative policy measures, such as asset purchases (Quantitative Easing) and negative interest rates, can be highly effective at the zero-lower bound.

The bigger concern is that policy makers have been somewhat reluctant to exploit all those alternatives to their full extent because they have been controversial and unpopular as the general public does not understand why and how these policies were implemented.

I could be wrong, but I do strongly belief that even a quite large and even prolonged correction in house prices do not have to translate into a financial crisis and a decline in economic adequate policy measures are taken.

As long as Central Bank's obey Bagehot's rule (lend freely to solvent institutions during times of crisis, but only do so against collateral and at a penalty rate) and ensure adequate levels of aggregate demand, Canada's economy should be just fine. Of course, this also implies that the US crisis of 2008 was really the fault of policy makers and could have been contained much earlier with alternative policy actions.

Many people have argued, falsely in my opinion, that the bursting of the housing bubble ultimately led to the financial crisis and the Great Recession in the US. While falling prices were surely one factor, other factors were of far more importance. It is now more or less accepted that monetary policy was far too restrictive in 2008 as the Fed was much more worried about high commodity prices, oil in particular, than falling aggregate demand. Housing prices had been stagnating or already falling for a couple of years before the crisis without having too much of an impact on the broader economy. It was only once the economic downturn became much more severe, that price falls exacerbated, thus leading to a financial crisis and asset price crash, all of which could have been prevented with more expansionary policy in 2008.

One of the main problems with macroeconomics and also the social sciences in general is obviously that we cannot run experiments. Being a student of economic history, one can try to compare historical episodes to each other that are of great similarity and try to reach some conclusions from such a comparative study. For example, the global financial crisis of 2008 was in many ways quite similar to the Great Depression in the 1930s, including its aftermath with many advanced economies suffering from years of economic stagnation (partly due to misguided austerity measures), which ultimately translated into a rise of populism and fascism.

So now it looks like house prices in Canada are falling. As of now, the phenomenon seems to be limited to the big metropolitan areas like Toronto and Vancouver, which have also seen the largest price appreciations in recent years. Average house prices in Toronto, for example, seem to be roughly 15% lower than their peak about 1.5 years ago. Will a nation-wide or even regional house price crash lead to a financial crisis and an economic downturn? Maybe, but I will argue that it's rather unlikely.

Let's consider some necessary conditions for a house price crash to become systemically relevant:

1) Banks are highly leveraged and undercapitalized, meaning that a big asset price crash can easily wipe out their capital. Moreover, as house price owners start to default on their mortgages, banks are seeing a further deterioration of their balance sheet. A financial crisis and a tightening of credit and liquidity can rapidly bring down the economy. The financial system is like the cardiovascular system of the economy. every individual, household and firm relies on the free flow of money and credit for our daily transactions. If the system is clogged, you have a problem: "Liquidity kills you quick!", as Perry Mehrling at INET likes to say.

2) House price owners are highly leveraged, meaning that a large fall in prices wipes out their entire equity.

3) The wealth effect is large: As asset prices decrease, households are cutting back their spending, either by necessity as they were overleveraged or as a precaution (precautionary savings), which translates into a further decline in aggregate demand.

4) There is a high degree of correlation among asset classes, meaning that a large house price correction might also bring about a stock market crash. This can simply be the result of contagion effects or alternatively an effect of the decline in economic activity itself.

5) Monetary policy is either constrained or just falling behind the curve as policy makers might not show the necessary resolve to prevent a large fall in aggregate demand.

Note that all these five conditions were satisfied in the US in 2008. Both households and the financial system were highly leveraged. People were just assuming that the party would go on forever. The Fed was extremely complacent in the beginning of the crisis, thus greatly exacerbating and even causing the downturn. Finally, many households quickly cut back their spending in response to the crisis as millions of jobs quickly evaporated and economy-wide spending went into free fall, which also brought about a spectacular decline in stock market prices.

Now, why do I think that Canada will not suffer a similar fate even if house prices continue to their decline. For starters, note that the Canadian financial system was already much more resilient 10 years ago. Canada was one of the few large advanced economies that did not have a financial crisis even though the economy was affected by the global downturn regardless.

Furthermore, many countries have made sure that the banking system has gradually become more resilient over time as policy makers have imposed higher capital requirements and are stress-testing the banks on a regular basis. Insofar as the house price decline at the moment is affecting the wealthiest parts of the country where the previous house price appreciations have also been the highest over the last decade, falling prices might translate only in a very small decline in aggregate spending if at all (a low wealth effect).

Last but not least, the Bank of Canada should reverse any decline in aggregate spending with a more expansionary monetary policy. While there is some concern that the policy rate right now is only at 1.25%, many studies have shown that alternative policy measures, such as asset purchases (Quantitative Easing) and negative interest rates, can be highly effective at the zero-lower bound.

The bigger concern is that policy makers have been somewhat reluctant to exploit all those alternatives to their full extent because they have been controversial and unpopular as the general public does not understand why and how these policies were implemented.

I could be wrong, but I do strongly belief that even a quite large and even prolonged correction in house prices do not have to translate into a financial crisis and a decline in economic adequate policy measures are taken.

As long as Central Bank's obey Bagehot's rule (lend freely to solvent institutions during times of crisis, but only do so against collateral and at a penalty rate) and ensure adequate levels of aggregate demand, Canada's economy should be just fine. Of course, this also implies that the US crisis of 2008 was really the fault of policy makers and could have been contained much earlier with alternative policy actions.

RSS Feed

RSS Feed